|

市场调查报告书

商品编码

1852112

基油:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Base Oil - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

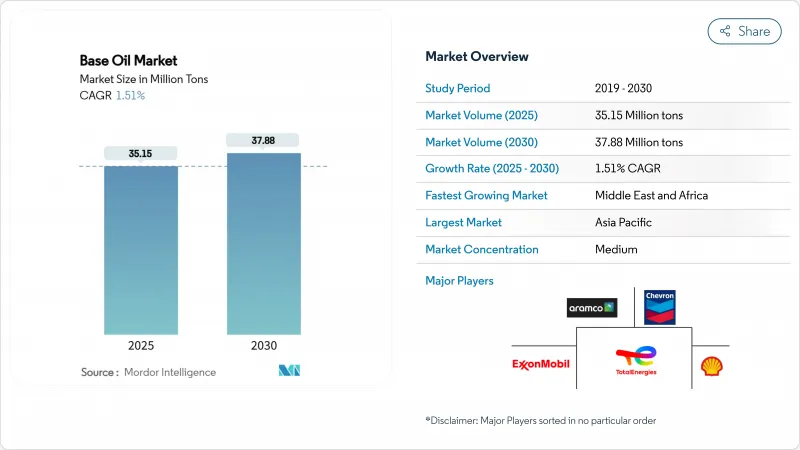

预计到 2025 年,基油市场规模将达到 3,515 万吨,到 2030 年将达到 3,788 万吨,预测期(2025-2030 年)的复合年增长率为 1.51%。

基油市场成长主要受三大因素驱动:一是基础油市场从I类到高性能II类和III类基础油的转变;二是全球排放法规日益严格;三是合成配方在电动车(EV)动力系统中的应用日益广泛。亚太地区销售量领先,但中东和非洲地区的成长速度最快,显示供应链正逐步向原油供应集中的地区调整。由于布兰特原油与杜拜原油价差收窄以及闭合迴路。

全球基油市场趋势与洞察

亚太地区生产群集的快速工业化

亚太地区製造业的蓬勃发展正支撑着基油市场需求成长的大部分。预计到2024年,中国原油日加工量将达到1,480万桶,将对金属加工液和液压油产生强劲的需求。日益壮大的炼油和石化一体化综合体网路将提升营运弹性,使生产商能够将产量比率转向盈利最高的基料等级。马来西亚国家石油公司(PETRONAS)在其2025-2027年的展望中预测,其基础油日产量将达到200万桶油当量(BOE),併计划在2028年通过生物炼製厂Start-Ups的启动,大力拓展下游特种化学品业务。这些投资将巩固该地区在基油市场的主导地位,并加速传统I类基础油产能的更新换代。

更严格的欧7和国七排放标准将提振对III/IV类车辆的需求。

欧盟7排放标准的实施要求汽车製造商在所有轻型汽油引擎上安装颗粒物过滤系统,推动了对超低挥发性III类润滑油的需求。中国的「中国七」排放标准也将加剧对低SAPS(硫磷灰石-磷灰石-苯乙烯类)润滑油的需求,同时,2022年至2026年间核准的44个炼油计划可望增强本地供应。将于2025年3月31日生效的ILSAC GF-7标准要求燃油经济性提高10%,促使调和商转向使用更高品质的基础油。 [ORONITE.COM] 这导致对加氢裂解装置和加氢异构化装置的资本投资增加,加速了基油市场的优质化。

布伦托夫/越南原油价差波动压力裕度

布兰特原油与杜拜原油的价差最快可能在2024年转为负值,这预示着中型含硫原油(VGO基油供应的关键原料)将出现短缺。科威特、阿曼和奈及利亚新建炼油厂带来的全球产能提升,压低了炼油厂利润率,并导致一些营运商(例如朗德尔巴塞尔休士顿炼油厂)在2025年初退出炼油厂业务。基油市场的独立炼油商被迫缩减营运规模或关闭老旧资产。

细分市场分析

2024年,II类基油将以42.89%的市占率持续维持领先地位,这主要得益于其均衡的性能成本比和完善的经销网络。壳牌公司在韦瑟林(Wesseling)的30万吨产能转化,也凸显了对加氢裂解油的持续信心。 III类基础油虽然目前绝对规模较小,但预计到2030年将以4.22%的复合年增长率成长,这主要得益于欧7排放标准和电动车冷却系统对超低挥发性和高抗氧化性的要求。因此,在预测期内,III类基础油的市场规模预计将比其他任何等级的基础油成长更快。

虽然在一些需要溶解性的领域,例如橡胶加工液和金属加工液,I类基础油仍然存在,但由于经济效益下降,其市场份额正在逐渐萎缩。 V类基础油凭藉其多样化的化学特性,包括用于生物润滑剂的仲多元醇酯,为创新铺平了道路。整体而言,基油市场正朝着更高的API等级发展,以满足更严格的OEM规格和永续性目标。

基油报告按基料类型(I类、II类、III类、IV类及其他)、应用领域(发动机油、变速箱及齿轮油、金属加工液、液压油、润滑脂及其他应用)和地区(亚太地区、北美地区、欧洲地区、南美地区、中东和非洲地区)进行细分。市场预测以百万吨为单位。

区域分析

亚太地区预计到2024年将占全球销售量的46.78%,这主要得益于中国原油日产量创纪录的1480万桶,以及印度计划于2025年前完成的190亿至220亿卢比的扩建项目。基油市场正受益于垂直整合的综合设施,这些设施可以根据净利率在燃料、化学品和基料之间灵活切换。日本和韩国将为电子产品的温度控管提供精密合成技术,而东南亚国家将增加产能以满足该地区的工业需求。

到2030年,中东和非洲的复合年增长率将达到3.48%,位居全球之首。阿布达比国家石油公司(ADNOC)投资35亿美元的鲁瓦伊斯原油灵活化计画将可加工更重的含硫原油,并优化II类和III类原油的生产。欧洲致力于压缩利润率和脱碳策略,其中包括在2026年前将道达尔能源公司的格拉姆皮茨油田改造为零原油平台。

北美正投资于特种PAO和III类计划,这主要得益于页岩油的经济效益。雪佛龙帕萨迪纳油田的升级改造将使每日处理能力提升至12.5万桶,同时提高喷射机燃料的灵活性。南美受益于巴西石化一体化带来的适度成长,但宏观经济的波动限制了大规模投资。整体而言,地域动态反映出产能正逐步向石油丰富、需求旺盛的地区扩散。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 亚太地区生产群集的快速工业化

- 更严格的欧7和国七排放标准将提振对III/IV类车辆的需求。

- 电动汽车温度控管系统推动了对高性能润滑油的需求

- 资料中心浸没式冷却剂(新型合成基料)的扩展

- 循环经济模式下闭合迴路炼油的经济学

- 市场限制

- 快速替换I类产能

- 布兰特原油与杜拜原油价差的波动对利润率带来压力。

- 欧盟即将把聚酰胺氧化物(PAOs)归类为微塑胶(欧洲化学品管理局)

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依基料

- 第一组

- 第二组

- 第三组

- 第四组

- 其他的

- 透过使用

- 机油

- 变速箱/齿轮油

- 金属加工油

- 油压

- 润滑脂

- 其他用途

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 印尼

- 越南

- 泰国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 埃及

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- ADNOC

- Chevron Corporation

- China Petrochemical Corporation(SINOPEC)

- CNOOC Limited

- Exxon Mobil Corporation

- Formosa Petrochemical Corporation

- Gazprom Neft PJSC

- GS Caltex Corporation

- Hindustan Petroleum Corporation Limited

- Indian Oil Corporation Ltd

- LUKOIL

- Nynas AB

- Petrobras

- PetroChina

- PETRONAS Lubricants International

- Philips 66 Company

- Repsol

- Saudi Arabian Oil Co.

- Sepahan Oil Company

- Shandong Qingyuan Group Co. Ltd.

- Shell plc

- SK Innovation Co. Ltd.

- TotalEnergies

第七章 市场机会与未来展望

The Base Oil Market size is estimated at 35.15 million tons in 2025, and is expected to reach 37.88 million tons by 2030, at a CAGR of 1.51% during the forecast period (2025-2030).

The measured growth of the base oil market is underpinned by three forces: the migration from Group I to higher-performance Group II and III stocks, tightening global emission rules, and the expanding role of synthetic formulations in electric-vehicle (EV) drivetrains. Asia-Pacific commands volume leadership, yet the Middle East and Africa records the fastest expansion, signaling a gradual realignment of supply chains toward crude-advantaged regions. Competitive positioning hinges on hydroprocessing technology, while refiners confront margin pressure from compressed Brent-Dubai spreads and rising capital outlays for catalyst upgrades. Opportunities emerge in immersion-cooling fluids for data centers and closed-loop re-refining initiatives that meet circular-economy targets.

Global Base Oil Market Trends and Insights

Rapid Industrialization Across APAC Production Clusters

Asia-Pacific's manufacturing boom underpins a significant share of incremental base oil market demand. China processed 14.8 million barrels per day of crude in 2024, creating robust pull for metal-working and hydraulic fluids. An expanding network of integrated refinery-petrochemical complexes increases operational flexibility, enabling producers to shift yields toward the most profitable base-stock grades. PETRONAS projects 2 million barrels of oil-equivalent output per day in its 2025-2027 outlook, with a downstream push into specialty chemicals supported by a biorefinery startup in 2028. These investments solidify the region's pre-eminence in the base oil market and accelerate the displacement of legacy Group I capacity.

Stricter Euro 7 and China VII Emission Norms Boosting Group III/IV Demand

The adoption of Euro 7 standards obliges automakers to fit particulate-filter systems across all light-duty gasoline engines, upping demand for ultra-low-volatility Group III stocks. China's parallel China VII framework intensifies the requirement for low-SAPS lubricants, while forty-four refining projects approved between 2022-2026 are poised to reinforce local supply. ILSAC GF-7, effective 31 March 2025, calls for a 10% fuel-economy gain, nudging blenders toward higher-quality base oils [ORONITE.COM]. Hydrocracking and hydro-isomerization units thus attract capital, accelerating the premiumization of the base oil market.

Volatile Brent-Dubai Crude Differentials Squeezing Margins

The Brent-Dubai spread turned negative at times in 2024, signaling scarce medium-sour barrels crucial for VGO-based base-oil feed. New Kuwait, Oman, and Nigeria refineries lifted global capacity, depressing margins and driving some operators, such as LyondellBasell Houston, to exit refining by early 2025. The crunch pressures independent players in the base oil market to trim runs or shutter older assets.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for High-Performance Lubricants in EV Thermal-Management Systems

- Expansion of Data-Center Immersion-Cooling Fluids

- Impending Micro-Plastic Classification of PAOs in the EU

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Group II maintained leadership with 42.89% of the base oil market share in 2024, owing to its balanced performance-cost equation and established distribution networks. Shell's 300,000-ton conversion at Wesseling underscores sustained confidence in hydrocracked stocks. Group III, though smaller on an absolute basis, advances at a 4.22% CAGR to 2030, buoyed by Euro 7 and EV-cooling mandates that call for ultra-low volatility and high oxidation resistance. The base oil market size for Group III is thus poised to expand faster than any other grade during the forecast horizon.

Group I endures in select rubber-processing and metal-working fluids requiring solvency, yet closures continue as economics deteriorate. Group V's diverse chemistries, including secondary polyol esters for bio-lubricants, round out innovation pathways. Altogether, the base oil market is migrating toward higher API groups to meet stricter OEM specifications and sustainability goals.

The Base Oil Report is Segmented by Base-Stock Type (Group I, Group II, Group III, Group IV, and Others), Application (Engine Oils, Transmission and Gear Oils, Metalworking Fluids, Hydraulic Fluids, Greases, and Other Applications), and Geography ( Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Million Tons).

Geography Analysis

Asia-Pacific generated 46.78% of 2024 volume, underpinned by China's record 14.8 million barrels-per-day crude runs and India's INR 1.9-2.2 lakh crore expansion program slated for completion by 2025. The base oil market benefits from vertically integrated complexes able to toggle between fuels, chemicals, and base stocks as margins dictate. Japan and South Korea supply precision synthetic technology for electronics thermal management, while Southeast Asian nations add capacity to serve regional industrial demand.

The Middle East and Africa posts a 3.48% CAGR to 2030, the fastest globally. ADNOC's USD 3.5 billion Ruwais Crude Flexibility Project enables processing heavier sour crudes, optimizing Group II and III output. Europe contends with margin compression and decarbonization pivots such as TotalEnergies' Grandpuits conversion into a zero-crude platform by 2026.

North America, bolstered by shale-oil economics, invests in specialty PAO and Group III projects; Chevron's Pasadena upgrade lifts throughput to 125,000 barrels per day while raising jet-fuel flexibility. South America enjoys moderate upside from Brazil's petrochemical integration, although macro volatility dampens large-scale investments. Collectively, geographic dynamics reflect a gradual diffusion of capacity into crude-advantaged and demand-rich locales while traditional centers adapt through specialization.

- ADNOC

- Chevron Corporation

- China Petrochemical Corporation (SINOPEC)

- CNOOC Limited

- Exxon Mobil Corporation

- Formosa Petrochemical Corporation

- Gazprom Neft PJSC

- GS Caltex Corporation

- Hindustan Petroleum Corporation Limited

- Indian Oil Corporation Ltd

- LUKOIL

- Nynas AB

- Petrobras

- PetroChina

- PETRONAS Lubricants International

- Philips 66 Company

- Repsol

- Saudi Arabian Oil Co.

- Sepahan Oil Company

- Shandong Qingyuan Group Co. Ltd.

- Shell plc

- SK Innovation Co. Ltd.

