|

市场调查报告书

商品编码

1906142

聚合物涂层织物:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Polymer Coated Fabric - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

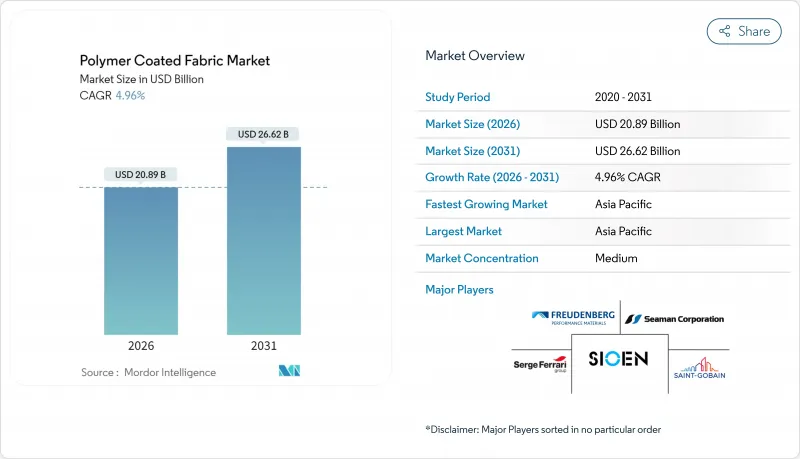

预计到 2026 年,聚合物涂层织物市场价值将达到 208.9 亿美元,高于 2025 年的 199 亿美元。

预计到 2031 年将达到 266.2 亿美元,2026 年至 2031 年的复合年增长率为 4.96%。

这一前景反映了对轻质高性能材料的持续投资,这些材料既符合更严格的化学品法规,又能实现脱碳目标。受交通运输内饰、防护衣和气候适应型建筑等领域需求趋同的推动,聚合物涂层织物市场保持稳定的成长动能。製造商正在利用兼具耐用性和可回收性的涂层技术,使终端用户能够满足生命週期成本和资讯揭露义务。虽然竞争程度适中,但策略性收购、区域产能扩张以及不含 PFAS 的创新正在使产品线之间形成明显的差异化。

全球聚合物涂层织物市场趋势及洞察

投资柔性太阳能背衬材料

太阳能资源丰富的经济体正在推广可适应曲面和轻型结构的织物光伏技术。聚四氟乙烯(PTFE)涂层玻璃纤维基板具有良好的耐候性,使柔性组件的运作可达20-25年,加速了其在建筑一体成型太阳能建筑幕墙中的应用。在中国,纺织业与光电产业的协同效应正在推动其商业化规模应用;而在欧盟,建筑师正在指定使用符合净零能耗建筑标准的轻质太阳能薄膜。

对轻质和永续内部装潢建材的需求日益增长

透过以聚合物涂层织物取代厚重的基材,汽车和航太原始设备製造商 (OEM) 可以实现 15-20% 的减重,从而直接提高燃油经济性。大陆集团已将稻壳二氧化硅和天然橡胶融入其涂层织物系列产品中,证明了可再生填料如何在不增加成本的情况下满足耐久性要求。

供应链区域化改变了国际贸易流向

地缘政治紧张局势加剧,推动生产区域化,增加了跨洲重迭涂装生产线的资本需求,并降低了规模经济效益。美国买家正将采购来源多元化,转向印度和东南亚,以降低关税风险。

细分市场分析

到2025年,聚氯乙烯(PVC)将占据聚合物涂层织物市场41.55%的份额,这反映了其强大的成本和加工优势。然而,受加工商响应邻苯二甲酸酯限制和回收强制性要求的推动,聚氨酯预计到2031年将以5.88%的复合年增长率增长。路博润的ESTANE RNW TPU在保持耐磨性的同时,碳足迹降低了59%,这表明绿色化学正在从利基市场走向主流市场。

