|

市场调查报告书

商品编码

1851844

智慧气动元件:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Smart Pneumatics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

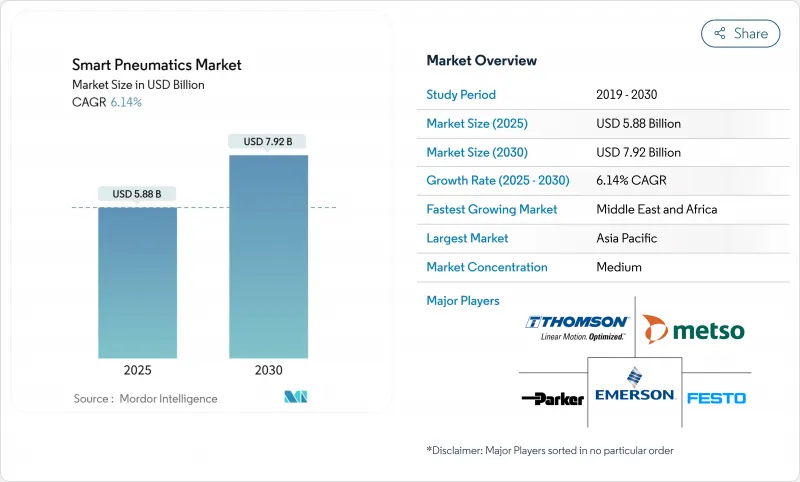

预计到 2025 年,智慧气动市场规模将达到 58.8 亿美元,到 2030 年将达到 79.2 亿美元,复合年增长率为 6.14%。

压缩空气动力与工业物联网 (IIoT) 连接的整合正在推动成长,这使得工厂环境中的即时监控、能源优化和预测性维护成为可能。製造商正优先进行气动系统升级,以减少计划外停机时间、降低压缩空气洩漏,并与製造执行系统 (MES) 和云分析无缝整合。亚太地区成长势头最为强劲,半导体领域的巨额投资和政府自动化专案正在扩大连网气动设备的装置量。同时,中东地区在油气井口应用领域也迅速普及,即时健康诊断有助于安全关键阀门的运作。数据管理是竞争的核心,领先的供应商正在增加人工智慧 (AI) 功能,以将感测器数据转化为可执行的洞察。

全球智慧气动市场趋势与洞察

一级汽车工厂对预测性维护的需求

一级汽车供应商正在气缸组件中嵌入压力、流量和温度感测器,以便在故障发生前数週检测到磨损模式。欧洲白车身生产线透过将气压感测器资料流与机器学习演算法相结合,识别异常丛集,从而实现了维护成本降低 20-30%,并将计划外停机次数降至几乎为零。北美动力传动系统工厂正在复製这个模式以保障生产线的节拍时间,而亚洲的原始设备製造商 (OEM) 则在当地劳动力短缺日益严重的背景下进行试点。随着电动车专案的扩展,混合车型组装需要依靠准确的故障预测来维持每小时的产量。因此,来自智慧气动设备的预测性健康数据正在将维护计划从日历式转变为基于状态的逻辑,从而维持运作并减少关键备件库存。

将相容IO-Link的感测器整合到气压阀中

IO-Link 将阀门从被动式气动开关转变为可寻址的现场设备。艾默生现场数据显示,阀门岛的自识别功能和控制器标籤的自动填充可将试运行时间缩短 40%。单一主控器上的八个 A 级连接埠支援流量、压力和位置感测器的组合,这些感测器可安装在距离 PLC 控制柜最远 30 公尺的位置,且不会造成讯号遗失。更快的设备更换速度缩短了平均维修时间,参数备份功能可防止手动设定点错误。在日本和韩国,由于需要频繁更换模具,IO-Link 在电子封装生产线上的应用正在加速。随着工厂采用 IO-Link 标准化感测器连接,气动诊断资料被传输到边缘网关,边缘网关再将警报资料包推送至 CMMS 应用,从而形成运作和维护之间的闭环。

乙太网路-IP与传统现场汇流排孤岛缺乏互通性

棕地计画通常运行着 PROFIBUS、DeviceNet 或 CC-Link 等独立网络,这些网路本身无法交换 CIP 物件。增加通讯协定网关会引入 5-15 毫秒的延迟,从而危及高速取放单元对时间要求极高的吹气序列。孤立的自动化模组阻碍了端到端的资料视觉性,维修团队不得不同时使用多种诊断工具。多重通讯协定节点和时间敏感型网路有望缓解这一问题,但它们需要等待资本预算週期和广泛部署。在此之前,系统整合必须设计混合产品,这需要在速度和成本之间做出妥协,从而延缓了旨在扩大智慧气动市场的更新计划。

