|

市场调查报告书

商品编码

1906280

硬木:市场份额分析、行业趋势和统计数据、成长预测(2026-2031)Hardwood - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

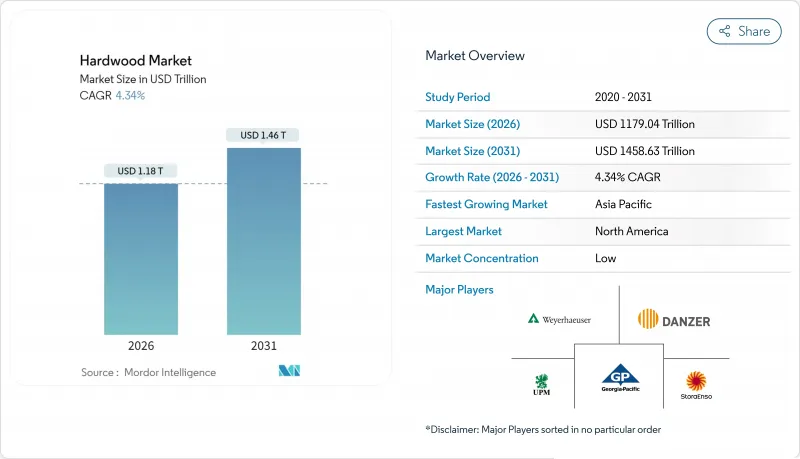

2025年硬木市场价值11300亿美元,预计到2031年将达到14586.3亿美元,而2026年为11790.4亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 4.34%。

成长的驱动力来自日益完善的永续性法规,例如欧盟的《森林砍伐条例》(EUDR),以及建筑、地板材料和高端家具等终端用户强劲的需求。市场领导正投资于垂直整合的供应链,以降低原材料采购风险;与此同时,全球范围内对非法伐木的打击力度加大,推高了合规成本,并进一步推高了认证木材的溢价。亚太地区的成长速度得益于持续的都市化和不断壮大的中产阶级消费群体,这与北美和欧洲虽然增长速度稍慢但仍然庞大的消费群体形成鲜明对比。在供应方面,锯木厂自动化带来的效率提升、数位化可追溯性的广泛应用以及美国旨在加速国内伐木的政策倡议,都预示着一个以生产力为导向、纪律主导的增长时代的到来。

全球硬木市场趋势与洞察

全球绿色建筑计划对经认证的永续硬木木材的需求不断增长

截至2025年,约有2.8亿公顷森林将获得PEFC(森林认证系统核准计画)或FSC(森林管理委员会)认证,第三方认证将从一种市场增值因素转变为进入要求。将于2024年12月生效的欧盟毁林法规(EUDR)将要求出口商提供每批货物的地理位置信息,迫使供应商在其分散的运营中建立数字化可追溯性。为此,FSC推出了专门的「监管模组」以减轻合规负担。认证溢价正在欧洲以外地区扩展,东亚和东南亚的进口商越来越多地要求提供检验的原产地证明,以确保下游产品能够进入经济合作暨发展组织(OECD)市场。必维国际检验集团(Bureau Veritas)观察到,将FSC、PEFC和合法性检查整合到一次现场审核中的多体系审核显着增加,从而降低了重复合规成本。

全球中产阶级在高檔木製家具上的支出正在上升

亚太地区收入的成长重新运作了对实木家具的需求,但短期销售额与住宅交易趋势同步波动。威廉布莱尔的分析显示,二手住宅交易与家具销售之间存在很强的相关性,这解释了为何儘管长期基础良好,但销售量却较为缓慢。较高的运费和通货紧缩的价格趋势持续挤压利润空间,但人口结构的利多因素,例如在家工作环境的改善,支撑着4%至6%的稳定成长。 2024年初,美国对印度的硬木出口额达287万美元,其中以白橡木、山胡桃木和红橡木为主。这显示印度的进口基础薄弱,但对优质硬木树种的需求却被压抑已久。

