|

市场调查报告书

商品编码

1906196

透水混凝土:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Pervious Concrete - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

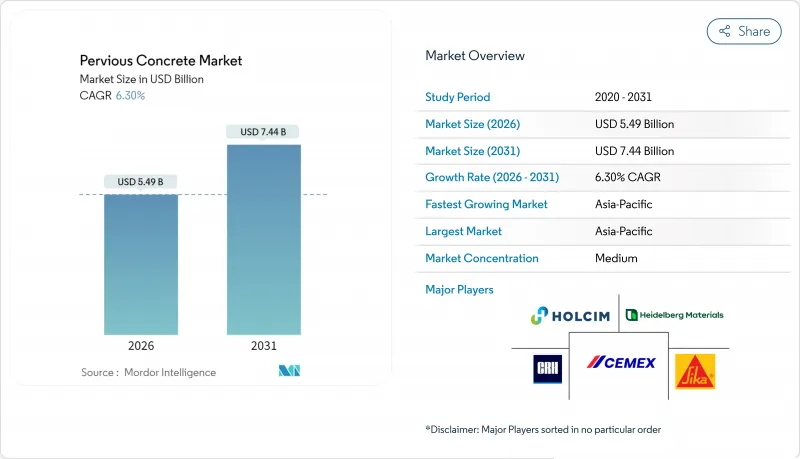

预计到 2026 年,透水混凝土市场规模将达到 54.9 亿美元,高于 2025 年的 51.6 亿美元。预计到 2031 年,透水混凝土市场规模将达到 74.4 亿美元,2026 年至 2031 年的复合年增长率为 6.3%。

都市区突发性内涝日益增多、强制性低影响开发(LID)标准以及企业对永续建筑的承诺,共同支撑着住宅、商业和公共基础设施计划中对透水混凝土的稳定需求。地方政府的税收优惠和「海绵城市」计画进一步加速了透水混凝土的普及,而混凝土配合比设计和聚合物改质技术的进步则拓展了其在结构应用领域的应用范围。由于跨国水泥生产商将透水解决方案纳入其低碳产品组合,以及区域建筑商投资专用浇筑设备,市场竞争仍温和。儘管技术纯熟劳工短缺和大都会圈骨材不足等供应方面的挑战仍然限制市场成长前景,但尚未阻碍透水混凝土市场的整体上升趋势。

全球透水混凝土市场趋势与洞察

都市区暴雨造成的损失加剧

市政当局正越来越多地采用透水混凝土进行雨水径流源头管理,以减少高峰流量,减轻老旧下水道网路的压力。透水混凝土的渗透能力高达每平方英尺每分钟8加仑(约30公升),其在暴雨期间减少径流的能力已在中国各大都市超过1万个「海绵城市」计划中得到验证。气候变迁导致降雨强度增加,使路面从被动式表面转变为主动式排水设施,从而提升了路面的提案。地方政府重视透水混凝土的双重功能,使其能够将路面和雨水基础设施整合到单一的资本支出中。其在中等降雨气候下的出色现场表现进一步巩固了其作为高性价比的灰色基础设施管道替代方案的地位。

强制性低影响开发(LID)分区法规

监管趋势正推动透水路面从一项可选的永续性措施转变为一项强制性要求。洛杉矶2024年的低影响开发(LID)条例强制规定,新建和改造的大规模不透水区域必须达到现场储存目标,并将透水混凝土定位为一站式解决方案。纽约市的《统一雨水管理规范》也采用了优先考虑储存的层级结构,同样提升了透水混凝土在更广泛的绿色基础设施框架中的重要性。开发商青睐透水混凝土,因为它只需单一规范即可满足多项要求(雨水管理、缓解热岛效应和获得LEED认证积分)。随着更多地区颁布类似法规,预计到本十年末,透水混凝土市场前景将持续走强。

需要有资格的承包商和专用浇筑设备

保持适当的孔隙率和均匀压实度是成功施工的关键,这与传统混凝土施工有显着差异。虽然NRMCA认证系统能够确保质量,但它限制了合格安装人员的数量,尤其是在培训资源匮乏的新兴市场。专用摊舖机和路面检测设备会增加承包商的初始成本,并减缓产能扩张,即使在政策支援较大的地区也是如此。这种人力和设备瓶颈会带来计划进度风险,并可能推高竞标价格,从而威胁到透水混凝土市场近期的成长。

