|

市场调查报告书

商品编码

1851770

现场可程式闸阵列(FPGA):市场份额分析、产业趋势、统计数据和成长预测(2025-2030 年)Field Programmable Gate Array (FPGA) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

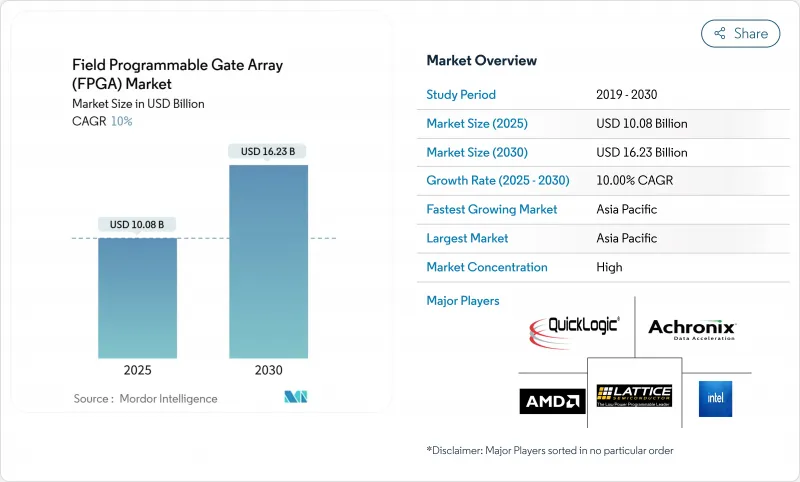

预计到 2025 年,现场可程式闸阵列(FPGA) 市场规模将达到 100.8 亿美元,到 2030 年将扩大到 162.3 亿美元,复合年增长率为 10.00%。

边缘人工智慧推理在超大规模资料中心的快速普及、向5G开放式无线架构的转型,以及汽车和航太电子产品对部署后重建日益增长的需求,都为市场提供了强劲的推动力。儘管高阶设备仍然是主要的收入来源,但随着设计团队在对成本敏感的工业、物联网和消费系统中部署FPGA技术,中阶产品也实现了快速成长。亚太地区已成为最大的製造地和成长最快的需求中心,受惠于电动车动力传动系统和新型太空卫星群。英特尔同意剥离Altera后,日益激烈的竞争重塑了供应商格局,而出口限制则刺激了中国国内的平行发展。此外,300毫米晶圆代工厂工厂产能紧张以及向成本高昂的16奈米及以下製程节点的过渡,迫使供应商优先考虑高利润应用,并与台积电和三星签订长期晶圆预订协议。

全球现场可程式闸阵列(FPGA) 市场趋势与洞察

超大规模资料中心对边缘AI推理的需求

随着延迟和功耗预算开始超过原始处理容量要求,超大规模营运商开始采用 FPGA 来加速 AI 推理。 AMD 的第二代 Versal AI Edge 装置的 TOPS/W 比第一代产品高出 3 倍,在降低营运成本的同时,实现了即时视觉分析。 Achronix 报告称,在运行大型语言模型时,FPGA 的成本和功耗比 GPU 方案低 200%,凸显了 FPGA 在记忆体受限工作负载中的效率。这种转变使得分散式计算模型得以实现,该模型将推理处理更靠近资料来源,从而缓解了频宽限制和资料主权风险。将封装内 HBM 和增强型 AI 引擎整合到领先的 FPGA 系列中,进一步巩固了 FPGA 在云端边缘拓扑结构中的地位。因此,现场可程式闸阵列)市场已成为超大规模资本支出计画中不可或缺的成长支柱。

向 5G ORAN 的过渡需要在无线电中采用可程式设计逻辑

开放式无线存取网计画促使通讯业者采用厂商中立的无线电单元,这些单元可以透过软体升级进行演进,而无需进行整体更换。英特尔的 Agilex 产品组合采用 10 奈米 SuperFin 工艺,提供软体定义无线电,能够适应新的 5G 版本,并降低整体拥有成本。莱迪思半导体 (Lattice Semiconductor) 为此硬体提供了参考协定栈,可为分散式网路提供零信任安全性和即时加密。 AMD 的 Zynq RFSoC DFE 的每瓦效能比之前的装置提高了一倍,使营运商能够在紧凑、功耗受限的射频单元中支援多频段运作。灵活的逻辑缩短了部署週期,这对于通讯业者融合私人 5G、固定无线存取和毫米波服务至关重要。

美国和欧盟对高效能FPGA出口中国实施限制。

美国工业与安全局的新规将于2023年下半年取消对华先进FPGA(现场可程式闸阵列)的民用豁免,限制了适用于人工智慧和军事应用的装置。这项变更迫使AMD-Xilinx和Intel-Altera暂停或授权大量订单,导致短期内销售下降。中国供应商如高文科技和盘古科技试图弥补缺口,但由于取得设计工具、智慧财产权和先进製程的门槛很高,短期内难以实现替代。跨国客户将敏感的生产转移到中国以外,或重新设计系统以适应非美国装置,扰乱了原本的全球供应链。在新贸易规则稳定之前,这种情况对现场闸阵列市场造成了压力。

细分市场分析

到2024年,高阶元件将占据现场可程式闸阵列)市场66.5%的份额,这反映了它们在资料中心加速和5G基础设施中的核心作用。这些平台通常拥有超过100万个逻辑单元,提供卓越的平均售价(ASP),同时还能实现GPU无法提供的确定性延迟,使其在安全关键型航太和金融科技工作负载中极具吸引力。 2030年,随着Lattice等製造商推出配备强化型AI引擎的成本优化产品以满足边缘运算预算,中阶低阶装置的复合年增长率(CAGR)将达到11.2%。设计工具也变得更加直观,使嵌入式工程师无需具备硬体知识即可采用可配置逻辑。

AMD推出Spartan UltraScale+后,其价值提案发生了转变。此技术功耗降低30%,I/O数量空前丰富,从高阶市场直接进军中阶。同时,模组厂商推出了预检验电路板,简化了引脚规划和PCB布局,缩短了设计週期。虽然这种转变有望缩小不同层级产品之间的价格差距,但随着新的AI和网路标准的出现,高阶元件仍将占据现场可程式闸阵列)市场的大部分份额,因为只有顶级製程节点的晶片才能满足这些标准。

预计到2024年,基于SRAM的解决方案将占总收入的55.4%,年复合成长率将达到11.8%,这得益于其无限次的重编程週期和强大的软体生态系统。然而,在穿戴式装置和汽车远端耐熔熔丝平台在国防航空电子设备领域占据着独特的地位,其一次性可编程性消除了篡改的风险。

软体可移植性正在打破历史壁垒,使设计人员能够基于功耗和安全性而非工具熟悉程度做出选择。新兴的异质架构将SRAM结构与片上非挥发性域集成,兼具两者的优势。虽然SRAM元件仍将主导现场可程式闸阵列)市场的收入,但由于快闪记忆体和耐熔熔丝产品功耗更低且适用于严苛环境,它们有望获得更大的市场份额。

现场可程式闸阵列按配置(高阶 FPGA、中阶/低阶 FPGA)、架构(基于 SRAM 的 FPGA、基于快闪记忆体的 FPGA 等)、技术节点(90nm 以上、20-90nm、16nm 以下)、终端市场(资料中心和云端运算、通讯和 5G 基础设施、欧洲汽车等)以及中东地区(北美汽车和欧洲亚洲)。

区域分析

亚太地区将在2024年占据现场可程式闸阵列)市场的主导地位,市占率将达到39.3%,预计到2030年将以17.1%的复合年增长率成长。中国大力推动半导体自主研发,尤其是在电动车驱动装置和卫星有效载荷领域涌现的创新者,推动了FPGA的大规模量产。台湾和韩国提供了先进的製造工艺,而日本则专注于汽车模组和工厂自动化子系统。印度的设计服务产业也取得了进展,莱迪思(Lattice)在普纳设立了研发中心,扩大了其工程人才储备。