由于国际反非法伐木法规(欧盟非法伐木法规、莱西法案)的加强,导致供应不稳定。

包括欧盟《森林砍伐条例》和美国《莱西法案》在内的严格法规要求对所有跨境硬木运输进行全程追踪,这增加了每笔交易的文件编制和检验负担。这种额外的审查增加了进出口商的成本,并已导致一些买家减少从难以证明合法采伐的地区订购木材。儘管欧盟委员会2025年4月发布的指导意见允许进行年度实质审查报告,但仍要求提交每批货物的地理数据,这增加了货源多元化供应商的固定成本。

细分市场分析

橡木将占据硬木市场最大份额,到2025年将占消费量的27.74%。宾州和密苏里州的立木价格报告显示,白橡木单板的价格上限显着提高,但混合锯材的平均价格稳定在每千板英尺约260美元,凸显了不同等级木材之间价格差异的扩大。胡桃木在高端家具和吸音板应用的推动下,预计将获得显着的市场份额,年复合成长率将达到5.71%,超过整体硬木市场的成长速度。由于受到《濒危野生动植物种国际贸易公约》(CITES)的管制,红木的产能持续受限,而樱桃木的市场成长则随着其流行週期的消退而趋于平缓。鹅掌楸和山毛榉等次要树种由于认证溢价而在特定计划规格中得到应用,但其规模尚未达到橡木和胡桃木的水平。拥有多元化树种组合的综合性公司可以利用区域价格差异来平滑收入,并对冲气候变迁导致的树种分布变化风险。

随着消费者选择树种时不仅考虑其美观性,也更加重视透明度,可追溯的价值链变得日益重要。这种良性循环使投资于森林管理委员会 (FSC) 和森林认证促进计划 (PEFC)审核的森林所有者受益,维持的价格差异足以抵消审核和产销监管链 (CoC) 的成本。

区域分析

北美地区占2025年销售额的36.55%,这得益于其丰富的森林资源、成熟的基础设施以及有利于认证林业的法规环境。美国2025年3月发布的《扩大伐木行政命令》旨在加强野火预防措施并减少对进口的依赖。然而,锯木厂的关闭,例如Canfor公司位于南卡罗来纳州的工厂关闭(导致产能减少3.5亿板英尺),凸显了市场週期可能超越政策预期。加拿大作为美国主要供应商的地位仍然至关重要。潜在的反补贴税可能会重塑跨境贸易格局,并影响中西部和东北部地区的计划经济效益。墨西哥正利用美墨加协定(USMCA)提供的免税准入,但其加工规模不足限制了其对美国边境附近区域家具产业丛集的贡献。

亚太走廊预计将以5.42%的复合年增长率成长,并成为硬木市场的重要成长引擎。 2024年,中国将进口998万立方公尺硬木原木,平均价格为每立方公尺277美元,儘管整体建设活动低迷,但中国仍将转向进口优质树种。印度的硬木市场仍具有巨大的成长潜力,美国木材仅占其构成比的5%。一旦物流和关税摩擦得到缓解,预计树种多样化将带来显着的成长潜力。东南亚出口国,尤其是越南,正在满足全球家具订单,但印尼的胶合板市场却面临需求下降的困境,凸显了该地区内部业绩的差异。

在欧洲,由于认证标准的实施,需求保持稳定。同时,欧盟木材法规(EUDR)正在重组供应链,有利于那些拥有良好管理记录的本土和北欧生产商。德国软木进口量大幅下降(预计2024年将下降34%),预示着结构性替代趋势的转变,这一趋势可能会蔓延至硬木市场。在中东和非洲,由于大型国家计划的推进,预计需求将会成长,但物流不稳定和窑炉产能有限限制了硬木市场短期内的扩张。然而,随着区域标准的推进,碳正建筑材料的发展前景仍然乐观。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 全球绿色建筑计划对经认证的永续硬木木材的需求不断增长

- 全球中产阶级在高级硬木家具上的支出不断增长

- 硬木单板工程木材製造的成长

- 全球住宅维修中实木地板的使用率不断上升

- 透过收割和锯木的技术创新来提高产量和供应效率

- 市场限制

- 由于加强了对非法采伐的国际法规(欧盟非法采伐条例、莱西法案),导致供应波动。

- 全球市场中来自更便宜的软木和复合材料替代品的价格压力

- 贸易中断和关税不确定性对硬木出口流量的影响

- 产业价值链分析

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 洞察市场最新趋势与创新

- 深入了解市场近期发展动态(新产品发表、策略性倡议、投资、合作、合资、扩张、併购等)

