|

市场调查报告书

商品编码

1940570

英国设施管理:市场占有率分析、产业趋势与统计、成长预测(2026-2031)United Kingdom (UK) Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

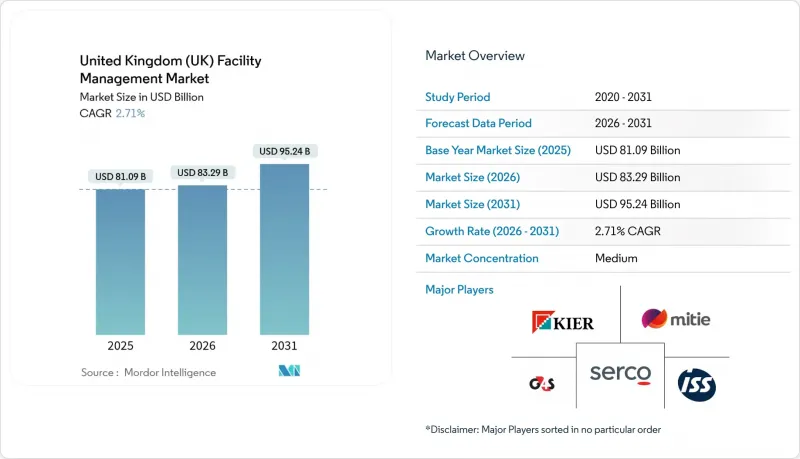

2025年英国设施管理市场价值为810.9亿美元,预计2031年将达到952.4亿美元,高于2026年的832.9亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 2.71%。

这种稳健的成长轨迹标誌着一个日益成熟的产业正在能源效率要求、数位转型以及对外包服务模式的持续偏好下不断发展。硬性服务至关重要,因为老旧建筑需要严格的机械、电气和管道维护才能达到最低能源效率标准。同时,软性服务也在快速发展,以满足职场的福祉和严格的卫生法规要求。从物联网感测器网路到人工智慧驱动的分析,技术整合正在实现更快的响应速度、更低的能耗以及基于绩效的合同,从而在不增加人员配置的情况下提高收入。随着公共和私人客户寻求能够确保合规性并在投入价格波动的情况下提供成本确定性的专业知识,外包势头持续强劲。儘管与英国脱欧相关的劳动力短缺和成本上涨正在挤压利润率,但公共部门维修资金的增加和灵活办公空间的兴起为那些能够快速创新的服务提供者提供了扩张途径。

英国设施管理市场趋势与洞察

技术整合(物联网、人工智慧、自动化)

人工智慧驱动的楼宇管理平台正在重新定义服务交付方式。英国智慧财产局在实施数位化工单入口网站后,将维护回应时间从14天缩短至几秒钟。智慧感测器即时传输人员占用率、温度和空气品质数据,使服务供应商能够从被动维护转向预测性维护,同时降低能源消耗并提升员工舒适度。世邦魏理仕进军超级大规模资料中心设施管理领域,凸显了该产业巨大的获利潜力,因为该产业需要全天候的分析监控。医疗保健和教育产业的客户正在主导这一趋势,因为合规制度要求持续进行环境监测。随着数位化仪錶板整合软性服务和硬性服务,服务提供者将清洁、保全、办公室支援和资产维护等服务打包到资料丰富的合约中,从而获得更高的价格溢价。

商业不动产的快速扩张

根据英国特许测量师学会 (RICS) 的数据,预计租户需求将在 2025 年第一季转正,伦敦市中心黄金地段的办公大楼租金预计将以每年约 5% 的速度增长。工业资产的投资热情最为强劲,受电子商务和近岸外包的推动,投资者需求净成长 18%。新开发项目带动了对性能验证、全生命週期资产管理和持续合规审核的需求成长。与开发商早期合作的设施管理人员将从智慧建筑中获得多年的稳定收入,这些智慧建筑从一开始就整合了 ESG(环境、社会和治理)仪錶板。同样,物流业的成长也推动了客製化设施管理方案的发展,这些方案结合了库存追踪技术、码头管理和先进的消防维护技术,适用于高容量仓库。

劳动力短缺和技能差距

饭店、清洁和餐饮业正面临设施管理职缺的困境,预计英国脱欧后将有13.2万个职缺。 2025年移民白皮书将把技术纯熟劳工签证的要求提高到RQF 6级,这将限制入门级设施管理职位的国际人才招募。自2005年以来,雇主在培训方面的投入下降了28%,导致技能短缺,同时,建筑物却在采用先进的数位系统。企业正在透过设立主管培训学院来应对这项挑战,这些学院专注于提升领导力和技术技能,例如Samsic旗下JPC推出的包含12个模组的「下一代」计画。然而,高离职率和劳动力老化仍然是限制该产业发展能力的因素。

细分市场分析

截至2025年,硬性服务将占英国设施管理市场的60.12%,这主要得益于英国国民医疗服务体系(NHS)高达116亿英镑(31.9亿美元)的延期维护支出以及日益严格的能源性能证书(EPC)期限。由于仍有28%的商业建筑EPC评级为D级或以下,英国设施管理市场中硬性服务合约的规模预计将会成长,这刺激了对机械、电气和管道(MEP)维修的需求。 MEP和HVAC(暖气、通风和空调)产业受益于净零排放的监管路径,该路径要求到2035年排放47%至62%。资产数位化将进一步推动对预测性维护分析的需求,使服务提供者能够在资产故障发生前进行干预,同时满足合规报告要求。

儘管目前软性服务规模较小,但在医院级清洁标准和职场体验创新的推动下,预计到2031年将以2.78%的复合年增长率增长。更严格的感染控制法规推动了对机器人消毒系统和感测器检验卫生通讯协定的需求。共享办公空间营运商对智慧门禁系统的需求推动了保全服务的现代化。格雷内尔消防法案实施后加强的消防安全措施推动了对整合警报测试和疏散规划服务的需求。这些因素共同促使服务提供者的产品组合转向融合卓越软性服务和资料驱动合规性的综合方案。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 目前运转率

- 主要FM业者的盈利能力

- 劳动指标 - 劳动参与率

- 按服务类型分類的设施管理市场占有率(%)

- 以硬性服务分類的设施管理市场占有率(%)

- 按软体服务分類的设施管理市场占有率(%)

- 主要都会区的都市化和人口成长

- 英国基础设施计画中的产业投资优先事项

- 与劳动和安全标准相关的监管驱动因素

- 市场驱动因素

- 商业不动产的快速扩张

- 技术整合(物联网、人工智慧、自动化)

- 外包趋势日益成长

- 更重视职场经验和员工福祉

- 严格的能源效率和净零排放法规

- 灵活办公空间的兴起对灵活的设施管理合约提出了更高的要求。

- 市场限制

- 労働力不足とスキルギャップ

- 营运成本上升给利润率带来压力。

- 供应商生态系统分散,阻碍服务标准化

- 智慧建筑系统中的资料安全问题

- 价值链分析

- PESTEL 分析

- 新参与企业的监管和法律体制

- 宏观经济指标对FM需求的影响

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 投资与资金筹措分析

第五章 市场规模与成长预测

- 按服务类型

- 硬服务

- 资产管理

- 机电及暖通空调服务

- 消防设备和安全措施

- 其他硬体维修服务

- 软服务

- 办公室支援与安全

- 清洁服务

- 餐饮服务

- 其他软性调频服务

- 硬服务

- 按产品类型划分

- 内部管理

- 外包

- 单频调频

- 综合设施管理(捆绑式设施管理)

- 综合设施管理(综合FM)

- 按最终用户行业划分

- 商业设施(IT/通讯、零售/仓储等)

- 餐饮服务业(饭店、餐厅、大型餐厅)

- 公共及公共基础设施(政府机构、教育机构、交通运输)

- 医疗保健(公立和私立机构)

- 工业和流程(製造业、能源业、采矿业)

- 其他终端用户产业(多用户住宅、娱乐、运动和休閒)

第六章 竞争情势

- 市场集中度

- 策略倡议与伙伴关係

- 市占率分析

- 公司简介

- ISS UK

- Mitie Group PLC

- Serco Group PLC

- Kier Group PLC

- G4S Facilities Management UK Limited

- Sodexo Facilities Management Services

- Compass Group

- Equans

- VINCI Facilities Limited

- Aramark Facilities Services

- Andron Facilities Management

- CSM Facilities Management Group

- Orton Group

- Global Facilities.

- BGIS

第七章 市场机会与未来展望

The United Kingdom facility management market was valued at USD 81.09 billion in 2025 and estimated to grow from USD 83.29 billion in 2026 to reach USD 95.24 billion by 2031, at a CAGR of 2.71% during the forecast period (2026-2031).

The measured trajectory signals a mature sector advancing under energy-efficiency mandates, digital transformation, and a sustained preference for outsourced service models. Hard services hold prime importance because ageing building stock demands strict mechanical, electrical, and plumbing upkeep to meet Minimum Energy Efficiency Standards, while soft services evolve quickly to address workplace well-being and stringent hygiene rules. Technology integration from IoT sensor grids to AI-powered analytics-cuts response times, trims energy consumption, and enables outcome-based contracts that grow revenue without proportionate head-count expansion. Outsourcing momentum continues as public and private clients seek specialist expertise that guarantees compliance and delivers cost certainty amid volatile input prices. Although Brexit-linked labour shortages and cost inflation compress margins, rising public-sector refurbishment funding and the spread of flexible workspaces offer expansion lanes for providers that innovate fast.

United Kingdom (UK) Facility Management Market Trends and Insights

Technology Integration (IoT, AI, Automation)

AI-driven building-management platforms are redefining service delivery, with the Intellectual Property Office cutting maintenance response times from 14 days to seconds after launching a digital work-order portal. Smart sensors relay live occupancy, temperature, and air-quality data, letting providers shift from reactive to predictive maintenance while lowering energy use and elevating employee comfort. CBRE's entry into hyperscale data-center facilities management underscores the high-margin potential in segments that demand 24-hour analytical monitoring. Healthcare and education clients lead adoption because compliance regimes mandate continuous environmental monitoring. As digital dashboards merge soft and hard services, providers package cleaning, security, office support, and asset maintenance into data-rich contracts that command price premiums.

Rapid Commercial Real Estate Expansion

Royal Institution of Chartered Surveyors data show occupier demand turned positive in Q1 2025, and prime office rents in Central London are projected to rise nearly 5% in the year. Industrial assets register the strongest investment appetite, with an +18% net balance in investor demand, propelled by e-commerce and near-shoring. New developments increase demand for commissioning, lifecycle asset management, and ongoing compliance auditing. Facility managers partnering early with developers secure multi-year revenue streams in smart-ready buildings that integrate ESG dashboards from day one. Logistics growth similarly drives tailored FM packages that combine inventory tracking technologies, dock management, and advanced fire-suppression maintenance for high-throughput warehouses.

Labor Shortages and Skill Gaps

Hospitality, cleaning, and catering units face 132,000 job vacancies post-Brexit, straining FM rosters. The 2025 Immigration White Paper raises the Skilled Worker visa threshold to RQF Level 6, curtailing access to international staff for entry-level FM roles. Employer training investment has fallen 28% since 2005, creating a skills deficit just as buildings adopt sophisticated digital systems. Firms counteract with supervisor academies such as JPC by Samsic's 12-module Next Gen programme focusing on leadership and technical upskilling. Nonetheless, high turnover and an aging workforce continue to limit sector capacity.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Outsourcing Trend

- Rising Focus on Workplace Experience and Employee Well-being

- Margin Pressure from Rising Operational Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard services held 60.12% of United Kingdom facility management market share in 2025, anchored by the NHS's GBP 11.6 billion (USD 3.19 billion) maintenance backlog and stringent EPC upgrade timelines. The United Kingdom facility management market size for hard-service contracts is poised to expand as 28% of commercial properties still rate D or lower on EPC scale, forcing accelerated mechanical, electrical, and plumbing overhauls. MEP and HVAC segments benefit from regulatory pathways to net-zero that mandate 47%-62% emissions cuts by 2035. Asset digitization further lifts demand for predictive-maintenance analytics, letting providers intervene before asset failure while meeting compliance reporting needs.

Soft services, while smaller today, are forecast to grow 2.78% CAGR through 2031, propelled by hospital-grade cleaning standards and workplace-experience innovations. Heightened infection-control rules elevate the premium for robotic disinfection systems and sensor-verified hygiene protocols. Co-working operators require smart access control, driving security-service modernization. Fire-safety upgrades tied to post-Grenfell legislation amplify demand for integrated alarm testing and evacuation-planning services. Together, these forces shift provider offerings toward comprehensive packages that merge soft-service excellence with data-backed compliance.

The United Kingdom Facility Management Market Report is Segmented by Service Type (Hard Services, Soft Services), Offering Type (In-House, Outsourced), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ISS UK

- Mitie Group PLC

- Serco Group PLC

- Kier Group PLC

- G4S Facilities Management UK Limited

- Sodexo Facilities Management Services

- Compass Group

- Equans

- VINCI Facilities Limited

- Aramark Facilities Services

- Andron Facilities Management

- CSM Facilities Management Group

- Orton Group

- Global Facilities.

