|

市场调查报告书

商品编码

1906179

欧洲建筑板材市场:市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年)Europe Building And Construction Sheets - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

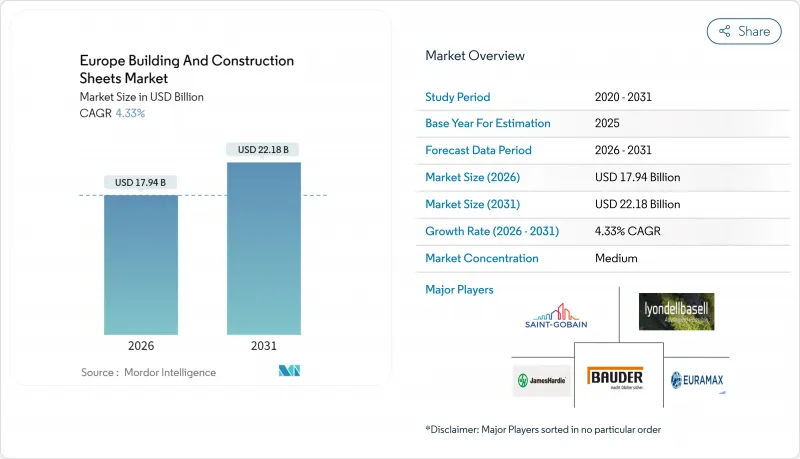

预计到 2026 年,欧洲建筑板材市场规模将达到 179.4 亿美元,从 2025 年的 172 亿美元成长到 2031 年的 221.8 亿美元,2026 年至 2031 年的复合年增长率为 4.33%。

这项展望证实了市场在动盪的宏观环境下永续性,并符合欧盟气候指令的要求——该指令规定到2030年实现零排放建筑。监管压力正推动板材市场转型为兼具结构性能、太阳能光电发电能力或增强隔热性能的板材。同时,每年1,562.3亿美元的公共资金刺激了对维修板材系统的需求,而蓬勃发展的资料中心产业和模组化建筑方法则拓展了商业机会。供应商之间的整合加速,尤其是在数位监控和低碳生产融合的领域,正在重塑欧洲建筑板材市场的竞争格局。

欧洲建筑板材市场趋势与洞察

收紧建筑围护结构的节能法规

在严格的法规和永续性目标的推动下,欧洲建筑板材市场正经历显着的变革时期。根据修订后的《建筑能源性能指令》,成员国必须在2030年前实现零排放建筑。这项要求迫使设计师优先选择兼具结构强度和高隔热性能或光伏层的板材。此外,计划于2030年前引入生命週期温室气体排放评估,也推动了对再生材料和低碳製造的需求。德国设立5,207.8亿美元的气候基金,并拨款至少1,041.5亿美元用于建筑业的脱碳,这项重大措施也刺激了市场需求。这些立法动力推高了价格溢价,并促进了市场研发活动的活性化。拥有低碳认证的供应商正努力成为公共项目的首选竞标,并抓住长期成长机会。

增加公共资金用于维修项目

受节能维修投资不断增长的推动,欧洲建筑板材市场正经历显着成长。欧盟每年津贴1,562.3亿美元用于节能维修项目,该项目旨在升级外墙、屋顶和覆层系统,而无需改变建筑主体结构。西班牙国家能源效率基金每年拨款3.8亿美元,优先扶持弱势家庭和节能性能欠佳的建筑。该计划重点推广经济高效的聚合物和混合板材,以实现切实可见的节能效果。法国重新推出了节能维修的免息贷款和税收优惠政策,即使新建项目成长放缓,也刺激了市场需求。资金筹措指南要求提供检验的性能证明,建筑商也越来越多地选择内建感测器的智慧板材,以提供即时热数据。这些因素共同支撑了该地区对专业维修产品的需求。

能源价格波动推高生产成本

由于能源价格波动和监管压力,欧洲建筑板材市场目前面临挑战。儘管天然气批发价格已从2023年的高点回落,但製造业用电价格仍高于历史平均水平,这给钢铁、铝和聚合物板材製造商的利润率带来了压力。欧盟排放交易体系的潜在延期将进一步推高碳排放成本,尤其是高炉作业的成本。为了应对这些挑战,企业正在实施现场太阳能光电解决方案和购电协议(PPA),但这需要大量的资本投资和漫长的审批流程。成本上涨也影响计划竞标,导致授标週期延长和材料替代。儘管存在这些障碍,但随着企业适应不断变化的能源和监管环境,市场预计将趋于稳定。

细分市场分析

到2025年,金属板材将占总收入的32.65%,巩固其作为欧洲建筑钢材市场结构基础的地位。市场需求依赖钢材的承载性能和铝材的耐腐蚀性,而这两种材料越来越多地采用低碳製程生产,例如使用再生能源运作的电弧炉。安赛乐米塔尔和塔塔钢铁欧洲公司正积极推广可减少高达40%排放的再生钢材。同时,建筑一体化光伏(BIPV)正在采用铝板作为薄膜电池的无框载体,从而将金属需求与绿色能源目标直接联繫起来。

到2031年,聚合物板材将以5.29%的复合年增长率成为成长最快的细分市场,因为建筑商在维修工程中更倾向于使用轻质板材,以避免结构加固。添加阻燃剂和紫外线稳定剂的配方可以延长使用寿命,而生物基树脂则提供了低碳替代方案。混合系统将柔性太阳能电池层压板和相变材料整合到多层聚合物薄膜中,从而拓展了其功能范围。沥青和橡胶仍将在防水和隔振领域发挥作用,但挥发性化合物法规的日益严格将对其市场份额构成挑战。总体而言,材料创新正在增强欧洲建筑板材市场供应商之间的差异化优势。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场趋势与动态

- 市场概览

- 市场驱动因素

- 更严格的建筑围护结构能源效率法规

- 增加公共资金用于维修项目

- 资料中心建设的增加推动了对结构铺板的需求。

- 模组化和异地建造方法的日益普及

- 将太阳光电技术整合到屋顶和墙体系统中

- 过渡到使用本地采购的低碳板材

- 市场限制

- 能源价格波动推高了生产成本。

- 限制低成本进口产品的贸易措施

- 熟练安装工人短缺

- 信贷环境收紧抑制了新建设。

- 价值/供应链分析

- 监管情势(欧盟绿色交易与能源绩效指令)

- 技术展望

- 永续性和循环经济

- 数位化和异地建造的影响

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 材料

- 沥青

- 橡皮

- 金属

- 聚合物

- 其他的

- 依建筑类型

- 新建工程

- 维修

- 最终用户

- 住宅

- 商业的

- 基础设施

- 按国家/地区

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Saint-Gobain

- LyondellBasell

- James Hardie Industries plc

- Paul Bauder GmbH

- Euramax International

- Celotex Limited

- Rauch Spanplattenwerk GmbH

- Rizolin LLC

- Icopal(BMI Group)

- CBG Composites GmbH

- Kingspan Group plc

- Tata Steel Europe

- ArcelorMittal Construction

- Sika AG

- Soprema Group

- Firestone Building Products(Holcim Elevate)

- IKO Industries

- Owens Corning

- BASF SE

- Knauf Insulation

- Coroplast Fritz Muller GmbH

第七章 市场机会与未来展望

The Europe Building & Construction Sheets Market size in 2026 is estimated at USD 17.94 billion, growing from 2025 value of USD 17.2 billion with 2031 projections showing USD 22.18 billion, growing at 4.33% CAGR over 2026-2031.

This outlook underscores the market's durability in a volatile macro environment and its alignment with European Union climate directives that mandate zero-emission buildings by 2030. Regulatory pressure is redirecting specifications toward sheets that combine structural performance with solar harvesting or enhanced thermal insulation. Simultaneously, USD 156.23 billion in annual public funding is stimulating demand for renovation-focused sheet systems, while the fast-rising data-centre sector and modular construction practices are widening commercial opportunities. Intensifying consolidation, particularly among suppliers that fuse digital monitoring with low-carbon production, is reshaping competitive dynamics across the Europe building construction sheets market.

Europe Building And Construction Sheets Market Trends and Insights

Stricter Energy-Efficiency Regulations for Building Envelopes

The European building and construction sheets market is undergoing a significant transformation driven by stringent regulations and sustainability goals. Under the revised Energy Performance of Buildings Directive, member states must achieve zero-emission building status by 2030. This mandate pushes specifiers to prioritize sheets that combine structural strength with high thermal resistance or photovoltaic layers. Additionally, life-cycle warming potential assessments, also due by 2030, are driving up the demand for recycled inputs and low-carbon manufacturing. Germany is making a significant move with its USD 520.78 billion climate fund, dedicating at least USD 104.15 billion to decarbonizing construction, which in turn amplifies volume requirements. This legislative momentum is boosting premium pricing and intensifying R&D efforts in the market. Suppliers with certified low embodied-carbon footprints are now securing preferred-bidder status on public projects, positioning themselves for long-term growth opportunities.

Expanded Public Funding for Renovation Programmes

The Europe building construction sheets market is witnessing significant growth, driven by increasing investments in energy-efficient retrofits. Annual EU grants of USD 156.23 billion are driving energy retrofits, upgrading facades, roofs, and cladding systems without major structural changes. Spain's National Energy Efficiency Fund allocates USD 380 million annually, prioritising vulnerable households and underperforming buildings. This focus leans towards cost-effective polymer and hybrid sheets, ensuring tangible kilowatt-hour savings. France has reintroduced zero-interest loans and tax breaks for energy-efficient upgrades, boosting demand even as new construction activity slows. Financing guidelines mandate verifiable performance, leading builders to opt for smart sheets with integrated sensors that provide real-time thermal data. These factors collectively sustain the demand for specialised renovation-grade products in the region.

Volatile Energy Prices Elevating Production Costs

The Europe building and construction sheets market is currently navigating challenges stemming from energy price volatility and regulatory pressures. While wholesale gas rates have retreated from their 2023 highs, electricity tariffs for manufacturers remain above historical averages, squeezing profit margins for steel, aluminium, and polymer sheet producers. The potential extension of the EU Emissions Trading System is further elevating carbon costs, particularly for blast-furnace operations. Companies are adopting on-site solar solutions and power-purchase agreements to mitigate these challenges, but these require significant capital investments and lengthy permitting processes. Cost inflation is also impacting project bids, causing delays in award cycles or material substitutions. Despite these hurdles, the market is expected to stabilize as firms adapt to evolving energy and regulatory landscapes.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Data-Centre Construction Increasing Demand for Structural Decking

- Rising Adoption of Modular and Off-Site Construction Methods

- Shortage of Skilled Installation Labour

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal sheets secured 32.65% of 2025 revenue, reinforcing their status as the structural backbone of the Europe building construction sheets market. Demand leans on steel's load-bearing capacity and aluminium's corrosion resistance, both increasingly produced through low-carbon pathways such as electric arc furnaces powered by renewable electricity. ArcelorMittal and Tata Steel Europe actively promote recycled-content grades that cut embodied emissions by up to 40%. In parallel, building-integrated photovoltaics adopt aluminium skins as frameless carriers for thin-film cells, linking metal demand directly to green-energy targets.

Polymer sheets deliver the fastest segment CAGR of 5.29% toward 2031 as contractors favour lightweight panels for retrofits that avoid structural reinforcement. Formulations incorporating fire retardants and UV stabilisers extend service life, while bio-based resins open a lower-carbon alternative. Hybrid systems embed flexible solar laminates or phase-change materials within multilayer polymer membranes, broadening functional scope. Bitumen and rubber maintain roles in waterproofing and vibration damping, yet continual regulatory tightening on volatile compounds challenges their market presence. Overall, material innovation strengthens supply-side differentiation across the Europe building construction sheets market.

The Europe Building and Construction Sheets Market Report is Segmented by Material (Bitumen, Rubber, Metal, Polymer and Others), by Construction Type (New Construction and Renovation), by End-User (Residential, Commercial and Infrastructure), and by Country (United Kingdom, Germany, France, Italy, Spain and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Saint-Gobain

- LyondellBasell

- James Hardie Industries plc

- Paul Bauder GmbH

- Euramax International

- Celotex Limited

- Rauch Spanplattenwerk GmbH

- Rizolin LLC

- Icopal (BMI Group)

- CBG Composites GmbH

- Kingspan Group plc

- Tata Steel Europe

- ArcelorMittal Construction

- Sika AG

- Soprema Group

- Firestone Building Products (Holcim Elevate)

- IKO Industries

- Owens Corning

- BASF SE

- Knauf Insulation

- Coroplast Fritz Muller GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter energy-efficiency regulations for building envelopes

- 4.2.2 Expanded public funding for renovation programmes

- 4.2.3 Growth in data-centre construction increasing demand for structural decking

- 4.2.4 Rising adoption of modular and off-site construction methods

- 4.2.5 Integration of solar technologies into roofing and cladding systems

- 4.2.6 Shift toward locally sourced, low-carbon sheet materials

- 4.3 Market Restraints

- 4.3.1 Volatile energy prices elevating production costs

- 4.3.2 Trade measures limiting access to low-cost imports

- 4.3.3 Shortage of skilled installation labour

- 4.3.4 Tighter credit conditions damping new-build pipelines

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape (EU Green Deal & EPBD)

- 4.6 Technological Outlook

- 4.7 Sustainability & Circularity Initiatives

- 4.8 Digitalisation & Off-site Construction Impact

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material

- 5.1.1 Bitumen

- 5.1.2 Rubber

- 5.1.3 Metal

- 5.1.4 Polymer

- 5.1.5 Others

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Renovation

- 5.3 By End-user

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Infrastructure

- 5.4 By Country

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Saint-Gobain

- 6.4.2 LyondellBasell

- 6.4.3 James Hardie Industries plc

- 6.4.4 Paul Bauder GmbH

- 6.4.5 Euramax International

- 6.4.6 Celotex Limited

- 6.4.7 Rauch Spanplattenwerk GmbH

- 6.4.8 Rizolin LLC

- 6.4.9 Icopal (BMI Group)

- 6.4.10 CBG Composites GmbH

- 6.4.11 Kingspan Group plc

- 6.4.12 Tata Steel Europe

- 6.4.13 ArcelorMittal Construction

- 6.4.14 Sika AG

- 6.4.15 Soprema Group

- 6.4.16 Firestone Building Products (Holcim Elevate)

- 6.4.17 IKO Industries

- 6.4.18 Owens Corning

- 6.4.19 BASF SE

- 6.4.20 Knauf Insulation

- 6.4.21 Coroplast Fritz Muller GmbH

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment