|

市场调查报告书

商品编码

1851758

虹膜辨识:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Iris Recognition - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

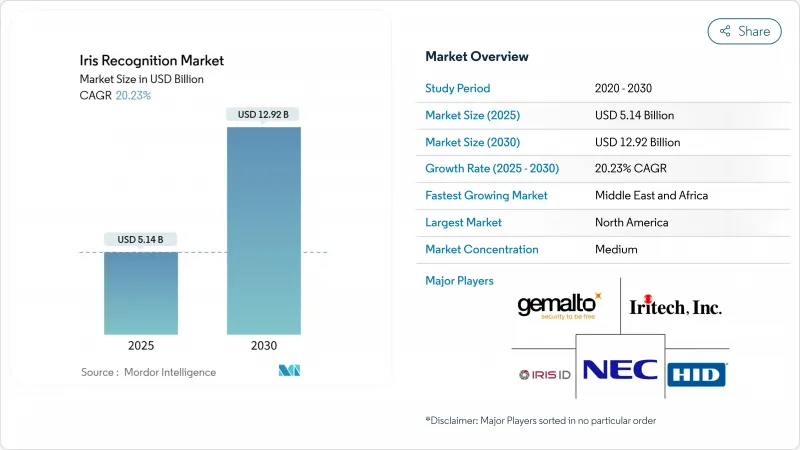

预计到 2025 年,虹膜辨识市场规模将达到 51.4 亿美元,到 2030 年将达到 129.2 亿美元,复合年增长率为 20.23%。

这一强劲的发展轨迹标誌着该技术正从政府的特定部署领域走向日常消费环境。对非接触式身分验证日益增长的需求、网路威胁风险的增加以及监管合规要求的提高,都在加速银行、医疗保健、旅游和消费电子等行业的应用。儘管硬体仍然是最大的成本中心,但随着云端原生匹配引擎速度的提升和中阶买家准入门槛的降低,软体的战略地位正在日益凸显。亚太地区凭藉大规模的国家识别项目获得了先发优势,而中东地区则在机场现代化和旅游业便利化的推动下,实现了最快的复合年增长率。日益激烈的竞争围绕着演算法的准确性、多模态整合以及能够应对不断变化的资料主权规则的以隐私为中心的设计特性。

全球虹膜辨识市场趋势与洞察

亚洲国民身分证和电子护照计画扩展

亚太地区各国政府持续推广虹膜辨识数位身分平台,以简化公共服务流程并促进普惠金融。印度的DigiLocker升级允许企业透过Aadhaar资料库验证员工身份,从而将服务对象扩展到个人公民之外。泰国公共卫生部门正在为外来务工人员部署多模态註册自助服务终端,将虹膜扫描与疫苗接种和福利资格关联起来。随着大规模生产,光学模组的成本已降至个位数美元水平,为预算有限的机构提供了切入点。随着註册势头持续强劲,供应商看到了维护合约和定期感测器更新带来的可持续收入潜力,而这些都得益于性能标准的提升。

增加中东走廊边境管制支出

海湾国家正在大规模部署虹膜辨识,以平衡主要机场的安全阈值和旅客流量目标。阿联酋的eGate专案由IDEMIA公司提供,采用远端虹膜辨识采集技术,无需接触入境柜檯即可完成居民和游客的入境手续。沙乌地阿拉伯的「2030愿景」工作小组要求所有新建航厦都必须配备多模态生物识别,这促使像Invixium这样的供应商致力于建立在地化组装线,以实现快速客製化。因此,采购流程倾向于高通量扫描器和云端匹配引擎,这些设备每小时可处理数千名旅客的入境手续,同时也为入境官员记录审核级别的证据。

机场多模态生物识别枢纽的高额资本支出

机场在对现有查核点进行改造,加装包含虹膜、脸部和指纹辨识等多种功能的多模态安检舱时,前期投入成本较高。运输安全管理局(TSA) 的试点计画显示,此类系统能够提高旅客吞吐量,但需要专用通道、LED 安全照明以及连接至中央匹配引擎的专用光纤回程传输。规模较小的美国机场通常会等到客流量达到投资回报週期后再部署,这迫使供应商采用模组化、计量收费的模式,分两阶段部署。

细分市场分析

由于需要精密的光学元件、可控的照明和坚固耐用的机壳,硬体仍将是虹膜辨识市场的主导力量,预计到2024年将占总收入的73%。然而,随着云端推理引擎提升辨识速度并实现无需大规模更换设备的灵活功能更新,成长动力正逐渐转向软体。系统营运商报告称,摄影机升级週期平均为四到五年,并按季度部署演算法补丁以提高识别精度,以适应不断变化的人口结构。

从2025年到2030年,软体产业的复合年增长率将达到22.8%,凸显了从资本支出模式转向订阅模式的转变。分层架构支援快速部署,以应对不断涌现的新隐私法规,这对医疗保健和金融采购委员会而言是一个重要影响因素。同时,组件供应商正在缩小红外线LED阵列的体积,并应用汽车级耐温等级,以支援在光照条件难以预测的户外环境中更广泛地部署。开放API镜头支援跨模态融合,使操作人员能够将虹膜和脸部影像从单一感测器传输到通用后端。

到2024年,1:N模式将占据虹膜辨识市场66.2%的份额,并广泛应用于边境管制、选民登记和福利发放等领域,这些领域需要处理数百万笔记录的资料库并进行一对多搜寻。各国政府会在旅游旺季投入大量运算预算,检验该架构应对并发查询的能力。

未来五年,一对一检验预计将以20.6%的复合年增长率成长,因为企业和行动钱包供应商将优先考虑快速用户检验而非详尽的去重。便利性也至关重要,因为延迟必须保持在250毫秒以下,以避免用户放弃结帐。欧洲的先驱银行目前正在将虹膜扫描与动态二维码令牌相结合来绑定交易会话,从而在不明显增加用户摩擦的情况下降低网路钓鱼风险。随着这些解决方案的规模化,数据将被反馈到自适应阈值引擎中,以改善不同文化背景用户群体中误报和漏报之间的平衡。

区域分析

到2024年,亚太地区将占全球收入的36%,这主要得益于印度超过12亿公民的Aadhaar识别系统註册以及智慧型手机的快速互动,使得生物识别互动变得普遍。中国行动电话厂商正在将虹膜解锁功能整合到旗舰机型中,以支援支付宝和微信支付等支付方式;而日本NEC公司则正在将其生物辨识技术套件商业化,应用于公共运输和零售自助结帐系统。监管环境的明朗化、行动资料通讯普及率高以及对价格敏感但又精通技术的消费者群体,为持续增长的用户基数创造了有利条件。

中东地区预计到2030年将以21.3%的复合年增长率实现最快增长,这主要得益于海湾机场无缝旅客通道的建设以及各国数位识别蓝图的推进。阿联酋决定逐步淘汰实体ID卡,转而采用脸部认证和虹膜辨识验证,凸显了阿联酋政府摆脱传统卡片的决心。在沙乌地阿拉伯,本地供应商正在联合生产扫描仪,这使得该地区成为需求和生产中心。

欧洲和北美正处于政策需求成熟的阶段。 GDPR 的强制要求推动了对国内云端节点和加密迭加层的投资,这需要采用以隐私为核心的设计架构。美国市场寄望联邦政府为海关和边防安全提供的资金,以扩大虹膜采集试点项目,并升级边境口岸和航空枢纽。由于公民自由组织正在监督部署情况,因此准确的活体检测和透明的审核追踪对于获得公众认可至关重要。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 亚洲国民身分证和电子护照计画扩展

- 增加中东走廊边境管制支出

- 智慧型手机OEM厂商采用设备端虹膜感测器

- 美国医疗保健领域非接触式患者身分识别强制措施的扩展

- 欧盟数位钱包计画加速了电子身分验证(e-KYC)的需求。

- 银行、金融服务和保险业的跨境反洗钱合规

- 市场限制

- 机场多模态生物识别枢纽的高额资本支出

- 非合作捕获场景下的精度劣化

- 资料主权和生物特征模板储存规范(欧盟GDPR)

- 北美公民意识与对自由的反弹

- 价值/供应链分析

- 监理与技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 投资分析

第五章 市场规模与成长预测

- 按组件

- 硬体

- 虹膜扫描仪

- 相机

- 整合虹膜辨识系统

- 其他光学模组和照明

- 软体

- 独立匹配引擎

- SDK 和中介软体

- 云端基础的平台

- 硬体

- 透过身份验证模式

- 1:1检验

- 1:N 歧视

- 透过使用

- 门禁和考勤

- 身分识别和边境管制

- 交易和支付认证

- 病患识别与电子病历集成

- 其他(KYC、监控、车载资讯娱乐系统)

- 按最终用户行业划分

- 政府和执法部门

- 银行、金融服务和保险(BFSI)

- 医疗保健和生命科学

- 消费性电子产品

- 军事/国防

- 旅行和移民

- 商业和公司

- 其他(教育、汽车OEM厂商)

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 新加坡

- 澳洲

- 纽西兰

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 肯亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- NEC Corporation

- IDEMIA

- HID Global(ASSA ABLOY)

- Thales Group(Gemalto)

- Iris ID Inc.

- IriTech Inc.

- EyeLock LLC

- Princeton Identity Inc.

- BioEnable Technologies Pvt. Ltd.

- IrisGuard UK Ltd.

- Aware Inc.

- Vision-Box

- DERMALOG Identification Systems

- Cognitec Systems GmbH

- Smartmatic

- Samsung Electronics Co., Ltd.

- Fujitsu Limited

- CLEAR Inc.

- CMITech Company Ltd.

- SRI International

第七章 市场机会与未来展望

The iris recognition market size stands at USD 5.14 billion in 2025 and is forecast to expand to USD 12.92 billion by 2030, reflecting a compound annual growth rate (CAGR) of 20.23%.

This robust trajectory shows how the technology has moved beyond niche government deployments into everyday consumer environments. Heightened demand for contact-free authentication, rising cyber-threat exposure, and stronger compliance expectations from regulators have all accelerated adoption across banking, healthcare, travel, and consumer electronics. Hardware remains the largest cost center, yet software gains more strategic weight as cloud-native matching engines improve speed and lower entry barriers for mid-sized buyers. Asia-Pacific commands an early-mover advantage through scaled national identity programs, while the Middle East delivers the fastest CAGR on the back of airport modernization and tourism facilitation mandates. Intensifying competition now revolves around algorithmic accuracy, multimodal integration, and privacy-centric design features that can withstand evolving data-sovereignty rules.

Global Iris Recognition Market Trends and Insights

Growing National-ID & e-Passport Programs in Asia

Asia-Pacific governments keep scaling iris-enabled digital identity platforms to streamline public-service delivery and financial inclusion. India's DigiLocker upgrade now allows corporate entities to verify staff credentials through the Aadhaar database, widening the addressable base beyond individual citizens.Thailand's public-health authorities have introduced multimodal enrolment kiosks for migrant workers, linking iris scans to vaccination and benefits eligibility. Optical module costs have fallen toward single-digit USD levels in high-volume production, giving budget-constrained agencies an entry point. As enrollment momentum continues, vendors see durable revenue from maintenance contracts and periodic sensor refresh cycles that follow increased performance standards.

Rising Border-Control Spending Across Middle-East Corridors

Gulf states deploy iris recognition at scale to balance security thresholds with passenger-flow targets in flagship airports. The UAE's eGate program, delivered with IDEMIA, employs iris-at-distance capture to process residents and visitors without touching immigration counters. Saudi Arabia's Vision 2030 task force mandates multimodal biometrics for all new terminals, prompting suppliers such as Invixium to commit to local assembly lines for quicker customization. The resulting procurement pipeline favors high-throughput scanners and cloud-ready matching engines that can clear several thousand travelers per hour while logging audit-grade evidence for immigration officials.

High CAPEX of Multimodal Biometric Hubs at Airports

Airports face steep upfront costs when retrofitting existing checkpoints with multimodal pods that include iris, face, and fingerprint options. U.S. Transportation Security Administration trials show passenger throughput gains yet require specialized lanes, LED-safe lighting, and dedicated fiber backhauls to central matching engines. Smaller regional airports postpone rollouts until passenger volumes justify the payback, creating a two-tier adoption curve that suppliers must navigate with modular, pay-per-use pricing models.

Other drivers and restraints analyzed in the detailed report include:

- Smartphone OEM Adoption of On-Device Iris Sensors

- Expansion of Contactless Patient-ID Mandates in U.S. Healthcare

- Data-Sovereignty & Biometric-Template Storage Regulations (EU GDPR)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware accounted for 73% of 2024 revenue and continues to anchor the iris recognition market, given the need for precision optics, controlled illumination, and rugged housings. Growth, however, shifts toward software as cloud inference engines raise recognition speeds and enable agile feature updates without forklift replacements. System operators report average upgrade cycles of four to five years for cameras, yet deploy quarterly algorithm patches to improve accuracy against evolving demographic mixes.

Software's 22.8% CAGR from 2025-2030 underscores the pivot from capital expenditure to subscription models, letting smaller enterprises trial enterprise-grade accuracy through pay-as-you-go APIs. The layered architecture supports quick rollouts when new privacy mandates emerge, a factor that materially influences procurement committees in health and finance. In parallel, component suppliers miniaturize infrared LED arrays and apply automotive-grade temperature ratings, expanding outdoor deployment windows where lighting is unpredictable. Open-API lenses invite cross-modality fusion, letting operators stream both iris and face images from a single sensor to common back ends.

The 1:N mode represented 66.2% iris recognition market size in 2024, supported by border-control, voter registry, and welfare-benefit rollouts requiring one-to-many searches against multimillion-record galleries. Governments reserve significant compute budgets for peak travel seasons, validating the architecture's resilience for concurrent queries.

Over the next five years, 1:1 verification is expected to record a 20.6% CAGR as corporates and mobile-wallet providers focus on rapid user validation rather than exhaustive de-duplication. The convenience angle resonates where latency must stay below 250 milliseconds to avoid checkout abandonment. Early adopter banks in Europe now pair iris scans with dynamic QR tokens to bind the transaction session, reducing phishing risk without noticeable user friction. As these point solutions scale, they feed data back into adaptive thresholding engines that improve false-accept/false-reject balances across culturally diverse user cohorts.

The Iris Recognition Market Report is Segmented by Component (Hardware, Software), Authentication Mode (1:1 Verification, 1:N Identification), Application (Access Control and Time-Attendance, ID and Border Control, and More), End-User Industry (Government and Law-Enforcement, BFSI, and More), and Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 36% of global revenue in 2024, underpinned by India's Aadhaar enrollment of over 1.2 billion citizens and rapid smartphone penetration that normalizes biometric interactions. Chinese handset vendors bundle iris unlock in flagship models to underpin Alipay and WeChat Pay transfers, while Japan's NEC commercializes its Bio-IDiom suite across transportation and retail self-checkout lanes. Regulatory clarity, strong mobile data coverage, and price-sensitive yet tech-savvy consumers create a fertile setting for sustained installation growth.

The Middle East records the fastest trajectory at 21.3% CAGR through 2030, fueled by Gulf airports' shift to seamless passenger corridors and national digital-ID roadmaps. The UAE's decision to retire physical Emirates ID cards in favor of a facial-and-iris credential highlights the policy's will to leapfrog legacy cards. Saudi Arabia's localization drives push vendors to co-manufacture scanners, positioning the region as both a demand hub and a production base.

Europe and North America display mature yet policy-shaped demand curves. GDPR obligations force privacy-by-design architectures, prompting greater investment in in-country cloud nodes and encryption overlays. The U.S. market banks on federal funding to update border checkpoints and aviation hubs, with Customs and Border Protection extending iris capture pilots to additional crossings. Civil-liberties groups monitor deployments, so accurate liveness detection and transparent audit trails are critical to winning public acceptance.

- NEC Corporation

- IDEMIA

- HID Global (ASSA ABLOY)

- Thales Group (Gemalto)

- Iris ID Inc.

- IriTech Inc.

- EyeLock LLC

- Princeton Identity Inc.

- BioEnable Technologies Pvt. Ltd.

- IrisGuard UK Ltd.

- Aware Inc.

- Vision-Box

- DERMALOG Identification Systems

- Cognitec Systems GmbH

- Smartmatic

- Samsung Electronics Co., Ltd.

- Fujitsu Limited

- CLEAR Inc.

- CMITech Company Ltd.

- SRI International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing National-ID and e-Passport Programs in Asia

- 4.2.2 Rising Border-Control spending across Middle-East corridors

- 4.2.3 Smartphone OEM Adoption of On-Device Iris Sensors

- 4.2.4 Expansion of Contactless Patient ID mandates in U.S. Healthcare

- 4.2.5 EU Digital Wallet Initiatives accelerating e-KYC demand

- 4.2.6 Cross-Border Money-laundering Compliance in BFSI

- 4.3 Market Restraints

- 4.3.1 High CAPEX of Multimodal Biometric Hubs at Airports

- 4.3.2 Accuracy Degradation under Non-cooperative Capture Scenarios

- 4.3.3 Data-sovereignty and Biometric-template Storage Regulations (EU GDPR)

- 4.3.4 Public Perception and Civil-liberties Backlash in North America

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Iris Scanners

- 5.1.1.2 Cameras

- 5.1.1.3 Integrated Iris-Recognition Systems

- 5.1.1.4 Other Optical Modules and Illumination

- 5.1.2 Software

- 5.1.2.1 Stand-alone Matching Engines

- 5.1.2.2 SDKs and Middleware

- 5.1.2.3 Cloud-based Platforms

- 5.1.1 Hardware

- 5.2 By Authentication Mode

- 5.2.1 1:1 Verification

- 5.2.2 1:N Identification

- 5.3 By Application

- 5.3.1 Access Control and Time-Attendance

- 5.3.2 ID and Border Control

- 5.3.3 Transaction and Payment Authentication

- 5.3.4 Patient Identification and EMR Linkage

- 5.3.5 Others (KYC, Surveillance, Automotive Infotainment)

- 5.4 By End-user Industry

- 5.4.1 Government and Law-Enforcement

- 5.4.2 Banking, Financial Services and Insurance (BFSI)

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Consumer Electronics

- 5.4.5 Military and Defense

- 5.4.6 Travel and Immigration

- 5.4.7 Commercial and Enterprise

- 5.4.8 Others (Education, Automotive OEMs)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Singapore

- 5.5.4.6 Australia

- 5.5.4.7 New Zealand

- 5.5.4.8 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Kenya

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 NEC Corporation

- 6.4.2 IDEMIA

- 6.4.3 HID Global (ASSA ABLOY)

- 6.4.4 Thales Group (Gemalto)

- 6.4.5 Iris ID Inc.

- 6.4.6 IriTech Inc.

- 6.4.7 EyeLock LLC

- 6.4.8 Princeton Identity Inc.

- 6.4.9 BioEnable Technologies Pvt. Ltd.

- 6.4.10 IrisGuard UK Ltd.

- 6.4.11 Aware Inc.

- 6.4.12 Vision-Box

- 6.4.13 DERMALOG Identification Systems

- 6.4.14 Cognitec Systems GmbH

- 6.4.15 Smartmatic

- 6.4.16 Samsung Electronics Co., Ltd.

- 6.4.17 Fujitsu Limited

- 6.4.18 CLEAR Inc.

- 6.4.19 CMITech Company Ltd.

- 6.4.20 SRI International

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

虹膜辨识市场:依组件、应用、部署方式及技术划分-2026-2032年全球市场预测

虹膜辨识市场:依组件、应用、部署方式及技术划分-2026-2032年全球市场预测 2026年全球虹膜辨识市场报告

2026年全球虹膜辨识市场报告 虹膜辨识生物辨识市场分析及预测(至2035年):依类型、产品、服务、技术、组件、应用、最终用户、安装类型、解决方案及部署方式划分虹膜辨识模组市场:按组件、认证模式、部署方式、应用程式和最终用户划分,全球预测(2026-2032年)

虹膜辨识生物辨识市场分析及预测(至2035年):依类型、产品、服务、技术、组件、应用、最终用户、安装类型、解决方案及部署方式划分虹膜辨识模组市场:按组件、认证模式、部署方式、应用程式和最终用户划分,全球预测(2026-2032年) 虹膜辨识市场规模、份额和成长分析(按组件、产品、应用、垂直产业和地区划分)-2026-2033年产业预测

虹膜辨识市场规模、份额和成长分析(按组件、产品、应用、垂直产业和地区划分)-2026-2033年产业预测 虹膜辨识市场规模、份额、成长分析(按组件、按产品、按应用、按行业垂直和按地区)—2025 年至 2032 年行业预测

虹膜辨识市场规模、份额、成长分析(按组件、按产品、按应用、按行业垂直和按地区)—2025 年至 2032 年行业预测 虹膜辨识市场规模、份额、趋势分析报告:按组件、应用、最终用途、地区和细分市场预测,2025 年至 2030 年

虹膜辨识市场规模、份额、趋势分析报告:按组件、应用、最终用途、地区和细分市场预测,2025 年至 2030 年 虹膜辨识市场:依技术类型、应用、组件展望、最终用户和地区划分,2024 年至 2031 年

虹膜辨识市场:依技术类型、应用、组件展望、最终用户和地区划分,2024 年至 2031 年