细分市场分析

智慧气动阀为大多数产业提供配备丰富感测器的歧管平台,这些平台可将压力、流量和循环次数等数据传输至PLC,预计2024年智慧气动市场收入将占比45%。阀门健康指标可用于制定基于状态的检修计划,帮助汽车喷漆车间避免因压力漂移而导致的过喷缺陷。将IO-Link整合到歧管模组中,简化了扩充流程,因为8通主阀无需更改线路即可热插拔模组。附加元件分析功能可计算每个阀门的洩漏量,从而揭示旧有系统中隐藏的能量损失。半导体工厂正在采用符合无尘室颗粒物标准的不銹钢阀门,以提高生产连续性。

到2030年,智慧气压模组将以8.5%的复合年增长率快速成长,透过将阀门控制、压力调节和边缘运算整合机壳,超越单一功能组件。 Festo的运动终端运行一个可下载的应用程序,可在几分钟内将模组从开关控制切换到比例控製或真空生成。这种灵活性减少了SKU数量,并加快了快速消费品工厂的产品切换速度。这些模组还整合了节能演算法,可自动降低待机压力,从而支援工厂整体的脱碳目标。模组在系统级编配中的作用正在不断扩大,使其成为智慧气动市场的重要组成部分,尤其是在为即插即用扩充性而设计的待开发区线中。

到2024年,硬体销售额将占总销售额的60%,这反映了工厂车间阀门、气缸、稳压器和歧管等设备的更换週期。新一代汽缸整合了磁编码器,可提供0.1毫米解析度的位置回馈,从而实现包装单元中的多轴协同运动。微型流量感测器安装在稳压器本体上,用于逐升撷取消耗资料。供应商越来越多地提供具有安全启动韧体符合OT网路安全框架,可防止未经授权的代码注入。

服务是成长最快的组成部分,2025 年至 2030 年的复合年增长率 (CAGR) 为 10%。云端仪表板彙总阀岛关键绩效指标 (KPI),按异常风险对其进行排序,并在电脑化维护管理系统 (CMMS) 平台上自动产生工单。能源审核服务利用数据为洩漏分配成本值,并说服财务部门为航空公司维修提供资金。远端协助订阅服务使供应商专家能够存取设备日誌,并指导工厂技术人员进行纠正措施,从而减少差旅。从长远来看,此类数据主导服务层可将交易型产品销售转化为经常性收入。

智慧气动市场按产品类型(智慧气动阀、智慧气动致动器、智慧气动模组)、组件、设备类型、终端用户产业(汽车、石油天然气、食品饮料)、通讯协定(EtherNet/IP、PROFINET、IO-Link)、分销通路和地区进行细分。市场预测以美元计价。

区域分析

2024年,亚太地区将占全球销售额的38%,这主要得益于中国「中国製造2025」的自动化策略以及台湾地区329亿新台币的半导体投资。高密度工厂集群正在采用内置分析功能的阀组,以便在压缩空气洩漏导致能源费用飙升之前及时发现并采取措施。日本汽车工厂正在压平机上部署支援IO-Link技术的汽缸,以缩短多车型轮班期间的换型时间。宁波智慧气动等本地供应商正在为该地区的中小型企业提供成本优化的客製化模组,这加剧了市场竞争,并推动了性价比的快速提升,从而巩固了其区域优势。

北美是一个成熟且充满创新精神的买家市场。汽车原始设备製造商 (OEM) 正在将阀岛连接到云端人工智慧引擎,以便提前 30 天预测生产线停机,从而减少停机损失。 CHIPS 法案为亚利桑那州、德克萨斯和俄亥俄州的新建工厂提供奖励,这些工厂均要求配备符合 ISO 1 级标准的洁净压缩空气网路以及即时露点警报系统。节能减排的要求正促使工厂采用空气管理系统,该系统可在閒置期间关闭供气管线,这反映了智慧气动市场向永续性发展的趋势。

预计到2030年,中东地区的复合年增长率将达到7.5%。各国石油公司正在对井口维修,加装基于PLC的安全停机装置,该装置集成了双冗余气动致动器,用于将阀桿运动曲线传输至中央控制室。恶劣的气候条件推动了对耐腐蚀合金、高温密封件以及能够预测砂粒侵入的自我诊断阀块的需求。除了石油和天然气产业,海湾国家也在投资食品和製药厂以实现经济多元化,并采用模组化气动系统来满足那些本地工程支援有限的偏远工厂的需求。这种新兴需求正在扩大智慧气动市场供应商的地域覆盖范围。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场驱动因素

- 欧洲一级汽车工厂对预测性维护的需求

- 将支援 IO-Link 的传感器整合到气动阀中(北美)

- 加速中国大陆和台湾半导体产能扩张

- 中东地区油气井口安全关键型应用

- 市场限制

- 乙太网路/IP与传统现场汇流排孤岛缺乏互通性

- 轻型生产线中高总拥有成本与电子机械替代方案的比较

- 价值/供应链分析

- 监管或技术环境

- 全球 ISO 5599-2 数位阀门标准化

- 波特五力分析

- 新进入者的威胁

- 买方/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 智慧气动致动器

- 智慧气动模组

- 按组件

- 硬体

- 软体

- 服务

- 依设备类型

- 圆柱

- 感应器

- 转变

- 按最终用户行业划分

- 车

- 石油和天然气

- 饮食

- 透过通讯协定

- EtherNet/IP

- PROFINET

- IO-Link

- 透过分销管道

- 直销

- 间接/系统整合商

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚洲地区

- 中东

- 以色列

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第六章 竞争情势

- 策略趋势

- 市占率分析

- 公司简介

- Emerson Electric Co.(incl. Aventics)

- Festo SE and Co. KG

- Parker Hannifin Corporation

- SMC Corporation

- Bosch Rexroth AG

- Siemens AG(Industrial Automation)

- Rotork plc

- IMI Norgren(part of IMI plc)

- Bimba Manufacturing Co.(a part of IMI)

- PHD Inc.

- PNEUMAX SpA

- Cypress EnviroSystems Corp.

- AirTAC International Group

- Ningbo Smart Pneumatic Co. Ltd.

- Bosch Rexroth AG

- Thomson Industries Inc.

- The Smart Actuator Company Ltd.

- Aventics(now part of Emerson)

- Ham-Let Group

- Metso Automation(Flow Control)

第七章 市场机会与未来展望

The smart pneumatics market is valued at USD 5.88 billion in 2025 and is forecast to reach USD 7.92 billion by 2030, reflecting a 6.14% CAGR.

Growth is propelled by the fusion of compressed-air power with IIoT connectivity, which allows real-time monitoring, energy optimization, and predictive maintenance within factory environments. Manufacturers are prioritizing pneumatic upgrades that reduce unplanned downtime, cut compressed-air leaks, and integrate seamlessly with MES and cloud analytics. Regional momentum is strongest in Asia-Pacific, where large-scale semiconductor investments and government automation programs are expanding the installed base of connected pneumatic devices. Meanwhile, the Middle East shows rapid uptake in oil-and-gas wellhead applications, where safety-critical valve actuation benefits from live health diagnostics. Competition centers on data stewardship, with leading suppliers adding AI capabilities that convert sensor data into actionable insights.

Global Smart Pneumatics Market Trends and Insights

Predictive-maintenance imperatives in automotive tier-1 plants

Automotive tier-1 suppliers are embedding pressure, flow, and temperature sensors into cylinder assemblies to detect wear patterns weeks before failure. European body-in-white lines have documented 20-30% maintenance cost reductions and near-zero unplanned stops by coupling pneumatic sensor streams with machine-learning algorithms that flag anomaly clusters. North American power-train plants replicate the model to protect line takt times, and Asian OEMs are piloting it as local labour shortages intensify. As electrified vehicle programs expand, mixed-model assembly lines rely on fault-prediction accuracy to sustain hourly throughput. Predictive health data from smart pneumatic devices therefore shifts maintenance planning from calendar to condition-based logic, preserving uptime and compressing inventory of critical spares.

Integration of IO-Link-ready sensors in pneumatic valves

IO-Link converts valves from passive air switches into addressable field devices. Emerson field data indicates commissioning time cuts of 40% when valve islands self-identify and auto-populate controller tags. Eight Class A ports on a single master support combinations of flow, pressure, and position sensors placed up to 30 m from PLC cabinets without signal loss. Faster device replacement lowers mean-time-to-repair, while parameter backups prevent manual set-point errors. Japan and South Korea have accelerated adoption in electronics packaging lines that must swap tooling frequently. As factories unify sensor connectivity on IO-Link, pneumatic diagnostics feed edge gateways that push alarm packets to CMMS applications, closing the loop between operations and maintenance.

Lack of Ethernet-IP interoperability with legacy fieldbus islands

Brownfield sites often operate PROFIBUS, DeviceNet, or CC-Link islands that cannot natively exchange CIP objects. Adding protocol gateways introduces 5-15 ms latency, which jeopardizes time-critical blow-off sequences in high-speed pick-and-place units. Isolated automation pockets hinder end-to-end data visibility, forcing maintenance teams to juggle multiple diagnostic tools. Multi-protocol nodes and Time-Sensitive Networking promise relief, yet widespread deployment awaits capital-budget cycles. Until then, system integrators must design hybrids that compromise on either speed or cost, slowing refresh projects that would otherwise expand the smart pneumatics market.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated semiconductor capacity build-out in China and Taiwan

- Safety-critical adoption in oil and gas well-heads

- High TCO versus electromechanical alternatives in light-duty lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Smart pneumatic valves anchored the smart pneumatics market with 45% revenue in 2024, supplying most industries with sensor-rich manifold platforms that broadcast pressure, flow, and cycle counts to PLCs. Valve health metrics inform condition-based overhaul schedules, helping automotive paint shops avoid overspray defects linked to pressure drift. Integration of IO-Link within manifold blocks simplifies expansion, as eight-way masters accept hot-swap cartridges without rewiring. Add-on analytics calculate leakage per valve, highlighting energy losses invisible in legacy systems. Semiconductor fabs adopt stainless-steel variants that comply with cleanroom particulate standards, reinforcing demand continuity.

Smart pneumatic modules are accelerating at an 8.5% CAGR through 2030, outpacing single-function components by bundling valve control, pressure regulation, and edge computing in one enclosure. Festo's Motion Terminal runs downloadable apps that switch a module from on/off control to proportional regulation or vacuum generation in minutes. Such flexibility lowers SKU counts and speeds product changeovers in fast-moving consumer-goods plants. Modules also embed energy-savings algorithms that auto-reduce stand-by pressure, supporting factory-wide decarbonization goals. Their expanding role in system-level orchestration positions them as pivotal contributors to the smart pneumatics market, particularly in greenfield lines designed for plug-and-play scalability.

Hardware accounted for 60% of 2024 revenue, reflecting the replacement cycle of valves, cylinders, regulators, and manifolds that populate factory floors. New-generation cylinders incorporate magnetic encoders delivering 0.1 mm resolution positional feedback, enabling coordinated multi-axis moves in packaging cells. Miniaturized flow sensors fit into regulator bodies, capturing consumption data down to the litre. Vendors increasingly ship hardware with secure boot firmware to guard against unauthorized code injection, aligning with OT cybersecurity frameworks.

Services represent the fastest-growing component at a 10% CAGR from 2025-2030. Cloud dashboards aggregate valve-island KPIs, rank them by anomaly risk, and generate automatic work orders in CMMS platforms. Energy-audit services use the data to assign cost values to leaks, convincing finance departments to fund air-line retrofits. Remote-assist subscriptions let vendor specialists access device logs, guiding plant technicians through corrective actions and reducing travel. Over time, this data-driven service layer converts transactional product sales into recurring revenue, an approach echoed by similar transitions in the smart pneumatics industry.

Smart Pneumatics Market Segmented by Product Type (Smart Pneumatic Valves, Smart Pneumatic Actuators and Smart Pneumatic Modules), Component, Instrument Type, End-User Industry (Automotive, Oil & Gas and Food & Beverage), Communication Protocol (EtherNet/IP, PROFINET and IO-Link), Distribution Channel and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 38% revenue in 2024, supported by China's automation drive under "Made in China 2025" and Taiwan's NT$32.9 billion semiconductor investments. High-density factory clusters adopt valve manifolds with built-in analytics that flag compressed-air leaks before they inflate utility bills. Japanese automotive plants roll out IO-Link enabled cylinders across stamping presses, cutting changeover times during multi-model shifts. Local vendors such as Ningbo Smart Pneumatic supply cost-optimized modules tailored to regional SMEs, intensifying competition and stimulating rapid price-performance improvements that strengthen regional dominance.

North America represents a mature yet innovation-focused buyer base. Automotive OEMs connect valve islands to cloud AI engines that predict line stoppages 30 days in advance, reducing downtime penalties. The CHIPS Act incentivizes new fabs in Arizona, Texas, and Ohio, each specifying ISO Class 1 clean-compressed-air networks with live dew-point alarms. Energy-reduction mandates push plants to adopt air-management systems capable of shutting off feed lines during idle periods, reflecting a broader push toward sustainability in the smart pneumatics market.

The Middle East is expected to grow at 7.5% CAGR through 2030. National oil companies retrofit wellheads with PLC-based safety shutdown units integrating dual-redundant pneumatic actuators that broadcast stem-movement profiles to central control rooms. The harsh climate drives demand for corrosion-resistant alloys, extended-temperature seals, and self-diagnosing valve blocks that anticipate sand ingress. Beyond oil and gas, Gulf states invest in food and pharmaceutical plants to diversify economies, adopting modular pneumatics that fit isolated facilities with limited local engineering support. This emerging demand widens the geographic footprint of smart pneumatics market suppliers.

- Emerson Electric Co. (incl. Aventics)

- Festo SE and Co. KG

- Parker Hannifin Corporation

- SMC Corporation

- Bosch Rexroth AG

- Siemens AG (Industrial Automation)

- Rotork plc

- IMI Norgren (part of IMI plc)

- Bimba Manufacturing Co. (a part of IMI)

- PHD Inc.

- PNEUMAX S.p.A.

- Cypress EnviroSystems Corp.

- AirTAC International Group

- Ningbo Smart Pneumatic Co. Ltd.

- Bosch Rexroth AG

- Thomson Industries Inc.

- The Smart Actuator Company Ltd.

- Aventics (now part of Emerson)

- Ham-Let Group

- Metso Automation (Flow Control)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Drivers

- 4.1.1 Predictive-maintenance imperatives in automotive tier-1 plants (Europe)

- 4.1.2 Integration of IO-Link-ready sensors in pneumatic valves (North America)

- 4.1.3 Accelerated semiconductor capacity build-out in China and Taiwan

- 4.1.4 Safety-critical adoption in oil and gas well-heads (Middle East)

- 4.2 Market Restraints

- 4.2.1 Lack of Ethernet-IP interoperability with legacy fieldbus islands

- 4.2.2 High TCO versus electromechanical alternatives in light-duty lines

- 4.3 Value / Supply-Chain Analysis

- 4.4 Regulatory or Technological Outlook

- 4.4.1 Global ISO 5599-2 digital valve standardization

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Smart Pneumatic Actuators

- 5.1.1 Smart Pneumatic Modules

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By Instrument Type

- 5.3.1 Cylinders

- 5.3.2 Transducers

- 5.3.3 Switches

- 5.4 By End-user Industry

- 5.4.1 Automotive

- 5.4.2 Oil and Gas

- 5.4.3 Food and Beverage

- 5.5 By Communication Protocol

- 5.5.1 EtherNet/IP

- 5.5.2 PROFINET

- 5.5.3 IO-Link

- 5.6 By Distribution Channel

- 5.6.1 Direct Sales

- 5.6.2 Indirect / System-Integrator

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 United Kingdom

- 5.7.2.2 Germany

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 South Korea

- 5.7.3.5 Rest of Asia

- 5.7.4 Middle East

- 5.7.4.1 Israel

- 5.7.4.2 Saudi Arabia

- 5.7.4.3 United Arab Emirates

- 5.7.4.4 Turkey

- 5.7.4.5 Rest of Middle East

- 5.7.5 Africa

- 5.7.5.1 South Africa

- 5.7.5.2 Egypt

- 5.7.5.3 Rest of Africa

- 5.7.6 South America

- 5.7.6.1 Brazil

- 5.7.6.2 Argentina

- 5.7.6.3 Rest of South America

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Emerson Electric Co. (incl. Aventics)

- 6.3.2 Festo SE and Co. KG

- 6.3.3 Parker Hannifin Corporation

- 6.3.4 SMC Corporation

- 6.3.5 Bosch Rexroth AG

- 6.3.6 Siemens AG (Industrial Automation)

- 6.3.7 Rotork plc

- 6.3.8 IMI Norgren (part of IMI plc)

- 6.3.9 Bimba Manufacturing Co. (a part of IMI)

- 6.3.10 PHD Inc.

- 6.3.11 PNEUMAX S.p.A.

- 6.3.12 Cypress EnviroSystems Corp.

- 6.3.13 AirTAC International Group

- 6.3.14 Ningbo Smart Pneumatic Co. Ltd.

- 6.3.15 Bosch Rexroth AG

- 6.3.16 Thomson Industries Inc.

- 6.3.17 The Smart Actuator Company Ltd.

- 6.3.18 Aventics (now part of Emerson)

- 6.3.19 Ham-Let Group

- 6.3.20 Metso Automation (Flow Control)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis