|

市场调查报告书

商品编码

1851810

自动取样器:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Autosamplers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

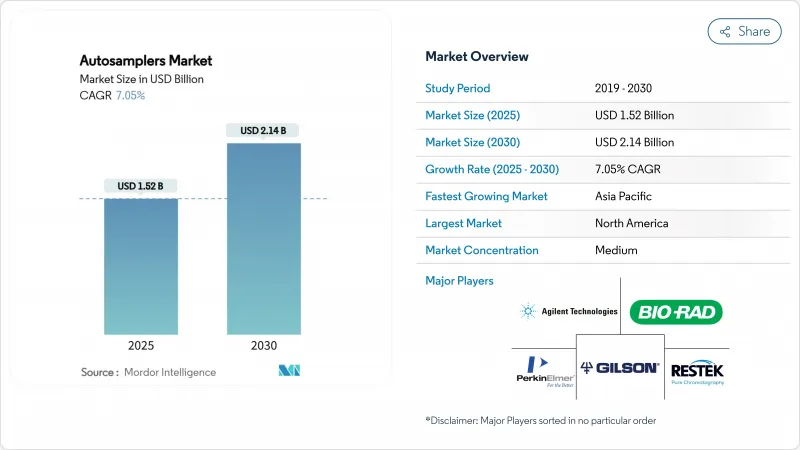

据估计,自动取样器市场规模将在 2025 年达到 15.2 亿美元,到 2030 年达到 21.4 亿美元,在预测期(2025-2030 年)内复合年增长率为 7.05%。

来自製药品管实验室的强劲更换需求以及环境和食品安全检测量的不断增长,支撑了仪器收入的稳定。 FDA等监管机构现在要求进行详细的分析方法验证,促使实验室采用自动化进样平台,以消除操作人员的差异并保护资料完整性。供应商也受益于人工智慧自动自动取样器的持续升级,这些自动进样器能够预测维护需求并减少计划外停机时间。自来水中PFAS化合物、农产品中农药残留以及新型化学品中杂质的监测力度加大,进一步拓宽了应用范围,推动自动取样器市场向更高通量和更高灵敏度的方向发展。亚太地区製造地的持续资本投资,使开发中国家成为未来大容量系统销售成长的关键驱动力。

全球自动取样器市场趋势与洞察

层析法在药物核准流程中的作用日益演变

美国食品药物管理局 (FDA) 目前强制要求对分析方法的稳健性实施更严格的控制,这一转变迫使生物製药公司实现样品处理的自动化,以满足数据完整性的要求。自动自动取样器可最大限度地减少人为误差,并确保全球生产网路的可重复性。整合式进样平台创建的集中式数位审核追踪加快了监管申报流程。复杂的生物製药需要多通道层析法分离,而这只有在无人值守的自动取样器操作下才能实现。生物相似药开发商也采用同样的策略来证明其可比较性,从而扩大了对新型疗法和后续疗法的需求。因此,随着所有后期研发项目的推进,自动取样器市场销量稳定成长。

加强全球食品安全与环境法规

欧盟「从农场到餐桌」的目标以及美国更新的饮用水中 PFAS 标准,对检测限的要求低于传统手动进样所能达到的水平。因此,食品和环境实验室正在整合能够处理更高浓度样品批次并减少残留的自动进样自动取样器。合约检测机构正在升级其平台以赢得监管竞标,这导致每三到五年就需要更换。仪器供应商正在采用灵活的支架来容纳各种类型的容器,使一台仪器能够处理环境和食品基质,从而提高运转率。跨国零售商现在必须遵守供应商检验规则,这要求他们与经过认证的实验室合作伙伴合作,并缩短了资金週转週期。这些相互交织的压力正在推动农业、水处理和包装行业的自动取样器市场进一步成长。

