|

市场调查报告书

商品编码

1906261

数位信任:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Digital Trust - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

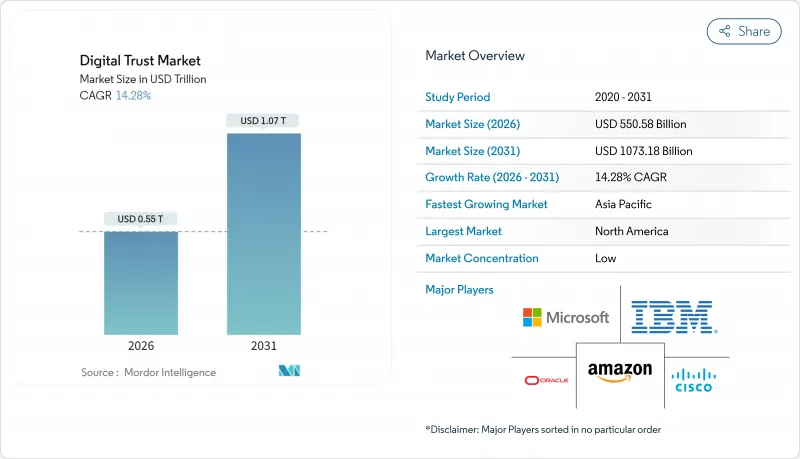

数位信任市场预计将从 2025 年的 4,817.9 亿美元成长到 2026 年的 5,505.8 亿美元,预计到 2031 年将达到 10731.8 亿美元,2026 年至 2031 年的复合年增长率为 14.28%。

网路攻击日益频繁,资料外洩成本预计到2024年将平均达到488万美元,全球隐私法规也日趋严格,这些因素迫使企业优先考虑在身分、装置、应用程式和资料流等各个层面检验的信任机制。云端迁移、人工智慧驱动的威胁侦测以及零信任架构的采用正在加速相关支出,而可携式数位身分钱包和机器间信任要求则扩大了这一领域的机会。随着平台供应商透过收购和合作整合自身能力,打造能够降低客户营运复杂性的整合解决方案,竞争格局仍在不断变化。

全球数位信任市场趋势与洞察

资料外洩事件的发生频率和成本日益增加

网路犯罪日益猖獗,全球平均每11秒就会发生一起勒索软体攻击。医疗机构遭受的网路攻击平均每次损失高达1,093万美元,而金融机构每次损失则高达604万美元。已实施人工智慧驱动的安全防护和自动化技术的机构已将资料外洩成本降低了220万美元,这不仅体现了该技术的保护优势,也揭示了其风险因素。中小企业仍然十分脆弱,60%的企业在遭受严重网路攻击后的六个月内破产,而43%的网路攻击事件的目标正是它们。

全球范围内不断扩大隐私权保护和电子身分识别法规

到2025年,全球75%的人口将生活在现代资料隐私法律的保护之下。欧盟的eIDAS 2.0要求所有成员国在2026年前实施数位身分钱包,并强制私部门在2027年12月前接受数位身分钱包。美国、欧盟和亚太地区(APAC)不同的框架正在增加跨国公司的遵循成本。随着行动优先策略在新兴经济体的普及,预计到2024年,数位身分平台的用户数量将达到50亿。

消费者「同意疲劳」正在降低用户参与度。

儘管97%的消费者关注线上资料隐私,但只有8%的人完全信任品牌,一年内下降了2个百分点。 89%的使用者感到密码疲劳,54%的使用者会放弃需要繁琐登入流程的服务。简化的无密码流程可以在不牺牲安全性的前提下提高使用者满意度。

细分市场分析

到2025年,解决方案业务将占总收入的61.85%,这主要得益于身分验证平台、认证服务和诈欺侦测引擎的推动,这些产品和服务构成了数位信任基础的核心。然而,到2031年,託管服务和专业服务将以14.72%的复合年增长率成长,这反映出企业越来越依赖第三方在零信任设计、监管审核和加密敏捷转型方面的专业知识。人才短缺迫使企业将保全行动,导致与资安管理服务提供者 (MSSP) 的合作日益增加。此外,由于74%的安全漏洞仍与人为错误有关,因此对培训服务的需求也不断增长。

供应商整合计划推动了对服务的需求。整合专家确保企业在逐步淘汰冗余的即插即用工具的过程中,业务连续性和资料完整性。託管安全服务填补了中小企业的人才缺口,而大型企业则聘请顾问公司建造威胁情报融合中心。平台供应商将咨询服务打包出售,以促进用户采纳并降低解约率,从而增强基本客群留存率。

截至2025年,由于受监管产业将关键金钥和日誌保存在实体资料中心,本地部署仍将维持65.05%的市场份额。然而,随着超大规模资料中心业者资料中心将高阶威胁情报来源和弹性处理功能整合到其原生安全套件中,到2031年,云端解决方案的复合年增长率将达到15.96%。与仅采用本地部署的竞争对手相比,部署了云端控制措施的组织可节省222万美元的安全漏洞成本。

混合部署将成为主流,加密密集型工作负载仍保留在本地,而分析和策略引擎则迁移到SaaS平台。受满足资料居住要求的自主云端计画的推动,云端采用中的数位信任市场规模预计将以15.96%的复合年增长率成长。同时,工厂和零售店的边缘运算将需要在设备附近实施分散式信任,从而催生对轻量级、无代理架构的需求。

全球数位信任市场按组件(解决方案和服务)、部署模式(云端、本地部署)、企业规模(大型企业、中小企业)、终端用户行业(银行、金融服务和保险 (BFSI)、医疗保健等)以及地区进行细分。产业预测以美元计价,并包含成长趋势、分析等内容。

区域分析

北美地区将继续保持领先地位,预计到2025年将占据34.85%的收入份额,这主要得益于各州隐私法(2023年美国国会提出了超过350项相关法案)以及远超世界其他地区的企业预算。平均每次资料外洩造成的损失高达980万美元,凸显了采用人工智慧驱动的侦测技术和零信任架构的必要性。随着大型企业选择能够提供证书、身分和存取管理 (IAM) 以及符合统一服务等级协定 (SLA) 的持续合规性的平台供应商,供应商整合正在加速进行。

亚太地区是成长最快的区域,预计到2031年将以14.31%的复合年增长率成长,这主要得益于行动互联网的大规模应用和政府主导的电子识别项目。中国、日本和印度的製造业集群正在采用机器身分框架来保护工业4.0资产。印尼、菲律宾和越南对兼顾成本和快速部署的云端原生信任层的需求日益增长。该地区的多元化发展也要求采用在地化的生物识别解决方案和支援多种语言的风险分析。

欧洲正受惠于eIDAS 2.0,该法案旨在建立通用的数位身分基础,并力争2030年实现80%的公民钱包普及率。由于金融监管机构敦促加快密码学技术的应用,欧洲的后量子密码试验比其他地区更为先进。同时,与美国的资料传输限制提高了合规要求,欧盟内部的硬体安全模组(HSM)容量正成为信任服务供应商的竞争优势。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 资料外洩事件的发生频率和成本日益增加

- 全球范围内不断扩大的隐私和电子识别法规

- 快速采用云端技术推动零信任部署

- 利用人工智慧/机器学习进行诈欺检测正变得越来越必要。

- 可重复使用/可携式数位身分的出现

- 智慧工厂中机器间可靠度的必要性

- 市场限制

- 初始整合和授权成本

- 监管和标准化格局分散

- 消费者对同意机制的疲劳会导致参与度下降。

- 缺乏高品质的标註数据,这会影响人工智慧的可靠性和安全性。

- 供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 买方的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 对影响市场的宏观经济因素进行评估

第五章 市场规模与成长预测

- 按组件

- 解决方案

- 服务

- 透过部署模式

- 基于云端的

- 本地部署

- 按组织规模

- 大公司

- 中小企业

- 按最终用户行业划分

- 银行、金融服务和保险(BFSI)

- 卫生保健

- 资讯科技/通讯

- 政府和公共部门

- 零售与电子商务

- 能源与公共产业

- 其他行业

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 东南亚

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Microsoft

- IBM

- Cisco Systems

- Amazon Web Services(AWS)

- Oracle

- Thales

- Entrust

- DigiCert

- Symantec(Broadcom)

- Okta

- DocuSign

- Ping Identity

- OneTrust

- Trulioo

- Jumio

- Mitek Systems

- Onfido

- CyberArk

- Palo Alto Networks

- Sift

- White-Space and Unmet-Need Assessment

The digital trust market is expected to grow from USD 481.79 billion in 2025 to USD 550.58 billion in 2026 and is forecast to reach USD 1073.18 billion by 2031 at 14.28% CAGR over 2026-2031.

Heightened cyber-attack frequency, rising data-breach costs averaging USD 4.88 million in 2024, and stringent global privacy regulations are compelling enterprises to prioritize verifiable trust mechanisms across identities, devices, applications, and data flows. Cloud migration, AI-enabled threat detection, and Zero-Trust architecture adoption collectively accelerate spending, while portable digital identity wallets and machine-to-machine trust requirements enlarge the addressable opportunity. Competitive dynamics remain fluid as platform vendors consolidate capabilities through acquisitions and alliances, enabling integrated offerings that reduce operational complexity for customers.

Global Digital Trust Market Trends and Insights

Rising frequency and cost of data breaches

Cybercrime are growing significantly, and ransomware attacks occur every 11 seconds worldwide. Healthcare incidents average USD 10.93 million per breach, while financial institutions face USD 6.04 million per event. Organizations that deploy AI-driven security and automation shave USD 2.2 million off breach expenses, illustrating technology's dual protective and risk factors. SMEs remain vulnerable; 60% fail within six months of a serious cyberattack, yet 43% of incidents already target them.

Expanding global privacy and e-ID regulations

Seventy-five percent of the world's population will live under modern data-privacy laws by 2025. The European Union's eIDAS 2.0 mandates digital identity wallets for all member states by 2026 and compels private-sector acceptance by December 2027. Divergent frameworks across the US, EU, and APAC increase compliance expense for multinationals. Digital identity platform usage is expected to reach 5 billion people in 2024 as mobile-first schemes proliferate in emerging economies.

Consumer "consent fatigue" eroding engagement

Ninety-seven percent of consumers worry about online data privacy, yet just 8% fully trust brands - down two percentage points in a year. Password exhaustion affects 89% of users; 54% abandon services that require cumbersome log-ins. Streamlined, passwordless flows lift satisfaction without sacrificing security.

Other drivers and restraints analyzed in the detailed report include:

- Rapid cloud adoption triggering Zero-Trust roll-outs

- AI/ML-powered fraud detection becoming table-stakes

- Fragmented regulatory and standards landscape

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions retained 61.85% of 2025 revenue, anchored by identity verification platforms, certificates, and fraud-detection engines that form the core of digital trust infrastructure. Yet managed and professional services will grow 14.72% CAGR through 2031, reflecting organizations' reliance on third-party expertise for Zero-Trust design, regulatory audits, and crypto-agile transitions. Staffing shortages press enterprises to outsource security operations, pushing MSSP partnerships higher. Training services expand because 74% of breaches still involve human error.

Vendor-consolidation programs amplify services demand; as organizations retire overlapping point tools, integration specialists ensure continuity and data integrity. Among SMEs, managed security offsets talent scarcity, while large enterprises engage consultancies to orchestrate threat-intelligence fusion centers. Platform vendors bundle advisory packages to boost adoption and reduce churn, reinforcing stickiness across their customer base.

On-premises deployments preserved 65.05% share in 2025 as regulated verticals retain critical keys and logs in physical data centers. However, cloud options will log a 15.96% CAGR to 2031 as hyperscalers embed sophisticated threat-intel feeds and elastic processing into native security suites. Organizations implementing cloud controls report USD 2.22 million lower breach costs than purely on-prem rivals.

Hybrid patterns prevail; encryption-intensive workloads remain on-premises, while analytics and policy engines shift to SaaS. Digital trust market size for cloud deployments is projected to advance at 15.96% CAGR, catalyzed by sovereign-cloud initiatives that satisfy data-residency demands. Meanwhile, edge computing in factories and retail branches necessitates distributed trust enforcement close to devices, creating openings for lightweight agentless architectures.

Global Digital Trust Market is Segmented by Component (Solutions and Services), Deployment Mode (Cloud, On-Premises), Enterprise Size (Large Enterprises, Small and Medium-Sized Enterprises (SMEs)), End-User Industry (Banking, Financial Services and Insurance (BFSI), Healthcare, and More) and by Geography. The Industry Forecasts are Provided in Terms of Value (USD). Covers Growth Trends, Analysis and More.

Geography Analysis

North America led with 34.85% revenue share in 2025, strengthened by state privacy laws - more than 350 bills tabled in US legislatures during 2023 - alongside enterprise budgets that dwarf global peers. Average breach costs of USD 9.8 million justify strategic adoption of AI-powered detection and zero-trust blueprints. Vendor consolidation accelerates as large firms select platform providers able to bundle certificates, IAM, and continuous compliance under unified SLAs.

