|

市场调查报告书

商品编码

1906072

家用杀虫剂(农药):市场占有率分析、产业趋势与统计、成长预测(2026-2031)Household Insecticides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

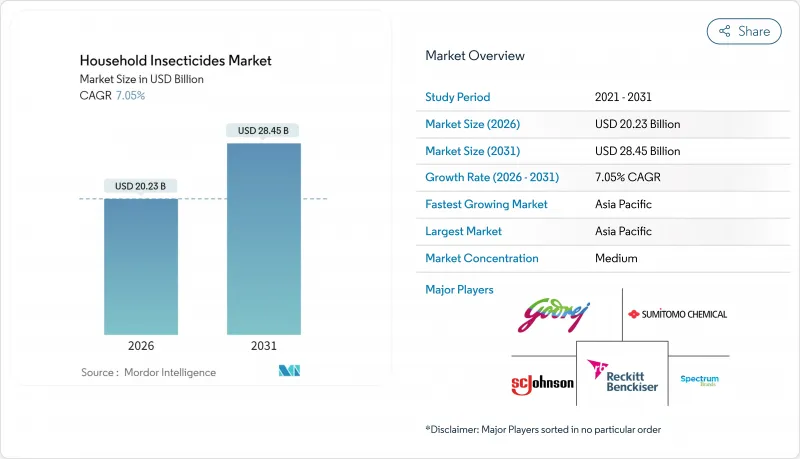

预计到 2026 年,家用杀虫剂(农药)市值将达到 202.3 亿美元,高于 2025 年的 189 亿美元,预计到 2031 年将达到 284.5 亿美元。

预计从 2026 年到 2031 年,其复合年增长率将达到 7.05%。

媒介传播疾病发生率上升、快速都市化以及监管机构对低毒活性成分的偏好,正在推动家用杀虫剂(农药)市场的扩张。登革热病例激增,预计到2024年将达到1,240万例,凸显了公共卫生问题的迫切性,也推动了对蚊蝇控制解决方案的高端需求。监管机构正在加强对合成拟除虫菊酯类杀虫剂的审查,同时加快对生物基成分的核准,促使製造商加速开发天然衍生产品。亚太地区占据家用杀虫剂(农药)市场40.0%的最大份额,主要归因于人口密集的城市地区有利于媒介生物的滋生。该地区的企业正在推出专有分子以应对当地的抗药性问题。同时,电子商务平台正在扩大其全球覆盖范围,并支援数据丰富的直接面向消费者的销售模式,这有利于那些拥有强大数位互动能力的品牌。原料供应链的波动带来了成本压力,而高端户外生活领域和智慧物联网设备则开启了新的收入来源。

全球家用杀虫剂(农药)市场趋势及洞察

虫媒疾病呈上升趋势

由于登革热、疟疾和基孔肯雅热疫情的爆发远超历史水平,疾病预防已成为家用杀虫剂(农药)市场的主要购买驱动因素。预计2023年至2024年间,全球登革热发生率将激增230%,将促使消费者转向价格分布更高、药效更持久的防护产品。气候变迁正在延长蚊子的繁殖季节,并将埃及斑蚊的分布范围扩大到温带地区,从而在欧洲和北美创造了新的销售机会。在登革热疫情威胁经济生产力的南美洲,各国政府正为弱势族群提供喷雾剂和蚊香的补贴。随着杀虫剂从日常用品转变为必需的健康防护用品,利用医疗建议和科学资讯进行讯息的品牌正在提高其在家庭中的渗透率。巴西创纪录的登革热疫情年份促使长效配方产品的研发,并强化了流行病学压力与研发重点之间的关联。

现代零售和电子商务通路的扩张

在家庭自给害虫防治领域,数位平台正在超越传统五金行。 2024年,亚马逊在德国的害虫防治产品销售额达到13亿美元,远超专业零售商的销售量。线上销售提高了产品透明度,使新参与企业能够凭藉丰富的产品资讯和评论与现有企业竞争。订阅模式锁定了补货需求,提高了客户终身价值,并平抑了家用杀虫剂(农药)市场的需求波动。从点选流和购买历史中收集的数据指南精准的促销活动,并优化了产品配方。这种通路转变加速了跨国扩张,使品牌能够绕过传统批发商直接销售。然而,复杂的标籤法规仍然要求进行本地化包装。千禧世代和Z世代消费者是线上购物的主导,他们透过行动装置购买驱虫剂的频率比年长消费者高出60%。

严格的国际和国内化学物质法规

主要供应商每年在REACH报名费用和测试方面的成本超过5000万欧元(5400万美元)。拟除虫菊酯类农药的重新评估导致部分产品上市延迟长达两年。小型公司缺乏克服这些障碍所需的财力,这可能导致产业整合和创新多样性降低。不同的国家法规迫使品牌维护多种配方,使得营运成本比统一管理体制下高出15-20%。预防原则加剧了不确定性,并增加了长期研发投资的风险。

细分市场分析

至2025年,蚊蝇防治产品将占家用杀虫剂(农药)市占率的33.62%。这主要受登革热和疟疾日益增长的担忧所驱动,促使人们更多地使用长效喷雾剂和蚊香。随着气候变迁导致地方性流行病区域扩大,预计这些病媒控制产品将继续保持主导地位。 Godrej公司推出的直接针对拟除虫菊酯类抗性蚊子的氟氯菊酯产品,显示病媒威胁如何引导研发重点。随着旅游需求的復苏加速了都市区虫害的蔓延,预计臭虫和甲虫控制将以9.41%的复合年增长率增长,成为成长最快的市场。人口密集城市的房东正在购买残留气雾剂以防止租户流失。白蚁防治在热带地区仍然具有重要意义,因为与防止财产损失相关的溢价仍然存在。虽然灭鼠工作一直保持稳定,但在高层建筑群中,由于食物废弃物收集滞后,灭鼠需求不断增加,因此引入了混合诱饵和陷阱系统。

消费者的支出模式揭示了一种优先考虑健康而非财产保护的优先顺序。即使有效成分成本相近,病媒控制产品也愿意收取10-15%的溢价。行销越来越强调疾病统计数据和紧迫性。随着旅游需求的復苏,便于携带的床蝨喷雾剂和洗衣添加剂开始进入大型量贩店。高层公寓大楼的公用设施走廊是蟑螂和蚂蚁的迁徙通道,这推动了对残留杀虫剂和智慧监测陷阱的需求,这些设备可以在虫害蔓延至整栋大楼之前提醒管理人员。

区域分析

预计到2025年,亚太地区将占全球家用杀虫剂(农药)市场的39.58%,年复合成长率达7.12%,主要得益于特大城市的扩张、疾病负担沉重以及全年温暖的气候。印度在销售方面领先全球市场,其中Godrej公司在本土活性成分的研发和利用普通零售通路建立广泛的分销网络方面主导。中国不断壮大的中产阶级正在增加对高端天然蚊香和智慧型设备的支出。同时,日本Earth公司凭藉其专利蟑螂饵剂持续维持市场主导地位,预计2024年销售额将达到1,390亿日圆(约9.3亿美元)(EARTH.JP)。东南亚预计将成为成长最快的地区,这主要得益于政府开展的登革热防控宣传活动,该活动对气雾剂的购买提供补贴。

在美国,日益严格的化学品监管导致天然系产品蚕食了合成产品的市场份额,而避蚊胺(DEET)在露营和健行领域仍然占据着稳固的地位。加拿大严格的标籤法规减缓了新产品推出,但也增强了消费者对授权品牌的信任。由于登革热疫情北移以及零售基础设施的现代化,墨西哥已成为高成长地区。该地区电子商务渗透率超过40%,直接面向消费者的订阅模式已成为都市区家庭的常态。

在欧洲市场,遵守REACH法规的负担以及温带地区害虫活动季节的缩短限制了其市场扩张。在南欧,从西班牙到希腊,夏季延长推动了人均使用量的增加。在德国,家居建材连锁店和线上平台是销量的主要主导,而英国市场在一系列关于气喘风险的报导之后,正迅速转向对宠物安全的无烟喷雾剂。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章:全球家用杀虫剂(农药)市场概况

第二章 引言

- 研究假设和市场定义

- 调查范围

第三章调查方法

第四章执行摘要

第五章 市场情势

- 市场概览

- 市场驱动因素

- 虫媒疾病呈上升趋势

- 现代零售和电子商务通路的扩张

- 快速的都市化和人口密度增加

- 监管政策转向低毒性生物基活性成分

- 智慧/物联网害虫防治设备的出现

- 户外生活趋势推动了对庭院和花园解决方案的需求。

- 市场限制

- 严格的国际和国内化学品法规

- 健康和环境毒性问题

- 关税导致原料供应链波动

- 昆虫抗药性增强,降低产品效力

- 技术展望

- 监管环境

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第六章 市场规模与成长预测

- 按昆虫类型

- 蚊子和苍蝇

- 老鼠和其他囓齿动物

- 白蚁

- 臭虫和甲虫

- 其他昆虫类型

- 依化学类型

- 合成

- DEET

- 派卡瑞丁

- 其他合成化学品

- 自然的

- 香茅油

- 香叶醇油

- 其他天然油脂

- 合成

- 按形式

- 粉末和颗粒

- 液体

- 气雾剂

- 线圈和雾化器

- 乳霜和乳液

- 其他形式

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 新加坡

- 亚太其他地区

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 北美洲

第七章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- SC Johnson & Son, Inc.

- Reckitt Benckiser Group plc

- Godrej Consumer Products Ltd.

- Spectrum Brands Holdings, Inc.

- Sumitomo Chemical Co., Ltd.

- Henkel AG & Co. KGaA(Combat)

- Bayer AG

- BASF SE

- FMC Corporation

- Central Garden & Pet Company

- Rentokil Initial plc

- Rollins, Inc.

- Ecolab Inc.

- UPL Limited

- Dabur India Limited

第八章:市场机会与未来展望

The household insecticides market size in 2026 is estimated at USD 20.23 billion, growing from 2025 value of USD 18.9 billion with 2031 projections showing USD 28.45 billion, growing at 7.05% CAGR over 2026-2031.

Intensifying vector-borne disease outbreaks, rapid urbanization, and regulatory incentives for low-toxicity actives drive this expansion within the household insecticides market. Escalating dengue fever cases, which rose to 12.4 million in 2024, underscore the public health urgency that fuels premium demand for mosquito and fly control solutions. Regulatory agencies are expediting approvals for bio-based ingredients while tightening scrutiny on synthetic pyrethroids, prompting manufacturers to accelerate natural portfolio development. Asia-Pacific holds the largest household insecticides market share at 40.0% due to dense cities that favor vector breeding, and the region's players are debuting indigenous molecules to counter local resistance patterns. Meanwhile, e-commerce platforms widen global reach and enable data-rich, direct-to-consumer models that reward brands with strong digital engagement. Supply chain volatility in raw materials adds cost pressure, but premium outdoor living segments and smart IoT-enabled devices open new revenue pathways.

Global Household Insecticides Market Trends and Insights

Rising Prevalence of Insect-Borne Diseases

Dengue, malaria, and chikungunya outbreaks are surging far beyond historical baselines, making disease prevention the primary purchase trigger in the household insecticides market. Global dengue incidence jumped 230% from 2023 to 2024, propelling consumers toward continuous protection products that command premium price points. Climate change lengthens mosquito breeding seasons and expands Aedes aegypti into temperate zones, which opens new sales pockets in Europe and North America. Governments subsidize spray and coil purchases for vulnerable communities, especially in South America, where the dengue burden threatens economic productivity. Brands leveraging medical endorsements and scientific messaging enjoy stronger household penetration, as insecticides shift from convenience goods to essential health safeguards. Brazil's record dengue year drove innovation in long-lasting formulations, reinforcing the link between epidemiological pressure and research and development focus.

Expansion of Modern Retail and E-commerce Channels

Digital platforms now outpace traditional hardware stores for do-it-yourself pest control. Amazon alone moved USD 1.3 billion of pest control products in Germany during 2024, dwarfing specialty retail volumes. Online availability elevates product transparency, letting challengers compete with incumbents through content-rich listings and review engines. Subscription models lock in replenishment, increasing customer lifetime value and smoothing demand seasonality in the household insecticides market. Data captured from clickstream and purchase histories guides targeted promotions and informs formulation tweaks. The channel shift accelerates cross-border expansion because brands bypass legacy wholesalers, although complex labeling laws still require localized packaging. Millennial and Gen Z shoppers lead the online cohort, purchasing insect repellents 60% more often via mobile than older consumers.

Stringent Global and National Chemical Regulations

REACH registration fees and testing costs now exceed EUR 50 million (USD 54 million) annually for leading suppliers. Pyrethroid re-evaluations delay launches by up to two years. Smaller firms lack the capital to clear such hurdles, leading to potential consolidation and reduced innovation diversity. Divergent national rules force brands to maintain multiple formulations, pushing operational costs 15-20% higher than under harmonized regimes. The precautionary principle fuels uncertainty, making long-horizon research and development investments riskier.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Urbanization and Population Density Growth

- Regulatory Shift Toward Low-Toxicity Bio-based Actives

- Health and Environmental Toxicity Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mosquitoes and flies controlled 33.62% of the household insecticides market share in 2025, propelled by dengue and malaria fears and boosted by continuous spray and coil adoption. The household insecticides market size attributable to these vectors will maintain leadership as climate change widens endemic zones. Godrej's renofluthrin launch directly tackles pyrethroid-resistant mosquitoes and underscores how vector pressure guides research and development focus. Bedbugs and beetles climb fastest at 9.41% CAGR because resurgent travel accelerates urban infestations; landlords in dense cities purchase residual aerosols to avert tenant turnover. Termite treatments remain regionally important in the tropics, sustaining premium pricing tied to property damage prevention. Rodent control plateaus but gains incremental volume in high-rise complexes where food waste collection lags, prompting hybrid bait and snap systems.

Consumer spending patterns reveal a hierarchy that favors health protection over property preservation. Vector control products tolerate 10-15% price premiums even when active ingredient costs are similar. Marketing increasingly highlights disease statistics to reinforce urgency. As travel rebounds, luggage-compatible bedbug sprays and laundry additives enter big box chains. Utility corridors in apartment towers serve as superhighways for cockroaches and ants, elevating demand for residual formulations and smart monitoring traps that alert maintenance staff before infestations spread building-wide.

The Household Insecticides Market Report is Segmented by Insect Type (Termites, Bedbugs and Beetles, and More), Chemical Type (Synthetic and Natural), Form (Dust and Granules, Liquids, Aerosol Sprays, Creams and Lotions, and More), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded a 39.58% share of the household insecticides market size in 2025 and is projected to rise at a 7.12% CAGR driven by megacity sprawl, high disease burden, and year-round warmth. India leads volume as Godrej pioneers indigenous actives and leverages vast distribution across general trade outlets. China's expanding middle class channels spending into premium natural coils and smart devices, while Japan's Earth Corporation sustains dominance through patented cockroach baits and recorded sales of JPY 139 billion (USD 930 million) in 2024 EARTH.JP. Southeast Asia shows the fastest incremental growth owing to government dengue campaigns that subsidize aerosol purchases.

The United States sees naturals encroaching on synthetic market share amid heightened chemical scrutiny, yet DEET remains entrenched for camping and hiking. Canada's stricter labeling laws slow new product launches but reinforce consumer trust in approved brands. Mexico emerges as a high-growth pocket as dengue spreads northward and retail infrastructure modernizes. Regional e-commerce penetration above 40% makes direct-to-consumer subscriptions the norm for urban households.

REACH compliance burdens and shorter pest seasons in temperate zones restrain Europe's market expansion. Southern Europe, from Spain to Greece, exhibits higher per-capita usage due to extended summers. Germany leads unit sales through DIY chains and online platforms, whereas the United Kingdom market pivots heavily toward pet-safe fume-free sprays following high press coverage of asthma concerns.

- SC Johnson & Son, Inc.

- Reckitt Benckiser Group plc

- Godrej Consumer Products Ltd.

- Spectrum Brands Holdings, Inc.

- Sumitomo Chemical Co., Ltd.

- Henkel AG & Co. KGaA (Combat)

- Bayer AG

- BASF SE

- FMC Corporation

- Central Garden & Pet Company

- Rentokil Initial plc

- Rollins, Inc.

- Ecolab Inc.

- UPL Limited

- Dabur India Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Table of Contents for Global Household Insecticides Market

2 Introduction

- 2.1 Study Assumptions and Market Definition

- 2.2 Scope of the Study

3 Research Methodology

4 Executive Summary

5 Market Landscape

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Rising prevalence of insect-borne diseases

- 5.2.2 Expansion of modern retail and e-commerce channels

- 5.2.3 Rapid urbanization and population density growth

- 5.2.4 Regulatory shift toward low-toxicity bio-based actives

- 5.2.5 Emergence of smart/IoT-enabled insect-control devices

- 5.2.6 Outdoor living trend boosting demand for patio/yard solutions

- 5.3 Market Restraints

- 5.3.1 Stringent global and national chemical regulations

- 5.3.2 Health and environmental toxicity concerns

- 5.3.3 Tariff-driven volatility in raw-material supply chains

- 5.3.4 Rising pest resistance reducing product efficacy

- 5.4 Technological Outlook

- 5.5 Regulatory Landscape

- 5.6 Porter's Five Forces Analysis

- 5.6.1 Bargaining Power of Suppliers

- 5.6.2 Bargaining Power of Buyers

- 5.6.3 Threat of New Entrants

- 5.6.4 Threat of Substitute Products

- 5.6.5 Intensity of Competitive Rivalry

6 Market Size and Growth Forecasts

- 6.1 By Insect Type (Value)

- 6.1.1 Mosquitoes and Flies

- 6.1.2 Rats and Other Rodents

- 6.1.3 Termites

- 6.1.4 Bedbugs and Beetles

- 6.1.5 Other Insect Types

- 6.2 By Chemical Type (Value)

- 6.2.1 Synthetic

- 6.2.1.1 DEET

- 6.2.1.2 Picaridin

- 6.2.1.3 Other Synthetic Chemicals

- 6.2.2 Natural

- 6.2.2.1 Citronella Oil

- 6.2.2.2 Geraniol Oil

- 6.2.2.3 Other Natural Oils

- 6.2.1 Synthetic

- 6.3 By Form (Value)

- 6.3.1 Dust and Granules

- 6.3.2 Liquids

- 6.3.3 Aerosol Sprays

- 6.3.4 Coils and Vaporizers

- 6.3.5 Creams and Lotions

- 6.3.6 Other Forms

- 6.4 By Geography (Value)

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.1.3 Mexico

- 6.4.1.4 Rest of North America

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.2.4 Italy

- 6.4.2.5 Spain

- 6.4.2.6 Russia

- 6.4.2.7 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Japan

- 6.4.3.4 Australia

- 6.4.3.5 Singapore

- 6.4.3.6 Rest of Asia-Pacific

- 6.4.4 Middle East

- 6.4.4.1 Saudi Arabia

- 6.4.4.2 United Arab Emirates

- 6.4.4.3 Rest of Middle East

- 6.4.5 Africa

- 6.4.5.1 South Africa

- 6.4.5.2 Egypt

- 6.4.5.3 Rest of Africa

- 6.4.1 North America

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 7.4.1 SC Johnson & Son, Inc.

- 7.4.2 Reckitt Benckiser Group plc

- 7.4.3 Godrej Consumer Products Ltd.

- 7.4.4 Spectrum Brands Holdings, Inc.

- 7.4.5 Sumitomo Chemical Co., Ltd.

- 7.4.6 Henkel AG & Co. KGaA (Combat)

- 7.4.7 Bayer AG

- 7.4.8 BASF SE

- 7.4.9 FMC Corporation

- 7.4.10 Central Garden & Pet Company

- 7.4.11 Rentokil Initial plc

- 7.4.12 Rollins, Inc.

- 7.4.13 Ecolab Inc.

- 7.4.14 UPL Limited

- 7.4.15 Dabur India Limited

8 Market Opportunities and Future Outlook

2026年全球家用杀虫剂市场报告

2026年全球家用杀虫剂市场报告 家用杀虫剂市场-全球产业规模、份额、趋势、机会、预测:按昆虫类型、化学类型、形状、地区和竞争格局划分,2021-2031年

家用杀虫剂市场-全球产业规模、份额、趋势、机会、预测:按昆虫类型、化学类型、形状、地区和竞争格局划分,2021-2031年 天然家用杀虫剂市场(按喷雾剂、产品类型、配方技术和分销管道划分),全球预测(2026-2032年)

天然家用杀虫剂市场(按喷雾剂、产品类型、配方技术和分销管道划分),全球预测(2026-2032年) 家用杀虫剂的全球市场:产品形态,组成,有效成分,用途,流通管道(线上,离线),各地区 - 市场规模,产业趋势,机会分析,预测(2025年~2033年)家用杀虫剂市场按产品类型、活性成分、销售管道、应用和最终用户划分—2025-2032 年全球预测

家用杀虫剂的全球市场:产品形态,组成,有效成分,用途,流通管道(线上,离线),各地区 - 市场规模,产业趋势,机会分析,预测(2025年~2033年)家用杀虫剂市场按产品类型、活性成分、销售管道、应用和最终用户划分—2025-2032 年全球预测 全球家用杀虫剂市场:预测至2032年-按产品类型、活性成分、目标害虫、分销管道、最终用户和地区进行分析

全球家用杀虫剂市场:预测至2032年-按产品类型、活性成分、目标害虫、分销管道、最终用户和地区进行分析 2025 年至 2033 年家用杀虫剂市场规模、份额、趋势及预测(按产品类型、成分、包装、应用、配销通路和地区)家用杀虫剂市场-全球产业规模、份额、趋势、机会及预测(按昆虫类型、化学类型、形态、地区和竞争情况细分,2020-2030 年)

2025 年至 2033 年家用杀虫剂市场规模、份额、趋势及预测(按产品类型、成分、包装、应用、配销通路和地区)家用杀虫剂市场-全球产业规模、份额、趋势、机会及预测(按昆虫类型、化学类型、形态、地区和竞争情况细分,2020-2030 年) 家用杀虫剂市场按类型、用途、包装和地区划分

家用杀虫剂市场按类型、用途、包装和地区划分 中东·非洲的家用杀虫剂市场:全球产业分析,规模,占有率,成长,趋势,预测,2024年~2031年

中东·非洲的家用杀虫剂市场:全球产业分析,规模,占有率,成长,趋势,预测,2024年~2031年