北美在资料中心基础设施、高可靠性航太和EDA软体领域保持领先地位。超大规模资料中心业者资料中心营运商为自我调整加速器投入巨额资本预算,以控制人工智慧服务成本,从而在该地区占据了强大的市场份额。出口许可证审查影响了运输模式,同时也促使国内加大对先进封装和OSAT能力的投资,以支持现场可程式闸阵列)市场的发展。

欧洲倾向德国汽车供应链和北欧通讯设备供应商。 ISO 26262合规性促进了汽车应用的发展,而能源转型计划则创造了对低损耗功率转换器的需求。欧盟的「数位十年」政策鼓励了可重构边缘运算平台的发展。儘管南美洲和中东及非洲目前所占份额较小,但预计在预测期内,5G基础设施和工业现代化带来的成长潜力将提升其市场份额。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 超大规模资料中心对边缘AI推理的需求

- 5G ORAN 转换需要无线电中的可重程式逻辑

- ASIC/SoC 製程尺寸缩小週期(7 奈米及以下)的快速原型製作需求

- 汽车功能安全合规性(ISO 26262)

- 新型太空卫星群的抗辐射设计

- 中国电动车动力传动系统总成厂商采用eFPGA实现马达控制

- 市场限制

- 美国和欧盟对中国高效能FPGA出口实施限制。

- 300毫米铸造能力分配变异性

- 与专用ASIC相比,静态功耗更高

- 价值链分析

- 监理展望

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 宏观经济趋势对FPGA产业的影响

第五章 市场规模与成长预测

- 成分

- 高阶FPGA

- 中阶低阶FPGA

- 建筑设计

- 基于SRAM的FPGA

- 基于快闪记忆体的FPGA

- 耐熔熔丝FPGA

- 依技术节点

- >90 奈米

- 20-90 nm

- 16奈米或更小

- 按终端市场划分

- 资料中心和云端运算

- 通讯和5G基础设施

- 汽车(ADAS、电气化)

- 工业自动化与机器人

- 航太与国防(航空电子设备、卫星通讯)

- 消费性电子产品和穿戴式装置

- 测试、测量和医疗设备

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 北欧国家(瑞典、挪威、芬兰、丹麦)

- 其他欧洲地区

- 亚太地区

- 中国

- 台湾

- 日本

- 韩国

- 印度

- ASEAN

- 亚太其他地区

- 南美洲

- 墨西哥

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Advanced Micro Devices Inc.(Xilinx)

- Intel Corporation

- Lattice Semiconductor Corp.

- Microchip Technology Inc.(Microsemi)

- Achronix Semiconductor Corp.

- QuickLogic Corporation

- Efinix Inc.

- GOWIN Semiconductor Corp.

- Flex Logix Technologies Inc.

- NanoXplore SAS

- Anlogic Infotech Co. Ltd.

- Pango Microsystems Inc.

- Shenzhen S2C Ltd.

- BittWare(Molex Company)

- Digilent Inc.

- AlphaData Parallel Systems Ltd.

- Colfax International

- Reflex Ces SAS

- Aldec Inc.

- Beijing Tsinghua Tongfang Co. Ltd.

第七章 市场机会与未来展望

The field programmable gate array market size reached USD 10.08 billion in 2025 and is forecast to expand to USD 16.23 billion by 2030 at a 10.00% CAGR.

Rapid adoption of edge-AI inference in hyperscale data centers, the migration to 5G open radio architectures, and the rising need for post-deployment reconfigurability in automotive and aerospace electronics gave the market clear momentum. High-end devices continued to anchor revenues, yet mid-range and low-end products climbed quickly as design teams pushed FPGA technology into cost-sensitive industrial, IoT, and consumer systems. Asia-Pacific emerged as both the largest manufacturing base and the fastest-growing demand center, benefiting from electric-vehicle powertrains and new-space constellations. Competitive intensity increased after Intel agreed to carve out Altera, reshaping supplier dynamics while export controls spurred parallel domestic development in China. Tighter 300 mm foundry capacity and the costly transition to <=16 nm nodes also forced vendors to prioritize high-margin applications and long-term wafer reservations with TSMC and Samsung.

Global Field Programmable Gate Array (FPGA) Market Trends and Insights

Edge-AI inference demand in hyperscale data centers

Hyperscale operators deployed FPGAs to accelerate AI inference once latency and power budgets began outweighing raw throughput requirements. AMD's Versal AI Edge Gen 2 devices delivered up to 3 X higher TOPS-per-watt than first-generation parts, enabling real-time vision analytics while containing operating expenses. Achronix reported 200 % cost and power advantages versus GPU alternatives when running large language models, underscoring FPGA efficiency in memory-bound workloads. This shift unlocked a distributed compute model where inference processing moved closer to data sources, easing bandwidth constraints and data-sovereignty risks. Integration of on-package HBM and hardened AI engines within leading FPGA families strengthened their position in cloud-edge topologies. Consequently, the field programmable gate array market found a durable growth pillar in hyperscale capital expenditure plans.

5G ORAN shift requiring re-programmable logic in radios

Open radio access network initiatives pushed carriers to adopt vendor-agnostic radio units that could evolve with software upgrades rather than forklift replacements. Intel's Agilex portfolio used 10 nm SuperFin technology to deliver software-defined radios that adapt to new 5G releases at a lower total cost of ownership. Lattice Semiconductor complemented that hardware with a reference stack providing zero-trust security and real-time encryption for disaggregated networks. AMD's Zynq RFSoC DFE doubled performance per watt versus prior devices, letting operators support multi-band operation inside compact, power-constrained radio heads. Flexible logic shortened rollout cycles, a critical factor as carriers blended private-5G, fixed-wireless access, and mmWave services. That flexibility secured a new volume opportunity for the field programmable gate array market across telecom infrastructure.

US-EU export controls on high-performance FPGAs to China

New Bureau of Industry and Security rules removed civilian exemptions for advanced FPGA shipments to China in late 2023, restricting devices suited for AI or military use. The shift forced AMD-Xilinx and Intel-Altera to halt or license-screen many orders, reducing near-term unit volumes. Chinese suppliers such as GOWIN and Pango sought to close the gap, yet hurdles in design tools, IP, and advanced process access limited immediate substitution. Multinational customers moved sensitive production away from China or redesigned systems to qualify non-US devices, fracturing previously global supply chains. The resulting uncertainty weighed on the field programmable gate array market until new trade norms stabilized.

Other drivers and restraints analyzed in the detailed report include:

- Rapid prototyping needs for ASIC/SoC shrink cycles (<=7 nm)

- Functional safety compliance in automotive (ISO 26262)

- Volatility in 300 mm foundry capacity allocation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-end devices held 66.5% of the field programmable gate array market share in 2024, reflecting their central role in data-center acceleration and 5G infrastructure. These platforms, often exceeding 1 million logic cells, carried premium ASPs yet delivered deterministic latency unavailable in GPUs, preserving their appeal for safety-critical aerospace and fintech workloads. Mid-range and low-end devices exhibited an 11.2% CAGR to 2030 as manufacturers like Lattice shipped cost-optimized parts with hardened AI engines that met edge-compute budgets. Design tools have grown more intuitive, letting embedded engineers adopt configurable logic without hardware backgrounds.

The value proposition evolved as AMD introduced Spartan UltraScale+ with 30% lower power and unrivaled I/O count, attacking the mid-range from above. Simultaneously, module vendors supplied pre-validated boards that abstracted pin-planning and PCB layout, trimming design cycles. These shifts are expected to compress the pricing gap between tiers, although high-end devices still command a majority of the field programmable gate array market size when new AI or networking standards emerge that only top-node silicon can satisfy.

SRAM-based solutions owned 55.4% revenue in 2024 and posted an 11.8% CAGR outlook thanks to unlimited reprogram cycles and a deep software ecosystem. Yet flash-based variants gained mindshare in wearables and automotive telematics, where instant-on behavior is vital. Microchip's RT PolarFire achieved MIL-STD-883 Class B, offering 50% lower power than equivalent SRAM parts while tolerating 100 krad radiation. Anti-fuse platforms sustained a niche in defense avionics where one-time programmability eliminates tampering risk.