儘管硅酮和聚乙烯在极端温度和化学惰性应用领域仍发挥其特殊作用,但生物基混合材料正在消费电子产品机壳和高端配件领域崭露头角。技术蓝图显示,领先的供应商正在将涂层创新与基材设计结合。弗罗伊登贝格的细丝纺粘技术能够实现更薄、更轻的薄膜,减少溶剂吸收,并提高涂装线的生产效率。这种整合方法表明,性能的提升既可以源自于聚合物技术的进步,也可以源自于织物结构的改进。

本聚合物涂层织物报告按产品类型(聚氯乙烯 (聚氯乙烯)、聚氨酯 (PU)、聚乙烯及其他)、应用领域(运输设备、工业设备罩、屋顶及遮阳篷、防护衣、家具、运动休閒及其他)和地区(亚太地区、北美地区、欧洲地区、南美地区、中东和非洲地区)进行分析。市场预测以美元以金额为准。

区域分析

预计到2025年,亚太地区将占聚合物涂层织物市场46.10%的份额,并在2031年之前以5.72%的复合年增长率成长。印度的纺织使命计画(2025年预算为6.29亿美元)已拨款用于技术纺织品的研发和涂层试点设施建设。从地铁到防洪屋顶等公共基础设施项目,将这些产能转化为对永续涂层织物的需求。

在北美,以技术主导的细分市场已经形成,航太和医疗设备製造商需要低挥发性有机化合物(VOC)和不含全氟烷基和多氟烷基物质(PFAS)的材料。电动车生产的回流推动了座椅布料和电池组外壳的本地在地采购增加。供应商正在美国待开发区工厂进行投资,旨在实现碳中和运营,特瑞堡位于卢瑟福县的计划(计划获得LEED认证)就是一个例证。

欧洲是一个受监管主导的市场,鼓励使用符合工业排放指令的无溶剂和水性涂料。原始设备製造商 (OEM) 重视材料资讯的全面揭露,这有利于获得认证的供应商,从而使高度合规的产品价格更具韧性。中东和非洲地区虽然规模较小,但正经历高于平均的成长,这主要得益于沿岸地区对气候适应型建筑的需求以及南非的产业多元化。有限的国内涂料生产线为愿意投资区域服务中心的成熟企业提供了外包机会。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 对轻质和永续内部装潢建材的需求日益增长

- 亚太地区製造业防护衣标准的提升

- 气候适应基础设施中建筑张拉结构的广泛应用

- 医用家具中抗菌涂层的应用

- 对柔性光伏背板材料的投资

- 市场限制

- 原油衍生聚合物价格波动

- 聚氯乙烯和邻苯二甲酸酯的环境法规

- 供应链区域化阻碍了全球贸易流动

- 价值链分析

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依产品类型

- 聚氯乙烯(PVC)

- 聚氨酯(PU)

- 聚乙烯

- 硅酮

- 其他的

- 透过使用

- 运输

- 工业设备罩

- 屋顶材料和遮阳设施

- 防护衣

- 家具

- 运动与休閒

- 其他的

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Continental AG

- Cooley Group

- Freudenberg Performance Materials Holding GmbH

- Heytex Gruppe

- OMNOVA North America Inc.

- Saint-Gobain

- Seaman Corporation

- Serge Ferrari Group

- Sioen Industries NV

- SPRADLING INTERNATIONAL GmbH

- SRF Limited

- Trelleborg AB

第七章 市场机会与未来展望

Polymer Coated Fabric Market size in 2026 is estimated at USD 20.89 billion, growing from 2025 value of USD 19.90 billion with 2031 projections showing USD 26.62 billion, growing at 4.96% CAGR over 2026-2031.

The outlook mirrors sustained investments in lightweight, high-performance materials that meet decarbonization targets while complying with more stringent chemical regulations. Demand consolidation in transportation interiors, protective clothing, and climate-resilient construction keeps the polymer coated fabric market on a steady growth track. Producers leverage coating chemistries that fuse durability with recyclability, allowing end-users to meet lifecycle cost and disclosure mandates. Competitive intensity remains moderate, yet strategic acquisitions, regional capacity expansion, and PFAS-free innovation sharpen differentiation across product lines.

