|

市场调查报告书

商品编码

1910531

脸部认证:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Facial Recognition - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

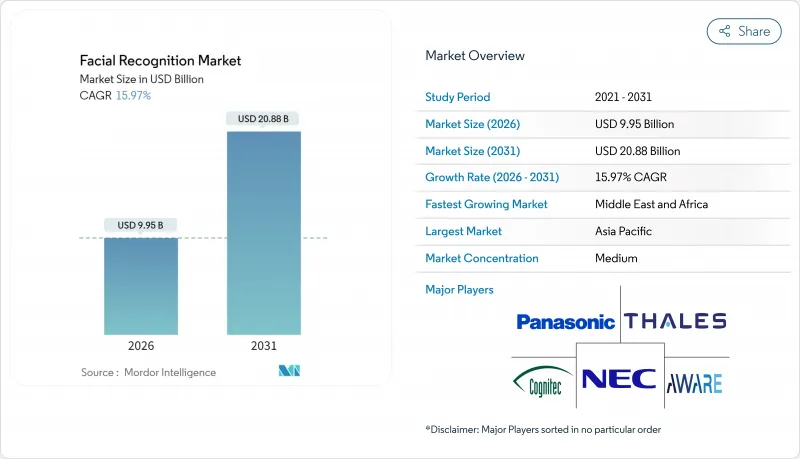

预计脸部辨识市场将从 2025 年的 85.8 亿美元成长到 2026 年的 99.5 亿美元,到 2031 年将达到 208.8 亿美元,2026 年至 2031 年的复合年增长率为 15.97%。

目前的成长依赖于边缘运算架构,该架构能够在亚秒级推理的同时,将生物识别资料保存在设备端,这是诸如中国《脸部辨识技术安全管理方法》等新法规所要求的。欧盟人工智慧法律中严格的使用者同意规则引导欧洲买家选择隐私保护型设计,并鼓励供应商预设整合差分隐私、同态加密和联邦学习等技术。硬体小型化和低功耗人工智慧加速器使得智慧型手机、执法记录器和自助服务终端能够作为註册点,将目标用户群扩展到固定CCTV之外。最后,支付、乘客互动和零售分析等应用程式正在补充传统的安全应用场景,实现收入来源多元化,并平滑各地区的需求週期。

全球脸部辨识市场趋势与洞察

加快新兴亚洲国家采用国民身分证和电子护照的步伐

越南计画在2025年在所有边境生物识别。新加坡的目标是到2026年将樟宜机场免护照通道的等待时间缩短40%,并实现95%的自动化。马来西亚和巴布亚纽几内亚也计划在全国推广生物辨识技术,这将使亚太地区的註册用户总数超过8亿,打造全球最大的设备脸部认证系统测试平台。供应商将获得授权收入和参考架构,这些架构都将影响从非洲到拉丁美洲的公共部门竞标。透过这些计划开发的互通性标准将降低金融服务提供者日后重复使用相同身分钱包时的整合风险。这将带动脸部认证市场对软体、边缘硬体和合规管理服务的结构性需求成长。

基于边缘运算的智慧摄影机在零售连锁店中迅速普及

预计到2024年,美国有组织零售犯罪造成的损失将超过1,000亿美元,这将加速边缘人工智慧摄影机的普及应用。这些摄影机无需将资料传输到云端伺服器即可分析人脸和行为。 Asda与FaceTech合作的试点计画实现了99.992%的准确率,即时删除不匹配的资料以满足GDPR的要求。美国排名前50的杂货店中有15家正在使用脸部辨识技术来辨识惯犯并侦测员工与顾客之间的串通行为(例如「甜心诈骗」)。基于Nvidia Jetson或EdgeCortix SAKURA-II开发板的即时分析可以减少商品损失,并为行销系统产生客户分析数据,从而在几个月内为零售商带来明显的投资收益(ROI)。由于脸部辨识损失预防和个人化客户体验的双重优势,零售业仍是私部门中人脸辨识技术应用成长最快的领域。

更严格的GDPR生物识别同意要求(欧盟27国)

欧盟人工智慧法将远端生物识别列为「高风险」技术,并禁止执法机关即时使用,仅有少数例外情况。该法也禁止在职场使用情绪辨识技术。企业必须进行资料保护影响评估,证明其合法权益,并在存在权力不对等的情况下获得明确同意。随着整合商添加遮罩功能、设备端处理和审核日誌,合规成本将增加20%至30%。虽然开发欧盟相容版本的供应商倾向于在其他市场重复使用隐私纳入设计架构,但随着小型公司选择退出或推迟进入欧洲市场,脸部辨识的近期普及速度正在放缓。

细分市场分析

2025年,随着演算法改进将误报率降低至0.1%以下,软体将占全球收入的57.20%,从而能够在标准CPU上部署。边缘硬体将成为成长最快的细分市场,复合年增长率将达到18.76%,因为金融和医疗保健行业的合规团队要求生物识别模板不得离开办公室。 SAKURA-II晶片能够在10W的功耗预算内运行复杂的模型,从而支援便利商店和交通枢纽的自助服务终端。

基于 API 的授权模式使开发者能够在数小时内将脸部认证功能整合到行动应用中,从而避免了传统承包计划通常需要数年才能完成的週期。同时,供应商将电脑视觉 SDK 与安全元件储存和专用加速器捆绑销售,确保了持续的收入来源,因为每个新的分析模组都以韧体提供。这种双边模式在推动软体普及的同时,也提高了脸部辨识市场的转换成本。

基于现有CCTV基础设施的二维演算法将在2025年占据43.10%的收入份额。然而,能够分析微表情、注意力持续时间和困倦程度的「情绪人工智慧」引擎将以18.11%的复合年增长率成长,从而重塑客户体验和道路安全应用。随着零售商、保险公司和汽车製造商将行为分析洞察转化为实际收益,预计到2031年,基于分析主导模组的脸部辨识市场规模将增加3.4倍。

此混合堆迭将 3D 深度资讯与 2D RGB 帧融合,以防止伪造并实现符合 ISO/IEC 30107-3 标准的生物识别验证。 Suprema 的 Q-Vision Pro 每台机器最多可验证 50,000 个用户,并为所有交易提供端对端加密,使 ATM 运营商能够取消 PIN 码垫片。这种安全和分析技术的结合持续推动着丰富的研发投入,并实现了授权、硬体和服务层面的多元化收入来源。

区域分析

至2025年,亚洲将占NEC总收入的38.25%,这主要得益于各国政府致力于将脸部认证融入数位公共基础设施。中国的「安全管理措施」要求所有储存超过10万个模板的企业向省级网路安全部门註册,这构成了一道筛选门槛,有利于拥有安全供应链的成熟供应商。在2025年日本大阪关西博览会上,NEC的脸部认证支付系统将投入120万参观者使用,这为NEC向东南亚地区拓展出口业务提供了绝佳的示范机会。

预计中东地区将以16.88%的复合年增长率成长,阿联酋的生物辨识身分识别系统将取代银行、医疗保健和公共入口网站的塑胶卡。杜拜机场正计划推出一套无需护照的旅行系统,将乘客的脸部资料与报到和零售钱包连接起来,使该地区成为无摩擦出行的试验场。海湾国家政府正在资助试点项目,并迅速将其转化为国家政策,从而缩短了引进週期,并加快了脸部认证市场供应商的收入成长。

北美地区由于航空公司部署和执法机关预算的重要性,仍占据重要地位,但也面临最高的诉讼风险。儘管客运量增长毋庸置疑,但国会对美国运输安全管理局(TSA)扩张的审查凸显了公民自由的担忧。运输安全局的碎片化导致各州法律五花八门,例如伊利诺伊州的《生物识别资讯隐私法案》(BIPA)和加州的《加州消费者隐私法案》(CPRA),这使得跨州部署变得复杂。欧洲严格的监管虽然减缓了城市即时监控的速度,但也增加了对能够进行设备端编辑和授权管理的边缘设备的需求,从而使隐私技术供应商在脸部辨识行业站稳了脚跟。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 目录

第二章 引言

- 研究假设和市场定义

- 调查范围

第三章调查方法

第四章执行摘要

第五章 市场情势

- 市场驱动因素

- 加快新兴亚洲国家采用国民身分证和电子护照的步伐

- 零售连锁店对边缘智慧摄影机的需求激增

- 北美航空公司将强制使用生物识别登机

- 海湾合作委员会金融科技领域迅速普及脸部认证支付与简易身分验证钱包

- 市场限制

- 更严格的GDPR生物识别同意要求(欧盟27国)

