|

市场调查报告书

商品编码

1852144

润滑脂:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Grease - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

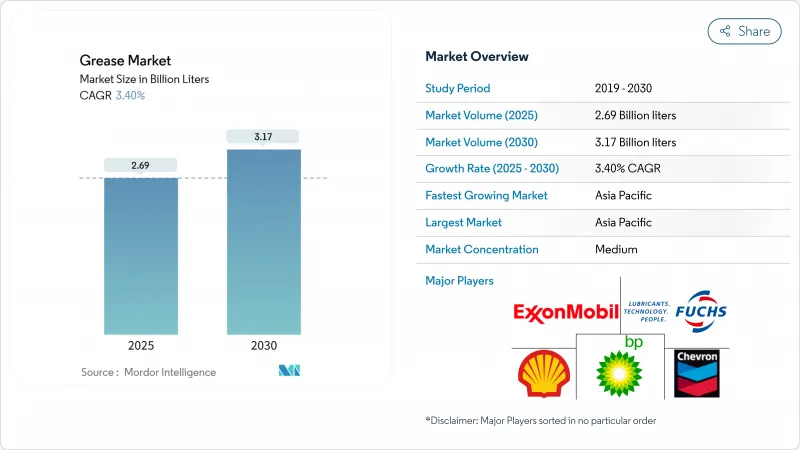

预计到 2025 年,润滑脂市场规模将达到 26.9 亿公升,到 2030 年将达到 31.7 亿公升,在预测期(2025-2030 年)内,复合年增长率将达到 3.40%。

增稠剂成分的变化更为活跃,钙基产品以9.10%的复合年增长率快速成长,开始动摇锂长期以来的主导地位。碳酸锂价格的波动、日益严格的环境法规以及电动车(EV)的技术需求,都在同时重塑买家的优先事项和供应商的产品组合。亚太地区凭藉着蓬勃发展的施工机械市场和全球成长最快的电动车製造基地,持续保持需求中心的地位。随着机械设计不断突破轴承、齿轮和密封件的传统应用范围,高温和极压等级的增稠剂正日益受到关注。

全球润滑脂市场趋势与洞察

欧盟和北美加工生产线中卫生食品级润滑剂的普及情况

随着加工商遵守FDA 21 CFR 178.3570和ISO 21469标准,对NSF H1认证润滑脂的需求正在加速成长。各工厂正转向「全H1」润滑脂方案,以消除交叉污染的风险;同时,合成基础油正在取代矿物油,以实现更高的耐温性(高达500°F)和更长的润滑週期。这一趋势在欧洲的麵包房、酪农和饮料厂尤为明显,这些工厂自2024年起将加强合规性检查。能够同时提供产品成分和工厂卫生认证的供应商正在赢得多厂区合同,从而确保稳定的供货量。

亚太地区电动车动力传动系统总成轴承采用锂基复合润滑脂和磺酸钙润滑脂

中国、韩国和印度电动车生产的快速发展正在重塑润滑脂配方要求。曾经转速为10,000转/分的轴承,如今转速已超过20,000转/分,并承受超过150 度C的热应力。实验室测试表明,磺酸钙润滑脂在接近600°F的温度下仍能保持稳定性,其性能比锂基复合润滑脂高出20%,同时还具有低电电阻。 2024年发布的OEM规范已将磺酸钙列为多款大众市场车型前后轴轴承的预设润滑脂。拥有稳定磺酸盐钙供应链的润滑脂生产商正抓住这一机会,争取签订多年期批量合约。

电池产业竞争导致碳酸锂成本波动

2021年至2024年,碳酸锂现货价格上涨。调查数据显示,锂精矿产量占全球总产量的比例在两年内从70%下降至60%,生产商目前正利用聚脲或钙基技术进行避险,以保障净利率。受季度润滑脂价格调整影响的买家正在寻求供应商多元化,以缓解现货短缺问题。一些汽车製造商正在预先核准磺酸钙润滑脂,以避免因锂基准价格波动而产生的合约中期附加税。

细分市场分析

到2024年,锂基润滑脂将占润滑脂市场的66%,而钙基润滑脂的销售量将以9.10%的复合年增长率成长。这种市场格局的转变源自于两大动态:锂价上涨以及钙基润滑脂优异的耐高温性能。製造商正在改造反应器生产线,以实现锂基和钙基润滑脂批次间的灵活切换,在降低原料风险的同时,确保产品代码核准客户要求。铝基复合润滑脂在船舶和造纸厂等应用领域,尤其是在防水润滑脂方面,仍占有重要地位。聚脲润滑脂通过去除金属皂来降低电阻,因此在对噪音敏感的电动车轴承应用中越来越受欢迎。由于聚脲润滑脂与传统锂基润滑脂不相容,终端用户对其广泛应用仍持谨慎态度,但OEM填充设备为快速提升销售提供了途径。

