|

市场调查报告书

商品编码

1906032

电网级电池:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)Grid Scale Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

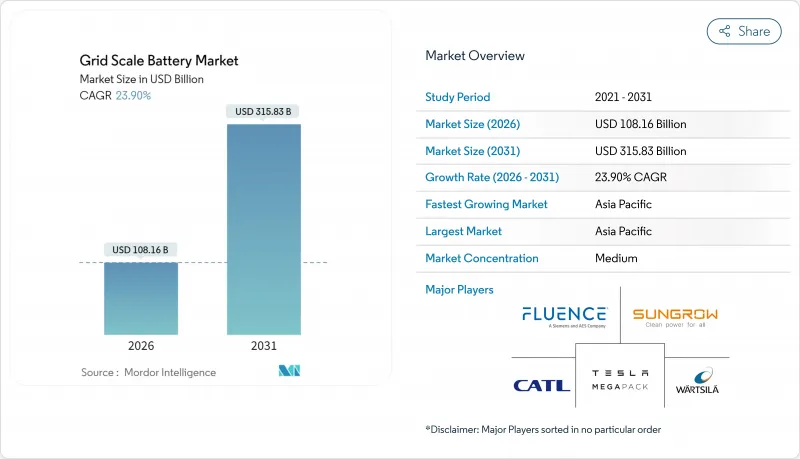

预计到 2026 年,电网级电池市场规模将达到 1,081.6 亿美元,高于 2025 年的 872.9 亿美元,预计到 2031 年将达到 3,158.3 亿美元。

预计从 2026 年到 2031 年,其复合年增长率将达到 23.9%。

锂离子电池技术成本的快速下降、可再生能源强制性标准的不断提高以及电网现代化改造的迫切需求,正在加速公用事业公司、开发商和大型能源用户的采购决策。预计到2024年,公用事业规模的装置容量将达到173吉瓦时(GWh),其中加州和德克萨斯州的增幅最大,因为这两个州都致力于在2030年前实现雄心勃勃的可再生能源目标。亚太地区的製造规模和政策支持巩固了其成本优势,而诸如2022年莫斯兰丁火灾等事故则促使业界更加关注安全创新。投资者正积极响应,以创纪录的资金流入与主流锂离子电池装置互补的长时储能技术,预示着计划经济效益和收益累积策略正在转变。

全球电网级电池市场趋势与洞察

锂离子电池成本下降

到2023年,锂离子电池组的平均价格将降至139美元/kWh时,较1991年下降97%。製造商预计到2026年,价格将跌破100美元/度。成本压力主要来自中国、美国和欧洲超级工厂的扩张、自动化製造以及供应链的最佳化。宁德时代麒麟2.0和比亚迪刀锋2.0平台支援6C快充和高能量密度,降低了4小时充电系统的辅助设备成本。这些改进使得购电协议成本更低,投资回收期更短,从而在利率波动的情况下维持了订单供应。随着单位经济效益的提升,开发商越来越倾向于采用大规模容量的系统以实现规模经济,从而加快安装和试运行实践的学习曲线。

强制性可再生能源併网

加州的目标是到2026年达到11.5吉瓦的储能容量,墨西哥则对公用事业规模的可再生强制规定5%的储能比例。欧洲的「Fit for 55」计画旨在推动区域储能容量在2024年成长超过21.9吉瓦时。政策制定者认为,储能对于实现净零排放目标、整合可变太阳能和风能发电以及推迟新增燃气调峰电厂容量至关重要。各国正在蓝图,将强制规定转变为竞争性竞标和技术中立的容量市场,使开发商能够获得降低资金筹措风险的收益合约。强制性规定也正在加速混合型太阳能+储能购电协议(PPA)的采购,这些协议能够保障计划电力购买并规避市场风险。

关键矿产供应链限制因素

预计到2030年,锂、钴和镍的需求量可能超过现有矿产产能,这将使开发商面临价格上涨和交付延迟的风险。中国占全球锂精炼量的60%和钴产量的75%,而刚果民主共和国(刚果(金))占全球钴矿产量的70%,造成了地缘政治风险的集中。钠离子电池和铁空气电池正成为新兴的替代技术:中国运作全球首座100兆瓦时钠离子电池工厂,美国公司正在试行一种永续100小时的铁空气电池系统。产业联盟正致力于推动多元化购电协议和回收政策,以降低对原料的依赖。

细分市场分析

到2025年,锂离子电池将占据电网级电池市场91.30%的份额,市场规模将达到796.8亿美元,成为最大的市场。预计到2031年,锂离子电池将以24.1%的复合年增长率成长。其成本优势(可与天然气高峰竞争)、高往返效率以及成熟的供应链是其主要优势。在锂离子电池中,磷酸锂铁在固定式应用的效能优于镍锰钴电池,循环寿命可达4000-6000次,且热失控风险较低。同时,宁德时代(CATL)的第二代钠离子电池模组有望成为寒冷气候下的理想替代方案,製造商预计将于2026年开始商业出货。

2025年,液流电池在电网级电池市场中所占份额不足3%,但在澳洲、加州和德国的长时储能竞标中,液流电池却处于主导。钒液流电池系统拥有25年的使用寿命和近乎零劣化,从而降低了计划生命週期内每兆瓦时的平准化成本。 2025年,为了因应可再生能源发电过剩,电力公司要求电池放电时间达到8小时或更长,这导致对铁空气和锌混合阴极技术的风险投资激增。日本的固态电池先导计画正在采用硫化物电解质来提高体积能量密度,但距离商业化生产仍需数年时间。因此,电池化学成分的最佳化方向正从单一主导平台转向针对特定应用的最佳化。

电网级电池市场报告按电池化学成分(锂离子电池、铅酸电池、钠基电池、液流电池和其他新兴化学成分)、应用(频率调节、能源套利/计费管理、负载转移和尖峰用电调节、可再生能源时间转移等)和地区(北美、欧洲、亚太地区、南美以及中东和非洲)进行细分。

区域分析

预计到2025年,亚太地区将占据电网级电池市场46.20%的份额,并在2026年至2031年间以25.2%的复合年增长率增长,这主要得益于中国的製造业优势和出口导向政策奖励。宁德时代(CATL)和比亚迪等中国供应商正在欧洲和北美洽谈数吉瓦级合同,同时投资兴建区域组装厂以降低贸易壁垒。日本的脱碳蓝图正在推动合作,力求2027年建成100兆瓦的储能容量;印度的生产连结奖励计画计画则为国内超级工厂提供补贴。韩国正在探索高阶固态电池,并寻求高端出口市场;澳洲则利用其丰富的可再生能源资源部署储能设施,以稳定电力供应。

北美地区总装置容量排名第二,这主要得益于《反通膨法案》的税额扣抵和各州可再生能源采购强制规定。加州的蓝图目标是到2026年实现11.5吉瓦的装置容量,而德克萨斯州已签署超过8吉瓦的併网协议,这将推动该地区电网级电池市场在2026年达到293亿美元。联邦能源监管委员会(FERC)的排队改革旨在清理540吉瓦的待审批储能计划,但平均併网时间仍超过三年,这构成了巨大的阻力。加拿大正优先考虑在偏远地区建造电池-柴油混合发电系统,以提高电网可靠性;墨西哥则透过对新建可再生能源计划强制实施5%的储能比例,创造了新的需求管道。

2024年,欧洲能源安全问题的迫切性日益凸显,届时装置容量将达到21.9吉瓦。德国联邦网路管理局已认可电池在容量储备和黑启动服务中的作用,英国容量市场也已签订15年合约以稳定现金流。南欧国家正在将公用事业规模的太阳能光电发电与储能结合,以缓解午后弃电。北欧营运商正在将水力发电与储能结合,以加强频率调节。欧盟清洁能源一揽子计画下的立法统一了电网服务定义,并促进了电池储能服务的跨境交易。监管方面的利多因素将推动该地区在2031年实现23.2%的复合年增长率。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 锂离子电池成本下降

- 强制性可再生能源併网

- 电网可靠性和韧性的必要性

- 有利的政策奖励(例如个人退休帐户、欧盟净零排放目标等)

- 太阳能+储能混合购电协议及收益积累

- 资料中心微电网需要稳定、绿能。

- 市场限制

- 关键矿产供应链限制因素

- 对电池安全和火灾风险的担忧

- 网格连接伫列中的瓶颈

- 辅助业务收益的抵销作用

- 供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 电池化学

- 锂离子电池(LFP、NMC、NCA)

- 铅酸电池

- 钠基(NAS,钠离子)

- 液流电池(钒、铁、锌溴)

- 其他新兴化学物质(金属空气电池、固态电池)

- 透过使用

- 频率调节

- 能源套利/建筑管理

- 负荷转移和尖峰用电调节

- 利用可再生能源进行时间转移

- 电力传输和分配的延误

- 黑尾鹟及其係统发育支持

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 澳洲和纽西兰

- 亚太其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 埃及

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势(併购、联盟、购电协议)

- 市场占有率分析(主要企业的市场排名和份额)

- 公司简介

- Tesla

- Fluence

- Sungrow Power Supply

- Contemporary Amperex Technology(CATL)

- Wartsila

- Panasonic

- LG Energy Solution

- Samsung SDI

- BYD

- East Penn

- GS Yuasa

- Clarios

- AES Corporation

- Powin Energy

- Hitachi Energy

- NEC ES(Koch)

- EnerSys

- ESS Tech

- Ambri

- Redflow

- EnerVenue

第七章 市场机会与未来展望

The Grid Scale Battery Market size in 2026 is estimated at USD 108.16 billion, growing from 2025 value of USD 87.29 billion with 2031 projections showing USD 315.83 billion, growing at 23.9% CAGR over 2026-2031.

Rapid cost declines in lithium-ion technology, binding renewable-portfolio standards, and urgent grid-modernization programs are accelerating procurement decisions across utilities, developers, and large energy users. Utility-scale installations climbed to 173 GWh in 2024, with California and Texas accounting for the largest additions as both states pursue aggressive 2030 renewable targets. Asia-Pacific's manufacturing scale and policy support have entrenched cost leadership, while performance incidents such as the 2022 Moss Landing fire sharpen industry focus on safety innovation. Investors are responding with record capital flows into long-duration technologies that complement the dominant lithium-ion fleet, signaling an evolution in project economics and revenue stacking strategies.

Global Grid Scale Battery Market Trends and Insights

Declining Lithium-Ion Battery Costs

Average lithium-ion pack prices fell to USD 139/kWh in 2023, a 97% slide since 1991, and manufacturers expect sub-USD 100/kWh levels by 2026. Cost pressure stems from gigafactory scaling, manufacturing automation, and optimized supply chains in China, the United States, and Europe. CATL's Qilin 2.0 and BYD's Blade 2.0 platforms add 6C fast-charging and higher energy densities, reducing balance-of-plant costs for four-hour systems. These improvements unlock lower-priced power-purchase agreements and shorten payback periods, sustaining order pipelines even amid interest-rate volatility. As unit economics improve, developers increasingly favor larger system formats to capture economies of scale, accelerating the learning curve on installation and commissioning practices.

Renewable-Energy Integration Mandates

California seeks 11.5 GW of storage by 2026, Mexico now requires 5% storage in utility-scale renewables, and Europe's Fit-for-55 package drives a regional buildout exceeding 21.9 GWh in 2024. Policymakers view storage as essential for meeting net-zero milestones, integrating variable solar and wind, and postponing gas-peaking additions. National roadmaps are translating mandates into competitive auctions and technology-neutral capacity markets, enabling developers to secure revenue contracts that de-risk financing. Mandates also accelerate procurement of hybrid solar-plus-storage PPAs that guarantee project offtake and hedge merchant risk.

Critical-Mineral Supply-Chain Constraints

Forecast demand for lithium, cobalt, and nickel could outstrip committed mining capacity by 2030, exposing developers to price spikes and delivery delays. China refines 60% of global lithium and 75% of cobalt, while the DRC holds 70% of mined cobalt output, concentrating geopolitical risk. Sodium-ion and iron-air chemistries are emerging alternatives: China commissioned the world's first 100 MWh sodium-ion plant in 2024, and US firms pilot iron-air systems for 100-hour endurance. Industry consortia lobby for diversified offtake agreements and recycling mandates to ease raw-material dependency.

Other drivers and restraints analyzed in the detailed report include:

- Grid Reliability & Resiliency Needs

- Favourable Policy Incentives (IRA, EU Net-Zero)

- Battery-Storage Safety & Fire-Risk Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The lithium-ion segment controlled 91.30% of the grid-scale battery market share in 2025 and generated the largest contribution to the grid-scale battery market size at USD 79.68 billion, expanding at a 24.1% CAGR through 2031. Cost parity with peaking gas, high round-trip efficiencies, and established supply chains sustain its position. Within lithium-ion, lithium iron phosphate eclipses nickel manganese cobalt for stationary use, offering 4,000-6,000 cycles and lower thermal-runaway risk. Meanwhile, CATL's second-generation sodium-ion modules promise viable substitution in cold climates, and manufacturers anticipate commercial shipments by 2026.

Flow batteries recorded <3% of the 2025 grid-scale battery market size but lead long-duration tenders in Australia, California, and Germany. Vanadium redox systems deliver 25-year lifespans with near-zero degradation, translating to lower levelized-cost per MWh over project life. Venture investments in iron-air and zinc hybrid-cathode technologies surged in 2025 as utilities seek 8+ hour discharge for renewable over-generation. Solid-state battery pilots in Japan use sulfide electrolytes to improve volumetric energy density, although commercial output remains several years away. The chemistry mix is therefore shifting toward application-specific optimization rather than a single winning platform.

The Grid Scale Battery Market Report is Segmented by Battery Chemistry (Lithium-Ion, Lead-Acid, Sodium-Based, Flow Batteries, and Other Emerging Chemistries), Application (Frequency Regulation, Energy Arbitrage/Bill Management, Load Shifting and Peak Shaving, Renewable-Energy Time-Shifting, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific held 46.20% of the grid-scale battery market share in 2025 and is on track for a 25.2% CAGR between 2026 and 2031, anchored by China's manufacturing dominance and export-oriented policy incentives. Chinese suppliers such as CATL and BYD negotiate multi-gigawatt contracts in Europe and North America while investing in regional assembly plants to mitigate trade barriers. Japan's decarbonization roadmap triggers partnerships to build 100 MW of storage by 2027, and India's Production Linked Incentive scheme channels subsidies toward local gigafactories. South Korea pursues high-end solid-state research and premium export niches, whereas Australia leverages abundant renewables to install storage for firmed capacity.

North America ranks second in total deployments, catalyzed by the Inflation Reduction Act's tax credits and state-level renewable procurement mandates. California's roadmap targets 11.5 GW by 2026, and Texas exceeds 8 GW in interconnection agreements, propelling the region's grid-scale battery market size to USD 29.3 billion in 2026. Queue reforms by FERC aim to clear 540 GW of pending storage-linked projects, yet interconnection timelines still average more than three years, representing a material headwind. Canada prioritizes grid reliability in remote provinces through battery-diesel hybrid systems, and Mexico enforces a 5% storage requirement for new renewable projects, creating an emerging demand pipeline.

Europe's urgency accelerated after 2024 energy-security disruptions, lifting installed capacity to 21.9 GWh that year. Germany's Bundesnetzagentur recognizes batteries in capacity reserves and black-start services, while the United Kingdom's capacity market secures 15-year contracts that stabilize cash flows. Southern European nations integrate storage with utility-scale solar to mitigate afternoon curtailment, and Nordic operators pair batteries with hydropower to enhance frequency control. Legislation under the EU Clean Energy Package harmonizes grid-service definitions, fostering cross-border trading of battery services. Regulatory tailwinds underpin a 23.2% CAGR for the region through 2031.

- Tesla

- Fluence

- Sungrow Power Supply

- Contemporary Amperex Technology (CATL)

- Wartsila

- Panasonic

- LG Energy Solution

- Samsung SDI

- BYD

- East Penn

- GS Yuasa

- Clarios

- AES Corporation

- Powin Energy

- Hitachi Energy

- NEC ES (Koch)

- EnerSys

- ESS Tech

- Ambri

- Redflow

- EnerVenue

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining lithium-ion battery costs

- 4.2.2 Renewable-energy integration mandates

- 4.2.3 Grid-reliability & resiliency needs

- 4.2.4 Favourable policy incentives (IRA, EU Net-Zero, etc.)

- 4.2.5 Hybrid solar-plus-storage PPAs & revenue stacking

- 4.2.6 Data-centre micro-grids demand firm clean power

- 4.3 Market Restraints

- 4.3.1 Critical-mineral supply-chain constraints

- 4.3.2 Battery-storage safety & fire-risk concerns

- 4.3.3 Interconnection-queue bottlenecks

- 4.3.4 Ancillary-service revenue cannibalisation

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Battery Chemistry

- 5.1.1 Lithium-ion (LFP, NMC, NCA)

- 5.1.2 Lead-acid

- 5.1.3 Sodium-based (NAS, Sodium-ion)

- 5.1.4 Flow Batteries (Vanadium, Iron, Zinc-Br)

- 5.1.5 Other Emerging Chemistries (Metal-air, Solid-state)

- 5.2 By Application

- 5.2.1 Frequency Regulation

- 5.2.2 Energy Arbitrage/Bill Management

- 5.2.3 Load Shifting and Peak Shaving

- 5.2.4 Renewable-Energy Time-Shifting

- 5.2.5 Transmission and Distribution Deferral

- 5.2.6 Black-Start and Grid-Forming Support

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Nordic Countries

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 ASEAN Countries

- 5.3.3.6 Australia and New Zealand

- 5.3.3.7 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Tesla

- 6.4.2 Fluence

- 6.4.3 Sungrow Power Supply

- 6.4.4 Contemporary Amperex Technology (CATL)

- 6.4.5 Wartsila

- 6.4.6 Panasonic

- 6.4.7 LG Energy Solution

- 6.4.8 Samsung SDI

- 6.4.9 BYD

- 6.4.10 East Penn

- 6.4.11 GS Yuasa

- 6.4.12 Clarios

- 6.4.13 AES Corporation

- 6.4.14 Powin Energy

- 6.4.15 Hitachi Energy

- 6.4.16 NEC ES (Koch)

- 6.4.17 EnerSys

- 6.4.18 ESS Tech

- 6.4.19 Ambri

- 6.4.20 Redflow

- 6.4.21 EnerVenue

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

电网级电池市场:2026-2032年全球市场预测(依化学成分、部署模式、应用、充电方式、输出容量范围、电池类型及能源容量范围划分)

电网级电池市场:2026-2032年全球市场预测(依化学成分、部署模式、应用、充电方式、输出容量范围、电池类型及能源容量范围划分) 2034年电网级电池系统市场预测-全球分析(按电池类型、系统组件、储能时间、所有权、併网方式、应用、最终用户和地区划分)

2034年电网级电池系统市场预测-全球分析(按电池类型、系统组件、储能时间、所有权、併网方式、应用、最终用户和地区划分) 电网级电池市场规模、份额、成长及全球产业分析:按类型、应用和区域划分,预测2026-2034年

电网级电池市场规模、份额、成长及全球产业分析:按类型、应用和区域划分,预测2026-2034年 2026年全球电网级电池储能市场报告全球电网级电池市场规模、份额、趋势和成长分析报告(2026-2034)

2026年全球电网级电池储能市场报告全球电网级电池市场规模、份额、趋势和成长分析报告(2026-2034) 电网级电池市场-全球产业规模、份额、趋势、机会和预测,按电池类型、所有权、应用、地区和竞争格局划分,2021-2031年预测

电网级电池市场-全球产业规模、份额、趋势、机会和预测,按电池类型、所有权、应用、地区和竞争格局划分,2021-2031年预测 电网级电池市场规模、份额和成长分析(按电池类型、所有权模式、应用和地区划分)-2026-2033年产业预测

电网级电池市场规模、份额和成长分析(按电池类型、所有权模式、应用和地区划分)-2026-2033年产业预测 全球电网规模蓄电池市场规模、份额和趋势分析报告:按类型、应用、地区和细分市场预测(2025-2030)到 2030 年电网规模电池储存市场预测:按类型、所有权模式、额定功率、应用和地区进行的全球分析到 2030 年电网规模电池市场预测:按电池类型、安装、额定功率、所有权模式、应用和地区进行的全球分析

全球电网规模蓄电池市场规模、份额和趋势分析报告:按类型、应用、地区和细分市场预测(2025-2030)到 2030 年电网规模电池储存市场预测:按类型、所有权模式、额定功率、应用和地区进行的全球分析到 2030 年电网规模电池市场预测:按电池类型、安装、额定功率、所有权模式、应用和地区进行的全球分析