Software portability is shrinking historical barriers, so designers can now choose based on power and security rather than tool familiarity. Emerging heterogeneous architectures integrate SRAM fabric with on-die non-volatile domains, providing the best-of-both options. While SRAM devices will continue leading the field programmable gate array market revenue, flash and anti-fuse offerings should carve larger shares in low-power and harsh-environment deployments.

Field Programmable Gate Array is Segmented by Configuration (High-End FPGA, and Mid-range/Low-end FPGA), Architecture (SRAM-Based FPGA, Flash-Based FPGA, and More), Technology Node (>=90 Nm, 20-90 Nm, and <=16 Nm), End Market (Data Centre and Cloud Computing, Telecommunications and 5G Infrastructure, Automotive, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa).

Geography Analysis

Asia-Pacific dominated the field programmable gate array market with 39.3% revenue in 2024 and showed a 17.1% CAGR outlook to 2030. China's push for semiconductor self-reliance, highlighted by domestic innovators in electric vehicle drives and satellite payloads, pulled in significant FPGA volumes. Taiwan and South Korea supplied advanced fabrication, while Japan specialized in automotive modules and factory automation subsystems. India's design-service sector advanced after Lattice opened an R&D center in Pune, broadening engineering talent pools.

North America maintained leadership in data-center infrastructure, high-reliability aerospace, and EDA software. Hyperscalers directed large capital budgets toward adaptive accelerators to manage AI service costs, ensuring the region's strong purchase share. Export-license reviews shaped shipment patterns but also prompted domestic investment in advanced packaging and OSAT capacity that supports the field programmable gate array market.

Europe leaned on Germany's automotive supply chain and Nordic telecom equipment providers. ISO 26262 compliance spurred in-vehicle usage, while energy-transition projects created demand for low-loss power converters. EU Digital Decade policies encouraged sovereign edge computing platforms that favor reconfigurability. Although South America and the Middle East, and Africa hold smaller slices today, growth potential in 5G infrastructure and industrial modernization should boost their contribution over the forecast period.

- Advanced Micro Devices Inc. (Xilinx)

- Intel Corporation

- Lattice Semiconductor Corp.

- Microchip Technology Inc. (Microsemi)

- Achronix Semiconductor Corp.

- QuickLogic Corporation

- Efinix Inc.

- GOWIN Semiconductor Corp.

- Flex Logix Technologies Inc.

- NanoXplore SAS

- Anlogic Infotech Co. Ltd.

- Pango Microsystems Inc.

- Shenzhen S2C Ltd.

- BittWare (Molex Company)

- Digilent Inc.

- AlphaData Parallel Systems Ltd.

- Colfax International

- Reflex Ces SAS

- Aldec Inc.

- Beijing Tsinghua Tongfang Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Edge-AI Inference Demand in Hyperscale Data Centres

- 4.2.2 5G ORAN Shift Requiring Re-programmable Logic in Radios

- 4.2.3 Rapid Prototyping Needs for ASIC/SoC Shrink Cycles (<=7 nm)

- 4.2.4 Functional Safety Compliance in Automotive (ISO 26262)

- 4.2.5 Radiation-Tolerant Designs for New-Space Constellations

- 4.2.6 Chinese EV Power-train OEMs Adopting eFPGAs for Motor Control

- 4.3 Market Restraints

- 4.3.1 US-EU Export Controls on High-performance FPGAs to China

- 4.3.2 Volatility in 300 mm Foundry Capacity Allocation

- 4.3.3 Higher Static Power Consumption vs. Dedicated ASIC

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Trends on the FPGA Industry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Configuration

- 5.1.1 High-end FPGA

- 5.1.2 Mid-range/Low-end FPGA

- 5.2 By Architecture

- 5.2.1 SRAM-based FPGA

- 5.2.2 Flash-based FPGA

- 5.2.3 Anti-fuse FPGA

- 5.3 By Technology Node

- 5.3.1 >=90 nm

- 5.3.2 20-90 nm

- 5.3.3 <=16 nm

- 5.4 By End Market

- 5.4.1 Data Centre and Cloud Computing

- 5.4.2 Telecommunications and 5G Infrastructure

- 5.4.3 Automotive (ADAS, Electrification)

- 5.4.4 Industrial Automation and Robotics

- 5.4.5 Aerospace and Defense (Avionics, SATCOM)

- 5.4.6 Consumer Electronics and Wearables

- 5.4.7 Test, Measurement and Medical Devices

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Nordics (Sweden, Norway, Finland, Denmark)

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Taiwan

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 India

- 5.5.3.6 ASEAN

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Mexico

- 5.5.4.2 Brazil

- 5.5.4.3 Argentina

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global and Market Overview, Core Segments, Financials, Strategy, Rank/Share, Products, Recent Moves)

- 6.4.1 Advanced Micro Devices Inc. (Xilinx)

- 6.4.2 Intel Corporation

- 6.4.3 Lattice Semiconductor Corp.

- 6.4.4 Microchip Technology Inc. (Microsemi)

- 6.4.5 Achronix Semiconductor Corp.

- 6.4.6 QuickLogic Corporation

- 6.4.7 Efinix Inc.

- 6.4.8 GOWIN Semiconductor Corp.

- 6.4.9 Flex Logix Technologies Inc.

- 6.4.10 NanoXplore SAS

- 6.4.11 Anlogic Infotech Co. Ltd.

- 6.4.12 Pango Microsystems Inc.

- 6.4.13 Shenzhen S2C Ltd.

- 6.4.14 BittWare (Molex Company)

- 6.4.15 Digilent Inc.

- 6.4.16 AlphaData Parallel Systems Ltd.

- 6.4.17 Colfax International

- 6.4.18 Reflex Ces SAS

- 6.4.19 Aldec Inc.

- 6.4.20 Beijing Tsinghua Tongfang Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

现场可程式闸阵列(FPGA) 市场规模、份额和成长分析(按配置、节点尺寸、技术、垂直产业和地区划分)-2026-2033 年产业预测

现场可程式闸阵列(FPGA) 市场规模、份额和成长分析(按配置、节点尺寸、技术、垂直产业和地区划分)-2026-2033 年产业预测 现场可程式闸阵列(FPGA) 市场按配置、节点尺寸、技术、垂直产业和地区划分 - 预测至 2030 年

现场可程式闸阵列(FPGA) 市场按配置、节点尺寸、技术、垂直产业和地区划分 - 预测至 2030 年 现场可程式闸阵列(FPGA) 市场分析及预测(至 2034 年):类型、产品、应用、技术、组件、最终用户、部署、功能、安装类型、解决方案

现场可程式闸阵列(FPGA) 市场分析及预测(至 2034 年):类型、产品、应用、技术、组件、最终用户、部署、功能、安装类型、解决方案 FPGA主机市场预测(至 2032 年):按产品类型、核心相容性、分销管道、技术、应用、最终用户和地区进行的全球分析

FPGA主机市场预测(至 2032 年):按产品类型、核心相容性、分销管道、技术、应用、最终用户和地区进行的全球分析 依技术类型、整合度、威胁类型和应用分類的FPGA安全市场-2025-2032年全球预测现场可程式闸阵列(FPGA) 市场按配置类型、节点尺寸、技术、架构、处理器类型和应用划分 - 全球预测,2025-2032 年

依技术类型、整合度、威胁类型和应用分類的FPGA安全市场-2025-2032年全球预测现场可程式闸阵列(FPGA) 市场按配置类型、节点尺寸、技术、架构、处理器类型和应用划分 - 全球预测,2025-2032 年 2025年全球现场可程式闸阵列市场报告2025年全球嵌入式FPGA市场报告

2025年全球现场可程式闸阵列市场报告2025年全球嵌入式FPGA市场报告 现场可程式闸阵列(FPGA) 市场:全球预测(2025-2030 年)

现场可程式闸阵列(FPGA) 市场:全球预测(2025-2030 年) 现场可程式闸阵列(FPGA) 市场 2025-2029

现场可程式闸阵列(FPGA) 市场 2025-2029