熟练的层析法操作人员短缺

许多资深分析师的退休速度超过了大学培养接班人的速度,迫使实验室依赖的专家数量减少。技能缺口使方法开发计划更加复杂,即使在自动化之后,这些专案仍然需要专家监督。小型实验室通常会延迟购买自动取样器,因为他们无法保证本地的故障排除支援。虽然设备供应商现在将远距离诊断和认证培训打包在一起以缓解人才短缺,但入职培训仍然会使新设备的采用延迟数月。亚太地区国家感受到的人才短缺最为严重,因为实验室的快速扩张超过了训练能力。这种劳动力失衡将抑制自动取样器市场的部分潜在需求,直到操作人员储备稳定下来。

细分市场分析

2024年,整合式自动取样器系统占据了59.61%的自动取样器市场。液相层析(HPLC)和超高效液相层析(UHPLC)仍然是药物放行检测的核心技术,因此液相层析法( LC)型号在出货量方面领先。气相层析法)系统在石油化工取证和环境挥发性有机化合物(VOC)监测中仍发挥重要作用,双模式设计可在单一机壳内支援这两种技术。持续的韧体更新可实现远端校准,从而减少20%的维护需求,并确保生产线检验执行时间。随着供应商应对仪器週期波动,诸如管瓶、注射器和温度控制模组等配件的重复销售也随之增长。能够进行微量注射的绿色化学产品可减少40%的溶剂用量,吸引了注重永续永续性的实验室管理人员。在预测期内,顶空进样和固相微萃取(SPME)平台将以10.64%的复合年增长率(CAGR)成长至2030年。这些成长动态将维持营收成长势头,并扩大自动取样器市场。

耗材和模组化升级也推高了已安装设备的平均售价。可容纳 1000 个微孔板管瓶的高容量样品架支援生物技术公司进行细胞培养代谢物筛检,取代了人工样品批量处理。基于人工智慧的针头健康评估可预测密封件磨损情况,从而实现及时订购替换零件,减少计划外停机时间。供应商积极交叉销售去离子水过滤装置和线上脱气装置,将自身定位为完整分析工作站的一站式供应商。这种捆绑销售策略增强了客户维繫,并提高了每台仪器的终身收入。因此,核心系统和配件的持续技术创新将在未来十年内支撑自动取样器市场的健康发展。

区域分析

2024年,北美将维持37.36%的自动取样器市场份额,这主要得益于强劲的药物研发管线、美国国立卫生研究院(NIH)的研究津贴以及美国环保署(EPA)对污染物排放法规的严格执行。美国实验室率先采用人工智慧驱动的自动取样器,并指出其显着的生产力提升足以支撑其溢价。多伦多和温哥华的加拿大生技产业丛集正在加速采购用于基因组医学检测的设备,而墨西哥的近岸工厂则正在调整分析方法以符合美国的进口法规。供应商的服务网路和耗材当日配送确保了全部区域的高运转率。

到2030年,亚太地区将以12.09%的复合年增长率实现最快增长,这主要得益于中国和印度扩大製剂和活性成分的生产规模,并赢得全球外包合约。在深圳和海得拉巴,政府补贴可抵销高达30%的自动化资本成本,进而促进多条生产线的部署。国内设备製造商与知名品牌合作,共同开发低成本产品,并扩大其在地级环保部门的影响力。韩国和日本正优先发展精准倡议的临床诊断自动化,使区域需求多元化。这些因素共同作用,将使自动取样器市场从传统的西方小众市场转变为真正的全球市场。

受REACH化学品法规和「从农场到餐桌」策略的推动,欧洲实现了稳步增长,这些战略要求严格监测农药残留。一家德国大型化学企业对其传统的品管实验室维修,配备了溶剂节约型自动取样器,以满足其企业碳排放目标。英国在脱欧后仍透过与欧盟分析指令保持一致,保持了投资的连续性。波兰和捷克共和国的东欧合约研究组织(CRO)丛集利用成本优势赢得了生物等效性测试业务,从而刺激了更多设备订单。中东/非洲和南美洲虽然受到资金缺口和技术技能短缺的限制,但在石化和食品出口产业的扩张推动下,自动进样器的应用正在逐步普及。整体而言,区域趋势正在强化自动取样器市场向区域销售发展的趋势。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 层析法在药物核准流程中的作用日益演变

- 加强全球食品安全与环境法规

- 推广实验室自动化以提高分析通量

- 扩展体学主导的临床诊断

- 基于人工智慧的预测性维护自动取样器市场

- 微量注射设计在绿色化学的应用

- 市场限制

- 熟练的层析法操作人员短缺

- 中小实验室面临高额资本投入与预算限制

- 严格的验证和合规时间表

- 智慧财产权碎片化及专利诉讼风险

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(单位:美元)

- 副产品

- 系统

- 液相层析法自动取样器市场

- 气相层析自动取样器市场

- 顶空和固相微萃取自动取样器市场

- 配件

- 系统

- 最终用户

- 製药和生物製药公司

- 环境与水质检测实验室

- 学术与合约研究实验室

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 亚太其他地区

- 中东和非洲

- GCC

- 南非

- 其他中东和非洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲国家

- 北美洲

第六章 竞争情势

- 市场集中度

- 市占率分析

- 公司简介

- Agilent Technologies, Inc.

- Thermo Fisher Scientific Inc.

- Shimadzu Corporation

- Waters Corporation

- PerkinElmer Inc.

- Bio-Rad Laboratories Inc.

- Gilson Inc.

- Restek Corporation

- Scion Instruments

- Tecan Group Ltd.

- HTA srl

- KNAUER Wissenschaftliche Gerate GmbH

- CTC Analytics AG

- Trajan Scientific(LEAP)

- GERSTEL GmbH

- DANI Instruments SpA

- LCTech GmbH

- ModuVision Technologies

- Valco Instruments(VICI)

- Ellutia Ltd.

第七章 市场机会与未来展望

The Autosamplers Market size is estimated at USD 1.52 billion in 2025, and is expected to reach USD 2.14 billion by 2030, at a CAGR of 7.05% during the forecast period (2025-2030).

Strong replacement demand from pharmaceutical quality-control laboratories, together with growing environmental and food-safety testing volumes, sustains steady equipment revenues. Regulatory bodies such as the FDA now require detailed analytical method validation, prompting laboratories to adopt automated sample-injection platforms that eliminate operator variability and safeguard data integrity. Vendors also benefit from continuous upgrades toward AI-ready autosamplers that predict maintenance needs and reduce unplanned downtime. Heightened scrutiny of PFAS compounds in water supplies, pesticide residues in produce, and impurities in new chemical entities further widens the application base, pushing the autosamplers market toward higher throughput and improved sensitivity. Ongoing capital investment in Asia Pacific manufacturing sites positions developing nations as critical future volume drivers for high-capacity systems.

Global Autosamplers Market Trends and Insights

Advancing Role of Chromatography in Drug Approval Workflows

The FDA now mandates tighter controls on analytical method robustness, and that shift forces biopharma companies to automate sample handling to comply with data-integrity expectations. Automated autosamplers minimize human error, thereby ensuring reproducibility across global manufacturing networks. Centralized digital audit trails created by integrated sampling platforms accelerate dossier assembly for regulatory submissions. Complex biologic molecules demand multi-lane chromatography sequences, which are only practical with unattended autosampler operation. Biosimilar developers adopt identical strategies to prove comparability, extending demand across both novel and follow-on therapeutics. In consequence, the autosamplers market secures stable volumes from every late-stage development program moving through the pipeline.

Tighter Global Food-Safety & Environmental Regulations

EU Farm-to-Fork objectives and updated US drinking-water standards for PFAS impose lower detection limits that conventional manual injection cannot meet. Food and environmental laboratories therefore integrate autosamplers capable of processing dense sample batches while holding low carry-over. Contract testing organizations upgrade platforms to win regulatory tenders, driving replacement purchases every three to five years. Equipment vendors embed flexible racks that accept diverse container types, allowing a single unit to address both environmental and food matrices, which improves utilization. Multinational retailers, now subject to supplier-verification rules, demand certified laboratory partners, reinforcing capital cycles. These intertwined pressures add incremental growth to the autosamplers market across agriculture, water, and packaging industries.