现场证据表明,中国风力发电机主轴承的润滑週期延长了30%,这进一步支持了磺酸钙润滑脂的广泛应用。与锂基复合润滑脂的比较测试证实,磺酸钙润滑脂具有更低的油水分离率和更优异的滴点性能,这对于在70°C以上峰值太阳辐射下运行的风力发电机而言是一项关键优势,即使机舱温度低于-20°C。生产商强调,钙的天然去污能力降低了添加剂的加工速度,从而节省了成本,部分抵消了磺酸盐成本的上涨。最终,增稠剂市场正日益细分为多种化学成分的产品组合,锂、钙、铝和聚脲等增稠剂各自在润滑脂市场中占据独特的性能优势。

预计到2024年,矿物油润滑脂将占据润滑脂市场75%的份额,而合成润滑脂预计将以4.90%的复合年增长率成长。聚α烯烃(PAO)基润滑脂因其氧化稳定性和宽广的温度范围,在合成润滑脂领域占据主导地位。美孚航空润滑脂SHC 100的使用温度范围为-54 ℃至177 ℃,其性能优势已获得航太原始设备製造商(OEM)的认可。生物植物来源酯类润滑脂在ASTM标准测试中,其抗氧化寿命已可与III类矿物油相媲美。

矿物油润滑脂能够满足底盘润滑和工业开式齿轮传动等对价格敏感的应用领域的需求,并符合NLGI(美国国家润滑脂协会)的建议标准。然而,现代高速生产线不断变化的运行温度要求,使得买家即使在中等应用领域也开始指定使用合成油和半合成油。了解PAO和酯类润滑脂中复杂添加剂溶解性的供应商,能够在特种润滑脂和食品级润滑脂市场中获得高于平均的利润。

区域分析

到2024年,亚太地区将占全球销售量的49%,年复合成长率达4.32%,是欧洲成长率的两倍。中国的製造业群聚、印度快速发展的基础设施以及东南亚的电动车零件产业群聚均保持着较高的运转率。壳牌决定将其位于泰国的润滑脂工厂产能提高三倍,达到每年1.5万吨,这充分体现了该地区的强劲发展势头。预计到2030年,亚太地区在全球润滑脂市场的占有率将达到52%,进一步巩固在该领域的领先地位。

北美地区在全球润滑油需求中占据很大份额,这主要得益于蓬勃发展的食品加工业和蓬勃发展的可再生能源项目。风电场的建造推动了对轮毂高度超过100公尺、维护週期为五年的合成润滑油的需求。监管机构对环保润滑油的重视,促使五大湖区和沿海航线的船舶业者将货物绞车点更换为符合EAL认证标准的润滑脂。

欧洲占了较大的销售量,但也面临最严格的监管挑战。 PFAS法规已促使汽车、航太和机械设备原始设备製造商(OEM)对供应商审核。能够提供不含PFAS且不牺牲可靠性的替代方案的供应商有望保持其市场份额。预计到2024年,南美洲以及中东和非洲的需求份额将较小。自动润滑系统的低普及率将推高单位消费量,但资金限制正在减缓技术升级。提供改装方案的服务供应商可以利用这种销售不平衡,加速润滑脂市场这些新兴领域的成长。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 食品级卫生润滑剂在欧盟和北美加工生产线上的普及

- 电动车动力传动系统总成轴承向锂基复合润滑脂和磺酸钙润滑脂过渡

- 在深海钻井中使用防水润滑脂。

- 印度和东协的施工机械热潮推动了极压润滑脂的需求。

- 电力业投资强劲成长

- 市场限制

- 电池产业竞争导致碳酸锂成本波动

- 欧盟REACH法规对PFAS和氮化硼添加剂的限制

- 自动润滑系统在非洲和南美洲的普及率较低

- 价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模和成长预测(价值和数量)

- 透过增稠剂

- 锂基

- 钙基

- 铝底座

- 聚脲

- 其他增稠剂

- 依产品类型

- 矿物油

- 合成油

- 生物基油

- 按表现等级

- 高温润滑脂

- 低温和极地级润滑脂

- 极压/高负荷润滑脂

- 按最终用户行业划分

- 汽车和其他交通工具

- 发电(风能、水力、火力)

- 重型机械

- 食品/饮料

- 冶金/金属加工

- 化学製造

- 其他行业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 印尼

- 马来西亚

- 泰国

- 越南

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 其他南美洲国家

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 埃及

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Ampol Limited

- Axel Christiernsson AB

- BECHEM Lubrication Technology LLC

- BP plc

- Chevron Corporation

- China Petrochemical Corporation

- DuPont

- ENEOS Corporation

- ETS Oil & Gas Ltd.

