|

市场调查报告书

商品编码

1906009

医用气体及设备:市场占有率分析、产业趋势及统计、成长预测(2026-2031)Medical Gases And Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

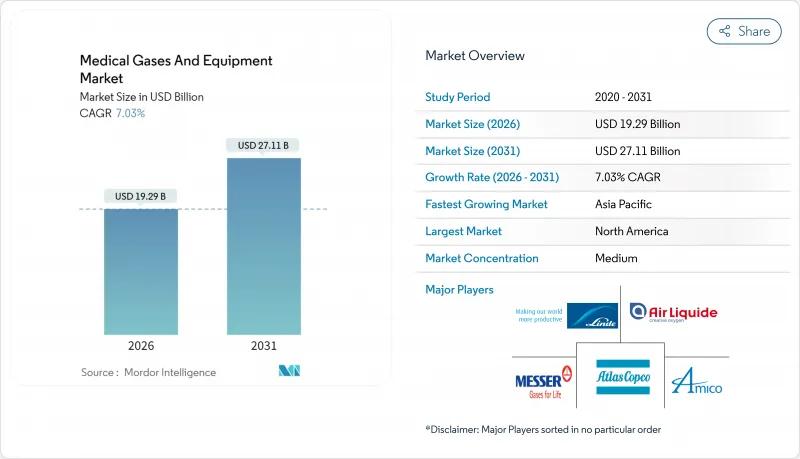

预计医用气体和设备市场将从 2025 年的 180.2 亿美元成长到 2026 年的 192.9 亿美元,到 2031 年将达到 271.1 亿美元,2026 年至 2031 年的复合年增长率为 7.03%。

人口老化带来的治疗需求不断增长、新冠疫情后医院基础设施的持续升级以及携带式製氧机技术的快速创新,共同推动了医用气体和设备市场的持续扩张。政府支持的氧气供应稳定计划、可穿戴感测器的微型化以及低全球暖化潜值(GWP)麻醉气体混合物的商业化,进一步促进了需求成长。同时,综合气体供应商正利用规模经济优势,与各大急诊护理机构签订长期合约。设备製造商市场依然分散,这为透过收购来深化产品系列、建构地域多元化的服务网络提供了空间,尤其是在高速成长的亚太市场。居家医疗的持续发展,推动了对气瓶充装、小规模现场製氧以及基于人工智慧的监测的需求,这些因素共同塑造了医用气体和设备市场的竞争格局。

全球医用气体及设备市场趋势与展望

对居家医疗和床边氧气疗法的需求不断增长

联邦医疗保险(Medicare)的36个月租赁框架支持可预测的报销,鼓励医疗服务提供者投资携带式设备,并提高患者对家庭氧气疗法的接受度。 FlexO2流量选择器等技术使用户主导调节次数翻了一番,并且自临床应用以来,患者的感知活动能力评分提高了80分。配备优化沸石床的携带式製氧机氧气精度现已达到98.68%,缩小了与固定式系统的性能差距。家庭护理领域13.01%的复合年增长率表明,这些改进与患者对熟悉环境的偏好相符。 2025年居家照护服务中心(CMS)的支付改革将使居家医疗费用增加2.5%,这将进一步推动分散式照护模式的发展。林德公司针对睡眠呼吸中止症患者的AIRGENIOUS试点计画降低了持续性正压呼吸器(CPAP)治疗的依从性,并证明了预测分析在提高慢性病照护遵从性方面的有效性。

呼吸系统疾病呈上升趋势

慢性阻塞性肺病(COPD)仍是导致病人需要吸氧住院的主要原因,占三级医院呼吸科病房病人总数的44.5%。典型的床位气体需求量平均每年为350立方公尺氧气和325立方公尺医用空气,并且随着出院病患人数和手术量的增加呈线性增长。欧洲规划者已将医用气体系统升级纳入国家呼吸系统策略,正如奥地利2025年总体规划所概述的。对疫情期间需求激增的分析表明,氧气消费量增加了高达20倍,凸显了供应基础设施永久性冗余的必要性。波兰的「医疗需求地图」倡议展示了呼吸系统疾病地图如何指导医院层面的气体系统投资。

