|

市场调查报告书

商品编码

1906252

油脂化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Oleochemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

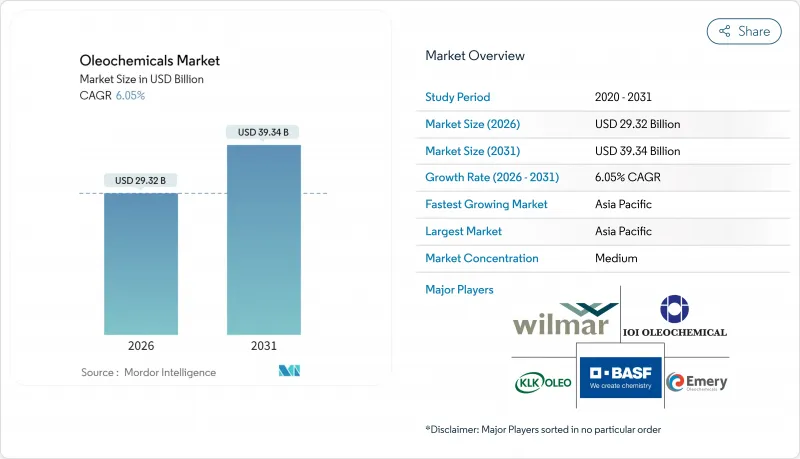

2025年油脂化学品市值为276.5亿美元,预计2031年将达到393.4亿美元,高于2026年的293.2亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 6.05%。

目前的扩张反映了政策主导的生物基表面活性剂需求、生物柴油掺混强制规定以及消费者对家用和个人护理产品中天然成分日益增长的偏好。光是印尼的B40计画就已将超过1500万千升棕榈油衍生的甲酯用于能源用途,加剧了传统化学应用领域的供应紧张。同时,欧盟的森林砍伐法规提高了合规成本,刺激了可追溯和认证供应链的投资。利用合成生物学方法将醣类和甲醇转化为脂肪酸和醇类的新兴技术正在兴起,预计将实现原料多样化并减少土地利用的影响。亚太地区仍然是生产和需求的重点,这得益于完善的棕榈油基础设施以及中国和东南亚个人护理产品消费的快速增长。

全球油脂化学品市场趋势及展望

扩大亚太地区的界面活性剂生产能力

中国、印尼和马来西亚界面活性剂生产计划的快速扩张,推动了对C12-C18脂肪酸和醇类的基准需求。 KLK OLEO在张家港新增20万吨年产能,反映了该地区在原料采购和物流方面的优势。本土个人护理品牌正积极采用天然乳化剂,以满足国内「清洁美容」标准并提升产品檔次。油价上涨推高了合成界面活性剂的价格,促使出口型生产商赢得对成本敏感的欧洲製造商的订单。世界各国政府正根据增值蓝图推动特种化学品的位置,进一步支持新建油脂化学品工厂。这些协同效应从根本上推动了油脂化学品市场的基础需求,并为缓解经济波动的影响奠定了基础。

个人护理和化妆品需求不断增长

预计2024年全球护肤零售额将成长9%,配方化学家们正越来越多地指定使用植物来源润肤剂、酯类和乳化剂。BASF的Verdesense产品线展示了蜡质植物基聚合物如何在不影响使用者体验的前提下取代微塑胶。北美消费者将可生物降解性视为最重要的购买因素,仅次于功效,这促使品牌商重新调整现有库存单位(SKU)的配方。亚洲跨国公司也反映了这一转变,正为其旗舰产品线寻求ECOCERT和COSMOS认证。基于鼠李醣脂的生物表面活性剂的商业试验显示出两位数的增长潜力,表明其有望在中期内取代合成乙氧基化物。由于优质化和永续性,特种油脂化学品的价格弹性仍然良好。

原物料价格波动

2024年,受厄尔尼诺现象导致产量下降的影响,原棕榈油期货价格在每吨780美元至970美元之间波动,对分离器和蒸馏器的毛利率带来压力。颱风对菲律宾种植园的破坏也导致椰子油价格飙升,进而推高了月桂酸衍生物的成本。北美买家转向巴西牛油,但出口量激增377%,导致当地油价上涨18%。生产商的应对措施是缩短合约期限并引入价格上涨条款。持续的价格波动使库存计划更加复杂,如果成本超过终端用户价格水平,则可能导致需求下降。

细分市场分析

到2025年,脂肪酸在全球油脂化学品市场将维持37.65%的份额,主要得益于清洁剂和个人护理产品的强劲需求。然而,在印尼、巴西和欧盟强制生质柴油计画的推动下,甲酯的油脂化学品市场规模预计将以7.68%的复合年增长率成长。透过发酵技术改进脂醇类可望重新调整成本曲线,但商业规模生产预计在2020年代末之前仍将受到限制。生物柴油生产造成的甘油供应过剩正在对价格构成下行压力,推动其在医药和食品领域的应用。政策主导的能源需求往往缺乏价格弹性,即使在经济放缓时期,也能支撑对甲酯的持续需求。同时,壬二酸和癸二酸等特种脂肪酸衍生物将以溢价交易,这将使能够为特定产品增值的综合生产商受益。

甲基酯的快速成长导致消费品价格上涨,在某些情况下,由于原料从肥皂成分转向其他用途,价格上涨不得不转嫁到消费品上。这促使市场参与企业寻求协同效应其市场通路的综效。拥有压榨、生质柴油和油脂化学品资产的综合农产品正在不断优化其资源配置。脂醇类的需求与无硫酸盐化妆品日益增长的趋势相交织,儘管酯类需求加速成长,但醇类的重要性依然凸显。由此形成了一个复杂的竞争格局,产品类型并非孤立运作,而是透过原料和产品特定的经济因素在更广泛的油脂化学品市场中相互关联。

区域分析

到2025年,亚太地区将占据油脂化学品市场47.12%的份额,这主要得益于棕榈油产业丛集的一体化发展和成本效益高的物流网络。该地区的复合年增长率预计将继续保持在7.92%,这主要受中国表面活性剂综合体业务运作和东南亚地区可支配收入成长的推动。然而,如果出口型企业未能达到欧盟和北美的永续性标准,则可能面临价格折扣,从而挤压利润空间。印尼生质柴油的普及正在推动原料转移和国内炼油厂投资,从而提升本地价值取得。马来西亚的特种化学品发展蓝图旨在2030年实现下游收入翻番,但技术纯熟劳工短缺可能会阻碍这一目标的实现。在南亚,肥皂需求正在成长,但其品质标准仍落后于经济合作暨发展组织市场,这限制了其价格的实现。

北美和欧洲正在努力平衡成熟的消费模式与技术创新。欧盟的政策已禁止使用间歇性二氧化碳排放量高的棕榈油,并鼓励使用废油和动物脂肪生产油脂化学品。同时,由创投支持的发酵Start-Ups已与跨国化妆品公司签订了销售合约。美国可再生柴油的成长吸收了部分动物脂肪,促使当地油脂化学品生产商不顾运费溢价,进口月桂酸油。在巴西的主导,南美洲是继亚太地区之后成长最快的地区。虽然不断扩大的压榨能力确保了大豆油的供应,但国内对生质柴油的需求仍占据相当大的比例。中东和非洲的产能落后,但需求正在成长。海湾国家正在鼓励在海事和采矿业中使用生物润滑剂,这为出口商创造了稳定成长的需求。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 扩大亚太地区的界面活性剂生产能力

- 个人护理和化妆品需求不断增长

- 脂肪酸甲酯生质柴油强制生产政策

- 向可生物降解和植物来源化学品过渡

- 利用合成生物学方法製备低成本脂醇类

- 市场限制

- 原物料价格波动

- 非政府组织和监管机构对不可持续棕榈油施加压力

- 在大宗应用领域,石油化学产品竞争激烈

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 产品类型

- 脂肪酸

- 脂醇类

- 甲酯

- 甘油

- 其他产品类型

- 原料来源

- 植物油

- 动物脂肪

- 终端用户产业

- 个人护理和化妆品

- 肥皂和清洁剂

- 食品/饮料

- 製药

- 聚合物

- 其他终端用户产业

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ASEAN

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- BASF

- Berg+Schmidt GmbH & Co. KG

- Cargill Inc.

- Croda International Plc

- Emery Oleochemicals

- Evonik Industries AG

- Godrej Industries Group

- IOI Oleochemical

- Kao Corporation

- KLK OLEO

- Kraton Corporation

- Musim Mas Group

- Oleon NV

- Procter & Gamble

- PT Ecogreen Oleochemicals

- VVF Ltd.

- Wilmar International Ltd.

第七章 市场机会与未来展望

The Oleochemicals Market was valued at USD 27.65 billion in 2025 and estimated to grow from USD 29.32 billion in 2026 to reach USD 39.34 billion by 2031, at a CAGR of 6.05% during the forecast period (2026-2031).

Current expansion reflects policy-driven demand for bio-based surfactants, biodiesel blending mandates, and accelerating consumer preference for natural ingredients across home and personal care applications. Indonesia's B40 program alone redirects more than 15 Million kilolitres of palm-based methyl esters into energy use, tightening supply for conventional chemical uses. Concurrently, the European Union (EU) Deforestation Regulation raises compliance costs and spurs investment in traceable, certified supply chains. Synthetic-biology routes that convert sugars or methanol into fatty acids and alcohols are emerging, promising feedstock diversification and lower land-use impacts. Asia-Pacific remains the focus of production and demand, supported by integrated palm infrastructure and fast-growing personal-care consumption in China and Southeast Asia.

Global Oleochemicals Market Trends and Insights

Growing Surfactants Capacity in Asia-Pacific

Surfactant manufacturing projects in China, Indonesia, and Malaysia are scaling rapidly, lifting baseline demand for C12-C18 fatty acids and alcohols. KLK OLEO's recent 200 ktpa expansion in Zhangjiagang underscores the region's feedstock and logistics advantage. Local personal-care brands are moving upmarket, incorporating naturally derived emulsifiers to meet domestic "clean beauty" standards. Export-oriented producers capture cost-sensitive orders from Europe as petro-inflation raises synthetic surfactant prices. Governments are promoting specialty chemicals under value-addition roadmaps, further anchoring new oleochemical units. The cumulative effect is a structural uplift in baseline offtake that cushions the oleochemicals market against cyclical swings.

Expanding Personal-Care and Cosmetics Demand

Global retail skin-care sales rose 9% in 2024, and formulating chemists increasingly specify plant-based emollients, esters, and emulsifiers. BASF's Verdessence line illustrates how waxy plant polymers replace microplastics without compromising sensory profiles . North American consumers rank biodegradability second only to efficacy in purchase drivers, pushing brand owners to reformulate legacy stock keeping unit (SKUs). Asian multinationals mirror this shift, aiming for ECOCERT and COSMOS accreditation on flagship lines. Bio-surfactant commercial trials using rhamnolipids show double-digit growth potential, signalling a medium-term substitution of synthetic ethoxylates. Collectively, premiumisation and sustainability converge to keep price elasticity favourable for specialty oleochemicals.

Feedstock Price Volatility

Crude palm oil futures swung between USD 780 and USD 970 per ton in 2024 following El Nino-linked yield drops, eroding gross margins for splitters and distillers. Coconut oil prices also spiked after typhoon damage to Philippine plantations, pressuring lauric acid derivative costs. North American buyers turned to Brazilian tallow, but a 377% export surge lifted local fat prices by 18%. Producers responded by shortening contract tenors and introducing price-escalation clauses. Persistent volatility complicates inventory planning and can trigger demand destruction when costs overshoot end-use price points.