细分市场分析

至2025年,水硬性透水混凝土将占透水混凝土市场57.20%的份额,成为停车场、人行道和广场等场所雨水管理的重要工具。市政低影响开发(LID)条例和海绵城市计划持续推动对这种设计风格的新需求,巩固了其在透水混凝土市场的主导地位。表面渗透测试技术和混合料优化技术的进步降低了维护成本,进一步增强了其对预算有限的公共部门负责人的吸引力。

目前结构性透水混凝土的绝对市场规模较小,但预计到2031年将以6.59%的复合年增长率成长,这主要得益于聚合物改质黏合剂的广泛应用。这种黏合剂能够在不影响孔隙连通性的前提下提高抗压强度。研究表明,水灰比为0.3是强度和水力性能同时提升的关键点,这促使工程师在低速道路路肩、停车场和公车站等场所采用透水结构路面。随着现场数据不断验证这些承载性能的提升,透水结构混凝土的市场规模预计将扩展到中型交通运输和轻工业应用领域。

区域分析

亚太地区预计将以6.78%的复合年增长率实现最快成长,占36.05%的最大市场。这主要得益于中国的「海绵城市」计划,该计划已在易涝都市区铺设了数千公里的透水性路面。印度Ultratech等製造商正在在地化生产透水添加剂,以满足季风季节的排水需求。同时,日本工程师正在利用预製模组化结构来缩短现场施工週期。这些技术创新表明,到预测期中期,该地区的市场规模预计将超过北美。

北美市场拥有成熟的法规结构、健全的承包商认证体系和丰厚的政府奖励。美国环保署 (EPA) 已将透水性路面列为最佳管理实践,这表明联邦政府的支持最终落实到各州的采购指南中。

在欧洲,随着成员国不断完善透水路面指南并融入循环经济原则(包括再生骨材的使用),监管主导的需求持续保持稳定。德国于2024年发布的透水路面设计标准正式确立了水力性能基准,消除了先前阻碍透水路面广泛应用的技术模糊之处。儘管南美洲和中东/非洲目前市场份额较小,但预计加速的都市化和气候变迁调适资金将推动透水路面试点计画的发展,逐步扩大这些新兴地区的透水混凝土市场。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 都市区突发性洪水灾害加剧

- 强制性低影响开发(LID)分区标准

- 北美对透水性路面的税收优惠

- 资料中心园区快速扩张(缓解热岛效应)

- 电气化的最后一公里仓库更喜欢凉爽的路面

- 市场限制

- 对认证安装人员和专用安装设备的需求

- 与传统混凝土相比,其结构承载能力有限。

- 主要城市开级骨材短缺

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 有意为之

- 水文

- 结构

- 透过使用

- 硬质景观

- 地板材料

- 其他用途

- 按最终用户行业划分

- 住宅

- 商业的

- 基础设施

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- AG Peltz Group

- Cementos Moctezuma

- Cemex SAB de CV

- Chaney Enterprises

- Concreto Ecologico de Mexico

- CRH

- Empire Blended Products

- Frank J. Fazzio and Sons Inc.

- Harmak

- Heidelberg Materials

- Holcim

- Raffin Construction

- Sika AG

- Ultra Ready-Mix Concrete

- UltraTech Cement Ltd.

第七章 市场机会与未来展望

Pervious Concrete market size in 2026 is estimated at USD 5.49 billion, growing from 2025 value of USD 5.16 billion with 2031 projections showing USD 7.44 billion, growing at 6.3% CAGR over 2026-2031.

Rising urban flash-flood events, mandatory low-impact-development (LID) codes, and corporate commitments to sustainable construction underpin steady demand for pervious concrete across residential, commercial, and public infrastructure projects. Municipal tax incentives and sponge-city programs further accelerate adoption, while advances in mix design and polymer modification are widening the material's structural use cases. Competitive intensity remains moderate as multinational cement producers integrate permeable solutions into low-carbon portfolios and regional contractors invest in specialized placement equipment. Supply-side challenges, such as chiefly skilled-labor shortages and aggregate scarcity in megacities, continue to temper growth prospects but have not derailed the broader upward trajectory of the pervious concrete market.

