|

市场调查报告书

商品编码

1906251

义大利地理空间分析:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Italy Geospatial Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

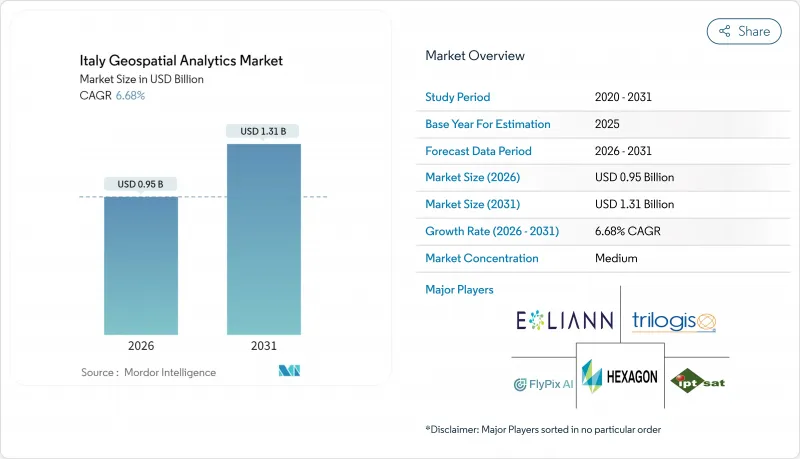

预计义大利地理空间分析市场将从 2025 年的 8.9 亿美元成长到 2026 年的 9.5 亿美元,到 2031 年将达到 13.1 亿美元,2026 年至 2031 年的复合年增长率为 6.68%。

欧盟资助的数位转型、热那亚大桥坍塌后强制性的基础设施安全措施以及2025年《公共工程法》规定的强制性BIM-GIS集成,共同推动了成长。米兰、都灵和博洛尼亚等城市的市政数位双胞胎部署正在创造持续的平台需求,而IRIDE地球观测卫星群则丰富了数据供应。随着HERE Technologies利用其与AWS价值11亿美元的合作关係提供人工智慧驱动的定位服务,云端采用正在加速。受2025年1月起强制性气候变迁保险政策的推动,对参数型保险的需求进一步扩大了高解析度风险分析的使用,随着企业将稀缺的太空资料科学技能外包,供应商也随之成长。

义大利地理空间分析市场趋势与洞察

义大利主要城市扩大智慧城市计划

米兰市实施了涵盖全市的数位双胞胎,整合了181平方公里的城市数据。该专案将物联网感测器与地理空间分析平台连接起来,以优化交通流量和建筑能源利用。都灵市将其拉瓦扎园区孪生计画的洞察扩展到全区资产监控,从而降低了12%的空间利用成本。波隆那的智慧运输控制中心每天处理487,700公里的道路数据,将尖峰时段的壅塞减少了9%。 5G行动网路支援资料流传输,促使各城市采用可扩展的云端原生地理空间解决方案。这些计划为可复製的欧盟智慧城市框架提供了蓝图,并增强了对义大利地理空间分析市场的需求。

促进桥樑、水坝和铁路等基础设施的健康监测

热那亚大桥事故后,义大利高速公路公司(Autostrade per Litaria)于2024年进行了1407次无人机飞行,利用合成孔径雷达(SAR)增强分析,将缺陷检测精度提高了11%。目前,国家指南要求6万座桥樑和542座大坝使用卫星干涉测量技术,以毫米级精度追踪其形变。数位双胞胎技术将卫星数据与地面感测器数据相结合,为16800公里铁路资产提供预测性维护平台,重新分配预算,并为分析供应商赢得多年期合同,从而推动了意大利地理空间分析市场的增长。

高级空间资料科学人才短缺

76%的义大利公司表示难以填补空间分析职缺,原因是每年仅有6,200名STEM(科学、技术、工程和数学)专业毕业生。 2024年,人工智慧投资仅占IT总预算的8.2%,低于欧盟13.5%的平均水平,凸显了劳动力供应链的技能短缺问题。大学难以更新云端原生地理空间架构的课程,迫使企业将部分功能外包给服务供应商。这导致计划成本居高不下,地理空间分析在义大利的市场渗透率缓慢。

细分市场分析

到2025年,解决方案将占据义大利地理空间分析市场56.00%的份额,因为买家倾向于选择端到端的平台来实现合规性和监控。然而,服务预计将缩小这一差距,实现12.55%的复合年增长率,这主要得益于BIM-GIS的强制应用,而BIM-GIS需要专业的配置知识。技能短缺日益严重,推动了外包业务的发展,顾问公司代表客户整合云端、人工智慧和地理空间功能。

义大利地理空间分析服务市场的扩张反映了託管数位双胞胎营运、预测性维护建模和自动化特征提取的需求。北部各市已签署多年期合同,涵盖平台建置、工作流程自动化和持续资料管理。中小企业选择基于订阅的託管服务以避免资本支出,这将进一步巩固该市场到2031年的两位数成长动能。

2025年,地表分析将占义大利地理空间分析市场规模的45.30%,主要驱动力来自地籍测量和公共产业资产管理。地理视觉化分析将以13.4%的复合年增长率成为成长最快的领域,这主要得益于3D城市孪生模型和身临其境型仪錶板的普及应用。网路分析将透过优化货运走廊,在物流领域保持稳定的渗透率,这些走廊每年处理1440亿吨公里的货物。

在义大利,地理视觉化领域在地理空间分析市场中所占份额不断增长,这主要得益于支援 WebGL 的平台,这些平台能够在普通装置上流畅播放逼真的模型。包括米兰斯福尔扎城堡在内的文化遗产管理机构利用这些工具来平衡文物保护义务与城市发展压力。企业则利用 3D 技术来缩短环境影响评估时间,并加快许可证核准。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 在义大利主要城市推广智慧城市项目

- 促进桥樑、水坝和铁路等基础设施的健康监测

- 扩大来自哥白尼计画和民用地球观测卫星星系的数据供应

- 根据新的《公共工程法》,BIM-GIS整合成为强制性要求。

- 利用地理空间风险评分的参数化保险的发展

- 欧盟復苏与韧性基金(RRF)为泛欧交通运输走廊(TEN-T走廊)提供的数位双胞胎资金

- 市场限制

- 免费/开放地理空间资料集的可用性

- 高技能空间资料科学家短缺

- 分散的市政采购和较长的销售週期

- Garante per la Protezione dati 加强隐私监控

- 价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 买方的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 报价

- 解决方案

- 服务

- 按类型

- 表面分析

- 网路分析

- 地理空间视觉化分析

- 最终用户

- 运输/物流

- 政府和国防机构

- 能源、公共产业和采矿

- 银行、金融服务和保险

- 农业/林业

- 房地产和建筑

- 其他最终用户

- 透过技术

- 地理资讯系统软体

- 遥感探测与地球观测

- 全球导航卫星系统和定位

- 空间资料科学与人工智慧平台

- 透过部署

- 云

- 本地部署

- 按公司规模

- 大公司

- 小型企业

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Airbus Defence and Space GmbH

- Ariespace Srl

- e-Geos SpA

- ESRI Italia Srl

- Flypix AI GmbH

- Fugro NV

- GECOsistema Srl

- Genius Loci Srl

- HERE Technologies Italia Srl

- Hexagon AB

- IPTSAT Srl

- Latitudo 40 Srl

- Planet Labs Italy Srl

- Rheticus Srl

- Telespazio SpA

- TomTom Italia SpA

- Trilogis Srl

- TeamDev Srl

- Topcon Positioning Italy Srl

- Trimble Italy Srl

第七章 市场机会与未来展望

The Italy geospatial analytics market is expected to grow from USD 0.89 billion in 2025 to USD 0.95 billion in 2026 and is forecast to reach USD 1.31 billion by 2031 at 6.68% CAGR over 2026-2031.

Growth rests on EU-funded digital transformation, infrastructure safety mandates after the Genoa bridge collapse, and mandatory BIM-GIS convergence under the 2025 Public Works Code. Municipal digital-twin rollouts in Milan, Turin, and Bologna generate sustained platform demand, while the IRIDE earth-observation constellation enriches data supply. Cloud deployment accelerates as HERE Technologies leverages a USD 1.1 billion AWS alliance to deliver AI-powered location services. Parametric insurance needs, catalyzed by compulsory climate coverage from January 2025, further expand high-resolution risk analytics consumption, and services vendors grow as firms outsource scarce spatial data science skills.

Italy Geospatial Analytics Market Trends and Insights

Smart-city programme scale-up across major Italian municipalities

Milan deployed a city-scale digital twin that integrates 181 sq km of urban data, combining IoT sensors with geospatial analytics platforms to optimize traffic flow and building energy use. Turin extends lessons from the Lavazza campus twin to district-wide asset monitoring that cuts space-utilization costs by 12%. Bologna's smart-mobility control room processes 487,700 km of road data daily, lowering peak-hour congestion by 9%. Fifth-generation mobile coverage underpins data streaming, pushing cities to procure scalable cloud-native geospatial solutions. These projects serve as blueprints for replicable EU smart-city frameworks that reinforce Italy's geospatial analytics market demand.

Infrastructure health-monitoring push for bridges, dams and rail

After the Genoa disaster, Autostrade per l'Italia ran 1,407 drone sorties in 2024, improving defect detection by 11% through SAR-enhanced analytics. National guidelines now require millimeter-level deformation tracking across 60,000 bridges and 542 dams via satellite interferometry. Digital twins link satellite feeds with ground sensors, supplying predictive maintenance dashboards for rail assets spanning 16,800 km. Resulting budget reallocations secure multiyear contracts for analytics vendors and fuel Italy geospatial analytics market growth.

Shortage of advanced spatial-data-science talent

Seventy-six percent of Italian firms report hiring difficulties for spatial analytics roles as annual STEM graduates tally just 6,200. AI investment sits at 8.2% of overall IT budgets in 2024, lagging the EU average of 13.5%, underscoring under-skilled labor pipelines. Universities struggle to refresh curricula on cloud-native geospatial architectures, prompting enterprises to outsource functions to service providers, which, in turn, inflates project costs and slows Italy's geospatial analytics market penetration.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory BIM-GIS convergence under Public Works Code

- Parametric-insurance growth using geospatial risk scores

- Fragmented municipal procurement and long sales cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions accounted for 56.00% of Italy geospatial analytics market share in 2025 as buyers preferred end-to-end platforms for compliance and monitoring. Services posted a 12.55% CAGR, however, and are projected to narrow the gap, propelled by mandatory BIM-GIS rollouts that require specialized configuration expertise. The escalating skills shortage drives outsourcing, letting consultancies integrate cloud, AI, and geospatial functions on behalf of clients.

Italy geospatial analytics market size gains within services reflect demand for managed digital-twin operations, predictive-maintenance modeling, and automated feature extraction. Northern municipalities award multi-year contracts covering platform setup, workflow automation, and continuous data stewardship. SMEs pick subscription-based managed services to sidestep capital outlays, reinforcing double-digit growth momentum through 2031.

Surface analysis delivered 45.30% of the Italy geospatial analytics market size in 2025, underpinned by cadastral mapping and utility asset management. Geo-visualization analysis grows fastest at 13.4% CAGR as three-dimensional city twins and immersive dashboards hit mainstream adoption. Network analysis retains steady uptake in logistics by optimizing freight corridors that handle 144 billion tonne-kilometers annually.

Italy's geospatial analytics market share gains for geo-visualization stem from WebGL-enabled platforms that stream photorealistic models on commodity devices. Heritage-site custodians, including Milan's Castello Sforzesco, employ these tools to reconcile preservation mandates with urban-development pressures. Enterprises leverage 3D insights to shorten environmental-impact assessments and accelerate permit approvals.

The Italy Geospatial Analytics Market Report is Segmented by Offering (Solution, Service), Type (Surface Analysis, and More), End-User (Transportation and Logistics, Government and Defence, and More), Technology (GIS Software, Remote-Sensing and Earth Observation, and More), Deployment (Cloud, On-Premise), Organisation Size (Large Enterprises, Smes), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Airbus Defence and Space GmbH

- Ariespace S.r.l.

- e-Geos S.p.A.

- ESRI Italia S.r.l.

- Flypix AI GmbH

- Fugro N.V.

- GECOsistema S.r.l.

- Genius Loci S.r.l.

- HERE Technologies Italia S.r.l.

- Hexagon AB

- IPTSAT S.r.l.

- Latitudo 40 S.r.l.

- Planet Labs Italy S.r.l.

- Rheticus S.r.l.

- Telespazio S.p.A.

- TomTom Italia S.p.A.

- Trilogis S.r.l.

- TeamDev S.r.l.

- Topcon Positioning Italy S.r.l.