- Exxon Mobil Corporation

- FUCHS

- Gazprom

- Gulf Oil International Ltd

- Idemitsu Kosan Co.,Ltd.

- Kluber Lubrication SE

- LUKOIL

- Morris Lubricants

- Orlen Oil

- Penrite Oi

- Petromin

- Petronas Lubricants International

- Saudi Arabian Oil Co.

- Shell Plc

- TotalEnergies

第七章 市场机会与未来展望

The Grease Market size is estimated at 2.69 Billion liters in 2025, and is expected to reach 3.17 Billion liters by 2030, at a CAGR of 3.40% during the forecast period (2025-2030).

Volume growth is steady rather than spectacular, yet the change in thickener mix is far more dynamic, with calcium-based products expanding at 9.10% CAGR and starting to chip away at lithium's long-held dominance. Price volatility for lithium carbonate, tightening environmental regulation and the technical needs of electric vehicles (EVs) are simultaneously reshaping buyer priorities and supplier portfolios. Asia Pacific maintains its role as the fulcrum of demand, propelled by construction equipment activity and the world's fastest-growing EV production base. High-temperature and extreme-pressure grades are capturing increasing attention as machinery designs push bearings, gears and seals far beyond traditional service envelopes.

Global Grease Market Trends and Insights

Hygienic Food-Grade Lubrication Uptake in EU & North America Processing Lines

Demand for NSF H1-registered greases is accelerating as processors align with FDA 21 CFR 178.3570 and ISO 21469 standards. Facilities are migrating to "all-H1" programs to eliminate the risk of cross-contamination, and synthetic base fluids are replacing mineral oils to achieve higher temperature resilience-up to 500 °F continuous service-and longer relubrication intervals. The trend is most evident in European bakeries, dairies and beverage plants, where compliance checks have tightened since 2024. Suppliers able to certify both product composition and plant hygiene are winning multi-site contracts that secure recurring volume.

EV e-Powertrain Bearing Shift to Lithium-Complex & Calcium-Sulfonate Greases in APAC

Rapid EV output in China, Korea and India is reshaping formulation requirements. Bearings that once ran at 10,000 rpm now exceed 20,000 rpm, pushing thermal loads beyond 150 °C. Laboratory tests show calcium-sulfonate greases sustaining consistency at dropping points near 600 °F, a 20% margin over lithium-complex alternatives, while also exhibiting lower electrical impedance. OEM specification sheets published in 2024 already list calcium-sulfonate as the default for front-and-rear e-axle bearings in several mass-market models. Grease producers with secure calcium sulfonate supply chains are using this window to lock in multi-year volume contracts.

Lithium Carbonate Cost Volatility Due to Battery-Sector Competition

Lithium carbonate spot prices climbed between 2021 and 2024. Survey data show lithium thickeners dropped from 70% of global output to 60% in two years, and producers now hedge with polyurea or calcium technologies to protect margins. Grease buyers exposed to quarterly price resets have diversified suppliers to mitigate spot shortages. Some automotive lines are pre-approving calcium-sulfonate greases to avoid mid-contract surcharges tied to lithium benchmarks.

Other drivers and restraints analyzed in the detailed report include:

- Offshore Deep-Water Drilling Boosting Water-Resistant Marine Greases

- Construction Equipment Boom in India & ASEAN Driving Extreme-Pressure Greases

- EU REACH Tightening on PFAS & Boron-Nitride Additives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-based products still accounted for 66% of the grease market in 2024, but calcium-based volumes are advancing at a 9.10% CAGR. This realignment is rooted in the dual dynamics of lithium price spikes and superior high-temperature resilience offered by calcium chemistries. Manufacturers are recalibrating reactor lines to flex between lithium and calcium batches, mitigating feedstock risk while preserving customer-approved product codes. Aluminum complex greases retain relevance in marine and paper-mill water-resistance niches. Polyurea grades gain traction in noise-sensitive EV bearing applications where the absence of metal soaps reduces electrical impedance. End users remain cautious about widespread polyurea adoption due to incompatibility with legacy lithium greases, but OEM-filled units present a fast-track pathway to volume growth.

Calcium-sulfonate's acceptance is further boosted by field evidence showing a 30% extension in relubrication intervals on wind turbine main bearings in China. Benchmark testing against lithium-complex rivals confirmed lower oil separation and superior drop-point performance-a critical advantage in turbines operating at nacelle temperatures below -20 °C yet experiencing sun-exposed peaks above 70 °C. Producers emphasize that calcium's natural detergency properties lower additive treat rates, yielding cost savings that partially offset higher sulfonate acid costs. Ultimately, the thickener landscape is fragmenting into multi-chemistry portfolios in which lithium, calcium, aluminum and polyurea each defend distinct performance niches within the grease market.

Mineral-oil greases represented 75% of the grease market share in 2024 and the synthetic grades is forecast to rise at 4.90% CAGR. Polyalphaolefin (PAO) bases dominate the synthetic pool thanks to oxidation stability and broad temperature envelopes. Mobil Aviation Grease SHC 100, qualified from -54 °C to 177 °C, exemplifies the performance advantage recognized by aerospace OEMs. Bio-based oils enjoy legislative tailwinds from EAL mandates and voluntary ESG programs. Vegetable-derived esters blended with antioxidant packages now rival Group III mineral oils on oxidative life in standard ASTM tests.

Mineral-oil greases keep price-sensitive applications such as chassis lubrication and industrial open-gear drives aligned with NLGI-recommended practices. However, the operating temperature swing required by modern high-speed production lines is pushing buyers to spec synthetics or semi-synthetics even in mid-range duty. Suppliers that master complex additive solubility in PAO and ester packages are positioned to capture above-average margins across specialty and food-grade segments of the grease market.

The Grease Market Report Segments the Industry by Thickener (Lithium-Based, Calcium-Based, and More), Product Type (Mineral Oil, Synthetic Oil, and More), Performance Grade (High-Temperature Greases, Low-Temperature and Arctic-Grade Greases, and More), End-User Industry (Automotive and Other Transportation, Power Generation, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

Geography Analysis

Asia Pacific retained 49% of global volume in 2024 and is expanding at a 4.32% CAGR, twice the pace of Europe. China's manufacturing complex, India's infrastructure surge and Southeast Asia's EV component clustering keep utilization rates high. Shell's decision to triple grease plant capacity in Thailand to 15,000 tonnes per year underscores the region's pull. The region's share of the grease market size is expected to touch 52% by 2030, cementing its structural leadership.

North America holds a significant share of the total volume, supported by robust food processing and a booming renewable power pipeline. Wind farm buildout has lifted demand for synthetics that can last five-year maintenance cycles at hub heights above 100 m. Regulatory emphasis on environmentally acceptable lubricants is pushing marine operators on the Great Lakes and coastal routes to convert cargo-winch points to EAL-certified greases.

Europe holds a significant share of the volume but faces the most stringent regulatory challenges. The PFAS restriction docket has triggered supplier audits across automotive, aerospace and machinery OEMs. Suppliers that demonstrate PFAS-free alternatives without sacrificing reliability are poised to keep share. South America and the Middle East & Africa together contribute a small share of 2024 demand. Low penetration of automatic lubrication systems raises per-unit grease consumption, but capital constraints slow technology upgrades. Service providers with retrofit solutions can leverage the volume imbalance to fast-track growth in these frontier segments of the grease market.

- Ampol Limited

- Axel Christiernsson AB

- BECHEM Lubrication Technology LLC

- BP p.l.c.

- Chevron Corporation

- China Petrochemical Corporation

- DuPont

- ENEOS Corporation

- ETS Oil & Gas Ltd.

- Exxon Mobil Corporation

- FUCHS

- Gazprom

- Gulf Oil International Ltd

- Idemitsu Kosan Co.,Ltd.

- Kluber Lubrication SE

- LUKOIL

- Morris Lubricants

- Orlen Oil

- Penrite Oi

- Petromin

- Petronas Lubricants International

- Saudi Arabian Oil Co.

- Shell Plc

- TotalEnergies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hygienic Food-Grade Lubrication Uptake in EU and North-America Processing Lines

- 4.2.2 EV e-Powertrain Bearing Shift to Lithium-Complex and Calcium-Sulfonate Grease

- 4.2.3 Offshore Deep-Water Drilling Boosting Water-Resistant Marine Grease

- 4.2.4 Construction Equipment Boom in India and ASEAN Driving Extreme-Pressure Grease

- 4.2.5 Robust Growth of Investments in the Power Generation Sector

- 4.3 Market Restraints

- 4.3.1 Lithium Carbonate Cost Volatility Due to Battery-Sector Competition

- 4.3.2 EU REACH Tightening on PFAS and Boron-Nitride Additives

- 4.3.3 Low Penetration of Auto-Lubrication Systems in Africa and South America

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Thickener

- 5.1.1 Lithium-based

- 5.1.2 Calcium-based

- 5.1.3 Aluminum-based

- 5.1.4 Polyurea

- 5.1.5 Other Thickeners

- 5.2 By Product type

- 5.2.1 Mineral Oil

- 5.2.2 Synthetic Oil

- 5.2.3 Bio-based Oil

- 5.3 By Performance Grade

- 5.3.1 High-Temperature Grease

- 5.3.2 Low-Temperature and Arctic-Grade Grease

- 5.3.3 Extreme-Pressure and Heavy-Load Grease

- 5.4 By End-user Industry

- 5.4.1 Automotive and Other Transportation

- 5.4.2 Power Generation (Wind, Hydro, Thermal)

- 5.4.3 Heavy Equipment

- 5.4.4 Food and Beverage

- 5.4.5 Metallurgy and Metalworking

- 5.4.6 Chemical Manufacturing

- 5.4.7 Other Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Indonesia

- 5.5.1.6 Malaysia

- 5.5.1.7 Thailand

- 5.5.1.8 Vietnam

- 5.5.1.9 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordics

- 5.5.3.7 Turkey

- 5.5.3.8 Russia

- 5.5.3.9 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Nigeria

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Ampol Limited

- 6.4.2 Axel Christiernsson AB

- 6.4.3 BECHEM Lubrication Technology LLC

- 6.4.4 BP p.l.c.

- 6.4.5 Chevron Corporation

- 6.4.6 China Petrochemical Corporation

- 6.4.7 DuPont

- 6.4.8 ENEOS Corporation

- 6.4.9 ETS Oil & Gas Ltd.

- 6.4.10 Exxon Mobil Corporation

- 6.4.11 FUCHS

- 6.4.12 Gazprom

- 6.4.13 Gulf Oil International Ltd

- 6.4.14 Idemitsu Kosan Co.,Ltd.

- 6.4.15 Kluber Lubrication SE

- 6.4.16 LUKOIL

- 6.4.17 Morris Lubricants

- 6.4.18 Orlen Oil

- 6.4.19 Penrite Oi

- 6.4.20 Petromin

- 6.4.21 Petronas Lubricants International

- 6.4.22 Saudi Arabian Oil Co.

- 6.4.23 Shell Plc

- 6.4.24 TotalEnergies

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Growing Usage of Polyurea Greases

润滑脂市场:按类型、应用、硬度和基础油划分-2026-2032年全球市场预测润滑脂市场:2026-2032年全球市场预测(依产品类型、基础油、增稠剂类型、包装、分销管道及应用划分)非锂基润滑脂市场:按类型、包装、应用、终端用户产业和销售管道划分-2026-2032年全球市场预测

润滑脂市场:按类型、应用、硬度和基础油划分-2026-2032年全球市场预测润滑脂市场:2026-2032年全球市场预测(依产品类型、基础油、增稠剂类型、包装、分销管道及应用划分)非锂基润滑脂市场:按类型、包装、应用、终端用户产业和销售管道划分-2026-2032年全球市场预测 润滑脂市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年

润滑脂市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年 油脂分析仪市场分析及预测(至2035年):依类型、产品类型、服务、技术、应用、最终用户、功能、安装类型、设备分类

油脂分析仪市场分析及预测(至2035年):依类型、产品类型、服务、技术、应用、最终用户、功能、安装类型、设备分类 2026年全球锂基润滑脂市场报告全氟聚醚润滑脂市场(依增稠剂类型、NLGI等级、黏度等级、添加剂功能、应用、终端用户产业和销售管道),全球预测,2026-2032年全球高温氟化润滑脂市场按形态、NLGI等级、包装、应用和最终用途产业划分,2026-2032年预测油脂袋市场:按材料、类型、应用、最终用户和通路划分-2026-2032年全球预测

2026年全球锂基润滑脂市场报告全氟聚醚润滑脂市场(依增稠剂类型、NLGI等级、黏度等级、添加剂功能、应用、终端用户产业和销售管道),全球预测,2026-2032年全球高温氟化润滑脂市场按形态、NLGI等级、包装、应用和最终用途产业划分,2026-2032年预测油脂袋市场:按材料、类型、应用、最终用户和通路划分-2026-2032年全球预测 日本润滑脂市场报告(按增稠剂类型、基础油、最终用户和地区划分,2026-2034年)

日本润滑脂市场报告(按增稠剂类型、基础油、最终用户和地区划分,2026-2034年)