Global Pervious Concrete Market Trends and Insights

Growing Urban Flash-Flood Incidents

Municipalities increasingly deploy pervious concrete to manage stormwater at its source, thereby reducing peak flows that overload aging sewer networks. The material's ability to infiltrate up to 8 gallons per square foot per minute lowers runoff volumes during cloudbursts, as evidenced by sponge-city projects that now exceed 10 000 installations across Chinese metropolitan areas. Escalating precipitation intensities linked to climate change enhance the value proposition by turning pavements into active drainage assets rather than passive surfaces. Local governments favor the dual-functionality of pervious concrete because it consolidates pavement and stormwater infrastructure into one capital outlay. Proven field performance in moderate-rainfall climates further cements its status as a cost-effective alternative to oversized gray-infrastructure pipes.

Mandatory Low-Impact-Development (LID) Zoning Codes

Regulatory momentum is shifting permeable pavements from optional sustainability features to prescriptive requirements. Los Angeles' 2024 LID Ordinance obliges sites adding or replacing large impervious expanses to meet on-parcel retention targets, positioning pervious concrete as a turnkey compliance pathway. New York City's Unified Stormwater Rule pursues a retention-first hierarchy that equally elevates the material within broader green-infrastructure frameworks. Developers gravitate toward pervious concrete because it satisfies multiple mandates-stormwater, heat-island mitigation, and LEED credits-within one specification. As more jurisdictions draft parallel codes, forecast visibility for the pervious concrete market strengthens through the end of the decade.

Need for Certified Contractors and Specialized Placement Equipment

Successful installations rely on maintaining correct void ratios and uniform compaction, tasks that differ markedly from conventional concrete practice. The NRMCA's certification framework ensures quality but restricts the pool of qualified installers, especially in emerging markets where training resources are thin. Specialized roller screeds and pavement testers elevate start-up costs for contractors, slowing capacity expansion even in regions with strong policy tailwinds. This talent and equipment bottleneck imposes project scheduling risks and can inflate bid prices, dampening near-term growth in the pervious concrete market.

Other drivers and restraints analyzed in the detailed report include:

- Tax Incentives for Porous Pavements in North America

- Rapid Expansion of Data-Center Campuses (Heat-Island Mitigation)

- Scarcity of Open-Graded Aggregates in Megacities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hydrological specifications accounted for 57.20% of pervious concrete market share in 2025, anchoring the category's role as an on-site stormwater management tool for parking lots, sidewalks, and plazas. Municipal LID ordinances and sponge-city projects continue to funnel new demand into this design archetype, reinforcing its dominance in the pervious concrete market. Advances in surface infiltration testing and mix optimization are also reducing maintenance costs, preserving the appeal for public-sector buyers that operate on constrained budgets.

Structural designs, while currently smaller in absolute terms, are on course for a 6.59% CAGR to 2031, propelled by polymer-modified binders that elevate compressive strength without sacrificing void connectivity. Research pinpoints a 0.3 water-cement ratio as an inflection point where strength gains and hydraulic performance intersect, encouraging engineers to specify structural pervious pavements for low-speed roadway shoulders, parking garages, and bus stops. As field data validate these load-bearing enhancements, the pervious concrete market size for structural mixes is expected to broaden into mid-duty transit and light-industrial applications.

The Pervious Concrete Market Report is Segmented by Design (Hydrological and Structural), Application (Hardscape, Floors, and Other Applications), End-User Industry (Residential, Commercial, and Infrastructure), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific is the fastest-growing territory with a CAGR of 6.78% and also holds the largest share of 36.05%, spearheaded by China's sponge-city initiative, which alone accounts for thousands of pervious pavement kilometers across flood-prone urban districts. Indian manufacturers such as UltraTech are localizing permeable mixes to align with monsoon-drainage needs, while Japanese engineers leverage precast modular formats that shorten site installation cycles. Collectively, these innovations underscore the region's potential to eclipse North American volume midway through the forecast period.

North America's market is characterized by mature regulatory frameworks, robust contractor certification programs, and generous municipal incentives. The U.S. Environmental Protection Agency lists permeable pavements among its best-management practices, signaling federal endorsement that filters down to state procurement guidelines.

Europe posts steady, regulation-led demand as member states refine permeable pavement guidelines and integrate circular-economy principles, including recycled aggregates. German design codes published in 2024 formalize hydraulic-performance benchmarks, removing technical ambiguities that previously hampered adoption. While South America and the Middle-East and Africa contribute smaller shares for now, accelerating urbanization and climate-adaptation funding are expected to catalyze permeable-pavement pilots that will gradually scale the pervious concrete market across these emerging regions.

- A.G. Peltz Group

- Cementos Moctezuma

- Cemex S.A.B. de C.V.

- Chaney Enterprises

- Concreto Ecologico de Mexico

- CRH

- Empire Blended Products

- Frank J. Fazzio and Sons Inc.

- Harmak

- Heidelberg Materials

- Holcim

- Raffin Construction

- Sika AG

- Ultra Ready-Mix Concrete

- UltraTech Cement Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing urban flash-flood incidents

- 4.2.2 Mandatory low-impact-development (LID) zoning codes

- 4.2.3 Tax incentives for porous pavements in North America

- 4.2.4 Rapid expansion of data-centre campuses (heat-island mitigation)

- 4.2.5 Electrified last-mile warehouses favour cool pavements

- 4.3 Market Restraints

- 4.3.1 Need for certified contractors and specialised placement equipment

- 4.3.2 Limited structural load-bearing versus conventional concrete

- 4.3.3 Scarcity of open-graded aggregates in megacities

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Design

- 5.1.1 Hydrological

- 5.1.2 Structural

- 5.2 By Application

- 5.2.1 Hardscape

- 5.2.2 Floors

- 5.2.3 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Infrastructure

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 A.G. Peltz Group

- 6.4.2 Cementos Moctezuma

- 6.4.3 Cemex S.A.B. de C.V.

- 6.4.4 Chaney Enterprises

- 6.4.5 Concreto Ecologico de Mexico

- 6.4.6 CRH

- 6.4.7 Empire Blended Products

- 6.4.8 Frank J. Fazzio and Sons Inc.

- 6.4.9 Harmak

- 6.4.10 Heidelberg Materials

- 6.4.11 Holcim

- 6.4.12 Raffin Construction

- 6.4.13 Sika AG

- 6.4.14 Ultra Ready-Mix Concrete

- 6.4.15 UltraTech Cement Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

混凝土护栏市场:依产品类型、材料类型、安装方式、应用领域和最终用户划分,全球预测(2026-2032)

混凝土护栏市场:依产品类型、材料类型、安装方式、应用领域和最终用户划分,全球预测(2026-2032) 2026-2034年全球高压釜养护加气混凝土市场规模、份额、趋势及成长分析报告全球干混喷射混凝土市场规模、份额、趋势和成长分析报告(2026-2034)

2026-2034年全球高压釜养护加气混凝土市场规模、份额、趋势及成长分析报告全球干混喷射混凝土市场规模、份额、趋势和成长分析报告(2026-2034) 日本混凝土市场规模、份额、趋势及预测(依混凝土类型、应用、最终用途产业及地区划分),2026-2034年

日本混凝土市场规模、份额、趋势及预测(依混凝土类型、应用、最终用途产业及地区划分),2026-2034年 2026年全球混凝土材料市场报告

2026年全球混凝土材料市场报告 生物基混凝土市场-全球产业规模、份额、趋势、机会、预测:按形状、应用、区域和竞争格局划分,2021-2031年

生物基混凝土市场-全球产业规模、份额、趋势、机会、预测:按形状、应用、区域和竞争格局划分,2021-2031年 石膏混凝土市场规模、份额及成长分析(按类型、应用、建筑类型、最终用户和地区划分)-2026-2033年产业预测

石膏混凝土市场规模、份额及成长分析(按类型、应用、建筑类型、最终用户和地区划分)-2026-2033年产业预测 磺酸盐混凝土外加剂市场规模、份额和成长分析(按产品类型、应用、终端用户产业、混合料类型、功能和地区划分)—2026-2033年产业预测

磺酸盐混凝土外加剂市场规模、份额和成长分析(按产品类型、应用、终端用户产业、混合料类型、功能和地区划分)—2026-2033年产业预测 混凝土市场规模、份额和成长分析(按混凝土类型、应用、终端用户产业和地区划分)-2026-2033年产业预测石膏混凝土市场-2025-2030年预测

混凝土市场规模、份额和成长分析(按混凝土类型、应用、终端用户产业和地区划分)-2026-2033年产业预测石膏混凝土市场-2025-2030年预测