- 美国演算法偏见诉讼风险

- 中国网路安全2.0硬体认证瓶颈

- 市民反对扩大全市监视录影机覆盖范围

- 监理展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第六章 市场规模与成长预测

- 按组件

- 硬体

- 网路摄影机和感测器

- 边缘人工智慧晶片

- 软体

- 脸部侦测和对齐

- 特征提取与匹配

- 活体检测

- 服务

- 託管服务

- 专业服务

- 硬体

- 透过技术

- 二维人脸部认证

- 3D脸部辨识

- 热感/红外线脸部认证

- 脸部分析和情绪人工智慧

- 混合和多模态演算法

- 透过部署

- 本地部署

- 基于云端的

- 边缘/设备端

- 依设备类型

- 固定监视录影机

- 行动和穿戴装置

- 智慧型手机

- 执法记录仪

- 自助服务终端和存取终端

- 透过使用

- 安全与监控

- 边境管制/电子门

- 公共区域CCTV分析

- 存取控制

- 企业和校园入口

- 智慧锁(住宅专用)

- 身份验证/电子KYC

- 数位银行註册

- SIM卡註册

- 支付和交易

- Face Pay(零售POS)

- 客户分析与个人化

- 店内定向广告

- 安全与监控

- 最终用户

- 政府和执法机关

- BFSI

- 零售与电子商务

- 卫生保健

- 汽车/运输设备

- 通讯/IT

- 饭店和娱乐

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- ASEAN

- 澳洲和纽西兰

- 亚太其他地区

- 中东和非洲

- 中东

- GCC

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 中东

- 北美洲

第七章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- NEC Corporation

- Thales Group

- IDEMIA

- Panasonic Corp.

- Aware, Inc.

- Cognitec Systems GmbH

- Face++, Megvii Technology

- SenseTime Holdings

- Clearview AI

- Daon, Inc.

- FacePhi Biometria SA

- AnyVision(now Oosto)

- SAFR(RealNetworks Inc.)

- CyberLink Corp.

- Innovatrics

- Suprema Inc.

- Herta Security

- iProov Ltd.

- Corsight AI

- VisionLabs

第八章:市场机会与未来展望

- 閒置频段与未满足需求评估

The Facial Recognition market is expected to grow from USD 8.58 billion in 2025 to USD 9.95 billion in 2026 and is forecast to reach USD 20.88 billion by 2031 at 15.97% CAGR over 2026-2031.

Growth now relies on edge-based architectures that deliver sub-second inference while allowing biometric data to remain on-device, a requirement embedded in new laws such as China's Security Management Measures for Facial Recognition Technology. Stricter consent rules under the EU AI Act steer European buyers toward privacy-preserving designs, pushing vendors to integrate differential privacy, homomorphic encryption, and federated learning by default. Hardware miniaturization and low-power AI accelerators have turned smartphones, body cameras, and kiosks into enrolment points, broadening the addressable base well beyond fixed CCTV. Finally, payments, passenger facilitation, and retail analytics now complement traditional security use cases, diversifying revenue streams and smoothing demand cycles across regions.

Global Facial Recognition Market Trends and Insights

Accelerating National ID and e-Passport Roll-outs in Emerging Asia

By 2025 Vietnam requires biometric authentication at every border, while Singapore's passport-free lanes at Changi have cut wait times by 40% and target 95% automated use by 2026. Malaysia and Papua New Guinea have scheduled nationwide deployments that push cumulative APAC enrolments above 800 million citizens, creating the world's largest testing ground for on-device facial verification systems. Vendors gain not only licence revenue but also reference architectures that influence public-sector bids from Africa to Latin America. Interoperability standards drafted in these projects reduce integration risk for financial-service players that later reuse the same ID wallets. The result is a structural pull-through for software, edge hardware, and managed compliance services across the facial recognition market.

Soaring Adoption of Edge-Based Smart Cameras in Retail Chains

Organized retail crime exceeded USD 100 billion in the United States in 2024, accelerating deployment of edge AI cameras that analyse faces and behaviours without streaming to cloud servers. Asda's pilot with FaiceTech achieves 99.992% accuracy and deletes non-matches instantly to satisfy GDPR mandates. Fifteen of the top 50 US grocers now use facial recognition to flag repeat offenders and detect employee-customer "sweethearting" fraud. Real-time analytics delivered on Nvidia Jetson or EdgeCortix SAKURA-II boards reduce shrinkage and generate footfall intelligence that feeds marketing systems, giving retailers a hard ROI within months. This twin benefit of loss prevention and experience personalisation keeps retail the fastest-growing private-sector adopter in the facial recognition market.

Strict GDPR Biometric Consent Requirements (EU-27)

The EU AI Act classifies remote biometric identification as "high-risk," banning real-time use for law enforcement except under narrow exemptions and prohibiting emotion recognition at work. Deployers must run Data Protection Impact Assessments, justify legitimate interest, and obtain explicit consent where power imbalances exist. Compliance costs rise 20-30% as integrators add masking, on-device processing, and audit logs. Vendors building EU-ready versions often re-use the privacy-by-design stack for other markets, but smaller firms exit or defer Europe, slowing short-term diffusion of the facial recognition market.

Other drivers and restraints analyzed in the detailed report include:

- Mandated Biometric Boarding by North-American Airlines

- Rapid Uptake of Face Pay and KYC-Lite Wallets in GCC Fintech

- Algorithmic Bias Litigation Risk in the United States

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 57.20% of global revenue in 2025 as algorithmic improvements lowered false accept rates to below 0.1% and enabled deployment on standard CPUs. Edge hardware remains the fastest-growing slice at 18.76% CAGR because compliance teams in finance and healthcare insist that biometric templates never leave the premises. SAKURA-II chips run complex models within 10 W power budgets, making autonomous kiosks viable inside convenience stores and transit hubs.

API-based licensing lets developers embed facial verification into mobile apps in hours, eliminating the multi-year cycles typical of earlier turnkey projects. At the same time, hardware vendors bundle computer-vision SDKs with secure-element storage and dedicated accelerators, locking in annuity streams as every new analytics module becomes a firmware download. This two-sided model keeps software sticky while raising switching costs for the entire facial recognition market.

2-D algorithms still ride on existing CCTV infrastructure and therefore generated 43.10% of 2025 revenue. Yet "emotion AI" engines that map micro-expressions, attention span, or drowsiness will grow at 18.11% CAGR, reshaping customer-experience and road-safety applications. The facial recognition market size for analytics-driven modules is forecast to rise 3.40 X by 2031 as retailers, insurers, and automakers monetise behavioural insights.

Hybrid stacks blend 3-D depth cues with 2-D RGB frames to thwart spoofing and deliver liveness checks that comply with ISO/IEC 30107-3. Suprema's Q-Vision Pro validates up to 50,000 users per device and encrypts every transaction end-to-end, allowing ATM operators to eliminate PIN pads. Such crossover of security and analytics keeps R&D pipelines full and diversifies revenue across licence, hardware, and service layers.

Facial Recognition Market Report is Segmented by Component (Hardware, Software, Services), Technology (2-D, 3-D, Thermal, Facial Analytics, Hybrid), Deployment (On-Premise, Cloud, Edge), Device (Fixed Cameras, Mobile, Smartphones, Kiosks), Application (Security, Identity Verification, Payments), End-User (Government, BFSI, Retail, Healthcare and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD)

Geography Analysis

Asia held 38.25% of 2025 revenue thanks to states that embed facial recognition into digital public infrastructure. China's Security Management Measures force any entity that stores templates for more than 100,000 persons to register with provincial cyber authorities, establishing a vetting hurdle that favours established vendors with secure supply chains. Japan's 2025 Osaka-Kansai Expo will run NEC face-payments for an anticipated 1.2 million visitors, a live showcase that can seed exports across Southeast Asia.

The Middle East will expand at a 16.88% CAGR as UAE's biometric ID replaces plastic cards across banking, healthcare, and public portals. Dubai Airport plans passport-free travel that links passengers' faces to boarding and retail wallets in one corridor, positioning the region as a laboratory for frictionless mobility. Gulf governments bankroll proof-of-concepts and rapidly convert them to nationwide policies, compressing adoption cycles and accelerating revenue capture for suppliers within the facial recognition market.

North America remains pivotal through airline rollouts and law-enforcement budgets but faces the strongest litigation risk. Congressional scrutiny over TSA's expansion highlights civil-liberty concerns even as passenger throughput gains are undeniable. Federal fragmentation spawns a patchwork of state laws Illinois' BIPA, California's CPRA making cross-border deployments complex. Europe's strict regime slows real-time city surveillance but ramps demand for edge devices running on-device redaction and consent management, giving privacy-tech vendors a foothold in the facial recognition industry.

