|

市场调查报告书

商品编码

1906115

梯子:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Ladder - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

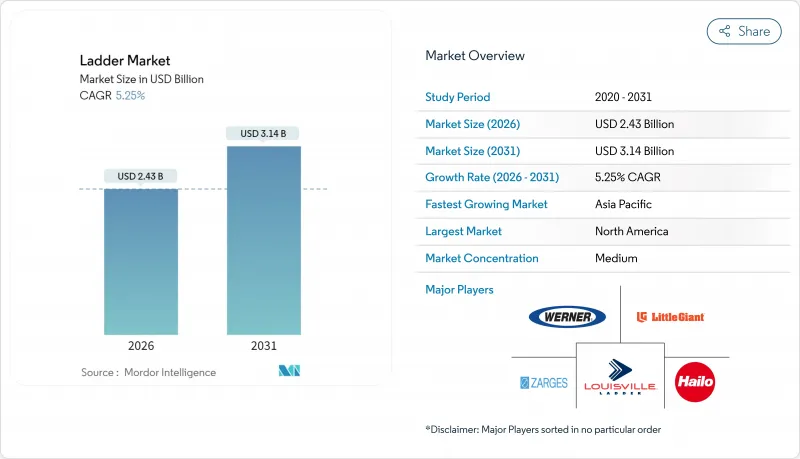

预计梯子市场规模将从 2025 年的 23.1 亿美元成长到 2026 年的 24.3 亿美元,到 2031 年将达到 31.4 亿美元,2026 年至 2031 年的复合年增长率为 5.25%。

温和成长反映出产品类型日趋成熟,并持续受益于住宅维修、美国基础设施投资与就业法案带来的基础设施支出以及专业承包商不断进行的设备更换。 ConstructConnect 预测,到 2025 年,美国建筑总支出将成长 8.5%,这将支撑商业和公共场所对新型和替换梯子的需求。儘管铝材因其强度重量比仍将占据主导地位,但随着公用事业公司采用非导电产品进行高压维护,玻璃纤维产品将推动销售成长。电子商务物流的扩张将促进仓库营运商所需的紧凑型伸缩梯的销售,而固定式通道系统的安全法规将推动用户在 OSHA 2036 年合规期限之前提前购买替换产品。竞争依然适中,区域品牌凭藉其丰富的专业产品目录和在地化的经销网络,与大规模跨国公司竞争。

全球梯子市场趋势与洞察

住宅维修与DIY文化的兴起

美国住宅越来越重视重建。预计到2024年11月,住宅中位数将达到420,400美元,促使人们选择维修房屋而非搬迁。千禧世代正值住宅高峰期,他们更倾向于自己计划维修,这得益于网路教学和大型零售商提供的专业工具。社群媒体促进了点对点的技术共用,方便了室内粉刷、更换吊扇和购买阁楼梯等。远距办公和混合办公模式的兴起推动了家庭办公室整修的需求,而折迭梯和多功能折迭梯正成为日常家用工具箱中的必备品。据经销商称,重量低于20磅的便携式梯子正在取代较重的梯子,因为消费者更注重便利性和储存效率。即使住宅建设放缓,这也为梯子创造了稳定的需求基础。

加强建筑工地安全规章

美国职业安全与健康管理局 (OSHA) 修订的「行走和工作表面规则」要求,超过 24 英尺(约 7.3 公尺)的新型固定梯必须配备防坠落系统,并呼吁在 2036 年前逐步淘汰笼式梯。承包商正在加快梯子更换计划,以避免后期进行大规模维修,这推动了带有集成电缆套管的无笼式垂直梯系统的销售。欧洲 EN 131 标准针对专业和非专业梯子,根据性能等级和测试负荷进一步细分了梯子行业,促进了高端产品的普及。像 Turner Construction 这样的大型建设公司正在实施「梯子是终点」的政策,要求使用可携式梯子必须获得书面授权,并将某些作业过渡到带有护栏的平台梯。保险公司现在将工伤赔偿保险费与梯子安全训练记录和设备劣化挂钩,迫使雇主更快更换梯子。能够使其产品通过 OSHA、ANSI 和 EN 标准的製造商,在企业发展享有竞争优势。

原物料价格波动

预计2025年第二季度,伦敦金属交易所铝现货价格将年增12%,反映出能源成本上涨正在挤压冶炼厂的利润空间。使用轧製成品捲材的梯子製造商通常受季度合约约束,因此现货价格的突然上涨会立即导致毛利率下降。用于平台扶手和延伸支撑的钢管也面临类似的波动,因为地缘政治事件改变了全球贸易流向。新兴市场的货币波动增加了依赖进口的组装购买力的不确定性。虽然製造商会将部分成本转嫁给经销商,但价格过度上涨会抑制对价格敏感的住宅通路的需求。为了规避风险,跨国公司正在推动轻质结构聚合物的应用,但根据ANSI A14通讯协定对新材料进行认证可能需要18个月,这减缓了市场接受度。

细分市场分析

到2025年,梯子市场将占最大份额,达到7.9亿美元(占全球收入的34.02%)。梯子因其四脚支撑的稳定性以及宽阔的踏板宽度,在油漆、装饰和轻型作业等领域广受欢迎。这种设计也非常适合采用玻璃纤维材质,既满足了隔热要求,又不影响便携性。儘管梯子具有这些优势,但由于紧凑型生活空间和移动办公人员的增加,人们对可折迭工具的需求不断增长,预计伸缩梯的年复合增长率将达到6.21%,因为折迭式工具便于存放于货车或壁橱中。

安全性的提升也推动了伸缩梯的成长。华纳公司于2025年4月推出的新产品,配备了一键式回缩机构,可防止夹伤,并带有可视锁定指示器,用于确认正确展开,从而解决了此前困扰该类产品的EN 131-6合规性问题。承包商非常欣赏伸缩梯的延伸范围,因为在最终现场检查期间移动大型伸缩梯会浪费时间,从而增加成本。产品发展趋势表明,虽然传统的梯凳仍将在住宅市场占有一席之地,但多功能、节省空间的型号将继续扩大市场份额。采用专利梯凳和立柱连接件以及自锁连接器的製造商能够获得更高的价格,并在专业用户群中培养品牌忠诚度。

到2025年,铝製梯子将占据42.10%的市场份额,这得益于其优异的强度重量比,使其在住宅和商业建筑中广泛应用。铝的耐腐蚀性和可回收性符合企业采购的永续性准则。同时,由于重量较重,玻璃纤维梯子预计将以6.78%的复合年增长率快速增长。这一成长主要受电力公司现场作业的推动,因为绝缘安全是电力产业的绝对要求。

在有电线路上作业的电力工人需要使用经认证可承受30kV电压的非导电梯子。玻璃纤维增强聚合物(GFRP)层压板不仅能提供这种保护,而且比涂漆铝材具有更好的抗紫外线劣化性能。现场研究表明,用10英尺长的玻璃纤维梯子代替木製桿梯,可使作业车辆的有效载荷减少14%,从而满足各州的轴重限制并降低燃油成本。同样,在屋顶上旋转5G天线的电信技术人员也指定使用玻璃纤维梯子,以避免高频电弧的风险。供应链数据显示,亚太地区玻璃纤维产品的订单约占材料成长的28%,显示绝缘梯的规格正日益趋于全球标准化。

区域分析

北美将引领市场,预计到2025年将占全球收入的31.85%,这主要得益于住宅维修需求的激增,以及在美国安全与健康管理局(OSHA)2036年监管截止日期前,人们提前用钢索式防坠落系统替换固定笼式防坠落装置。美国独栋住宅的维修支出较去年同期成长3.5%,支撑了对铝製梯子和玻璃纤维平台的需求。加拿大公共产业加快了网路加固计划,指定使用28英尺长的绝缘伸缩梯,而墨西哥加工厂的扩张则推动了工业平台的订单。预计2025年建设产业将成长8.5%,从而确保商业室内装修和民用基础设施建设所需的梯子供应稳定。

亚太地区是成长最快的地区,由于公共基础设施项目的不断扩张,预计到2031年将以5.62%的复合年增长率成长。印度计划在2029财年之前投入1.45兆美元,将增加对可携式高空作业设备的依赖,用于桥樑检测和地铁电气化专案。在中国,儘管工地机械化程度不断提高,但轻型高空作业解决方案仍然必不可少,因此对基本梯子的需求仍然强劲。高空作业平台的使用日益普及,此趋势在相关工地也同样适用。澳洲和日本的订单量持续成长,这主要得益于港口现代化和老旧电力线路的更换以扩大产能。印尼等东南亚新兴市场为中端品牌提供了机会,这些品牌可以透过本地组装来规避进口关税。

欧洲拥有成熟且稳定的市场结构。德国和法国的维修项目优先考虑节能维修,这需要频繁地进入阁楼和维修外墙,从而带动了梯子的稳定销售。 EN 131「专业级」标准要求梯子采用更粗的立柱和加固的横檔,这也推高了梯子的平均售价。北欧国家正在整合环保标准,并为铝含量超过70%可回收的梯子提供采购点。同时,中东和非洲地区在行业多元化规划的推动下正经历早期成长,但物流方面的挑战阻碍了市场渗透。拉丁美洲的产品週期性改进正在推进,巴西不断增长的农业产业带动了用于粮仓维护的玻璃纤维梯子季节性进口量的增长。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 住宅维修与DIY文化的扩展

- 加强建筑工地安全规章

- 扩大对新兴经济体的基础建设投资

- 不断扩大的电子商务仓储网络

- 在高压设备维护中引入玻璃纤维增强复合材料(GFRP)梯子

- 基于物联网的租赁车队使用情况分析

- 市场限制

- 原物料价格波动

- 与梯子相关的伤害促使人们需要替代方案

- 租赁模式蚕食了新销售额

- 以无人机/移动式升降工作平台取代巡检工作

- 产业价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 洞察市场最新趋势与创新

- 深入了解近期产业发展动态(新产品发布、策略性倡议、投资、合作、合资、扩张、併购等)

第五章 市场规模与成长预测

- 依产品类型

- 梯子

- 伸缩梯

- 平台梯

- 折迭式梯

- 伸缩梯

- 特殊/订製梯子

- 材料

- 铝

- 玻璃纤维

- 钢

- 木头

- 塑胶/复合材料

- 按最终用户行业划分

- 住宅/DIY

- 建造

- 工业製造

- 公用事业和通信

- 适用于商业和机构用途

- 运输/物流

- 透过分销管道

- 线下通路(家居建材商店、工业批发商)

- 线上(电子商务平台、直接面向消费者)

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 秘鲁

- 智利

- 阿根廷

- 南美洲其他地区

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 比荷卢经济联盟

- 北欧国家

- 其他欧洲地区

- 亚太地区

- 印度

- 中国

- 日本

- 澳洲

- 韩国

- 东南亚

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- WernerCo

- Louisville Ladder Inc.

- Little Giant Ladders(Wing Enterprises)

- Zarges GmbH

- Hailo Werk

- Altrex BV

- KRAUSE-Werk GmbH

- Youngman Group(Werner UK)

- Gorilla Ladders(Tricam)

- Tubesca-Comabi

- Telesteps AB

- Featherlite Ladders

- FACAL

- Hymer-Leichtmetallbau

- ABRU(Werner)

- Shanghai Ruiju Tools

- Zhejiang Yongkang Chuangxin

- Jinma Ladder

- Alinco Inc.

- Hermans

第七章 市场机会与未来展望

The Ladder market is expected to grow from USD 2.31 billion in 2025 to USD 2.43 billion in 2026 and is forecast to reach USD 3.14 billion by 2031 at 5.25% CAGR over 2026-2031.

Moderate growth reflects a maturing product category that continues to benefit from residential renovation, infrastructure outlays supported by the U.S. Infrastructure Investment and Jobs Act, and ongoing equipment renewal by professional trades. ConstructConnect projects 8.5% growth in total U.S. construction spending in 2025, a trend that underpins new and replacement ladder demand across commercial and institutional job sites. Aluminum remains the leading material owing to weight-to-strength advantages, while fiberglass leads unit growth as utilities adopt non-conductive products for high-voltage maintenance. E-commerce logistics expansion sustains sales of compact telescopic configurations sought by warehouse operators, and safety regulations on fixed access systems stimulate replacement purchases well before OSHA's 2036 compliance deadline. Competitive intensity stays moderate because regional brands counterbalance large multinationals through specialized catalog depth and localized distribution.

Global Ladder Market Trends and Insights

Rising Residential Renovation and DIY Culture

Homeowners in the United States prioritized remodeling as the median selling price reached USD 420,400 in November 2024, encouraging upgrades rather than relocations. Millennials entering peak ownership years prefer doing projects themselves, helped by online tutorials and wider access to pro-grade tools through big-box retailers. Social media visibility increases peer-to-peer skill sharing that boosts ladder purchases for interior painting, ceiling fan replacement, and attic access. Remote and hybrid work has heightened demand for home office conversions, pushing step ladders and multipurpose articulating designs into routine household toolkits. Distributors report that portable ladders under 20 lb are replacing heavier legacy units as consumers favor convenience and storage efficiency. The effect on the ladders market is a steady baseline of unit demand, even when new-build housing slows.

Heightened Safety Regulations in Construction

OSHA's revised Walking and Working Surfaces rule requires all new fixed ladders over 24 ft to include a fall-arrest system, phasing out cages by 2036. Contractors are accelerating replacement programs to avoid bulk retrofits later, spurring sales of cage-free vertical systems with integrated cable sleeves. European EN 131 Professional vs. Non-Professional classifications further segment the ladders industry by performance level and test loads, encouraging premium SKUs. Large builders such as Turner Construction enforce "ladders last" policies that mandate written permission for portable ladder use, shifting certain tasks to platform models with guardrails. Insurers now link workers' compensation premiums to documented ladder safety training and equipment age, nudging employers to refresh fleets sooner. Manufacturers able to certify products across OSHA, ANSI, and EN standards enjoy a competitive edge that aligns with global contractors' multi-region operations.

Volatility in Raw-Material Prices

London Metal Exchange aluminum cash prices climbed 12% year-over-year through Q2 2025, mirroring energy cost inflation that tightens smelter margins. Ladder producers consuming mill-finish coil are often locked into quarterly contracts, so spot surges translate to immediate gross-margin compression. Steel tube inputs used in platform railings and extension stiles face similar volatility as geopolitical events reshape global trade flows. Currency swings in emerging markets worsen purchasing-power unpredictability for import-reliant assemblers. Producers pass some costs to distributors, but excessive hikes dampen demand in price-sensitive residential channels. To hedge exposure, multinationals pursue lightweight structural polymers; however, certifying new materials under ANSI A14 protocols can take 18 months, slowing market uptake.

Other drivers and restraints analyzed in the detailed report include:

- Growing Infrastructure Spending in Emerging Economies

- Expansion of E-commerce Warehouse Networks

- Ladder-Related Injuries Prompting Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Step ladders generated the largest slice of the ladder market size at USD 0.79 billion in 2025, equal to 34.02% of global revenue. Their popularity in painting, decor, and light-duty trade tasks rests on inherent stability from four-leg contact and wide tread depth. The design also adapts easily to fiberglass construction, letting utilities meet dielectric requirements without sacrificing portability. Despite that dominance, telescopic ladders are on course for a 6.21% CAGR as compact living and mobile workforces seek collapsible tools that fit in vans or closets.

Safety upgrades underpin telescopic momentum. Werner's April 2025 launch introduced single-button retraction that prevents finger pinches, alongside visual lock indicators to certify proper extension. These features mitigate the EN 131-6 compliance gaps that previously tarnished the category. Contractors appreciate telescopic reach on job-site punch-lists where time penalties for moving bulky extension ladders add cost. Product evolution signals that multifunctional, space-saving formats will continue to gain share even as traditional step designs hold ground in household settings. Manufacturers leveraging patented rung-to-stile joints and automatic-locking couplers command premium pricing and foster brand loyalty across pro user communities.

Aluminum contributed 42.10% to the ladder market share in 2025, reflecting its optimal strength-to-weight ratio that supports widespread adoption across residential and commercial settings. Its corrosion resistance and recyclability align with sustainability guidelines in corporate procurement. Conversely, fiberglass, though heavier, is projected to log the fastest 6.78% CAGR, a pace attributed to electric utility field work where dielectric safety is non-negotiable.

Utility crews working on energized lines require non-conductive ladders certified to 30 kV ratings. Glass-fiber reinforced polymer (GFRP) laminates provide that protection while resisting UV degradation better than painted aluminum. Field studies show that replacing wood pole steps with 10 ft fiberglass variants cuts line-truck payload weight by 14%, letting fleets meet state axle limits and lower fuel costs. Telecommunications technicians rotating 5G antennas on rooftops similarly specify fiberglass to avoid RF arc hazards. Supply chain data indicates that fiberglass orders comprise almost 28% of material volume growth in Asia-Pacific, suggesting a global normalization of insulated ladder specifications.

The Ladder Market Report is Segmented by Product Type (Step Ladders, Extension Ladders, Platform Ladders, and More), Material (Aluminum, Fiberglass, Steel, and More, End-User Industry (Residential/DIY, Construction, Industrial Manufacturing, Utilities & Telecom, and More)), Distribution Channel (Offline, Online), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 31.85% of global revenue in 2025 after residential renovation surged and OSHA's forthcoming 2036 compliance deadline spurred early replacement of fixed cages with cable-based fall-arrest systems. U.S. single-family remodeling outlays rose 3.5% year-over-year, sustaining demand for aluminum stepladders and fiberglass podium units. Canadian utilities accelerated network-hardening programs that specify 28 ft insulated extensions, while Mexican maquiladora expansions drove industrial platform orders. Construction forecasts of 8.5% growth for 2025, cement expectations of steady ladder procurement across commercial interiors and civil infrastructure.

Asia-Pacific is the fastest-growing region, tracking a 5.62% CAGR to 2031 as public infrastructure pipelines ramp up. India's planned USD 1.45 trillion outlay through FY 2029 increases reliance on portable access equipment for bridge girder inspection and metro rail electrification. China's transition to mechanized job-site workflows keeps basic ladder demand resilient because finishing trades still require lightweight solutions for ceiling work, even where aerial lifts proliferate. Australia and Japan sustain orders by modernizing port facilities and replacing aging transmission lines with higher-capacity circuits. Southeast Asian growth markets such as Indonesia open opportunities for mid-tier brands that can localize assembly to avoid import duties.

Europe maintains a mature yet stable profile. Renovation stimulus programs in Germany and France prioritize energy-efficient retrofits that necessitate frequent attic access and facade repairs, translating to consistent ladder sales. EN 131's Professional category compels contractors to upgrade to thicker stiles and reinforced rungs, benefits that raise average selling prices. Nordic countries integrate environmental criteria, awarding procurement points for ladders with recyclable aluminum content above 70%. Meanwhile, the Middle East and Africa show early-stage growth tied to industrial diversification plans, though logistical hurdles constrain full market penetration. Latin American adoption follows commodity cycles, with Brazilian agribusiness expansions supporting seasonal spikes in fiberglass ladder imports for grain elevator maintenance.

- WernerCo

- Louisville Ladder Inc.

- Little Giant Ladders (Wing Enterprises)

- Zarges GmbH

- Hailo Werk

- Altrex B.V.

- KRAUSE-Werk GmbH

- Youngman Group (Werner UK)

- Gorilla Ladders (Tricam)

- Tubesca-Comabi

- Telesteps AB

- Featherlite Ladders

- FACAL

- Hymer-Leichtmetallbau

- ABRU (Werner)

- Shanghai Ruiju Tools

- Zhejiang Yongkang Chuangxin

- Jinma Ladder

- Alinco Inc.

- Hermans

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising residential renovation & DIY culture

- 4.2.2 Heightened safety regulations in construction

- 4.2.3 Growing infrastructure spending in emerging economies

- 4.2.4 Expansion of e-commerce warehouse networks

- 4.2.5 Adoption of GFRP ladders in high-voltage maintenance

- 4.2.6 IoT-enabled usage analytics in rental fleets

- 4.3 Market Restraints

- 4.3.1 Volatility in raw-material prices

- 4.3.2 Ladder-related injuries prompting alternatives

- 4.3.3 Rental model cannibalizing new sales

- 4.3.4 Drone/MEWP substitution for inspection tasks

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Industry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Step Ladders

- 5.1.2 Extension Ladders

- 5.1.3 Platform Ladders

- 5.1.4 Folding Ladders

- 5.1.5 Telescopic Ladders

- 5.1.6 Specialty/Custom Ladders

- 5.2 By Material

- 5.2.1 Aluminum

- 5.2.2 Fiberglass

- 5.2.3 Steel

- 5.2.4 Wood

- 5.2.5 Plastic/Composite

- 5.3 By End-User Industry

- 5.3.1 Residential / DIY

- 5.3.2 Construction

- 5.3.3 Industrial Manufacturing

- 5.3.4 Utilities & Telecom

- 5.3.5 Commercial & Institutional

- 5.3.6 Transportation & Logistics

- 5.4 By Distribution Channel

- 5.4.1 Offline (Home-Improvement Stores, Industrial Distributors)

- 5.4.2 Online (E-commerce Platforms, Direct-to-Consumer)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX

- 5.5.3.7 NORDICS

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South-East Asia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East & Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East & Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 WernerCo

- 6.4.2 Louisville Ladder Inc.

- 6.4.3 Little Giant Ladders (Wing Enterprises)

- 6.4.4 Zarges GmbH

- 6.4.5 Hailo Werk

- 6.4.6 Altrex B.V.

- 6.4.7 KRAUSE-Werk GmbH

- 6.4.8 Youngman Group (Werner UK)

- 6.4.9 Gorilla Ladders (Tricam)

- 6.4.10 Tubesca-Comabi

- 6.4.11 Telesteps AB

- 6.4.12 Featherlite Ladders

- 6.4.13 FACAL

- 6.4.14 Hymer-Leichtmetallbau

- 6.4.15 ABRU (Werner)

- 6.4.16 Shanghai Ruiju Tools

- 6.4.17 Zhejiang Yongkang Chuangxin

- 6.4.18 Jinma Ladder

- 6.4.19 Alinco Inc.

- 6.4.20 Hermans

7 Market Opportunities & Future Outlook

- 7.1 Multi-Functional and Space-Saving Ladder Solutions

- 7.2 Rising DIY Culture Boosting Household Ladder Demand

梯子市场:依产品类型、技术、最终用途产业及通路划分,2026-2032年全球预测

梯子市场:依产品类型、技术、最终用途产业及通路划分,2026-2032年全球预测 阁楼:全球市场份额和排名、总收入和需求预测(2025-2031年)阁楼梯市场按产品类型、材质、应用、机构类型、安装类型和分销管道划分-2025-2032年全球预测

阁楼:全球市场份额和排名、总收入和需求预测(2025-2031年)阁楼梯市场按产品类型、材质、应用、机构类型、安装类型和分销管道划分-2025-2032年全球预测 2025年全球梯子市场报告

2025年全球梯子市场报告 梯子市场 - 全球产业规模、份额、趋势、机会和预测(细分、按材料类型、按应用、按地区、按竞争,2020-2030 年预测)

梯子市场 - 全球产业规模、份额、趋势、机会和预测(细分、按材料类型、按应用、按地区、按竞争,2020-2030 年预测) 阁楼梯子市场:按产品类型、按应用、按分销管道、按地区

阁楼梯子市场:按产品类型、按应用、按分销管道、按地区 梯子市场:2025-2029 年全球

梯子市场:2025-2029 年全球 世界梯子市场

世界梯子市场![阶梯市场:趋势、机会与竞争分析 [2024-2030]](/sample/img/cover/42/default_cover_5.png) 阶梯市场:趋势、机会与竞争分析 [2024-2030]

阶梯市场:趋势、机会与竞争分析 [2024-2030]