|

市场调查报告书

商品编码

1906256

亚磷酰胺:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Phosphoramidite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

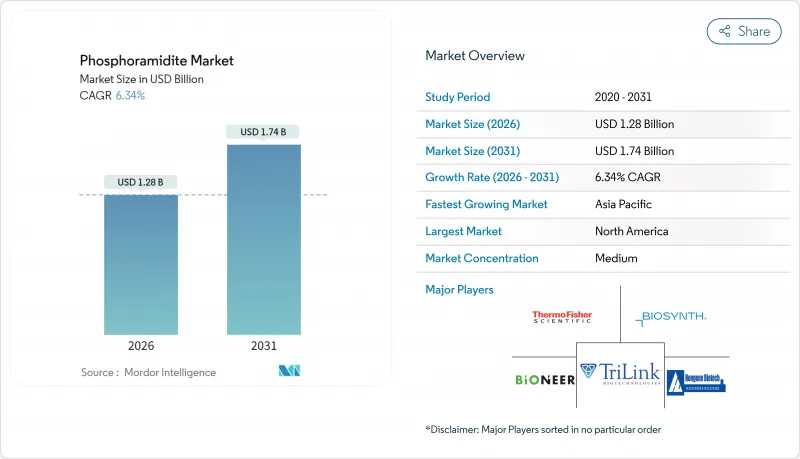

预计到 2026 年,亚磷酰胺市值将达到 12.8 亿美元,高于 2025 年的 12 亿美元。

预计到 2031 年,该市场规模将达到 17.4 亿美元,2026 年至 2031 年的复合年增长率为 6.34%。

治疗性寡核苷酸、基因编辑技术以及合成生物学规模化生产的进步正汇聚成一股强劲的需求成长动能。美国食品药物管理局(FDA) 于 2024 年核准的两种药物——伊美替司他 (imetelstat) 和奥利扎森 (olezarsen)——证明了此类药物的疗效,并推动了整个价值链的产能扩张。同时,对高通量合成技术的投资降低了单位成本,提高了其在诊断和研究应用中的可用性。政府对基因组医学的津贴,以及产业为确保地域分散的供应链所做的努力,进一步增强了长期消费前景。

全球亚磷酰胺市场趋势与洞察

核酸疗法研发管线快速扩张

2024年核准的两款First-in-Class药物imetelstat和olezarsen证实了反义寡核苷酸和GalNAc偶联平台的临床疗效,推动了目前全球正在进行的229项肿瘤临床试验。同年发布的FDA综合指南简化了药理学和安全性要求,并缩短了研发週期。这些协同效应导致后期研发项目数量激增,这些项目需要公斤级符合GMP规范的亚磷酰胺。随着每个候选药物从早期阶段推进商业化阶段,随着生产规模从克级扩大到吨级,年需求量增加一倍。随着药物组合从罕见疾病转向常见心血管代谢疾病,每位患者族群的药物需求将进一步成长,预计未来十年需求将持续成长。

加速合成生物学平台的应用

合成生物学领域整体正经历两位数成长,主要得益于RNA疫苗、精准酵素和生物基化学品的发展。 DNA晶圆代工厂和云端设计工具支援超高通量合成,消耗大量的亚磷酰胺。酵素方法,例如Codexis公司98%偶联效率的平台,可以减少杂质并补充现有的化学方法,但目前还无法取代它们。人工智慧的整合优化了建造设计,增加了序列的复杂性和长度,这两方面都会导致每批次试剂用量的增加。在美国、德国和新加坡新建生物合成平台的投资,凸显了开发人员对化学合成建构模组的坚定信心。

符合GMP标准的生产设施需要高额资金投入。

光是新建工厂扩建一项就可能耗资超过7.25亿美元,例如安捷伦公司在2025年宣布,其寡核苷酸产能将翻倍,并于2026年开始营运。建设的复杂性体现在反应器组、溶剂回收系统和C级洁净室等各个方面,验证期往往长达数年。小规模的新参与企业通常难以获得资金筹措,导致产能集中在财力雄厚的现有企业手中。较长的投资回收期和技术过时的风险加剧了投资风险,即使市场需求不断增长,也阻碍了新企业进入市场。