Shortage of Chromatography-Skilled Operators

Many senior analysts retire faster than universities can train replacements, pushing laboratories to depend on fewer specialists. The skills gap complicates method-development projects that still require expert oversight even after automation. Small laboratories often postpone autosampler purchases because they cannot guarantee local support for troubleshooting. Equipment suppliers now bundle remote diagnostics and certified training to mitigate the talent deficit, yet onboarding still delays utilization by several months. Asia Pacific nations feel the shortage most acutely due to rapid laboratory expansion outstripping educational capacity. This workforce imbalance suppresses a portion of latent demand in the autosamplers market until operator pipelines stabilize.

Other drivers and restraints analyzed in the detailed report include:

- Lab-Automation Push for Higher Analytical Throughput

- Expansion of Omics-Driven Clinical Diagnostics

- High Capex & Budget Limits at SME Labs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Integrated autosampler systems secured 59.61% of autosamplers market share in 2024 as laboratories favored turnkey combinations that align mechanically and electronically with chromatography instruments. Liquid chromatography models lead volume shipments because HPLC and UHPLC remain the backbone of pharmaceutical release testing. Gas chromatography systems maintain relevance in petrochemical forensics and environmental VOC monitoring, while dual-mode designs support both techniques within one chassis. Continuous firmware updates now enable remote calibration that cuts maintenance calls by 20%, ensuring uptime for validated production lines. The complementary accessories subsegment vials, syringes, temperature-control blocks drives recurring sales that cushion vendors against equipment-cycle swings. Green-chemistry variants with micro-volume injection reduce solvent use by 40%, an attractive metric for sustainability-focused laboratory managers. Over the forecast horizon, headspace and SPME platforms expand fastest at a 10.64% CAGR through 2030, propelled by global rules on aromatic hydrocarbon and organophosphate residues in food and soil. These growth dynamics preserve top-line momentum and broaden the autosamplers market.

Consumables and modular upgrades also lift average selling prices across installed bases. High-capacity racks that hold 1,000 microtiter vials support cell-culture metabolite screening at biotech firms, replacing manual sample batching. AI-driven needle health diagnostics now predict seal wear, triggering just-in-time ordering of replacement parts and reducing unexpected downtime. Vendors actively cross-sell de-ionized water filtration units and in-line degassers, embedding themselves as single-source suppliers for entire analytical workcells. This bundling strategy reinforces customer retention and amplifies lifetime revenues per instrument. Sustained innovation across core systems and accessories therefore underpins a healthy autosamplers market size during the coming decade.

The Autosamplers Market Report is Segmented by Product (Systems [Liquid Chromatography Autosamplers, Gas Chromatography Autosamplers, Headspace & SPME Autosamplers] and Accessories), End User (Pharmaceutical & Biopharmaceutical Companies, Environmental & Water-Testing Labs, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 37.36% of autosamplers market size in 2024 because of deep pharmaceutical pipelines, NIH research grants, and active EPA enforcement of contaminant rules. US laboratories adopt AI-enhanced autosamplers early, citing productivity gains that justify premium pricing. Canadian biotech clusters in Toronto and Vancouver accelerate purchases for genomic medicine trials, while Mexican near-shore plants align analytical methods with US import regulations. Vendor service networks and same-day consumables delivery sustain high uptime across the region.

Asia Pacific posts a 12.09% CAGR through 2030, the fastest worldwide, as China and India expand formulation and active-ingredient manufacturing to capture global outsourcing contracts. Government subsidies in Shenzhen and Hyderabad offset up to 30% of automation capital costs, catalyzing multi-line deployments. Domestic instrument makers partner with leading brands to co-develop low-price variants, expanding reach into county-level environmental bureaus. South Korea and Japan emphasize clinical-diagnostic automation for precision-medicine initiatives, thereby diversifying regional demand. The combined momentum redefines the autosamplers market as a truly global arena rather than a legacy Western niche.