Other drivers and restraints analyzed in the detailed report include:

- Biodiesel Mandates for Fatty Acid Methyl Esters

- Shift Toward Biodegradable, Plant-Based Chemicals

- NGO and Regulatory Pressure on Unsustainable Palm Oil

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Global fatty acids retained 37.65% Oleochemicals market share in 2025 on the back of solid detergent and personal-care demand. The Oleochemicals market size for methyl esters, however, is projected to rise at a 7.68% CAGR, supported by mandatory biodiesel programs across Indonesia, Brazil, and the EU. Fatty alcohol innovation through fermentation could recalibrate cost curves, yet commercial volumes will remain limited until late decade. Glycerine oversupply from biodiesel yields downward price pressure, encouraging its uptake in pharma and food applications. As policy-driven energy demand is largely price-inelastic, methyl ester offtake continues even during economic slowdowns. Conversely, specialty fatty acid derivatives such as azelaic and sebacic acids enjoy premium streams, benefiting integrated producers able to valorise by-products.

Methyl esters' rapid growth diverts feedstock away from soap noodles, occasionally forcing price pass-throughs in consumer staples. Market participants thus explore route-to-market synergies: integrated agribusinesses with crushing, biodiesel, and oleochemical assets optimise allocation daily. Fatty alcohol demand intersects with rising sulfate-free cosmetic trends, reinforcing alcohol's relevance despite ester acceleration. Net effect is a nuanced competitive landscape where product categories no longer operate in silos, but rather interlink through feedstock and coproduct economics within the wider Oleochemicals market.

The Oleochemicals Market Report is Segmented by Product Type (Fatty Acids, Fatty Alcohols, Methyl Esters, Glycerine, and More), Feedstock Source (Vegetable Oils and Animal Fats), End-User Industry (Personal Care and Cosmetics, Food and Beverages, Pharmaceuticals, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 47.12% Oleochemicals market share in 2025, anchoring the Oleochemicals market courtesy of integrated palm clusters and cost-efficient logistics. Regional CAGR of 7.92% will continue as China's surfactant complexes ramp up and Southeast Asian disposable incomes climb. Yet export-centric players must meet EU and North American sustainability thresholds or risk margin-eroding discounts. Indonesian biodiesel uptake diverts feedstock and fosters domestic refinery investments that lift local value capture. Malaysia's specialty chemicals roadmap aims to double downstream revenue by 2030, though skilled-labour shortages could constrain execution. South Asia shows rising demand for soap noodles, but quality specifications still lag the Organization for Economic Cooperation and Development (OECD) markets, tempering price realization.

North America and Europe balance mature consumption with technological innovation. EU policy bans high-ILUC palm, incentivising waste-oil and animal fat-based oleochemicals, while venture-backed fermentation start-ups secure offtake agreements with cosmetic multinationals. US renewable diesel growth sequesters tallows, prompting local oleochemical players to import lauric oils despite freight premiums. South America, led by Brazil, grows fastest after Asia-Pacific (APAC); expanding crush capacity ensures ready soybean oil supply, although domestic biodiesel uptake absorbs a significant slice. Middle East and Africa lag in production capacity but present incremental demand, with Gulf states encouraging bio-lubricant uptake in marine and mining sectors, offering gradual yet stable pull for exporters.

- BASF

- Berg+Schmidt GmbH & Co. KG

- Cargill Inc.

- Croda International Plc

- Emery Oleochemicals

- Evonik Industries AG

- Godrej Industries Group

- IOI Oleochemical

- Kao Corporation

- KLK OLEO

- Kraton Corporation

- Musim Mas Group

- Oleon NV

- Procter & Gamble

- PT Ecogreen Oleochemicals

- VVF Ltd.

- Wilmar International Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Surfactants Capacity in Asia-Pacific

- 4.2.2 Expanding Personal-care and Cosmetics Demand

- 4.2.3 Biodiesel Mandates for Fatty Acid Methyl Esters

- 4.2.4 Shift Toward Biodegradable, Plant-based Chemicals

- 4.2.5 Synthetic-biology Routes to Low-cost Fatty Alcohols

- 4.3 Market Restraints

- 4.3.1 Feedstock Price Volatility

- 4.3.2 NGO and Regulatory Pressure on Unsustainable Palm Oil

- 4.3.3 Petrochemical Price Competition in Bulk Applications

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 Product Type

- 5.1.1 Fatty Acids

- 5.1.2 Fatty Alcohols

- 5.1.3 Methyl Esters

- 5.1.4 Glycerine

- 5.1.5 Other Product Types

- 5.2 Feedstock Source

- 5.2.1 Vegetable Oils

- 5.2.2 Animal Fats

- 5.3 End-user Industry

- 5.3.1 Personal Care and Cosmetics

- 5.3.2 Soap and Detergent

- 5.3.3 Food and Beverages

- 5.3.4 Pharmaceuticals

- 5.3.5 Polymers

- 5.3.6 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 BASF

- 6.4.2 Berg+Schmidt GmbH & Co. KG

- 6.4.3 Cargill Inc.

- 6.4.4 Croda International Plc

- 6.4.5 Emery Oleochemicals

- 6.4.6 Evonik Industries AG

- 6.4.7 Godrej Industries Group

- 6.4.8 IOI Oleochemical

- 6.4.9 Kao Corporation

- 6.4.10 KLK OLEO

- 6.4.11 Kraton Corporation

- 6.4.12 Musim Mas Group

- 6.4.13 Oleon NV

- 6.4.14 Procter & Gamble

- 6.4.15 PT Ecogreen Oleochemicals

- 6.4.16 VVF Ltd.

- 6.4.17 Wilmar International Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

- 7.2 Increased Use of Biofuels

油脂化学品市场报告:按类型、形态、应用、原料和地区划分(2026-2034年)

油脂化学品市场报告:按类型、形态、应用、原料和地区划分(2026-2034年) 全球油脂化学品市场规模、份额、趋势和成长分析报告(2026-2034年)

全球油脂化学品市场规模、份额、趋势和成长分析报告(2026-2034年) 2026 年全球油脂化学品市场报告2026年全球特种油脂化学品市场报告

2026 年全球油脂化学品市场报告2026年全球特种油脂化学品市场报告 全球油脂化学品市场,2026-2030日本油脂化学品市场报告(按类型、形态、应用、原料和地区划分,2026-2034年)

全球油脂化学品市场,2026-2030日本油脂化学品市场报告(按类型、形态、应用、原料和地区划分,2026-2034年) 特种油脂化学品市场规模、份额及成长分析(按产品、原料、应用及地区划分)-2026-2033年产业预测

特种油脂化学品市场规模、份额及成长分析(按产品、原料、应用及地区划分)-2026-2033年产业预测 特种油脂化学品市场-全球产业规模、份额、趋势、机会和预测,依产品、应用、地区和竞争格局划分,2020-2030年预测油脂化学品市场-全球产业规模、份额、趋势、机会与预测,依产品、应用、地区和竞争细分,2020-2030 年预测

特种油脂化学品市场-全球产业规模、份额、趋势、机会和预测,依产品、应用、地区和竞争格局划分,2020-2030年预测油脂化学品市场-全球产业规模、份额、趋势、机会与预测,依产品、应用、地区和竞争细分,2020-2030 年预测 油脂化学品市场,按产品类型、来源、最终用户、国家和地区划分-2025 年至 2032 年全球产业分析、市场规模、市场份额及预测

油脂化学品市场,按产品类型、来源、最终用户、国家和地区划分-2025 年至 2032 年全球产业分析、市场规模、市场份额及预测