细分市场分析

到2025年,DNA亚磷酰胺将占据亚磷酰胺市场51.85%的份额,其在反义和诊断探针合成中的核心作用将继续推动市场成长。儘管基数较小,但由于对体内稳定性的需求不断增长,LNA亚型预计将以8.21%的复合年增长率超越其他化学类型。随着多公斤级肿瘤和心臟病药物进入后期临床试验,用于DNA诱变的亚磷酰胺市场预计将稳定扩张。学术界的持续需求,以及新兴的CRISPR引导RNA工作流程,将支撑RNA亚磷酰胺的需求,而2'-O-甲基化和硫代磷酸酯等特殊修饰则在高价格分布创造了一个利基市场。

多重修饰策略的进步,例如1,3-二硫杂环己烷-2-基甲氧羰基酰化碱基的方法,正在扩大联合治疗的设计可能性。一些生物技术公司正在测试的酶连接构建方法,与化学DNA亚磷酰胺相比,尤其是在高度修饰的DNA骨架中,它们具有互补而非竞争关係。

到2025年,受治疗产品线不断扩展和垂直整合生产模式的推动,製药和生物技术公司将占据亚磷酰胺市场56.74%的份额。然而,外包趋势正在推动合约开发和生产组织(CDMO)和受託研究机构(CRO)的发展,预计这两类组织在预测期内将以9.18%的最快成长。药明康德(WuXi STA)的27条运作中的寡核苷酸生产线以及TriLink的CleanCap授权模式凸显了市场对相关服务的强劲需求。学术机构保持着稳定的基础需求,而诊断检查室则越来越多地订购用于受监管检测套组的高纯度产品。

区域分析

预计到2025年,北美将占据39.78%的收入份额,这得益于完善的监管环境、大规模开发商的存在以及大量创业投资的流入。默克集团(Merck KGaA)斥资7,600万美元对其位于密苏里州的生物偶联工厂进行升级,显示该地区的资本密集度将持续保持高位。此外,美国透过TriLink许可生态系统在CleanCap支持的mRNA技术领域也主导,进一步巩固了该国的创新丛集。

亚太地区预计到2031年将以7.29%的复合年增长率成长,主要受低生产成本和国内对先进治疗方法日益增长的需求驱动。无锡STA位于泰兴的占地169英亩的工厂自2024年初运作以来,代表了国内合约研发生产机构(CDMO)的规模。鼓励「中国+多国」采购的政策转变,以及修订后的反间谍法规,正促使跨国公司将其供应链多元化至印度、越南和泰国,从而重塑其供应链的区域结构。

欧洲凭藉先进的製造技术和严格的品质标准,仍然是重要的战略基地。 BioSpring位于奥芬巴赫的RNA大型生产设施计画于2027年竣工,届时将成为全球最大的专用核酸生产设施之一,彰显了该地区对高价值生物製药的承诺。加上欧洲药物寡核苷酸联盟的协调工作,该地区将继续保持其在卓越製造和绿色化学应用方面的标竿地位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 核酸疗法研发管线快速扩张

- 加速合成生物学平台的应用

- 对个人化医疗和诊断的需求日益增长

- 政府资助基因组研究倡议

- 高通量寡核苷酸合成的技术进步

- 对安全生物製药供应链的策略性投资

- 市场限制

- 符合GMP标准的生产设施需要高额资金投入。

- 严格的原料纯度监管标准

- 与溶剂废弃物处理相关的环境问题。

- 复杂低聚物化学领域熟练劳动力短缺

- 监管环境

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按类型

- DNA亚磷酰胺

- RNA亚磷酰胺

- LNA亚磷酰胺

- 2'-O-甲基化RNA亚磷酰胺

- 特种/改质亚磷酰胺

- 最终用户

- 製药和生物技术公司

- 学术和研究机构

- CDMO 和 CRO

- 诊断实验室

- 其他最终用户

- 透过使用

- 治疗性寡核苷酸

- 诊断试剂

- 基因和细胞疗法

- 合成生物学与基因编辑

- 研究工具

- 按纯度等级

- 标准调查等级

- 高效液相层析级

- GMP级

- 超高纯度

- 透过合成方法

- 固相化学合成

- 酶促DNA/RNA合成

- 化学-酵素混合法

- 按生产规模

- 研究/创造规模(小于1毫摩尔)

- 试验/临床规模(>100 mmol)

- 商业/GMP生产规模(100毫摩尔或以上)

- 地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 亚太其他地区

- 中东和非洲

- GCC

- 南非

- 其他中东和非洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 市占率分析

- 公司简介

- Thermo Fisher Scientific Inc.

- Danaher Corp.(Integrated DNA Technologies)

- Merck KGaA(Sigma-Aldrich)

- Biosynth Ltd

- TriLink BioTechnologies

- Bioneer Corporation

- Hongene Biotech Corp.

- LGC Biosearch Technologies

- Glen Research

- Bachem AG

- Eurofins Genomics

- Synbio Technologies

- PolyOrg, Inc.

- Creative Biolabs, Inc.

- Lumiprobe Corp.

- QIAGEN NV

- Agilent Technologies Inc.

- Twist Bioscience

- BOC Sciences

- GenScript Biotech

第七章 市场机会与未来展望

Phosphoramidite market size in 2026 is estimated at USD 1.28 billion, growing from 2025 value of USD 1.20 billion with 2031 projections showing USD 1.74 billion, growing at 6.34% CAGR over 2026-2031.

Therapeutic oligonucleotides, gene-editing advances, and synthetic biology scale-up collectively underpin robust demand momentum. Two United States Food and Drug Administration approvals in 2024-imetelstat and olezarsen-validated the drug-class and triggered capacity additions across the value chain. Parallel investments in high-throughput synthesis technologies have lowered unit costs, improving accessibility for diagnostics and research applications. Government grants for genomic medicine along with industry initiatives to secure geographically diverse supply chains further reinforce long-term consumption prospects.

Global Phosphoramidite Market Trends and Insights

Rapid Expansion of Nucleic Acid Therapeutics Pipeline

Two first-in-class approvals in 2024, imetelstat and olezarsen, confirmed clinical efficacy for antisense and GalNAc-conjugated platforms and encouraged 229 oncology trials now active worldwide. Comprehensive FDA guidance issued the same year has streamlined pharmacology and safety expectations, shortening development timelines. The cumulative result is a rising pool of late-stage assets requiring kilogram-scale GMP phosphoramidites. Each candidate's progression from early stage to commercial launch multiplies annual demand because manufacturing campaigns scale from grams to multiple metric tons. As pharmaceutical portfolios pivot from rare disorders to prevalent cardiometabolic diseases the material requirement per patient cohort swells further, extending demand visibility into the next decade.

Accelerating Adoption of Synthetic Biology Platforms

The wider synthetic biology arena is expanding at double-digit rates, driven by RNA vaccines, precision enzymes, and bio-based chemicals. DNA foundries and cloud-based design tools support ultrahigh-throughput syntheses that consume vast volumes of phosphoramidites. Enzymatic approaches such as Codexis' 98% coupling-efficiency platform reduce impurities and complement established chemical methods without yet displacing them. Integration of artificial intelligence optimizes construct design, raising sequence complexity and length, both of which raise reagent usage per batch. Capital spending by new biofoundries in the United States, Germany, and Singapore evidences durable developer confidence in chemically synthesized building blocks.

High Capital Requirements for GMP-Grade Manufacturing Facilities

A single greenfield plant expansion can exceed USD 725 million, as confirmed by Agilent's 2025 announcement to double oligonucleotide output with operations commencing in 2026. Build-out complexity spans reactor suites, solvent recovery systems, and Class C cleanrooms, while validation timelines stretch to multiple years. Smaller entrants often struggle to marshal comparable funding, which concentrates capacity among financially robust incumbents. Extended payback periods and the prospect of technology obsolescence amplify investment risk, thereby tempering market entry despite rising demand.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Personalized Medicine and Diagnostics

- Government Funding for Genomic Research Initiatives

- Stringent Regulatory Standards for Raw Material Purity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

DNA phosphoramidites held 51.85% of the phosphoramidite market share in 2025 and continue anchoring the phosphoramidite market thanks to their central role in antisense and diagnostic probe synthesis. LNA subtypes, while representing a smaller base, are forecast to outpace other chemistries at an 8.21% CAGR amid rising in vivo stability needs. The phosphoramidite market size for DNA-based variants is projected to expand steadily as multi-kilogram oncology and cardiology drug campaigns enter late-stage trials. Continued academic demand plus new CRISPR guide-RNA workflows sustain RNA amidite volume, whereas specialty modifications such as 2'-O-methyl and thiophosphate commands premium pricing niches.

Advances in multi-modification strategies, exemplified by the 1,3-dithian-2-yl-methoxycarbonyl method for acylated bases, are broadening design possibilities for combination therapies. Enzymatic ligation-based construction methods trialed by several biotech firms complement, rather than compete with, chemical DNA amidites, particularly for highly modified backbones.

Pharmaceutical and biotechnology enterprises consumed 56.74% of the phosphoramidite market in 2025, driven by expanding therapeutic pipelines and vertically integrated manufacturing ambitions. Outsourcing trends nonetheless propel CDMOs and CROs, whose 9.18% CAGR marks the fastest uptake in the forecast horizon. WuXi STA's 27 operational oligonucleotide lines and TriLink's CleanCap licensing model attest to brisk service demand. Academic institutions preserve a meaningful baseline volume, while diagnostic labs increasingly order high-purity lots for regulated test kits.

The Phosphoramidite Market Report is Segmented by Type (DNA Phosphoramidites, and More), End-User (Pharmaceutical & Biotechnology Companies, and More), Application (Therapeutic Oligonucleotides, and More), Purity Grade (Standard Research Grade, and More), Synthesis Method (Solid-Phase Chemical Synthesis, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America posted 39.78% revenue share in 2025, underpinned by established regulatory clarity, large developer presence, and significant venture-capital flows. Merck KGaA's USD 76 million upgrade of its Missouri bioconjugation site illustrates sustained capital deepening within the region. The United States also leads in CleanCap-enabled mRNA technologies through TriLink's licensing ecosystem, reinforcing domestic innovation clusters.

Asia-Pacific is forecast to grow at 7.29% CAGR through 2031, propelled by lower production costs and rising internal demand for advanced therapies. WuXi STA's 169-acre Taixing facility, operational since early 2024, exemplifies the scale domestic CDMOs are reaching. Policy shifts encouraging "China-plus-many" sourcing, combined with updated anti-espionage regulations, are prompting multinational firms to diversify across India, Vietnam, and Thailand, reshaping supply-chain geography.

Europe maintains a strategic foothold through advanced manufacturing and rigorous quality norms. BioSpring's Offenbach RNA megafacility, on track for completion in 2027, will be among the world's largest dedicated nucleic-acid plants, underscoring regional commitment to high-value biologics. Coupled with the European Pharma Oligonucleotide Consortium's harmonization work, the continent remains a reference point for manufacturing excellence and green-chemistry adoption.

- Thermo Fisher Scientific

- Danaher Corp. (Integrated DNA Technologies)

- Merck

- Biosynth Ltd

- TriLink BioTechnologies

- Bioneer

- Hongene Biotech Corp.

- LGC Biosearch Technologies

- Glen Research

- Bachem AG

- Eurofins

- Synbio Technologies

- PolyOrg, Inc.

- Creative Biolabs, Inc.

- Lumiprobe Corp.

- QIAGEN

- Agilent Technologies

- Twist Bioscience

- BOC Sciences

- GenScript Biotech

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Expansion of Nucleic Acid Therapeutics Pipeline

- 4.2.2 Accelerating Adoption of Synthetic Biology Platforms

- 4.2.3 Growing Demand For Personalized Medicine and Diagnostics

- 4.2.4 Government Funding For Genomic Research Initiatives

- 4.2.5 Technological Advancements in High-Throughput Oligo Synthesis

- 4.2.6 Strategic Investments in Secure Biopharma Supply Chains

- 4.3 Market Restraints

- 4.3.1 High Capital Requirements for GMP-Grade Manufacturing Facilities

- 4.3.2 Stringent Regulatory Standards for Raw Material Purity

- 4.3.3 Environmental Concerns Over Solvent Waste Disposal

- 4.3.4 Limited Skilled Workforce For Complex Oligo Chemistry

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat Of New Entrants

- 4.5.2 Bargaining Power Of Buyers

- 4.5.3 Bargaining Power Of Suppliers

- 4.5.4 Threat Of Substitutes

- 4.5.5 Intensity Of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 DNA Phosphoramidites

- 5.1.2 RNA Phosphoramidites

- 5.1.3 LNA Phosphoramidites

- 5.1.4 2'-O-Methyl RNA Phosphoramidites

- 5.1.5 Specialty / Modified Phosphoramidites

- 5.2 By End-User

- 5.2.1 Pharmaceutical & Biotechnology Companies

- 5.2.2 Academic & Research Institutes

- 5.2.3 CDMOs & CROs

- 5.2.4 Diagnostic Laboratories

- 5.2.5 Other End-Users

- 5.3 By Application

- 5.3.1 Therapeutic Oligonucleotides

- 5.3.2 Diagnostics

- 5.3.3 Gene & Cell Therapy

- 5.3.4 Synthetic Biology & Gene Editing

- 5.3.5 Research Tools

- 5.4 By Purity Grade

- 5.4.1 Standard Research Grade

- 5.4.2 HPLC Grade

- 5.4.3 GMP Grade

- 5.4.4 Ultra-High Purity Grade

- 5.5 By Synthesis Method

- 5.5.1 Solid-Phase Chemical Synthesis

- 5.5.2 Enzymatic DNA/RNA Synthesis

- 5.5.3 Hybrid Chemical-Enzymatic

- 5.6 By Production Scale

- 5.6.1 Research / Discovery Scale (<1 mmol)

- 5.6.2 Pilot / Clinical Scale (1>100 mmol)

- 5.6.3 Commercial / GMP Manufacturing Scale (>100 mmol)

- 5.7 Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 Australia

- 5.7.3.5 South Korea

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East & Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East & Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Thermo Fisher Scientific Inc.

- 6.3.2 Danaher Corp. (Integrated DNA Technologies)

- 6.3.3 Merck KGaA (Sigma-Aldrich)

- 6.3.4 Biosynth Ltd

- 6.3.5 TriLink BioTechnologies

- 6.3.6 Bioneer Corporation

- 6.3.7 Hongene Biotech Corp.

- 6.3.8 LGC Biosearch Technologies

- 6.3.9 Glen Research

- 6.3.10 Bachem AG

- 6.3.11 Eurofins Genomics

- 6.3.12 Synbio Technologies

- 6.3.13 PolyOrg, Inc.

- 6.3.14 Creative Biolabs, Inc.

- 6.3.15 Lumiprobe Corp.

- 6.3.16 QIAGEN N.V.

- 6.3.17 Agilent Technologies Inc.

- 6.3.18 Twist Bioscience

- 6.3.19 BOC Sciences

- 6.3.20 GenScript Biotech

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

2'-OMe-C 淋巴酰胺市场按产品类型、应用、最终用户和分销管道划分,全球预测,2026-2032 年2'-OMe-G亚磷酰胺市场按产品类型、应用、最终用户和分销管道划分,全球预测,2026-2032年2'-OMe-Ibu-G亚磷酰胺市场按纯度等级、产品形式、方法、应用和最终用户划分 - 全球预测(2026-2032)DMT-dG亚磷酰胺市场按纯度等级、合成规模、技术、应用和最终用户划分,全球预测,2026-2032年亚磷酰胺市场按应用、类型、最终用户和形态划分 - 全球预测 2025-2032

2'-OMe-C 淋巴酰胺市场按产品类型、应用、最终用户和分销管道划分,全球预测,2026-2032 年2'-OMe-G亚磷酰胺市场按产品类型、应用、最终用户和分销管道划分,全球预测,2026-2032年2'-OMe-Ibu-G亚磷酰胺市场按纯度等级、产品形式、方法、应用和最终用户划分 - 全球预测(2026-2032)DMT-dG亚磷酰胺市场按纯度等级、合成规模、技术、应用和最终用户划分,全球预测,2026-2032年亚磷酰胺市场按应用、类型、最终用户和形态划分 - 全球预测 2025-2032 亚磷酰胺市场:产业趋势及2035年全球预测 - 依亚磷酰胺类型、合成寡核苷酸类型、应用领域、治疗领域及地区划分

亚磷酰胺市场:产业趋势及2035年全球预测 - 依亚磷酰胺类型、合成寡核苷酸类型、应用领域、治疗领域及地区划分 亚磷酰胺市场-全球产业规模、份额、趋势、机会和预测,按类型、应用、地区和竞争细分,2020-2030 年

亚磷酰胺市场-全球产业规模、份额、趋势、机会和预测,按类型、应用、地区和竞争细分,2020-2030 年 亚磷酰胺市场规模、份额和趋势分析报告:按类型、应用、最终用途、地区和细分市场预测,2025 年至 2033 年

亚磷酰胺市场规模、份额和趋势分析报告:按类型、应用、最终用途、地区和细分市场预测,2025 年至 2033 年 全球亚磷酰胺市场

全球亚磷酰胺市场 亚磷酰胺市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

亚磷酰胺市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测