严格遵守多司法管辖区的cGMP和药典要求

美国食品药物管理局(FDA)的最终规则将于2025年12月生效,届时将要求医用气体供应商全面遵守现行药品生产品质管理规范(cGMP)和标籤通讯协定,并需投资更新其填充和分析系统。香港将于2026年6月起将医用气体归类为药品,并引进新的经销商许可製度。同时,相关修订将协调基于ISO标准的医疗设备品管与cGMP的细化,以增加跨境规成本为代价,促进全球标准的趋同。

细分市场分析

到2025年,纯医用气体将占医用气体和设备市场的37.12%,这反映了其在从医院到家庭护理等各种治疗应用中的重要性。受居家医疗日益普及和呼吸系统疾病发病率上升的推动,氧气预计将以8.82%的复合年增长率增长。医用空气、二氧化碳、氦气和特种气体可用于手术充气、诊断和磁振造影,但氦气供应的波动导致价格上涨,对医院预算造成压力。加州大学旧金山分校(UCSF)成功地将氧化亚氮的消耗量减少了80-90%,促使各医疗机构转向使用便携式气瓶,以减少管道连接和废弃物排放。

配套的医用气体设备涵盖压缩机、气瓶以及管道监测系统等。阿特拉斯·科普柯于2023年收购Medi-teknique,便是产业整合旨在拓展服务范围和持续维护收入的一个例证。 Beacon Medies的全球分销网路将真空和歧管系统整合到新建医院中,并透过多模光纤环网实现即时警报功能。日益增长的永续性意识正推动医院采用低全球暖化潜势(GWP)的麻醉气体混合物。由于DESFLURANE的全球暖化潜势值显着低于地氟烷,欧洲监管机构建议使用SEVOFLURANE,这迫使供应商重新设计挥发性气体的回收和清除系统。

儘管到2025年,包装式氧气瓶仍将保持45.05%的市场份额,但受患者对移动性需求以及医疗机构对经济高效的慢性病护理模式的重视,可携式製氧机预计将以每年9.67%的速度增长。德克萨斯农工大学的计算设计表明,动态沸石成分可以调节氧气流量以满足患者不断变化的需求,从而在不牺牲纯度的前提下减轻重量。同时,林德公司在2024年获得了59份小规模现场製氧设备订单,这反映出医院对自主型氧气供给能力的兴趣,以应对供应中断的情况。

大型三级医院为了追求可预测的单位成本,仍然倾向于现场批量生产,而需要超高纯度医用气体的专科医疗中心则更倾向于液态批量供应。持续的钢瓶备用需求确保了所有治疗方式的稳定需求,从而巩固了医用气体和设备市场的多元化收入来源。

区域分析

北美地区预计到2025年将占全球收入的35.25%,这得益于其成熟的支付系统、严格的FDA监管以及携带式製氧机的广泛应用。随着医院透过现场储氧罐维持氧气供应的冗余,以及CMS不断完善报销机制,居家医疗的普及率持续成长。该地区的设备供应商受益于清晰的监管路径,该路径既认可创新,又避免了模糊的市场进入规则。

亚太地区预计将以13.19%的复合年增长率增长,在所有地区中位居榜首,这主要得益于大规模医院扩建、人口老龄化以及政府对医疗基础设施的大力投入。印度计画新增17,800张病床,并制定了价值500亿美元的医疗设备蓝图,显示管道系统和气瓶的需求可能激增。中国自2024年起实施的扶持性采购政策预计将在2025年提振医疗设备支出,进一步巩固该地区作为关键成长引擎的地位。林德和梅塞尔在印度和东南亚地区的空气分离装置扩建项目,体现了供应商致力于维护区域供应稳定的决心。