- Trimble Italy S.r.l.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Smart-city programme scale-up across major Italian municipalities

- 4.2.2 Infrastructure health-monitoring push for bridges, dams and rail

- 4.2.3 Copernicus and private EO constellations expanding data supply

- 4.2.4 Mandatory BIM-GIS convergence under new Public Works Code

- 4.2.5 Parametric-insurance growth using geospatial risk scores

- 4.2.6 EU RRF digital-twin funds for TEN-T corridors

- 4.3 Market Restraints

- 4.3.1 Availability of free/open geospatial data sets

- 4.3.2 Shortage of advanced spatial-data-science talent

- 4.3.3 Fragmented municipal procurement and long sales cycles

- 4.3.4 Heightened privacy scrutiny by Garante per la Protezione dati

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Type

- 5.2.1 Surface Analysis

- 5.2.2 Network Analysis

- 5.2.3 Geo-visualisation Analysis

- 5.3 By End-user

- 5.3.1 Transportation and Logistics

- 5.3.2 Government and Defence

- 5.3.3 Energy, Utilities and Mining

- 5.3.4 Banking, Financial Services and Insurance

- 5.3.5 Agriculture and Forestry

- 5.3.6 Real-Estate and Construction

- 5.3.7 Other End-users

- 5.4 By Technology

- 5.4.1 GIS Software

- 5.4.2 Remote-Sensing and Earth Observation

- 5.4.3 GNSS and Positioning

- 5.4.4 Spatial Data-Science and AI Platforms

- 5.5 By Deployment

- 5.5.1 Cloud

- 5.5.2 On-premise

- 5.6 By Organisation Size

- 5.6.1 Large Enterprises

- 5.6.2 SMEs

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Airbus Defence and Space GmbH

- 6.4.2 Ariespace S.r.l.

- 6.4.3 e-Geos S.p.A.

- 6.4.4 ESRI Italia S.r.l.

- 6.4.5 Flypix AI GmbH

- 6.4.6 Fugro N.V.

- 6.4.7 GECOsistema S.r.l.

- 6.4.8 Genius Loci S.r.l.

- 6.4.9 HERE Technologies Italia S.r.l.

- 6.4.10 Hexagon AB

- 6.4.11 IPTSAT S.r.l.

- 6.4.12 Latitudo 40 S.r.l.

- 6.4.13 Planet Labs Italy S.r.l.

- 6.4.14 Rheticus S.r.l.

- 6.4.15 Telespazio S.p.A.

- 6.4.16 TomTom Italia S.p.A.

- 6.4.17 Trilogis S.r.l.

- 6.4.18 TeamDev S.r.l.

- 6.4.19 Topcon Positioning Italy S.r.l.

- 6.4.20 Trimble Italy S.r.l.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

地理空间分析市场:按类型、技术、部署模式、组织规模、应用程式和最终用户划分-2026-2032年全球市场预测汽车地理空间分析市场:按交付方式、部署方式、感测器类型、车辆类型、自动驾驶等级和应用划分-2026-2032年全球市场预测

地理空间分析市场:按类型、技术、部署模式、组织规模、应用程式和最终用户划分-2026-2032年全球市场预测汽车地理空间分析市场:按交付方式、部署方式、感测器类型、车辆类型、自动驾驶等级和应用划分-2026-2032年全球市场预测 2026年全球无人机地理空间分析市场报告

2026年全球无人机地理空间分析市场报告 地理空间分析市场分析及预测(至 2035 年):按类型、产品、服务、技术、组件、应用、部署、最终用户和解决方案划分2026年全球地理空间分析人工智慧市场报告2026年全球地理空间分析市场报告

地理空间分析市场分析及预测(至 2035 年):按类型、产品、服务、技术、组件、应用、部署、最终用户和解决方案划分2026年全球地理空间分析人工智慧市场报告2026年全球地理空间分析市场报告 全球地理空间分析市场规模、份额、趋势和成长分析报告(2026-2034)

全球地理空间分析市场规模、份额、趋势和成长分析报告(2026-2034) 日本地理空间分析市场报告(按组件、类型、技术、企业规模、部署模式、垂直产业和地区划分,2026-2034 年)

日本地理空间分析市场报告(按组件、类型、技术、企业规模、部署模式、垂直产业和地区划分,2026-2034 年) 到地理空间分析市场:2035年前的产业趋势和全球预测 - 各元件类型,各技术类型,各部署类型,各组织规模,各业界,各地区

到地理空间分析市场:2035年前的产业趋势和全球预测 - 各元件类型,各技术类型,各部署类型,各组织规模,各业界,各地区 地理空间分析:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030)

地理空间分析:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030)