第五章 市场规模与成长预测

- 按物种

- 橡木

- 枫

- 樱桃

- 核桃

- 桃花心木

- 其他的

- 透过使用

- 地板材料

- 家具

- 建造

- 室内设计与装饰

- 工业包装和托盘

- 木製品

- 其他用途

- 透过分销管道

- 直销

- 分销商/批发商

- 零售(线下和线上)

- 其他分销管道

- 按地区

- 北美洲

- 加拿大

- 美国

- 墨西哥

- 南美洲

- 巴西

- 秘鲁

- 智利

- 阿根廷

- 其他南美洲

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 比荷卢经济联盟(比利时、荷兰、卢森堡)

- 北欧国家(丹麦、芬兰、冰岛、挪威、瑞典)

- 其他欧洲地区

- 亚太地区

- 印度

- 中国

- 日本

- 澳洲

- 韩国

- 东南亚(新加坡、马来西亚、泰国、印尼、越南、菲律宾)

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Weyerhaeuser Company

- Georgia-Pacific LLC

- Danzer Group

- Baillie Lumber Co.

- Stora Enso Oyj

- UPM-Kymmene Oyj

- Mohawk Industries, Inc.

- Armstrong Flooring, Inc.

- Rougier Afrique International

- Samling Group

- Greenply Industries Ltd.

- Arauco

- Sumitomo Forestry Co., Ltd.

- Dongwha International

- Columbia Forest Products

- Century Plyboards Ltd.

- Norbord Inc.

- Kronospan Limited

- Mannington Mills, Inc.

- Roseburg Forest Products

- Holzindustrie Schweighofer(HS Timber Group)

- Stella-Jones Inc.

第七章 市场机会与未来展望

The Hardwood Market was valued at USD 1130 billion in 2025 and estimated to grow from USD 1179.04 billion in 2026 to reach USD 1458.63 billion by 2031, at a CAGR of 4.34% during the forecast period (2026-2031).

Growth is underpinned by tightening sustainability regulations-most notably the European Union Deforestation Regulation (EUDR)-and by resilient end-use demand in construction, flooring, and high-end furniture. Market leaders are funding vertically integrated supply chains to de-risk raw-material availability, while tighter global enforcement against illegal logging is raising compliance costs yet reinforcing the premium for certified wood. Asia-Pacific's pace, buoyed by ongoing urbanization and rising middle-class spending, balances the cooler but still sizable consumption base in North America and Europe. On the supply side, efficiency-boosting sawmill automation, wider deployment of digital traceability, and U.S. policy moves to accelerate domestic harvesting all point to an era of disciplined, productivity-led growth.

Global Hardwood Market Trends and Insights

Rising Demand for Certified Sustainable Hardwood in Global Green Building Projects

Roughly 280 million hectares of forests carried either PEFC (Programme for the Endorsement of Forest Certification systems) or Forest Stewardship Council (FSC) certification in 2025, turning third-party validation into an entry requirement rather than a marketing add-on . The EU Deforestation Regulation (EUDR), effective December 2024, forces exporters to present geolocation data for every shipment, pushing suppliers to retrofit digital traceability across fragmented operations. FSC reacted with a dedicated "Regulatory Module" to ease compliance . The certification premium is migrating beyond Europe, as importers in East and South-East Asia increasingly ask for verified provenance to protect their downstream access to Organisation for Economic Co-operation and Development (OECD) markets. Bureau Veritas confirms a marked rise in multi-scheme audits that bundle FSC, PEFC, and legality checks into one field mission, thereby trimming compliance overlap costs.

Expanding Middle-Class Expenditure on Premium Hardwood Furniture Worldwide

Income gains across Asia-Pacific have reset aspirations toward solid-wood furniture, yet short-term sales fluctuate with housing turnover. An assessment by William Blair shows a tight correlation between existing-home transactions and furniture receipts, explaining subdued volumes despite intact long-term fundamentals. Freight rates and deflationary price trends continue to squeeze margins, though demographic tailwinds-such as remote-work configurations that elevate home-office quality-anchor a 4%-6% steady-state growth band. Early-2024 U.S. hardwood exports to India reached USD 2.87 million, led by white oak, hickory, and red oak, underscoring the gap between India's low import base and its latent appetite for premium hardwood species.