- TotalEnergies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid industrialisation across APAC production clusters

- 4.2.2 Stricter Euro 7 and China VII emission norms boosting Group III/IV demand

- 4.2.3 Rising demand for high-performance lubricants in EV thermal-management systems

- 4.2.4 Expansion of data-centre immersion-cooling fluids (novel synthetic base-stocks)

- 4.2.5 Closed-loop re-refining economics under circular-economy mandates

- 4.3 Market Restraints

- 4.3.1 Rapid substitution away from Group I capacities

- 4.3.2 Volatile Brent-Dubai crude differentials squeezing margins

- 4.3.3 Impending micro-plastic classification of PAOs in the EU (ECHA)

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Base-Stock Type

- 5.1.1 Group I

- 5.1.2 Group II

- 5.1.3 Group III

- 5.1.4 Group IV

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Engine Oils

- 5.2.2 Transmission and Gear Oils

- 5.2.3 Metalworking Fluids

- 5.2.4 Hydraulic Fluids

- 5.2.5 Greases

- 5.2.6 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Indonesia

- 5.3.1.7 Vietnam

- 5.3.1.8 Thailand

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Nordic Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 South Africa

- 5.3.5.6 Nigeria

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ADNOC

- 6.4.2 Chevron Corporation

- 6.4.3 China Petrochemical Corporation (SINOPEC)

- 6.4.4 CNOOC Limited

- 6.4.5 Exxon Mobil Corporation

- 6.4.6 Formosa Petrochemical Corporation

- 6.4.7 Gazprom Neft PJSC

- 6.4.8 GS Caltex Corporation

- 6.4.9 Hindustan Petroleum Corporation Limited

- 6.4.10 Indian Oil Corporation Ltd

- 6.4.11 LUKOIL

- 6.4.12 Nynas AB

- 6.4.13 Petrobras

- 6.4.14 PetroChina

- 6.4.15 PETRONAS Lubricants International

- 6.4.16 Philips 66 Company

- 6.4.17 Repsol

- 6.4.18 Saudi Arabian Oil Co.

- 6.4.19 Sepahan Oil Company

- 6.4.20 Shandong Qingyuan Group Co. Ltd.

- 6.4.21 Shell plc

- 6.4.22 SK Innovation Co. Ltd.

- 6.4.23 TotalEnergies

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Renewable/Bio-based PAO commercial scale-up

- 7.3 Integrated re-refining and virgin-base-oil hubs

基油市场按产品等级、基油、应用类型、最终用户产业和销售管道划分-2025-2030 年全球预测环烷基础油市场按产品类型、製程类型、包装类型、应用、分销管道和最终用途划分-2025-2030 年全球预测

基油市场按产品等级、基油、应用类型、最终用户产业和销售管道划分-2025-2030 年全球预测环烷基础油市场按产品类型、製程类型、包装类型、应用、分销管道和最终用途划分-2025-2030 年全球预测 全球环烷变压器油市场

全球环烷变压器油市场 搪光油市场预测至2032年:全球分析(按类型、基础油类型、黏度等级、销售管道、应用、最终用户和地区)

搪光油市场预测至2032年:全球分析(按类型、基础油类型、黏度等级、销售管道、应用、最终用户和地区) 2025年环烷基油全球市场报告2025年基油全球市场报告

2025年环烷基油全球市场报告2025年基油全球市场报告 日本基础油市场报告,按类型(矿物油、合成油、生物基油)、组别(第一组、第二组、第三组、第四组、第五组)、应用(汽车油、工业油、金属加工液、液压油、润滑脂等)和地区划分,2025 年至 2033 年

日本基础油市场报告,按类型(矿物油、合成油、生物基油)、组别(第一组、第二组、第三组、第四组、第五组)、应用(汽车油、工业油、金属加工液、液压油、润滑脂等)和地区划分,2025 年至 2033 年 2026-2032 年环烷基油市场规模(按黏度指数类型、应用和地区)基础油市场报告,按类型(矿物油、合成油、生物基油)、组别(第一组、第二组、第三组、第四组、第五组)、应用(汽车油、工业油、金属加工液、液压油、润滑脂等)和地区划分,2025 年至 2033 年

2026-2032 年环烷基油市场规模(按黏度指数类型、应用和地区)基础油市场报告,按类型(矿物油、合成油、生物基油)、组别(第一组、第二组、第三组、第四组、第五组)、应用(汽车油、工业油、金属加工液、液压油、润滑脂等)和地区划分,2025 年至 2033 年 再生基油市场报告:趋势、预测和竞争分析(至 2031 年)

再生基油市场报告:趋势、预测和竞争分析(至 2031 年)