|

市场调查报告书

商品编码

1906191

聚酯轮胎帘布帘布:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Polyester Tire Cord Fabrics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

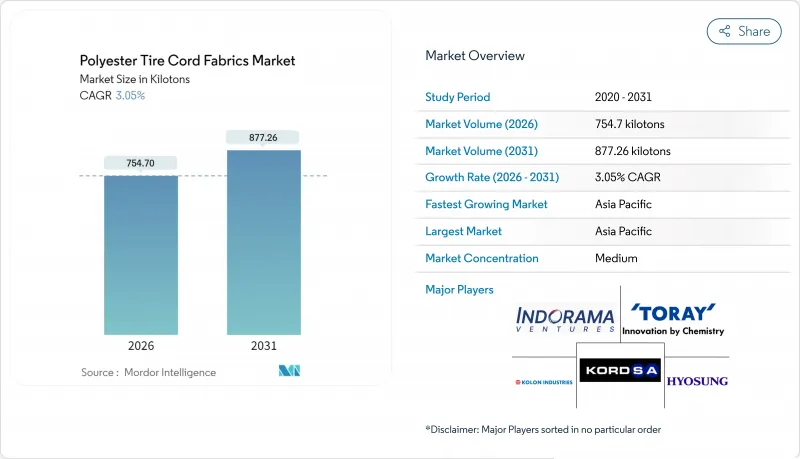

预计到 2026 年,聚酯轮胎帘布帘子布市场规模将达到 754.7 千吨,从 2025 年的 732.37 千吨增长到 2031 年的 877.26 千吨,2026 年至 2031 年的复合年增长率为 3.05%。

亚太地区子午线轮胎的日益普及、高模量低收缩率(HMLS)纱线的加速应用以及电动车(EV)产量的扩张,共同支撑了这一稳步增长。晓星和科隆等公司接近满载运作、PTA/MEG价格的长期波动以及欧盟和美国日益严格的甲醛法规,都在推动成本结构和竞争策略的重组。供应正转向具备再生PET加工能力的一体化生产商,而中小加工商则专注于研发无甲醛黏合剂技术以获得监管部门的批准。区域需求热点包括印度卡车子午线轮胎加工量的激增以及越南以出口为导向的乘用车轮胎丛集,儘管其他地区斜交轮胎的使用量有所下降,但这两个地区仍然推动了对高分子量聚酯(HMLS)的需求。

全球聚酯轮胎帘布帘子布市场趋势及展望

亚太地区子午线轮胎的快速普及

2024年,子午线轮胎在亚太地区的乘用车中广泛应用,与前一年相比显着成长。这项变更主要源自于中国和印度汽车製造商为应对燃油经济性法规而采取的措施,这些法规在滚动阻力测试中对斜交轮胎的设计提出了不利评价。子午线轮胎需要比斜交轮胎更多的聚酯帘布层以承受更高的充气压力,这推动了对高模量、低收缩率(HMLS)聚酯的需求,即便斜交轮胎的需求有所下降。在中东,新建轮胎工厂的计划全部专注于子午线轮胎生产线,这将推动聚酯消费量的长期成长。虽然东南亚国协商用车车队采用子午线轮胎的速度较为缓慢,但柴油价格的飙升有力地支撑了子午线轮胎的整体拥有成本优势。预计此一趋势将持续惠及发展中地区后采用者所采用的聚酯轮胎帘布层市场。

OEM厂商正迅速转向使用HMLS纱线并淘汰PCI。

轮胎製造商正从标准强度聚酯纤维转向高密度低强度(HMLS)聚酯纤维。这些新型纤维可透过减少汽车胎体帘布层数来减轻重量。 HMLS纱线的低热收缩率使其适用于无需后压插入(PCI)的生产线,从而降低工厂能耗并缩短生产週期。Bridgestone和米其林已试行了无PCI生产线,但全面推广应用将取决于改良型RFL化学製程的规模化应用,以控制废品率。高强度纱线和消除PCI的双重优势可降低轮胎单位成本并提升永续性指标,进一步增强了原始设备製造商(OEM)对HMLS聚酯纤维的偏好。

PTA/MEG原物料价格波动

布兰特原油价格对对苯二甲酸单乙酯(PTA)和乙二醇单乙酯(MEG)的价格影响显着,这两种原料合计约占聚酯成本的70%,导致加工商的利润率每月波动。 2024年亚洲PTA现货价格的大幅波动扰乱了非一体化加工商的预算。虽然像晓星这样的一体化企业能够利用自有单体来缓解这种波动,但规模较小的加工商却被迫每季与原始设备製造商(OEM)重新谈判,导致扩张计划停滞,研发支出削减。

细分市场分析

到2025年,子午线轮胎的需求量将占57.31%,预计到2031年将成长4.05%。这一成长速度超过了斜交轮胎的产量成长,从而推动了该细分市场聚酯轮胎帘布层市场规模的扩大。子午线轮胎在巡航速度下运转温度比斜交轮胎低15-20°C,使电动车平台能够在不增加汽车胎体重量的情况下有效应对电池产生的热量。斜交轮胎在农业和非公路应用领域仍然占据主导地位,但其较低的初始价格并不能弥补其在公路行驶中更高的燃油经济性。中国乘用车子午线轮胎的普及率已超过临界值,预计2024年,商用车也将达到相当高的普及率。这两种趋势都导致每条轮胎的帘布层用量增加,而这主要是由于更高的充气压力所致。这项变化是聚酯轮胎帘布层市场成长最主要的驱动因素。

儘管成熟经济体的斜交轮胎产量正在下降,但在撒哈拉以南非洲地区,由于可修復性比总成本更为重要,斜交轮胎的产量却在上升。然而,由于中东地区的新工厂倾向于只生产子午线轮胎,全球斜交轮胎市场份额持续下降。韩泰轮胎的iON轮胎将化学回收的HMLS纱线与钢丝带束层结合,实现了永续性和强度之间的平衡。它展示了混合结构如何降低长途运输应用中子午线轮胎的溢价。这项创新将促进子午线轮胎的成长,同时防止聚酯纤维在主流速度等级轮胎中被芳香聚酰胺取代。

聚酯轮胎帘布帘子布市场报告按轮胎类型(子午线轮胎和斜交轮胎)、应用领域(乘用车、商用车及其他应用)和地区(亚太地区、北美地区、欧洲地区、南美地区以及中东和非洲地区)进行细分。市场预测以吨为单位。

区域分析

到2025年,亚太地区将占全球市场份额的49.07%,并在2031年之前以每年3.95%的速度成长。这一成长主要得益于中国乘用车轮胎工厂的高产运转率以及印度作为主要汽车市场的崛起。科隆公司近期在越南的投资旨在提升工厂产能,以满足锦湖轮胎、赛龙轮胎和Bridgestone等产业巨头的需求。越南的乘用车轮胎出口量和聚酯帘布层年消费量印证了该国在聚酯轮胎帘布层市场的重要地位。

北美和欧洲在全球整体产量中占据相当大的份额,但成长速度正在放缓。这种停滞归因于轮胎行驶里程趋于稳定以及胎面寿命延长。为响应欧盟的甲醛限制规定,市场已显着转向使用无甲醛黏合剂,其中Cocoon公司主导地位。为响应供应链区域化的趋势,锦湖化工正在考虑在欧洲待开发区工厂,以符合美墨加协定(USMCA)的原产地规则。同时,大陆集团的永续聚酯倡议鼓励当地加工商对再生材料含量进行认证,这使得市场格局更加复杂,并提高了聚酯轮胎帘布帘子布市场的准入门槛。

南美洲和中东/非洲地区合计占据了相当大的市场份额,并持续稳定成长。倍耐力已在沙乌地阿拉伯开设了一家工厂,其位于摩洛哥的世纪工厂预计将有助于提高轮胎产量。此次产量激增预计将满足高模量、低直径(HMLS)帘线的需求。 2024年,土耳其的Cordoza公司推出了一条聚酯纱线生产线,旨在为当地原始设备製造商(OEM)提供策略性供应。虽然巴西的轮胎产量正在復苏,但国内帘线产能不足,只好依赖从台湾台塑集团进口。这些区域动态凸显了局部供不应求可能扩大聚酯轮胎帘布帘线市场,即使在轮胎产量不高的地区也是如此。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 子午线轮胎的普及率正在飙升,尤其是在亚太地区。

- 原始设备製造商正在迅速转向高强度HMLS PET纱线

- 电动车(EV)产量加速成长,推动了对低滚动阻力汽车胎体的需求。

- 消除固化后膨胀(PCI)带来的潜在节能效果

- OEM对再生/生物基PET绳材的永续性要求

- 市场限制

- PTA/MEG原物料价格波动

- 欧盟和美国黏合剂的甲醛含量(RFL)实施更严格的监管

- 在超高速应用中,芳香聚酰胺线的性能差异

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按轮胎类型

- 子午线轮胎

- 斜交轮胎

- 透过使用

- 搭乘用车

- 商用车辆

- 其他应用

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 土耳其

- 俄罗斯

- 北欧国家

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Bekaert

- Century Enka Limited

- CORDENKA GmbH & Co. KG

- Far Eastern New Century Corporation

- Firestone Fibers & Textiles

- FORMOSA TAFFETA CO., LTD.

- HYOSUNG

- Indorama Ventures Public Company Limited

- Jiangsu Taiji Industry New Materials Co., Ltd.

- Junma Group

- Kolon Industries Inc.

- KORDARNA Plus as

- Kordsa Teknik Tekstil AS

- Madura Industrial Textiles Ltd.

- Shandong Helon Polytex Chemical Fibre

- SRF Limited

- TEIJIN FRONTIER(USA),INC.

- TORAY INDUSTRIES,INC.

- Zhejiang Hailide New Material Co., Ltd.

第七章 市场机会与未来展望

Polyester Tire Cord Fabrics Market size in 2026 is estimated at 754.7 kilotons, growing from 2025 value of 732.37 kilotons with 2031 projections showing 877.26 kilotons, growing at 3.05% CAGR over 2026-2031.

Rising radial-tire penetration across Asia-Pacific, the accelerating shift to high-modulus low-shrinkage (HMLS) yarns, and expanding electric-vehicle (EV) output underpin this steady headline growth. Hyosung's and Kolon's near-full plant utilization, along with chronic PTA/MEG price swings, and the tightening of EU and U.S. formaldehyde rules are reshaping cost structures and competitive strategies. Supply is tilting toward integrated producers with recycled-PET capability, while smaller converters focus on formaldehyde-free bonding to secure regulatory clearance. Regional demand hot spots include India's surging truck radial conversion and Vietnam's export-oriented passenger-tire cluster, each lifting HMLS polyester volumes despite bias-tire contraction elsewhere.

Global Polyester Tire Cord Fabrics Market Trends and Insights

Surging Radial-Tire Penetration in Asia-Pacific

In 2024, passenger cars in the Asia-Pacific region widely adopted radial tires, marking a significant increase from previous years. This shift was largely driven by Chinese and Indian OEMs adapting to fuel-economy regulations that penalized bias designs in rolling-resistance tests. Radial tires, requiring more polyester cord than their bias counterparts to manage heightened inflation pressures, have consequently boosted demand for High Modulus Low Shrinkage (HMLS) polyester, even as bias tire volumes decline. In the Middle East, greenfield tire projects have committed exclusively to radial lines, ensuring a long-term increase in polyester consumption. While commercial vehicle fleets in ASEAN nations have been slow to adopt, surging diesel prices are making a compelling case for the total cost of ownership in favor of radial tires. This trend positions the polyester tire cord fabrics market to steadily benefit from late adopters in developing regions.

Rapid OEM Shift to HMLS Yarns and PCI Elimination

Tire manufacturers are shifting from standard-tenacity polyester to HMLS grades. These new grades allow for carcass-ply cuts that reduce weight. The lower thermal shrinkage of HMLS yarns also supports production lines that skip post-cure inflation (PCI), cutting plant energy use and shortening cycle times. Bridgestone and Michelin have piloted PCI-free lines, but widespread rollout hinges on scaling modified RFL chemistries that control scrap rates. Combined, higher-tenacity yarns and PCI elimination improve cost per tire and sustainability metrics, reinforcing OEM preference for HMLS polyester.

Volatile PTA/MEG Feedstock Prices

Brent crude prices heavily influence PTA and MEG, which together account for nearly 70% of polyester costs, causing converter margins to fluctuate within months. In 2024, Asian PTA spot prices experienced significant changes, disrupting budgets for non-integrated converters. While integrated players like Hyosung mitigate this volatility using captive monomers, smaller firms find themselves renegotiating quarterly with OEMs, leading to stalled expansion plans and reduced research and development spending.

Other drivers and restraints analyzed in the detailed report include:

- Accelerating EV Production Demanding Low-Rolling-Resistance Carcasses

- OEM Sustainability Mandates for Recycled/Bio-Based PET Cords

- Formaldehyde Restrictions and Performance Limits in Premium Tires

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Radial designs represented 57.31% of 2025 demand and are expected to grow at 4.05% to 2031, outpacing the growth of bias output, thereby increasing the size of the polyester tire cord fabrics market for this segment. Radials run 15-20 °C cooler at cruising speed, enabling EV platforms to manage battery-induced heat loads without adding extra weight to the carcass. Bias tires continue to dominate in agricultural and off-road niches, yet their lower upfront price fails to offset the higher fuel consumption on the road. In China, passenger cars have seen radial adoption surpassing a significant level. Meanwhile, by 2024, commercial vehicles reached a notable penetration rate. Each of these transitions has led to an increase in cord usage per tire, attributed to heightened inflation pressure. This shift stands as the most significant volume driver for the growth of the polyester tire cord fabrics market.

Bias volumes are contracting in mature economies but growing in sub-Saharan Africa, where repairability is prioritized over total cost. Even so, the global bias share continues to shrink as Middle East greenfield plants specify radial-only lines. Hankook's iON tire combines chemically recycled HMLS yarn with steel belts to strike a balance between sustainability and strength, demonstrating how hybrid constructions can reduce the radial premium in long-haul applications. Such innovations sustain radial growth while preventing the displacement of polyester by aramid in mainstream speed ratings.

The Polyester Tire Cord Fabrics Market Report is Segmented by Tire Type (Radial Tire and Bias Tire), Application (Passenger Cars, Commercial Vehicles, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific contributed 49.07% of global volume in 2025 and is expanding at 3.95% to 2031. This growth is largely driven by China's passenger-tire plants operating at high capacity and India emerging as a major car market. Kolon's recent investment in Vietnam aims to boost the plant's capacity, aligning with the demands of industry giants like Kumho, Sailun, and Bridgestone. Vietnam's passenger tire exports and its annual consumption of polyester cord underscore the market's significance for polyester tire cord fabrics.

North America and Europe together represent a notable share of the global volume but are experiencing slower growth. This stagnation is attributed to plateauing vehicle miles and extended tread life. In response to the EU's formaldehyde caps, there's a noticeable shift towards formaldehyde-free adhesives, with Cokoon leading the charge. Reflecting a trend of supply-chain regionalization, Kumho is eyeing a greenfield site in Europe to align with USMCA's rules of origin. Meanwhile, Continental's ambition for sustainable polyester is pushing local converters to authenticate their recycled content, complicating the landscape but simultaneously raising entry barriers in the polyester tire cord fabrics market.

South America, the Middle East, and Africa collectively hold a significant market share, with steady growth. Pirelli has established a facility in Saudi Arabia, while Morocco's Sentury factory is set to contribute additional tire production. This surge in production is expected to meet the demand for HMLS cord. In 2024, Turkey's Kordsa unveiled a polyester yarn line, strategically catering to nearby OEMs. Although Brazil's tire production is on the mend, the country struggles with insufficient domestic cord capacity, resulting in a reliance on imports from Taiwan's Formosa Taffeta. Such inter-regional dynamics highlight how localized shortages can amplify the polyester tire cord fabrics market, even in regions with modest tire production.

- Bekaert

- Century Enka Limited

- CORDENKA GmbH & Co. KG

- Far Eastern New Century Corporation

- Firestone Fibers & Textiles

- FORMOSA TAFFETA CO., LTD.

- HYOSUNG

- Indorama Ventures Public Company Limited

- Jiangsu Taiji Industry New Materials Co., Ltd.

- Junma Group

- Kolon Industries Inc.

- KORDARNA Plus a.s.

- Kordsa Teknik Tekstil A.S.

- Madura Industrial Textiles Ltd.

- Shandong Helon Polytex Chemical Fibre

- SRF Limited

- TEIJIN FRONTIER(U.S.A.),INC.

- TORAY INDUSTRIES,INC.

- Zhejiang Hailide New Material Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging radial-tire penetration, especially in Asia-Pacific

- 4.2.2 Rapid OEM shift to high-tenacity HMLS PET yarns

- 4.2.3 Accelerating EV production demanding low-rolling-resistance carcasses

- 4.2.4 Energy-saving potential from eliminating post-cure inflation (PCI)

- 4.2.5 OEM sustainability mandates for recycled / bio-based PET cords

- 4.3 Market Restraints

- 4.3.1 Volatile PTA/MEG feed-stock prices

- 4.3.2 Adhesive (RFL) formaldehyde restrictions tightening in EU and U.S.

- 4.3.3 Performance gap vs. aramid cords for ultra-high-speed applications

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Tire Type

- 5.1.1 Radial Tire

- 5.1.2 Bias Tire

- 5.2 By Application

- 5.2.1 Passenger Cars

- 5.2.2 Commercial Vehicles

- 5.2.3 Other Application

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Turkey

- 5.3.3.7 Russia

- 5.3.3.8 NORDIC Countries

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Bekaert

- 6.4.2 Century Enka Limited

- 6.4.3 CORDENKA GmbH & Co. KG

- 6.4.4 Far Eastern New Century Corporation

- 6.4.5 Firestone Fibers & Textiles

- 6.4.6 FORMOSA TAFFETA CO., LTD.

- 6.4.7 HYOSUNG

- 6.4.8 Indorama Ventures Public Company Limited

- 6.4.9 Jiangsu Taiji Industry New Materials Co., Ltd.

- 6.4.10 Junma Group

- 6.4.11 Kolon Industries Inc.

- 6.4.12 KORDARNA Plus a.s.

- 6.4.13 Kordsa Teknik Tekstil A.S.

- 6.4.14 Madura Industrial Textiles Ltd.

- 6.4.15 Shandong Helon Polytex Chemical Fibre

- 6.4.16 SRF Limited

- 6.4.17 TEIJIN FRONTIER(U.S.A.),INC.

- 6.4.18 TORAY INDUSTRIES,INC.

- 6.4.19 Zhejiang Hailide New Material Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment