|

市场调查报告书

商品编码

1906131

联氨:市占率分析、产业趋势与统计、成长预测(2026-2031)Hydrazine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

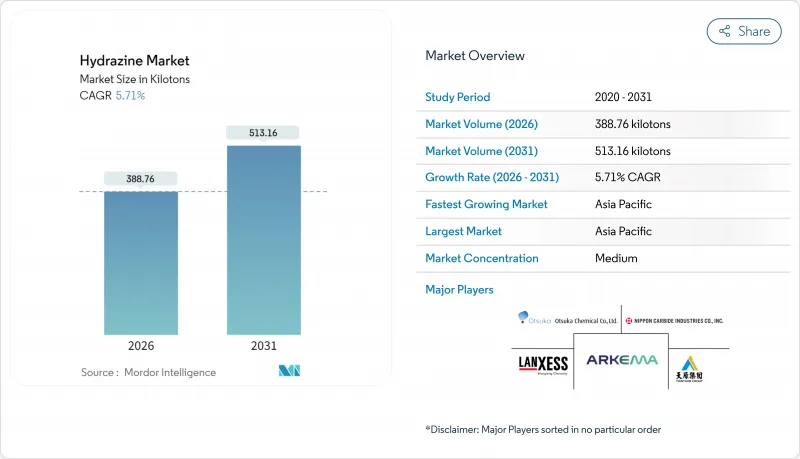

2025年联氨市值为367.75千吨,预计从2026年的388.76千吨增加到2031年的513.16千吨。

预测期(2026-2031 年)的复合年增长率预计为 5.71%。

联氨在杀虫剂、防腐蚀、聚合物泡沫和新兴能源系统中不可替代的作用,推动了其需求的韧性。欧洲和北美的监管审查持续加强,而亚太地区的产能扩张则抵消了其他地区潜在的产量下降。供应面的投资重点在于更安全的联氨水合物生产工艺,而下游的製药和燃料电池技术用户则正在开闢新的成长途径。竞争优势的关键在于垂直整合和长期合同,以确保原材料供应并控制合规成本。

全球联氨市场趋势及展望

农业化学品产业需求不断成长

中国、印度和巴西农业集约化程度的增加导致农药消费量居高不下,而联氨仍是马来酰肼、异噁唑烷酮和其他植物生长调节剂活性成分的重要中间体。中国领先的生产商拥有超过20万吨的专用产能,供应国内和出口通路,保障了製剂商的供应安全。奈米工程联氨衍生物的研究表明,其有望以更低的剂量实现全面的害虫防治,在维持药效的同时减少对环境的影响。由于食品安全监管即时于环境法规,这些地区的联氨市场依然保持稳定。

扩大其作为医药中间体的用途

联氨骨架可用于选择性合成抗结核、抗发炎和抗忧郁剂药物,近期製程创新已在温和、溶剂高效的条件下实现了89-97%的产率。吡咯Hydrazone等临床候选药物在治疗浓度下可抑制结核分枝桿菌,从而推动了美国和印度活性药物原料药(API)生产商的需求。为解决毒性问题,生产者正利用其特异性的亲核性质,同时拓展间接合成路线,从而避免处理大量联氨。因此,预计製药业仍将是联氨市场成长最快的用户领域。

高毒性及更严格的监管

联氨被列入欧洲化学品管理局的“高度关注物质清单”,并受到严格的授权要求和职业暴露限值限制。目前,合规要求包括封闭式输送管线、洗涤器系统和持续空气监测,这增加了德国、法国和美国配方商的营运成本。与肝毒性和致癌性相关的责任问题迫使保险公司提高保费,并阻碍了新进业者。虽然亚太地区的法规目前相对宽鬆,但随着跨国客户日益要求全球合规,全球范围内正在逐步实施更高的安全标准。

细分市场分析

到2025年,联氨将占联氨市场销售量的60.17%,复合年增长率(CAGR)高达5.89%,位居该细分市场之头。与无水肼相比,水合肼的蒸气较低,ISO储槽物流更便捷,且监理认证流程也较顺畅,因此备受青睐。锅炉水处理厂、聚合物发泡和原料药合成厂正在建造专用的水合物储存设施,以降低现场风险并提高需求稳定性。特种盐,例如硫酸联氨,则供应电子和分析应用等细分市场,这些领域对化学计量控制的要求更高。

监管机构目前明确建议尽可能使用水合物级产品,这促使供应商投资研发高纯度、低金属含量的配方,以满足製药业的合规要求。燃料电池开发商也倾向于使用一水合物作为液体载体原型,因为它兼具高功率密度和易挥发性控制,从而支持了需求的逐步成长。这些趋势共同巩固了联氨的市场主导地位,使其免受即将出台的无水肼监管规定的全面影响,并支撑了更广泛的联氨市场。

联氨市场报告按类型(联氨、硝酸联氨、硫酸联氨及其他)、应用(腐蚀抑制剂、炸药、火箭燃料、医药原料等)、终端用户产业(製药、农业化学品等)和地区(亚太、北美、欧洲、南美、中东和非洲)进行细分。市场预测以吨为单位。

区域分析

预计亚太地区将引领联氨市场,到2025年将占据55.51%的市场份额,并预计在2031年之前以6.05%的复合年增长率实现最快成长。中国从氨原料到下游农业化学品的完整价值链具有成本优势,而印度蓬勃发展的製药业正在推动高纯度水合肼的进口。儘管存在安全挑战,但政府对特种化学品国内生产的激励措施正在推动产能的进一步扩张。

北美市场成熟但仍在不断发展。儘管监管合规推高了营运成本,但国防应用和防腐蚀合约支撑着联氨的基本消费量。公司于2024年完成对Calca Solutions的私募股权收购,增强了投资者对其稳定的自由现金流以及下一代固体火箭发动机项目推动的未来需求增长的信心。

在REACH法规审批压力日益增大的情况下,欧洲面临最严峻的挑战。一些中型製剂生产商正在缩减产能,或将原料转移至土耳其和东欧的关联公司,以避免审批延误。整体而言,不同的管理体制造成了联氨市场两极化的局面:亚太地区加速发展,欧洲市场趋于整合,而北美则在风险管理和策略需求之间寻求平衡。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 农业化学品产业需求不断成长

- 扩大其作为医药中间体的用途

- 扩大其作为聚合物泡沫膨鬆剂的用途

- 水处理基础设施扩建

- 用于燃料电池系统的联氨氢载体

- 市场限制

- 高毒性及更严格的监管

- 氨价格波动

- 太空领域向绿色单组元推进剂(HAN/H2O2)的过渡

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按类型

- 联氨

- 硝酸联氨

- 硫酸联氨

- 其他类型

- 透过使用

- 腐蚀抑制剂

- 霹雳

- 火箭燃料

- 医药原料

- 农药前驱

- 发泡剂

- 其他用途

- 按最终用户行业划分

- 製药

- 杀虫剂

- 产业

- 其他终端用户产业

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 卡达

- 阿拉伯聯合大公国

- 奈及利亚

- 埃及

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Acuro Organics Limited

- Arkema

- BroadPharm

- Calca Solutions(AE Industrial Partners)

- Gujarat Alkalies and Chemicals Limited

- HPL Additives Limited

- Lanxess

- Loba Chemie Pvt. Ltd.

- MERU CHEM PVT.LTD.

- Nippon Carbide Industries Co., Inc.

- Otsuka Chemical Co.,Ltd.

- Yibin Tianyuan Group

第七章 市场机会与未来展望

The Hydrazine Market was valued at 367.75 kilotons in 2025 and estimated to grow from 388.76 kilotons in 2026 to reach 513.16 kilotons by 2031, at a CAGR of 5.71% during the forecast period (2026-2031).

Demand resilience stems from hydrazine's irreplaceable role in agrochemicals, corrosion control, polymer foams, and emerging energy systems. Regulatory scrutiny in Europe and North America continues to tighten, yet capacity additions in Asia-Pacific offset potential volume losses elsewhere. Supply-side investments concentrate on safer production routes for hydrazine hydrate, while downstream users in pharmaceuticals and fuel-cell technology create fresh growth avenues. Competitive positioning focuses on vertical integration and long-term contracts to secure feedstock and manage compliance costs.

Global Hydrazine Market Trends and Insights

Rising Demand from Agrochemicals

Escalating agricultural intensification in China, India, and Brazil keeps pesticide consumption high, and hydrazine remains the indispensable intermediate for maleic hydrazide, isoxazolidinone, and other growth-regulator actives. Large Chinese producers report dedicated capacities above 200,000 tons that feed both domestic and export pipelines, supporting supply security for formulating companies. Research into nano-engineered hydrazine derivatives achieves full pest mortality at lower dosage, signaling potential for reduced environmental loading while preserving efficacy. Regulatory focus on food security in these regions outweighs immediate environmental bans, thus sustaining the hydrazine market.

Growing Use as Pharmaceutical Intermediate

Hydrazine scaffolds enable the selective synthesis of anti-tubercular, anti-inflammatory, and antidepressant molecules, and recent process innovations deliver 89-97% yields under mild, solvent-efficient conditions. Clinical candidates such as pyrrole hydrazones inhibit Mycobacterium tuberculosis at therapeutic concentrations, widening demand among active pharmaceutical ingredient (API) manufacturers in the United States and India. To tackle toxicity concerns, producers are scaling indirect routes that avoid bulk hydrazine handling, yet still leverage its unique nucleophilic profile. As a result, the pharmaceutical segment is expected to remain the fastest-growing user base within the hydrazine market.

Highly Toxic Nature and Tightening Regulations

Hydrazine features on the European Chemicals Agency's Substances of Very High Concern list, triggering strict authorization and occupational exposure limits. Compliance now demands sealed transfer lines, scrubber systems, and continuous air monitoring, pushing operating costs higher for formulators across Germany, France, and the United States. Liability linked to liver toxicity and carcinogenicity also forces insurers to raise premiums, discouraging new entrants. Although Asia-Pacific regulations are comparatively lenient today, multinational customers increasingly require global compliance, slowly extending higher safety standards worldwide.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Adoption as Blowing Agent in Polymer Foams

- Expansion of Water-Treatment Infrastructure

- Shift Toward Green Monopropellants in Space

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hydrazine hydrate accounted for 60.17% of 2025 volume within the hydrazine market and recorded the segment-leading 5.89% CAGR outlook. Preference for aqueous grades stems from lower vapor pressure, simplified ISO-tank logistics, and smoother regulatory certification versus anhydrous material. Boiler-water treatment, polymer foaming, and API synthesis plants install dedicated hydrate storage to reduce on-site risk profiles, reinforcing demand stability. Specialty salts such as hydrazine sulfate serve electronics and analytical niches where tighter stoichiometric control is essential.

Regulators now explicitly recommend hydrate grades when feasible, catalyzing supplier investments in high-purity, low-metal formulations engineered for pharmaceutical compliance. Fuel-cell developers also gravitate toward monohydrate for liquid-carrier prototypes that balance power density with managed volatility, sustaining incremental offtake. Collectively, these trends entrench hydrazine hydrate's leadership and shield the segment from the full force of impending restrictions on anhydrous forms, supporting the broader hydrazine market.

The Hydrazine Report is Segmented by Type (Hydrazine Hydrate, Hydrazine Nitrate, Hydrazine Sulfate, and Other Types), Application (Corrosion Inhibitor, Explosives, Rocket Fuel, Medicinal Ingredient, and More), End-User Industry (Pharmaceuticals, Agrochemicals, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific dominated the hydrazine market with a 55.51% hydrazine market share in 2025 and is forecast to post the fastest 6.05% CAGR through 2031. China's integrated value chain, from ammonia feedstock to downstream pesticides, confers cost leadership, while India's pharmaceutical build-out boosts high-purity hydrate imports. Government incentives for local specialty-chemical production stimulate further capacity additions despite safety headwinds.

North America remains a mature yet evolving arena. Regulatory compliance elevates operating costs, but defense applications and corrosion-control contracts sustain baseline hydrazine consumption. The 2024 private-equity acquisition of Calca Solutions underscores investor belief in steady free cash flow and future volume support from next-generation solid rocket motor programs.

Europe confronts the stiffest hurdles as REACH authorization pressures escalate. Several mid-tier formulators have trimmed capacity or shifted sourcing to affiliates in Turkey and Eastern Europe to circumvent licensing delays. Collectively, divergent regulatory regimes create a two-speed hydrazine market in which Asia-Pacific accelerates while Europe consolidates and North America balances between risk management and strategic necessity.

- Acuro Organics Limited

- Arkema

- BroadPharm

- Calca Solutions (AE Industrial Partners)

- Gujarat Alkalies and Chemicals Limited

- HPL Additives Limited

- Lanxess

- Loba Chemie Pvt. Ltd.

- MERU CHEM PVT.LTD.

- Nippon Carbide Industries Co., Inc.

- Otsuka Chemical Co.,Ltd.

- Yibin Tianyuan Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand from Agrochemicals

- 4.2.2 Growing Use as Pharmaceutical Intermediate

- 4.2.3 Increasing Adoption as Blowing Agent in Polymer Foams

- 4.2.4 Expansion of Water-Treatment Infrastructure

- 4.2.5 Hydrazine-Based Hydrogen Carrier for Fuel-Cell Systems

- 4.3 Market Restraints

- 4.3.1 Highly Toxic Nature and Tightening Regulations

- 4.3.2 Volatility in Ammonia Prices

- 4.3.3 Shift Toward Green Monopropellants (HAN/H2O2) in Space

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Hydrazine Hydrate

- 5.1.2 Hydrazine Nitrate

- 5.1.3 Hydrazine Sulfate

- 5.1.4 Other Types

- 5.2 By Application

- 5.2.1 Corrosion Inhibitor

- 5.2.2 Explosives

- 5.2.3 Rocket Fuel

- 5.2.4 Medicinal Ingredient

- 5.2.5 Precursor To Pesticides

- 5.2.6 Blowing Agent

- 5.2.7 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Pharmaceuticals

- 5.3.2 Agrochemicals

- 5.3.3 Industrial

- 5.3.4 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Acuro Organics Limited

- 6.4.2 Arkema

- 6.4.3 BroadPharm

- 6.4.4 Calca Solutions (AE Industrial Partners)

- 6.4.5 Gujarat Alkalies and Chemicals Limited

- 6.4.6 HPL Additives Limited

- 6.4.7 Lanxess

- 6.4.8 Loba Chemie Pvt. Ltd.

- 6.4.9 MERU CHEM PVT.LTD.

- 6.4.10 Nippon Carbide Industries Co., Inc.

- 6.4.11 Otsuka Chemical Co.,Ltd.

- 6.4.12 Yibin Tianyuan Group

7 Market Opportunities and Future Outlook

- 7.1 Hydrazine as hydrogen-rich liquid fuel for next-gen fuel cells

- 7.2 Bio-route production via anammox bacteria