Europe records steady growth driven by REACH chemical regulations and the Farm-to-Fork strategy that mandates rigorous monitoring of pesticide residues. German chemical giants retrofit legacy QC labs with solvent-saving autosamplers to hit corporate carbon targets. The United Kingdom continues parallel compliance with EU analytical directives post-Brexit, preserving investment continuity. Eastern European CRO clusters in Poland and the Czech Republic leverage cost advantages to win bioequivalence studies, fueling additional equipment orders. Middle East & Africa and South America follow with gradual adoption, constrained by financing gaps and technical-skills shortages yet supported by expanding petrochemical and food-export sectors. Overall, geography trends collectively strengthen the autosamplers market trajectory toward diversified regional sales.

- Agilent Technologies

- Thermo Fisher Scientific

- Shimadzu

- Waters Corporation

- PerkinElmer

- Bio-Rad Laboratories

- Gilson

- Restek

- Scion Instruments

- Tecan Group

- HTA s.r.l.

- KNAUER Wissenschaftliche Gerate GmbH

- CTC Analytics AG

- Trajan Scientific (LEAP)

- GERSTEL GmbH

- DANI Instruments SpA

- LCTech GmbH

- ModuVision Technologies

- Valco Instruments (VICI)

- Ellutia Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advancing Role of Chromatography in Drug Approval Workflows

- 4.2.2 Tighter Global Food-Safety & Environmental Regulations

- 4.2.3 Lab-Automation Push for Higher Analytical Throughput

- 4.2.4 Expansion of Omics-Driven Clinical Diagnostics

- 4.2.5 Ai-Enabled Predictive-Maintenance Autosamplers

- 4.2.6 Green-Chemistry Micro-Volume Injection Designs

- 4.3 Market Restraints

- 4.3.1 Shortage of Chromatography-Skilled Operators

- 4.3.2 High Capex & Budget Limits at Sme Labs

- 4.3.3 Stringent Validation & Compliance Timelines

- 4.3.4 Fragmented IP & Patent-Litigation Risks

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product

- 5.1.1 Systems

- 5.1.1.1 Liquid Chromatography Autosamplers

- 5.1.1.2 Gas Chromatography Autosamplers

- 5.1.1.3 Headspace & SPME Autosamplers

- 5.1.2 Accessories

- 5.1.1 Systems

- 5.2 By End User

- 5.2.1 Pharmaceutical & Biopharmaceutical Companies

- 5.2.2 Environmental & Water-Testing Labs

- 5.2.3 Academic & Contract Research Laboratories

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East & Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East & Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Agilent Technologies, Inc.

- 6.3.2 Thermo Fisher Scientific Inc.

- 6.3.3 Shimadzu Corporation

- 6.3.4 Waters Corporation

- 6.3.5 PerkinElmer Inc.

- 6.3.6 Bio-Rad Laboratories Inc.

- 6.3.7 Gilson Inc.

- 6.3.8 Restek Corporation

- 6.3.9 Scion Instruments

- 6.3.10 Tecan Group Ltd.

- 6.3.11 HTA s.r.l.

- 6.3.12 KNAUER Wissenschaftliche Gerate GmbH

- 6.3.13 CTC Analytics AG

- 6.3.14 Trajan Scientific (LEAP)

- 6.3.15 GERSTEL GmbH

- 6.3.16 DANI Instruments SpA

- 6.3.17 LCTech GmbH

- 6.3.18 ModuVision Technologies

- 6.3.19 Valco Instruments (VICI)

- 6.3.20 Ellutia Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

自动取样器市场:按产品类型、组件、样品类型、溶剂类型、分销管道、应用和最终用户划分-2025-2032年全球预测

自动取样器市场:按产品类型、组件、样品类型、溶剂类型、分销管道、应用和最终用户划分-2025-2032年全球预测 全球自动采样器市场规模研究与预测(按产品、配件、最终用户和区域划分)2022-2032 年

全球自动采样器市场规模研究与预测(按产品、配件、最终用户和区域划分)2022-2032 年