欧洲仍然是关键市场,这主要得益于严格的环境法规,这些法规正在加速低全球暖化潜势(GWP)麻醉剂的普及应用。英国国民医疗服务体系(NHS)逐步淘汰地DESFLURANE的倡议在整个欧洲大陆产生了连锁反应,迫使供应商改变配方,并促使医院升级復苏室系统。液化空气集团在法国、德国和巴西签订的低碳氧气供应合约凸显了范围3排放在公立医院采购标准中日益增长的重要性。

中东/非洲和南美洲都是具有高潜力的早期市场。对三级医疗机构的投资以及药典标准的逐步统一将创造新的机会,但经济波动和分散的报销体系将限制短期内的扩张。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 对居家医疗和床边氧气疗法的需求不断增长

- 呼吸系统疾病呈上升趋势

- 新冠疫情后政府资助的氧气基础设施

- 携带式和可穿戴式浓度设备和感测器的微型化

- 环境友善、低全球暖化潜值麻醉气体混合物的商业化

- 基于人工智慧的天然气管道预测监测和库存管理

- 市场限制

- 严格遵守多司法管辖区的cGMP和药典要求

- 长期家庭氧气疗法的报销有限

- 散装气体处理中的职场安全责任和保险成本。

- 氦气供应的不确定性推高了特种气体成本

- 波特五力分析

- 新进入者的威胁

- 买方/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(金额:美元)

- 副产品

- 医用气体

- 纯医用气体

- 氧

- 氧化亚氮

- 医用空气

- 二氧化碳

- 氦气和特种气体

- 医用气体混合物

- 生物环境

- 纯医用气体

- 医用气体设备

- 压缩机

- 圆柱

- 软管组件和阀门

- 面罩和套管

- 吸力系统

- 歧管和管路系统

- 警报和监控系统

- 医用气体

- 按模式

- 大规模现场发电

- 包装汽缸

- 液体/散装货物运输

- 可携式製氧机

- 透过使用

- 治疗

- 诊断和影像

- 製药生产与研究

- 冷冻手术和冷冻疗法

- 居家医疗

- 最终用户

- 医院

- 门诊手术中心

- 居家照护环境

- 学术和研究机构

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 亚太其他地区

- 中东和非洲

- GCC

- 南非

- 其他中东和非洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第六章 竞争情势

- 市场集中度

- 市占率分析

- 公司简介

- Linde plc

- Air Liquide

- Air Products & Chemicals

- Messer Group

- Taiyo Nippon Sanso

- Atlas Copco

- BeaconMedaes

- Amico Group

- Matheson Tri-Gas

- GCE Group

- NOVAIR

- Luxfer Gas Cylinders

- Getinge AB

- Dragerwerk AG

- INOX Air Products

- South African Oxygen(Afrox)

- Gulf Cryo

- Coregas Pty

- SOL Group

- Air Water Inc.

- Invacare Corporation

第七章 市场机会与未来展望

The Medical Gases And Equipment Market is expected to grow from USD 18.02 billion in 2025 to USD 19.29 billion in 2026 and is forecast to reach USD 27.11 billion by 2031 at 7.03% CAGR over 2026-2031.

Rising therapeutic demand from aging populations, steady hospital infrastructure upgrades after COVID-19, and rapid innovation in portable concentrators underpin sustained expansion of the medical gases and equipment market. Government-supported oxygen resilience projects, miniaturization of wearable sensors, and the commercialization of low-GWP anesthetic blends further reinforce volume growth, while consolidated gas suppliers leverage scale to secure long-term contracts across acute-care settings. Equipment makers remain fragmented, creating space for bolt-on acquisitions that deepen product portfolios and geographically diversified service footprints, especially in high-growth Asia-Pacific markets. The continued shift toward home-based care amplifies cylinder refilling, small on-site generation, and AI-enabled monitoring demand, collectively shaping the competitive contours of the medical gases and equipment market.