Supply Volatility Due to Stricter International Anti-Illegal Logging Regulations (EUDR, Lacey Act)

Stringent rules, including the EU Deforestation Regulation and the U.S. Lacey Act, now demand end-to-end tracking for every load of hardwood that crosses a border, adding layers of paperwork and verification to each transaction. The extra scrutiny raises costs for importers and exporters alike and has already pushed some buyers to scale back orders from regions where proving a legal harvest is difficult. The European Commission's April 2025 guidance allows annual due diligence filings but still demands shipment-level geodata, raising fixed costs for suppliers handling diverse sourcing pools.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Engineered Wood Manufacturing Utilizing Hardwood Veneers

- Increasing Adoption of Hardwood Flooring in Residential Renovations Globally

- Price Pressure from Cheaper Softwood and Composite Substitutes in Global Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Oak controlled 27.74% of 2025 consumption, giving it the single-largest slice of the hardwood market. Pennsylvania and Missouri stumpage reports reveal impressive ceiling prices for white oak veneer, yet mixed sawlog averages settled near USD 260 per thousand board feet, spotlighting widening value bands across grades. Walnut, propelled by luxury furniture and acoustic-panel applications, is set to capture an outsized wallet share as its 5.71% CAGR outstrips overall hardwood market growth. Mahogany remains capacity-constrained under CITES (Convention on International Trade in Endangered Species) listing, while cherry treaded water after fashion cycles cooled. Secondary species, including tulipwood and beech, ride certification premiums into niche project specifications but lack the scale of oak or walnut. Diversified species portfolios allow integrated firms to exploit regional price differentials, smoothing earnings and hedging against climate-induced shifts in species distribution.

Consumers increasingly choose species not only for aesthetics but also for transparency credentials, amplifying the strategic value of traceable supply chains. That virtuous loop rewards forest owners investing in Forest Stewardship Council or Programme for the Endorsement of Forest Certification audits, sustaining a price delta that compensates for audit and chain-of-custody costs.

The Hardwood Market is Segmented by Species (Oak, Maple, and More), Application (Flooring, Furniture, and More), Distribution Channel (Direct Sales, Distributors/Wholesalers, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 36.55% of 2025 turnover thanks to expansive forest inventories, mature infrastructure, and a regulatory environment conducive to certified forestry. The March 2025 U.S. executive order to expand harvesting aims to fortify wildfire mitigation and reduce import reliance, although sawmill closures such as Canfor's South Carolina operations-which will remove 350 million board feet of capacity-underscore how market cycles can still override policy intent. Canada's role as a top U.S. supplier remains pivotal; potential countervailing duties could reshape cross-border trade flows and influence project economics across the Midwest and Northeast. Mexico leverages USMCA tariff-free access but lacks processing scale, limiting its upside to regional furniture clusters near the U.S. border.

The Asia-Pacific corridor, growing at 5.42% CAGR, is the hardwood market's chief momentum engine. China imported 9.98 million m3 of hardwood logs in 2024 at an average USD 277 per m3, pivoting toward premium species despite overall tepid construction activity. India's hardwood market remains under-indexed; U.S. lumber constitutes just 5% of its import mix, leaving significant runway for species diversification once logistics and tariff frictions ease. Southeast Asian exporters-Vietnam, particularly-are filling global furniture orders, yet Indonesia's plywood segment wrestles with demand slumps, pointing to heterogeneous performance across the region.

Europe delivers stable, certification-led demand but is rewriting supply chains through the EUDR filter, effectively favoring domestic and Nordic producers with robust chain-of-custody records. Germany's softwood import collapse (-34% in 2024) hints at structural substitution into engineered products, likely to spill over into hardwood patterns. The Middle East and Africa pool gains from sovereign mega-projects; however, volatile logistics and limited kiln-dry capacity restrict near-term hardwood roll-outs, while long-term visibility remains promising as local standards embrace carbon-positive building materials.

- Weyerhaeuser Company

- Georgia-Pacific LLC

- Danzer Group

- Baillie Lumber Co.

- Stora Enso Oyj

- UPM-Kymmene Oyj

- Mohawk Industries, Inc.

- Armstrong Flooring, Inc.

- Rougier Afrique International

- Samling Group

- Greenply Industries Ltd.

- Arauco

- Sumitomo Forestry Co., Ltd.

- Dongwha International

- Columbia Forest Products

- Century Plyboards Ltd.

- Norbord Inc.

- Kronospan Limited

- Mannington Mills, Inc.

- Roseburg Forest Products

- Holzindustrie Schweighofer (HS Timber Group)

- Stella-Jones Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Certified Sustainable Hardwood in Global Green Building Projects

- 4.2.2 Expanding Middle-Class Expenditure on Premium Hardwood Furniture Worldwide

- 4.2.3 Growth of Engineered Wood Manufacturing Utilizing Hardwood Veneers

- 4.2.4 Increasing Adoption of Hardwood Flooring in Residential Renovations Globally

- 4.2.5 Technological Advancements in Harvesting & Sawmilling Enhancing Yield and Supply Efficiency

- 4.3 Market Restraints

- 4.3.1 Supply Volatility Due to Stricter International Anti-Illegal Logging Regulations (EUDR, Lacey Act)

- 4.3.2 Price Pressure from Cheaper Softwood and Composite Substitutes in Global Markets

- 4.3.3 Trade Disruptions and Tariff Uncertainties Impacting Hardwood Export Flows

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Species

- 5.1.1 Oak

- 5.1.2 Maple

- 5.1.3 Cherry

- 5.1.4 Walnut

- 5.1.5 Mahogany

- 5.1.6 Others

- 5.2 By Application

- 5.2.1 Flooring

- 5.2.2 Furniture

- 5.2.3 Construction

- 5.2.4 Interior Design & Decoration

- 5.2.5 Industrial Packaging & Pallets

- 5.2.6 Millwork

- 5.2.7 Other Applications

- 5.3 By Distribution Channel

- 5.3.1 Direct Sales

- 5.3.2 Distributors/Wholesalers

- 5.3.3 Retailers (offline and online)

- 5.3.4 Other Distribution Channels

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 Canada

- 5.4.1.2 United States

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 India

- 5.4.4.2 China

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East And Africa

- 5.4.5.1 United Arab of Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East And Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Weyerhaeuser Company

- 6.4.2 Georgia-Pacific LLC

- 6.4.3 Danzer Group

- 6.4.4 Baillie Lumber Co.

- 6.4.5 Stora Enso Oyj

- 6.4.6 UPM-Kymmene Oyj

- 6.4.7 Mohawk Industries, Inc.

- 6.4.8 Armstrong Flooring, Inc.

- 6.4.9 Rougier Afrique International

- 6.4.10 Samling Group

- 6.4.11 Greenply Industries Ltd.

- 6.4.12 Arauco

- 6.4.13 Sumitomo Forestry Co., Ltd.

- 6.4.14 Dongwha International

- 6.4.15 Columbia Forest Products

- 6.4.16 Century Plyboards Ltd.

- 6.4.17 Norbord Inc.

- 6.4.18 Kronospan Limited

- 6.4.19 Mannington Mills, Inc.

- 6.4.20 Roseburg Forest Products

- 6.4.21 Holzindustrie Schweighofer (HS Timber Group)

- 6.4.22 Stella-Jones Inc.

7 Market Opportunities & Future Outlook

- 7.1 Demand for Sustainable and Certified Hardwood

- 7.1.1 Custom and Modular Furniture Trends

2025-2029年全球硬木市场

2025-2029年全球硬木市场 全球硬木市场

全球硬木市场 硬木市场-全球产业规模、份额、趋势、机会及预测,按类型(白蜡木、樱桃木、枫木、橡木、桦木)、按应用(地板、家具、其他)、按地区、按竞争细分,2020-2030 年预测

硬木市场-全球产业规模、份额、趋势、机会及预测,按类型(白蜡木、樱桃木、枫木、橡木、桦木)、按应用(地板、家具、其他)、按地区、按竞争细分,2020-2030 年预测