|

市场调查报告书

商品编码

1906240

种子黏合剂:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Seed Binders - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

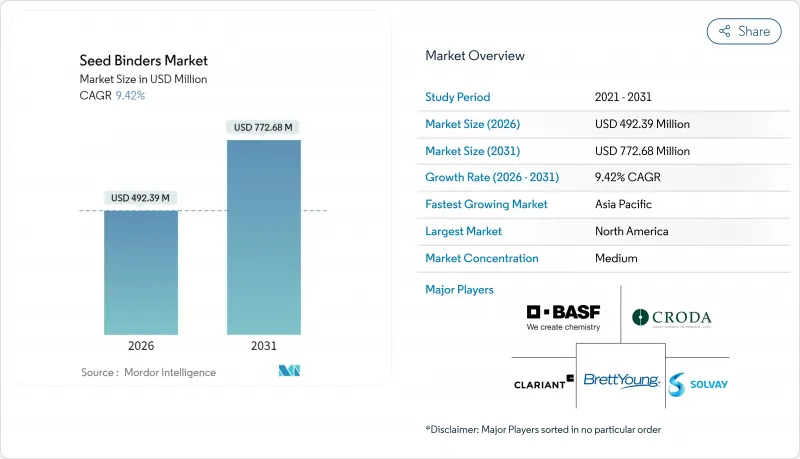

预计到 2026 年,种子黏合剂市场规模将达到 4.9,239 亿美元,高于 2025 年的 4.5 亿美元。

预计到 2031 年将达到 7.7268 亿美元,2026 年至 2031 年的复合年增长率为 9.42%。

对精准播种设备的投资不断增长、活性成分含量限制法规日益严格以及农场整合程度的提高,都推动了对能够改善种子流动性、种子形状均匀性和生物覆盖率的黏合剂的需求。种子黏合剂市场正转型为种子企业和设备製造商的策略性投入品类别,而薄膜创业投资。儘管石油化学原料价格波动和残留物合规成本限制了短期盈利,但供应商对可再生化学品和生物製剂的关注,持续为高价值作物创造了溢价机会。

全球种子黏合剂市场趋势与洞察

高价值作物中薄膜包覆种子的快速应用

薄膜包衣技术可改善播种过程中的流动性并减少粉尘,从而提高幼苗出苗率并降低工人接触粉尘的风险。玉米种子试验表明,产量提升带来的收益超过了包衣成本,并减少了漏播和重播现象。种子成本在其总生产预算中所占比例很小,因此,专业蔬菜种植者正在迅速采用这项技术,因为它能带来即时的投资回报。BASF推出了不含微塑胶的环保型包衣系统,其环保性能可与聚乙烯醇媲美。在那些透过配备GPS的播种机和即时种子分析技术来量化均匀单粒播种优势的地区,薄膜包衣技术的市场渗透率最高。此外,监管机构核准薄膜包衣技术可减少农药径流,也促进了该技术的应用。

精准播种技术的发展需要种子形状均匀。

现代播种机对种子大小的公差要求非常严格,以保持99%的分离率,这迫使种子生产商采用包覆和覆膜工艺来标准化种子形状。农艺学研究表明,播种不当会导致15-20%的收入损失,促使种植者采用统一性播种工艺。精密农业正在扩展到巴西、中国和印度,使得对形状可控种子的需求不再局限于美国和欧洲等传统核心地区。设备製造商也积极回应,销售专为包衣种子设计的播种机,进一步将种子捆扎机市场融入机械化趋势。不断上涨的农业劳动力成本正在推动机械化播种成为灌溉园艺的标准作业方式。

石油化学原料价格波动

预计到2025年中期,聚合级丙烯价格将上涨110.23美元/吨,将挤压聚乙烯醇生产商的利润空间。依赖价格挂钩合约的黏合剂供应商难以迅速转嫁成本,导致种子黏合剂市场短期盈利下降。地缘政治因素驱动的运费溢价推高了欧洲原料的到岸成本,使其高于亚洲,造成区域不平衡。儘管一些生产商透过长期合约进行避险,但这只是将风险延后。价格波动促使客户尝试生物基替代品,加速了从石油基产品转型为生物基产品的工作。

细分市场分析

截至2025年,聚乙烯醇将占据种子黏合剂市场41.10%的份额,这主要得益于其长期以来具有的可预测黏度、可靠的黏合性和低成本等优势。该细分市场的优势在于其与杀虫剂、杀菌剂和着色剂的广泛兼容性,这使得聚乙烯醇得以在谷物和饲料种子领域保持主导地位。受欧盟对微塑胶残留物监管力度加大的影响,生物聚合物替代品预计将推动种子黏合剂市场规模以11.55%的复合年增长率成长,在所有产品类型中增速最高。蛋白质和木质素基黏合剂近期涌现,旨在满足高端园艺种子市场的需求,在该市场中,无微塑胶标籤的产品价格更高。共聚物混合物和丙烯酸类产品则满足了诸如耐碱性土壤等特殊需求,而聚丙烯酸酯在缓释营养基质中继续发挥其独特的作用。植物油基聚氨酯网络的创新为潮湿热带气候下的种子储存提供了优于传统化学替代品的防潮屏障。

随着包衣生产线改造维修,采用低温干燥循环以防止天然聚合物的热解,生物聚合物的应用正在加速。加工商报告称,每吨处理过的种子可节省高达15%的能源,而这项额外收益与企业的减碳目标相符。领先的种子企业正利用生物聚合物的优势来打造差异化的品牌组合,尤其是在有机领域,因为合成聚合物残留会阻碍认证。巴西甘蔗发酵原料供应的扩大预示着未来成本将趋于一致。儘管预计整体产品结构将重新平衡,但现有的聚乙烯醇产能和价格竞争力将确保传统化学製程和新型化学製程在整个预测期内共存。

区域分析

预计到2025年,北美将创造全球整体31.60%的价值。此地位得益于北美农场规模大规模、播种机普及率高,以及相关法规认可种子处理可作为减少农场外化学物质迁移的措施。即时碳追踪模组(例如BASF的Xarvio生质能源指数)的整合,为决策支援增添了新的维度,能够量化种子包衣在植物生长初期之后的效果。贝克公司位于密苏里州的新大豆加工厂,进一步推动了加工能力的持续成长,并增强了支持种子包衣剂市场的区域服务生态系统。

亚太地区是成长最快的地区,预计到2031年复合年增长率将达到11.85%。中国每年1,200万吨的种子需求量、印度价值500亿美元的特种化学品产业基础,以及政府推行的精准播种项目,都是推动成长的主要动力。水稻和玉米生产的快速机械化带动了种子包衣的需求,而普遍存在的缺锌土壤则加速了微量元素包覆技术的应用。中国沿海地区可生物降解聚合物的在地化生产正在不断扩大,这不仅降低了关税负担,也缩短了当地种子企业的前置作业时间。

随着严格的微塑胶指令推动欧洲在2028年前逐步淘汰传统聚合物,欧洲预计将实现温和成长。 Incotec公司率先推出无微塑胶产品,使其在监管驱动的采购环境中占优势。南欧的蔬果产业正在采用高浓度生物涂层来减少农产品中的杀菌剂残留,这些农产品需接受严格的零售审核。南美洲的成长正在放缓,巴西的双季种植制度提高了包衣种子(一种促进种子在有限播种期内发芽的种子)的经济效益。阿根廷大力发展本地农业化学品生产,有助于稳定树脂供应,并降低黏合剂买家的外汇风险。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 扩大高价值作物中薄膜包覆种子的应用

- 精准播种技术的发展需要种子形状均匀。

- 加强监管,减少每公顷农药使用量

- 缓释微量营养素包衣的快速扩张

- 生物基黏合剂新资金筹措新兴企业的创业投资

- 将粘合剂功能整合到生物种子处理中

- 市场限制

- 石化原料价格波动

- 严格的残留物标准会延缓产品核可。

- 大种子物种中粘合剂效力的局限性

- 特种生物聚合物供应链风险

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依产品类型

- 聚乙烯醇

- 聚丙烯酸酯

- 生物聚合物基

- 其他的

- 按作物类型

- 谷物和谷类

- 油籽和豆类

- 水果和蔬菜

- 其他作物

- 按功能

- 薄膜涂层

- 造粒

- 覆层

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 法国

- 英国

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 亚太其他地区

- 中东

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- BASF SE

- Incotec Group BV(Croda International Plc)

- Clariant

- BrettYoung

- Covestro AG(Abu Dhabi National Oil Company)

- Germains Seed Technology(Associated British Foods)

- Michelman, Inc.

- SEEDPOLY Biocoatings Private Limited

- Solvay

- Omnia Specialities Pty(Omnia Holdings)

- Sekisui Specialty Chemicals America

- Borregaard AS

- Novonesis

- Centor Group

- SilviBio

第七章 市场机会与未来展望

The seed binders market size in 2026 is estimated at USD 492.39 million, growing from 2025 value of USD 450 million with 2031 projections showing USD 772.68 million, growing at 9.42% CAGR over 2026-2031.

Higher spending on precision planting hardware, mounting regulations that cap active-ingredient loads, and widespread farm consolidation jointly lift demand for binders that improve seed flow, shape uniformity, and biological coverage. Film coating and pelleting applications now influence planter engineering decisions, turning the seed binders market into a strategic input category for both seed companies and equipment manufacturers. Investment momentum stays strong as venture capital backs biodegradable polymer innovators that reduce microplastic risk while matching the handling properties of polyvinyl alcohol. Petrochemical feedstock volatility and residue-limit compliance costs temper near-term profitability, yet supplier focus on renewable chemistries and integrated biological formulas continues to unlock premium pricing opportunities across high-value crops.

Global Seed Binders Market Trends and Insights

Surging Adoption of Film-Coated Seeds in High-Value Crops

Film coating improves flowability and cuts planter dust, which in turn raises crop establishment rates and limits operator exposure. Corn seed trials show lower skips and doubles, delivering yield gains that outweigh coating costs. Specialty vegetable growers adopt the technology quickly because seed costs form a minor share of total production budgets, making return-on-investment immediate. BASF launched a microplastic-free system that matches polyvinyl alcohol performance without environmental baggage. Penetration is strongest in markets where GPS-enabled planters and real-time sowing analytics quantify the benefit of uniform seed singulation. Regulatory endorsement that film coatings lower pesticide runoff further accelerates uptake.

Growth of Precision Planting Techniques Demanding Uniform Seed Shape

Modern planters require tight seed-size tolerance to maintain 99% singulation, pressing seed companies to adopt pelleting and encrusting that standardize geometry. Agronomic studies link poor seed placement to 15-20% profit loss, which motivates grower adoption of uniformity treatments. Precision agriculture now expands in Brazil, China, and India, spreading the need for shaped seeds beyond traditional U.S. and European strongholds. Equipment makers reciprocate by marketing planters calibrated for coated seeds, further locking the seed binders market into the mechanization trend. Rising farm labor costs cement mechanized sowing as the default in irrigated horticulture, adding long-term momentum.

Fluctuating Petro-Chemical Raw Material Prices

Polymer-grade propylene prices are projected to climb USD 110.23 per metric ton by mid-2025, squeezing margins for polyvinyl alcohol producers. Binder suppliers that rely on formula-pricing contracts struggle to pass costs through quickly, reducing short-term profitability within the seed binders market. Freight premiums linked to geopolitical events elevate feedstock landed cost in Europe more than in Asia, creating a regional imbalance. Some manufacturers hedge with long-term contracts, yet such instruments only delay exposure. Volatility motivates customers to test bio-based substitutes, accelerating the shift away from petroleum derivatives.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Lower Pesticide Loading per Hectare

- Rapid Expansion of Controlled-Release Micro-Nutrient Coatings

- Stringent Residue Limits Delaying Product Approvals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, polyvinyl alcohol commanded 41.10% of the seed binders market share, underscoring a legacy of predictable viscosity, proven adhesion, and low cost. The segment's strength remains anchored in broad compatibility with insecticides, fungicides, and colorants, advantages that keep polyvinyl alcohol dominant in cereals and forage seeds. The seed binders market size for biopolymer-based alternatives is projected to post a 11.55% CAGR, the fastest among product classes, as regulatory scrutiny over microplastic persistence intensifies in the European Union. Recent launches of protein-based and lignin-derived binders cater to premium horticultural seeds where microplastic-free labeling commands price premiums. Copolymer blends and acrylics address niche needs such as alkaline-soil tolerance, while polyacrylates maintain distinct roles in controlled-release nutrient matrices. Innovation in vegetable-oil polyurethane networks unlocks moisture-barrier functions that outperform legacy chemistries when seeds are stored in humid tropical climates.

Biopolymer adoption accelerates as coating lines retrofit to handle lower-temperature drying cycles that prevent thermal degradation of natural polymers. Processors report up to 15% energy savings per metric ton of treated seed, a side benefit that aligns with corporate carbon-reduction pledges. Early-mover seed companies leverage biopolymer claims to differentiate brand portfolios, notably in organic segments where synthetic polymer residue disqualifies certification. Raw-material supply is scaling through sugar-cane fermentation in Brazil, signaling future cost parity. Overall, the product mix is set to rebalance, yet entrenched polyvinyl alcohol capacity and price competitiveness ensure the coexistence of legacy and novel chemistries during the forecast horizon.

The Seed Binders Market Report is Segmented by Product Type (Polyvinyl Alcohol, Polyacrylate, Biopolymer-Based, and Others), Crop Type (Cereals and Grains, Oilseeds and Pulses, Fruits and Vegetables, and Other Crops), Function (Film Coating, Pelleting, and Encrusting), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 31.60% of global value in 2025, a position anchored by large farm sizes, high planter adoption, and regulations that recognize seed treatments as a mitigation tool for off-field chemical movement. Integration of real-time carbon-tracking modules, such as BASF's Xarvio Bioenergy metric, adds a new layer of decision support that quantifies coating benefits beyond stand establishment. Beck's latest soybean processing plant in Missouri underscores continuing capital flow toward treating capacity, reinforcing a regional service ecosystem that sustains the seed binders market.

Asia-Pacific is the breakout geography with a 11.85% CAGR to 2031 as China's 12 million metric tons annual seed requirement and India's USD 50 billion specialty-chemicals base intersect with government programs that encourage precision sowing. Rapid mechanization of rice and maize production lifts pelleting demand, while widespread zinc-deficient soils accelerate micronutrient encrusting adoption. Local production of biodegradable polymers expands in coastal China, lowering tariff exposure and shortening lead times for regional seed companies.

Europe posts a moderate growth rate as its stringent microplastics directive pushes end-users to transition away from conventional polymers by 2028. Incotec's early launch of microplastic-free offerings positions the company favorably in a compliance-driven purchasing environment. Southern Europe's fruit and vegetable sectors adopt high-load biological coatings that lessen fungicide residue on produce destined for strict retailer audits. South America advances at slow growth rate because Brazil's double-cropping system magnifies the economic return on pelleted and encrusted seeds that speed emergence during compressed planting windows. Argentina's push for local agrochemical manufacturing supports resin availability, reducing foreign-exchange exposure for binder buyers.

- BASF SE

- Incotec Group BV (Croda International Plc)

- Clariant

- BrettYoung

- Covestro AG (Abu Dhabi National Oil Company)

- Germains Seed Technology (Associated British Foods)

- Michelman, Inc.

- SEEDPOLY Biocoatings Private Limited

- Solvay

- Omnia Specialities Pty (Omnia Holdings)

- Sekisui Specialty Chemicals America

- Borregaard AS

- Novonesis

- Centor Group

- SilviBio

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging adoption of film-coated seeds in high-value crops