Global Polymer Coated Fabric Market Trends and Insights

Investments in Flexible Photovoltaic Back-Sheet Fabrics

Solar-rich economies champion fabric-based photovoltaics that conform to curved or lightweight structures. PTFE-coated glass fiber substrates deliver weather tolerance and enable 20-25-year operating life of flexible modules, accelerating adoption in building-integrated solar facades. Chinese textile-solar synergies underpin commercial scale, while EU architects specify low-mass solar membranes to meet net-zero building codes.

Increasing Demand for Lightweight, Sustainable Interior Materials

Automotive and aerospace OEMs see 15-20% weight savings when polymer coated fabrics replace heavier substrates, translating directly to fuel efficiency gains. Continental AG integrates rice-husk silica and natural rubber into its coated fabric range, demonstrating how renewable fillers meet durability specifications without cost penalties.

Supply-Chain Localization Disrupting Global Trade Flows

Geopolitical tensions spur regionalized production, raising capital needs for duplicate coating lines across continents and compressing economies of scale. U.S. buyers diversify sourcing toward India and Southeast Asia to mitigate tariff exposure.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Protective-Clothing Standards Across APAC Manufacturing

- Adoption of Antimicrobial Coatings in Healthcare Furnishings

- Environmental Scrutiny of PVC and Phthalates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PVC held 41.55% polymer-coated fabric market share in 2025, reflecting entrenched cost and processing advantages. Polyurethane, however, is projected to post a 5.88% CAGR to 2031 as converters adapt to phthalate restrictions and recyclability mandates. Lubrizol's ESTANE RNW TPU offers a 59% lower carbon footprint while maintaining abrasion resistance, illustrating how greener chemistries transition from niche to mainstream.

Silicone and polyethylene retain specialized roles in extreme-temperature or chemically inert uses, whereas bio-based hybrids gain traction in consumer electronics casings and luxury accessories. Technological roadmaps reveal that leading suppliers pair coating innovation with substrate engineering. Freudenberg's fine-filament spunbond supports thinner, lighter membranes, lowering solvent uptake and boosting coating line throughput. This integrated approach underscores how performance gains derive from both polymer advances and fabric architecture.

The Polymer Coated Fabric Report is Segmented by Product Type (PVC (Polyvinyl Chloride), Polyurethane (PU), Polyethylene, and Others), Application (Transportation, Industrial Equipment Covers, Roofing and Awning, Protective Clothing, Furniture, Sports and Leisure, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 46.10% polymer-coated fabric market share in 2025 and is projected to register a 5.72% CAGR through 2031. India's Textile Mission, backed by USD 629 million in 2025 budget allocations, earmarks funds for technical-textile research and development and pilot coating facilities. Public infrastructure programs, from metro rail to flood-resilient roofing, convert this capacity into sustained coated fabric off-take.

North America secures a technology-driven niche where aerospace and medical OEMs demand low-VOC, PFAS-free materials. Reshoring of electric-vehicle production amplifies local sourcing for seat fabrics and battery-pack covers. The polymer-coated fabric market sees suppliers investing in U.S. greenfield plants built for carbon-neutral operation, as evidenced by Trelleborg's Rutherford County project, slated for LEED certification

Europe remains a regulation-led market incubating solvent-free, waterborne coatings aligned with the Industrial Emissions Directive. OEM preference for full material disclosure favors certified suppliers, creating price resilience for high-compliance products. Middle East and Africa, though smaller, post above-average growth on the back of climate-resilient construction in the Gulf and industrial diversification in South Africa. Limited domestic coating lines present outsourcing opportunities for incumbents willing to invest in regional service hubs.