Global Medical Gases And Equipment Market Trends and Insights

Rising Demand for Home Healthcare & POC Oxygen Therapy

Medicare's 36-month rental framework underpins predictable reimbursement, encouraging supplier investment in portable devices and reinforcing patient acceptance of at-home oxygen therapy.Technology such as FlexO2 flow selectors has doubled user-initiated adjustments, raising perceived activity capacity scores by 80 points after clinical deployment.Portable concentrators that use optimized zeolite beds now deliver 98.68% oxygen accuracy, narrowing the performance gap with stationary systems. A 13.01% CAGR in the home-care segment illustrates how these improvements align with patient preference for familiar environments. CMS's 2025 payment update, lifting home health rates by 2.5% adds further momentum to decentralized care models. Linde's AIRGENIOUS pilot among sleep-apnea users cut CPAP non-compliance, showcasing predictive analytics for chronic-care adherence.

Growing Prevalence of Respiratory Diseases

COPD remains the chief driver of oxygen admissions, representing 44.5% of respiratory ward volume in tertiary hospitals. Typical bed-based gas demand averages 350 m3 oxygen and 325 m3 medical air each year, scaling directly with discharge volumes and surgical intensity. European planners have already embedded medical gas system upgrades into national respiratory strategies, as shown in the Austrian Masterplan 2025. Analysis of pandemic surges revealed oxygen consumption rising up to 20-fold, anchoring the need for permanent redundancy in supply infrastructure. Poland's Maps of Health Needs initiative highlights how respiratory disease mapping guides investment in gas systems at hospital level.

Stringent Multi-Jurisdictional cGMP & Pharmacopeia Compliance

The FDA's final rule, effective December 2025, mandates full current good manufacturing practice and labeling protocols for medical gases, compelling suppliers to invest in upgraded filling and analytical systems. Hong Kong will classify medical gases as pharmaceutical products from June 2026, introducing a new licensing layer for distributors. Parallel amendments harmonize ISO-based device quality management with cGMP clarifications, raising cross-border compliance costs yet fostering global standard convergence.

Other drivers and restraints analyzed in the detailed report include:

- Government-Funded Oxygen Infrastructure Build-Outs Post-COVID

- Miniaturization of Portable/Wearable Concentrators & Sensors

- Limited Reimbursement for Long-Term Home Oxygen Therapy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pure Medical Gases captured 37.12% of the medical gases and equipment market in 2025, reflecting indispensable therapeutic use across hospitals and home settings. Oxygen is projected to record an 8.82% CAGR, aided by expanding home-care adoption and respiratory disease prevalence. Medical Air, Carbon Dioxide, and Helium & Specialty Gases serve surgical insufflation, diagnostics, and MRI needs, though helium supply volatility has driven price escalations that strain hospital budgets. Nitrous Oxide consumption is shifting toward portable cylinders as institutions remove piped lines to curb waste, following UCSF's 80-90% reduction success.

Complementary medical gas equipment ranges from compressors and cylinders to pipeline monitoring systems. Atlas Copco's 2023 Medi-teknique acquisition illustrates consolidation aimed at service breadth and recurring maintenance revenue. BeaconMedaes' global distributor network embeds vacuum and manifold systems within new hospital builds, leveraging multi-mode optical fiber ring networks for real-time alarm capabilities. A rising focus on sustainability is prompting hospitals to adopt low-GWP anesthetic blends. European regulators endorse sevoflurane over desflurane because of its far lower global-warming potential, nudging suppliers to re-engineer recovery and scavenging systems for volatile agents.

Packaged Cylinders retained a 45.05% share in 2025, yet Portable Concentrators are forecast to grow 9.67% annually as patients demand mobility and healthcare providers emphasize cost-effective chronic-care models. Computational design by Texas A&M shows that dynamic zeolite configurations can tailor oxygen flow to fluctuating patient needs, reducing weight without cutting purity. Meanwhile, Linde recorded 59 small on-site plant wins in 2024, reflecting hospital interest in self-reliant oxygen capacity to hedge against supply disruptions.

Bulk on-site generation continues to attract large tertiary hospitals seeking predictable unit costs, whereas liquid bulk delivery supports specialty centers with ultra-high purity requirements. The continued preference for cylinder backup ensures steady demand across every modality, cementing a diversified revenue mix within the medical gases and equipment market.

The Medical Gases and Equipment Market Report is Segmented by Product (Medical Gases [Pure Medical Gases, and More], and Medical Gas Equipment [Compressors, and More]), Modality (Bulk On-Site Generation, and More), Application (Therapeutic, and More), End User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 35.25% of 2025 revenue, anchored by mature payer systems, strict FDA oversight, and widespread adoption of portable concentrators. Hospitals maintain redundant oxygen generation backed by on-site bulk tanks, while home-care penetration continues to rise as CMS refines reimbursement. Regional equipment vendors benefit from clear regulatory pathways that reward innovation without ambiguous market access rules.

Asia-Pacific is projected to grow at 13.19% CAGR, the highest among all regions, driven by large-scale hospital expansion, aging populations, and proactive government funding for medical infrastructure. India's planned capacity additions of 17,800 beds alongside a USD 50 billion medical device roadmap illustrate the underlying demand surge for pipeline systems and cylinders. China's supportive procurement policies post-2024 are expected to unlock medical device spending in 2025, reinforcing the region's status as the foremost growth engine. Air separation unit expansions by Linde and Messer across India and Southeast Asia signal supplier commitment to sustaining regional supply security.

Europe remains a major market, propelled by stringent environmental mandates that accelerate low-GWP anesthesia adoption. The NHS elimination of desflurane has cascaded across continental practice, compelling suppliers to reformulate and hospitals to upgrade recovery systems. Air Liquide's low-carbon oxygen supply contracts in France, Germany, and Brazil showcase the rising importance of Scope 3 emissions in public hospital procurement criteria.

Middle East & Africa and South America collectively represent high-potential but early-stage markets. Investments in tertiary care facilities and the gradual harmonization of pharmacopeia standards will unlock incremental opportunities, although economic volatility and reimbursement fragmentation temper near-term scale.

- Linde plc

- Air Liquide

- Air Products & Chemicals

- Messer Group

- Taiyo Nippon Sanso

- Atlas Copco

- Beckton Dickinson

- Amico Group

- Matheson Tri-Gas

- GCE Group

- NOVAIR

- Luxfer Gas Cylinders

- Getinge

- Dragerwerk AG

- INOX Air Products

- South African Oxygen (Afrox)

- Gulf Cryo

- Coregas Pty

- SOL Group

- Air Water Inc.

- Invacare

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Home Healthcare & POC Oxygen Therapy

- 4.2.2 Growing Prevalence of Respiratory Diseases

- 4.2.3 Government-Funded Oxygen Infrastructure Build-Outs Post-COVID

- 4.2.4 Miniaturization of Portable/ Wearable Concentrators & Sensors

- 4.2.5 Commercialization of Eco-Friendly Low-GWP Anaesthesia Gas Blends

- 4.2.6 AI-Enabled Predictive Gas-Pipeline Monitoring & Inventory Control

- 4.3 Market Restraints

- 4.3.1 Stringent Multi-Jurisdictional cGMP & Pharmacopeia Compliance

- 4.3.2 Limited Reimbursement for Long-Term Home Oxygen Therapy

- 4.3.3 Workplace-Safety Liability & Insurance Costs for Bulk-Gas Handling

- 4.3.4 Helium Supply Volatility Driving Up Specialty-Gas Costs

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product

- 5.1.1 Medical Gases

- 5.1.1.1 Pure Medical Gases

- 5.1.1.1.1 Oxygen

- 5.1.1.1.2 Nitrous Oxide

- 5.1.1.1.3 Medical Air

- 5.1.1.1.4 Carbon Dioxide

- 5.1.1.1.5 Helium & Specialty Gases

- 5.1.1.2 Medical Gas Mixtures

- 5.1.1.3 Biological Atmosphere

- 5.1.1.1 Pure Medical Gases

- 5.1.2 Medical Gas Equipment

- 5.1.2.1 Compressors

- 5.1.2.2 Cylinders

- 5.1.2.3 Hose Assemblies & Valves

- 5.1.2.4 Masks & Cannulas

- 5.1.2.5 Vacuum & Suction Systems

- 5.1.2.6 Manifold & Pipeline Systems

- 5.1.2.7 Alarm & Monitoring Systems

- 5.1.1 Medical Gases

- 5.2 By Modality

- 5.2.1 Bulk On-site Generation

- 5.2.2 Packaged Cylinders

- 5.2.3 Liquid/Bulk Delivery

- 5.2.4 Portable Concentrators

- 5.3 By Application

- 5.3.1 Therapeutic

- 5.3.2 Diagnostic & Imaging

- 5.3.3 Pharmaceutical Manufacturing & Research

- 5.3.4 Cryosurgery & Cryotherapy

- 5.3.5 Home Healthcare

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Home Care Settings

- 5.4.4 Academic & Research Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Linde plc

- 6.3.2 Air Liquide

- 6.3.3 Air Products & Chemicals

- 6.3.4 Messer Group

- 6.3.5 Taiyo Nippon Sanso

- 6.3.6 Atlas Copco

- 6.3.7 BeaconMedaes

- 6.3.8 Amico Group

- 6.3.9 Matheson Tri-Gas

- 6.3.10 GCE Group

- 6.3.11 NOVAIR

- 6.3.12 Luxfer Gas Cylinders

- 6.3.13 Getinge AB

- 6.3.14 Dragerwerk AG

- 6.3.15 INOX Air Products

- 6.3.16 South African Oxygen (Afrox)

- 6.3.17 Gulf Cryo

- 6.3.18 Coregas Pty

- 6.3.19 SOL Group

- 6.3.20 Air Water Inc.

- 6.3.21 Invacare Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

医用气体及设备市场:2026-2032年全球市场预测(依产品类型、设备类型、来源、应用、最终用户及通路划分)

医用气体及设备市场:2026-2032年全球市场预测(依产品类型、设备类型、来源、应用、最终用户及通路划分) 医用气体市场规模、份额、趋势和预测:按气体类型、应用、最终用户和地区划分,2026-2034年医用气体混合设备市场:按产品类型、最终用户、应用和气体类型划分-2026-2032年全球市场预测

医用气体市场规模、份额、趋势和预测:按气体类型、应用、最终用户和地区划分,2026-2034年医用气体混合设备市场:按产品类型、最终用户、应用和气体类型划分-2026-2032年全球市场预测 氧气生产设备市场规模、份额和成长分析:按产品类型、技术、产能、纯度、应用、最终用户和地区划分 - 2026-2033 年产业预测

氧气生产设备市场规模、份额和成长分析:按产品类型、技术、产能、纯度、应用、最终用户和地区划分 - 2026-2033 年产业预测 2026年全球医用气体和设备市场报告

2026年全球医用气体和设备市场报告 医用气体经销店市场分析及预测(至2035年):依类型、产品、服务、技术、组件、应用、材质、设备、最终使用者及安装类型划分日本医用气体市场规模、份额、趋势和预测:按气体类型、应用、最终用户和地区划分,2026-2034年

医用气体经销店市场分析及预测(至2035年):依类型、产品、服务、技术、组件、应用、材质、设备、最终使用者及安装类型划分日本医用气体市场规模、份额、趋势和预测:按气体类型、应用、最终用户和地区划分,2026-2034年 全球医用气体市场-2026-2031年预测

全球医用气体市场-2026-2031年预测 2026-2030年全球医用气体混合器市场

2026-2030年全球医用气体混合器市场 医用气体设备市场机会、成长要素、产业趋势分析及2026年至2035年预测

医用气体设备市场机会、成长要素、产业趋势分析及2026年至2035年预测