- 4.2.2 Growth of precision planting techniques demanding uniform seed shape

- 4.2.3 Regulatory push for lower pesticide loading per hectare

- 4.2.4 Rapid expansion of controlled-release micro-nutrient coatings

- 4.2.5 Venture-capital funding in bio-based binder start-ups

- 4.2.6 Integration of binder functionality into biological seed treatments

- 4.3 Market Restraints

- 4.3.1 Fluctuating petro-chemical raw material prices

- 4.3.2 Stringent residue limits delaying product approvals

- 4.3.3 Limited binder efficacy on large-seed species

- 4.3.4 Supply-chain risk for specialty biopolymers

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Polyvinyl Alcohol

- 5.1.2 Polyacrylate

- 5.1.3 Biopolymer-based

- 5.1.4 Others

- 5.2 By Crop Type

- 5.2.1 Cereals and Grains

- 5.2.2 Oilseeds and Pulses

- 5.2.3 Fruits and Vegetables

- 5.2.4 Other Crops

- 5.3 By Function

- 5.3.1 Film Coating

- 5.3.2 Pelleting

- 5.3.3 Encrusting

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 France

- 5.4.3.3 United Kingdom

- 5.4.3.4 Russia

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Turkey

- 5.4.5.3 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Incotec Group BV (Croda International Plc)

- 6.4.3 Clariant

- 6.4.4 BrettYoung

- 6.4.5 Covestro AG (Abu Dhabi National Oil Company)

- 6.4.6 Germains Seed Technology (Associated British Foods)

- 6.4.7 Michelman, Inc.

- 6.4.8 SEEDPOLY Biocoatings Private Limited

- 6.4.9 Solvay

- 6.4.10 Omnia Specialities Pty (Omnia Holdings)

- 6.4.11 Sekisui Specialty Chemicals America

- 6.4.12 Borregaard AS

- 6.4.13 Novonesis

- 6.4.14 Centor Group

- 6.4.15 SilviBio

7 Market Opportunities and Future Outlook

晶圆代工厂黏合剂市场:按组件、部署模式、服务类型、应用和最终用户划分-2026-2032年全球市场预测黏合剂市场:2026-2032年全球市场预测(按产品类型、材料、尺寸、应用和分销管道划分)

晶圆代工厂黏合剂市场:按组件、部署模式、服务类型、应用和最终用户划分-2026-2032年全球市场预测黏合剂市场:2026-2032年全球市场预测(按产品类型、材料、尺寸、应用和分销管道划分) 全球有机黏合剂市场规模、份额、趋势和成长分析报告(2026-2034年)全球纤维黏合剂市场规模、份额、趋势和成长分析报告(2026-2034年)

全球有机黏合剂市场规模、份额、趋势和成长分析报告(2026-2034年)全球纤维黏合剂市场规模、份额、趋势和成长分析报告(2026-2034年) 全球纺织黏合剂市场

全球纺织黏合剂市场 日本苯乙烯丙烯酸乳胶(黏合剂)市场,2025-2029

日本苯乙烯丙烯酸乳胶(黏合剂)市场,2025-2029 纺织黏合剂市场-全球产业规模、份额、趋势、机会和预测,按材料(丙烯酸共聚物、苯乙烯丙烯酸酯共聚物、乙烯基丙烯酸酯共聚物等)细分,按应用、地区和竞争情况,2020-2030 年预测

纺织黏合剂市场-全球产业规模、份额、趋势、机会和预测,按材料(丙烯酸共聚物、苯乙烯丙烯酸酯共聚物、乙烯基丙烯酸酯共聚物等)细分,按应用、地区和竞争情况,2020-2030 年预测 有机黏合剂市场,按产品类型、形式、应用、国家和地区划分-2025 年至 2032 年全球产业分析、市场规模、市场份额及预测铸造黏合剂市场-全球产业规模、份额、趋势、机会和预测,按黏合剂类型、应用、化学黏合剂子类型、地区和竞争情况细分,2020-2030 年预测

有机黏合剂市场,按产品类型、形式、应用、国家和地区划分-2025 年至 2032 年全球产业分析、市场规模、市场份额及预测铸造黏合剂市场-全球产业规模、份额、趋势、机会和预测,按黏合剂类型、应用、化学黏合剂子类型、地区和竞争情况细分,2020-2030 年预测 亚太地区的聚氨酯粘合剂市场(2025年)

亚太地区的聚氨酯粘合剂市场(2025年)