Asia-Pacific is the fastest-growing region at 14.31% CAGR through 2031, riding on mass-scale mobile internet usage and government-backed e-ID programs. Manufacturing corridors in China, Japan, and India deploy machine-identity frameworks to secure Industry 4.0 assets. Indonesia, the Philippines, and Vietnam drive demand for cloud-native trust layers that balance cost with rapid rollout. Variability across the region necessitates localized biometric solutions and language-aware risk analytics.

Europe benefits from eIDAS 2.0, which sets a common digital-identity baseline and targets 80% citizen-wallet adoption by 2030. Post-quantum cryptography pilots are more advanced here than in any other region, as financial watchdogs urge crypto-agile readiness. Meanwhile, data-transfer restrictions with the US add compliance layers, making on-EU-soil HSM capacity a competitive differentiator for trust-service providers.

- Microsoft

- IBM

- Cisco Systems

- Amazon Web Services (AWS)

- Oracle

- Thales

- Entrust

- DigiCert

- Symantec (Broadcom)

- Okta

- DocuSign

- Ping Identity

- OneTrust

- Trulioo

- Jumio

- Mitek Systems

- Onfido

- CyberArk

- Palo Alto Networks

- Sift

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising frequency and cost of data breaches

- 4.2.2 Expanding global privacy and e-ID regulations

- 4.2.3 Rapid cloud adoption triggering Zero-Trust roll-outs

- 4.2.4 AI/ML-powered fraud detection becoming table-stakes

- 4.2.5 Emergence of reusable / portable digital identitiesf

- 4.2.6 Machine-to-machine trust needs in smart factories

- 4.3 Market Restraints

- 4.3.1 Up-front integration and licensing costs

- 4.3.2 Fragmented regulatory and standards landscape

- 4.3.3 Consumer consent fatigue eroding engagement

- 4.3.4 Limited high-quality labelled data for Trust-and-Safety AI

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 Banking, Financial Services and Insurance (BFSI)

- 5.4.2 Healthcare

- 5.4.3 IT and Telecommunications

- 5.4.4 Government and Public Sector

- 5.4.5 Retail and E-Commerce

- 5.4.6 Energy and Utilities

- 5.4.7 Other Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Southeast Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Microsoft

- 6.4.2 IBM

- 6.4.3 Cisco Systems

- 6.4.4 Amazon Web Services (AWS)

- 6.4.5 Oracle

- 6.4.6 Thales

- 6.4.7 Entrust

- 6.4.8 DigiCert

- 6.4.9 Symantec (Broadcom)

- 6.4.10 Okta

- 6.4.11 DocuSign

- 6.4.12 Ping Identity

- 6.4.13 OneTrust

- 6.4.14 Trulioo

- 6.4.15 Jumio

- 6.4.16 Mitek Systems

- 6.4.17 Onfido

- 6.4.18 CyberArk

- 6.4.19 Palo Alto Networks

- 6.4.20 Sift

- 6.5 White-Space and Unmet-Need Assessment

全球数位信任市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析及预测(2026-2034)

全球数位信任市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析及预测(2026-2034) 数位信任服务市场:2026-2032年全球预测(依解决方案类型、部署模式、组织规模、服务模式和产业垂直领域划分)数位双胞胎城市解决方案市场:按组件、技术、部署模式、应用和最终用户划分-2026-2032年全球预测

数位信任服务市场:2026-2032年全球预测(依解决方案类型、部署模式、组织规模、服务模式和产业垂直领域划分)数位双胞胎城市解决方案市场:按组件、技术、部署模式、应用和最终用户划分-2026-2032年全球预测 数位信任市场规模、份额和成长分析(按解决方案、身份验证类型、部署类型、企业规模、最终用户和地区划分)—产业预测(2026-2033 年)

数位信任市场规模、份额和成长分析(按解决方案、身份验证类型、部署类型、企业规模、最终用户和地区划分)—产业预测(2026-2033 年) 数位信任市场规模、份额和趋势分析报告:按组件、技术、公司规模、最终用途、地区和细分市场预测,2025 年至 2033 年

数位信任市场规模、份额和趋势分析报告:按组件、技术、公司规模、最终用途、地区和细分市场预测,2025 年至 2033 年 数位信任市场按最终用途产业、解决方案类型、部署模型、组织规模、数位 ID 类型和地区划分

数位信任市场按最终用途产业、解决方案类型、部署模型、组织规模、数位 ID 类型和地区划分 全球数位信託市场 2024-2031

全球数位信託市场 2024-2031