- NEC Corporation

- Thales Group

- IDEMIA

- Panasonic Corp.

- Aware, Inc.

- Cognitec Systems GmbH

- Face++, Megvii Technology

- SenseTime Holdings

- Clearview AI

- Daon, Inc.

- FacePhi Biometria SA

- AnyVision (now Oosto)

- SAFR (RealNetworks Inc.)

- CyberLink Corp.

- Innovatrics

- Suprema Inc.

- Herta Security

- iProov Ltd.

- Corsight AI

- VisionLabs

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Table of Contents

2 INTRODUCTION

- 2.1 Study Assumptions and Market Definition

- 2.2 Scope of the Study

3 RESEARCH METHODOLOGY

4 EXECUTIVE SUMMARY

5 MARKET LANDSCAPE

- 5.1 Market Drivers

- 5.1.1 Accelerating National ID and e-Passport Roll-outs in Emerging Asia

- 5.1.2 Soaring Adoption of Edge-based Smart Cameras in Retail Chains

- 5.1.3 Mandated Biometric Boarding by North-American Airlines

- 5.1.4 Rapid Uptake of Face Pay and KYC-lite Wallets in GCC Fintech

- 5.2 Market Restraints

- 5.2.1 Strict GDPR Biometric Consent Requirements (EU-27)

- 5.2.2 Algorithmic Bias Litigation Risk in the U.S.

- 5.2.3 China Cyber-Security Classified Protection 2.0 Hardware Certification Bottlenecks

- 5.2.4 Public Push-back on City-wide Camera Expansion

- 5.3 Regulatory Outlook

- 5.4 Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Buyers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitutes

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 6.1 By Component

- 6.1.1 Hardware

- 6.1.1.1 Cameras and Sensors

- 6.1.1.2 Edge AI Chips

- 6.1.2 Software

- 6.1.2.1 Face Detection and Alignment

- 6.1.2.2 Feature Extraction and Matching

- 6.1.2.3 Liveness Detection

- 6.1.3 Services

- 6.1.3.1 Managed Services

- 6.1.3.2 Professional Services

- 6.1.1 Hardware

- 6.2 By Technology

- 6.2.1 2-D Facial Recognition

- 6.2.2 3-D Facial Recognition

- 6.2.3 Thermal/Infra-red Facial Recognition

- 6.2.4 Facial Analytics and Emotion AI

- 6.2.5 Hybrid and Multimodal Algorithms

- 6.3 By Deployment

- 6.3.1 On-premise

- 6.3.2 Cloud-based

- 6.3.3 Edge / On-device

- 6.4 By Device Form-factor

- 6.4.1 Fixed Surveillance Cameras

- 6.4.2 Mobile and Wearables

- 6.4.2.1 Smartphones

- 6.4.2.2 Body-worn Cameras

- 6.4.3 Kiosks and Access Terminals

- 6.5 By Application

- 6.5.1 Security and Surveillance

- 6.5.1.1 Border Control / e-Gates

- 6.5.1.2 Public Area CCTV Analytics

- 6.5.2 Access Control

- 6.5.2.1 Corporate and Campus Entry

- 6.5.2.2 Smart Locks (Residential)

- 6.5.3 Identity Verification / e-KYC

- 6.5.3.1 Digital Banking On-boarding

- 6.5.3.2 SIM Registration

- 6.5.4 Payments and Transactions

- 6.5.4.1 Face Pay (Retail POS)

- 6.5.5 Customer Analytics and Personalisation

- 6.5.5.1 In-store Targeted Advertising

- 6.5.1 Security and Surveillance

- 6.6 By End-user

- 6.6.1 Government and Law-Enforcement

- 6.6.2 BFSI

- 6.6.3 Retail and E-commerce

- 6.6.4 Healthcare

- 6.6.5 Automotive and Transportation

- 6.6.6 Telecom and IT

- 6.6.7 Hospitality and Entertainment

- 6.7 By Geography

- 6.7.1 North America

- 6.7.1.1 United States

- 6.7.1.2 Canada

- 6.7.1.3 Mexico

- 6.7.2 South America

- 6.7.2.1 Brazil

- 6.7.2.2 Argentina

- 6.7.2.3 Chile

- 6.7.2.4 Rest of South America

- 6.7.3 Europe

- 6.7.3.1 Germany

- 6.7.3.2 United Kingdom

- 6.7.3.3 France

- 6.7.3.4 Italy

- 6.7.3.5 Spain

- 6.7.3.6 Nordics

- 6.7.3.7 Rest of Europe

- 6.7.4 Asia Pacific

- 6.7.4.1 China

- 6.7.4.2 Japan

- 6.7.4.3 South Korea

- 6.7.4.4 India

- 6.7.4.5 ASEAN

- 6.7.4.6 Australia and New Zealand

- 6.7.4.7 Rest of Asia Pacific

- 6.7.5 Middle East and Africa

- 6.7.5.1 Middle East

- 6.7.5.1.1 GCC

- 6.7.5.1.2 Turkey

- 6.7.5.1.3 Rest of Middle East

- 6.7.5.2 Africa

- 6.7.5.2.1 South Africa

- 6.7.5.2.2 Nigeria

- 6.7.5.2.3 Rest of Africa

- 6.7.5.1 Middle East

- 6.7.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 7.4.1 NEC Corporation

- 7.4.2 Thales Group

- 7.4.3 IDEMIA

- 7.4.4 Panasonic Corp.

- 7.4.5 Aware, Inc.

- 7.4.6 Cognitec Systems GmbH

- 7.4.7 Face++, Megvii Technology

- 7.4.8 SenseTime Holdings

- 7.4.9 Clearview AI

- 7.4.10 Daon, Inc.

- 7.4.11 FacePhi Biometria SA

- 7.4.12 AnyVision (now Oosto)

- 7.4.13 SAFR (RealNetworks Inc.)

- 7.4.14 CyberLink Corp.

- 7.4.15 Innovatrics

- 7.4.16 Suprema Inc.

- 7.4.17 Herta Security

- 7.4.18 iProov Ltd.

- 7.4.19 Corsight AI

- 7.4.20 VisionLabs

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 8.1 White-space and Unmet-Need Assessment

人工智慧脸部辨识市场按组件、技术、应用、部署模式和最终用户产业划分,全球预测(2026-2032年)

人工智慧脸部辨识市场按组件、技术、应用、部署模式和最终用户产业划分,全球预测(2026-2032年) 脸部认证门锁市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能及安装类型划分

脸部认证门锁市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能及安装类型划分 脸部辨识市场-全球产业规模、份额、趋势、机会及预测(依技术、应用、最终用户、地区及竞争格局划分,2021-2031年)

脸部辨识市场-全球产业规模、份额、趋势、机会及预测(依技术、应用、最终用户、地区及竞争格局划分,2021-2031年) 全球脸部辨识市场,2026-2030年RGB-IR脸部辨识模组市场按组件类型、部署模式、应用程式和最终用户划分 - 全球预测(2026-2032年)交流扼流圈市场按产品类型、电感值、磁芯材质、安装方式、频率范围、应用和最终用户划分-2026-2032年全球预测双眼人脸部辨识模组市场:2026-2032年全球预测(按组件、技术、应用和安装环境划分)多因素身份验证解决方案市场按身份验证类型、部署模式、组织规模、垂直行业、组件、应用类型、最终用户和订阅模式划分,全球预测,2026-2032年非接触式指纹辨识设备市场:按最终用户、应用、产品类型、技术、认证模式和部署方式分類的全球预测(2026-2032年)

全球脸部辨识市场,2026-2030年RGB-IR脸部辨识模组市场按组件类型、部署模式、应用程式和最终用户划分 - 全球预测(2026-2032年)交流扼流圈市场按产品类型、电感值、磁芯材质、安装方式、频率范围、应用和最终用户划分-2026-2032年全球预测双眼人脸部辨识模组市场:2026-2032年全球预测(按组件、技术、应用和安装环境划分)多因素身份验证解决方案市场按身份验证类型、部署模式、组织规模、垂直行业、组件、应用类型、最终用户和订阅模式划分,全球预测,2026-2032年非接触式指纹辨识设备市场:按最终用户、应用、产品类型、技术、认证模式和部署方式分類的全球预测(2026-2032年) 脸部辨识市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2026-2034)

脸部辨识市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2026-2034)