- BGIS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.1.1 Current Occupancy Rates

- 4.1.2 Profitability Rates of Major FM Players

- 4.1.3 Workforce Indicators - Labor Participation

- 4.1.4 Facility Management Market Share (%), by Service Type

- 4.1.5 Facility Management Market Share (%), by Hard Services

- 4.1.6 Facility Management Market Share (%), by Soft Services

- 4.1.7 Urbanization and Population Growth in Major Metros

- 4.1.8 Sector Investment Priorities in United Kingdom's Infrastructure Pipeline

- 4.1.9 Regulatory Drivers Specific to Labour and Safety Standards

- 4.2 Market Drivers

- 4.2.1 Rapid Commercial Real Estate Expansion

- 4.2.2 Technology Integration (IoT, AI, Automation)

- 4.2.3 Increasing Outsourcing Trend

- 4.2.4 Rising Focus on Workplace Experience and Employee Well-being

- 4.2.5 Stringent Energy-Efficiency and Net-Zero Regulations

- 4.2.6 Rise of Flexible Workspaces Requiring Agile FM Contracts

- 4.3 Market Restraints

- 4.3.1 Labor Shortages and Skill Gaps

- 4.3.2 Margin Pressure from Rising Operational Costs

- 4.3.3 Fragmented Supplier Ecosystem Hindering Service Standardization

- 4.3.4 Data-Security Concerns in Smart Building Systems

- 4.4 Value Chain Analysis

- 4.5 PESTEL Analysis

- 4.6 Regulatory and Legislative Framework for Market Entrants

- 4.7 Impact of Macroeconomic Indicators on FM Demand

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Services

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Services

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard FM Services

- 5.1.2 Soft Services

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft FM Services

- 5.1.1 Hard Services

- 5.2 By Offering Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.2.2.1 Single FM

- 5.2.2.2 Bundled FM

- 5.2.2.3 Integrated FM

- 5.3 By End-user Industry

- 5.3.1 Commercial (IT and Telecom, Retail and Warehouses, etc.)

- 5.3.2 Hospitality (Hotels, Eateries, Large-scale Restaurants)

- 5.3.3 Institutional and Public Infrastructure (Govt, Education, Transportation)

- 5.3.4 Healthcare (Public and Private Facilities)

- 5.3.5 Industrial and Process (Manufacturing, Energy, Mining)

- 5.3.6 Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Partnerships

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ISS UK

- 6.4.2 Mitie Group PLC

- 6.4.3 Serco Group PLC

- 6.4.4 Kier Group PLC

- 6.4.5 G4S Facilities Management UK Limited

- 6.4.6 Sodexo Facilities Management Services

- 6.4.7 Compass Group

- 6.4.8 Equans

- 6.4.9 VINCI Facilities Limited

- 6.4.10 Aramark Facilities Services

- 6.4.11 Andron Facilities Management

- 6.4.12 CSM Facilities Management Group

- 6.4.13 Orton Group

- 6.4.14 Global Facilities.

- 6.4.15 BGIS

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Technology-led Integrated FM (IoT, BMS, AI-based Predictive Maintenance)

- 7.3 ESG-compliant FM Solutions Demand

- 7.4 Future Service-Model Shifts (Outcome-based Contracts)

机器人即服务 (RaaS) 市场分析及至 2035 年预测:按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和功能划分电脑辅助设施管理 (CAFM) 市场分析及至 2035 年预测:按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和模组划分设施管理市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能及解决方案划分

机器人即服务 (RaaS) 市场分析及至 2035 年预测:按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和功能划分电脑辅助设施管理 (CAFM) 市场分析及至 2035 年预测:按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和模组划分设施管理市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能及解决方案划分 亚太地区设施管理:市场占有率分析、产业趋势与统计、成长预测(2026-2031)新加坡设施管理:市场占有率分析、产业趋势与统计、成长预测(2026-2031)欧洲设施管理:市场占有率分析、产业趋势与统计、成长预测(2026-2031)美国设施管理:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)

亚太地区设施管理:市场占有率分析、产业趋势与统计、成长预测(2026-2031)新加坡设施管理:市场占有率分析、产业趋势与统计、成长预测(2026-2031)欧洲设施管理:市场占有率分析、产业趋势与统计、成长预测(2026-2031)美国设施管理:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年) 设施管理市场-全球产业规模、份额、趋势、机会与预测:按组件、部署、市场渗透率、产品类型、组织规模、应用、地区和竞争格局划分,2021-2031年义大利设施管理市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)印尼设施管理市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

设施管理市场-全球产业规模、份额、趋势、机会与预测:按组件、部署、市场渗透率、产品类型、组织规模、应用、地区和竞争格局划分,2021-2031年义大利设施管理市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)印尼设施管理市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)