- Continental AG

- Cooley Group

- Freudenberg Performance Materials Holding GmbH

- Heytex Gruppe

- OMNOVA North America Inc.

- Saint-Gobain

- Seaman Corporation

- Serge Ferrari Group

- Sioen Industries NV

- SPRADLING INTERNATIONAL GmbH

- SRF Limited

- Trelleborg AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Lightweight, Sustainable Interior Materials

- 4.2.2 Growth in Protective-Clothing Standards Across APAC Manufacturing

- 4.2.3 Surge in Architectural Tensile Structures for Climate-Resilient Infrastructure

- 4.2.4 Adoption of Antimicrobial Coatings in Healthcare Furnishings

- 4.2.5 Investments in Flexible PV Back-Sheet Fabrics

- 4.3 Market Restraints

- 4.3.1 Volatility of Crude-Derived Polymer Prices

- 4.3.2 Environmental Scrutiny of PVC and Phthalates

- 4.3.3 Supply-Chain Localization Disrupting Global Trade Flows

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 PVC (Polyvinyl Chloride)

- 5.1.2 PU (Polyurethane)

- 5.1.3 Polyethylene

- 5.1.4 Silicone

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Transportation

- 5.2.2 Industrial Equipment Covers

- 5.2.3 Roofing and Awning

- 5.2.4 Protective Clothing

- 5.2.5 Furniture

- 5.2.6 Sports and Leisure

- 5.2.7 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Continental AG

- 6.4.2 Cooley Group

- 6.4.3 Freudenberg Performance Materials Holding GmbH

- 6.4.4 Heytex Gruppe

- 6.4.5 OMNOVA North America Inc.

- 6.4.6 Saint-Gobain

- 6.4.7 Seaman Corporation

- 6.4.8 Serge Ferrari Group

- 6.4.9 Sioen Industries NV

- 6.4.10 SPRADLING INTERNATIONAL GmbH

- 6.4.11 SRF Limited

- 6.4.12 Trelleborg AB

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

防水布料市场:按材料、技术、应用和分销管道划分-2026-2032年全球市场预测涂层织物市场:2026-2032年全球市场预测(按产品类型、涂层材料、涂层製程、基材类型和最终用途行业划分)

防水布料市场:按材料、技术、应用和分销管道划分-2026-2032年全球市场预测涂层织物市场:2026-2032年全球市场预测(按产品类型、涂层材料、涂层製程、基材类型和最终用途行业划分) 2026年全球国防涂料市场报告

2026年全球国防涂料市场报告 抗菌涂层风管市场规模、份额和成长分析:按材料类型、应用领域、涂层技术、终端用户产业和地区划分 - 2026-2033 年产业预测

抗菌涂层风管市场规模、份额和成长分析:按材料类型、应用领域、涂层技术、终端用户产业和地区划分 - 2026-2033 年产业预测 全球涂层织物市场规模、份额、趋势和成长分析报告(2026-2034年)合成皮革市场:2026-2032年全球预测(按类型、技术、应用和销售管道划分)

全球涂层织物市场规模、份额、趋势和成长分析报告(2026-2034年)合成皮革市场:2026-2032年全球预测(按类型、技术、应用和销售管道划分) 涂层织物市场-全球产业规模、份额、趋势、机会和预测,按产品、应用、地区和竞争格局划分,2020-2030年预测

涂层织物市场-全球产业规模、份额、趋势、机会和预测,按产品、应用、地区和竞争格局划分,2020-2030年预测 衬里:全球市场份额和排名、总收入和需求预测(2025-2031年)

衬里:全球市场份额和排名、总收入和需求预测(2025-2031年) 2025年全球衬里内衬市场涂层管道市场按材料、绝缘类型、管道尺寸、形式、最终用途产业和分销管道划分-2025-2030 年全球预测

2025年全球衬里内衬市场涂层管道市场按材料、绝缘类型、管道尺寸、形式、最终用途产业和分销管道划分-2025-2030 年全球预测