|

市场调查报告书

商品编码

1906884

生物农药:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Biopesticides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

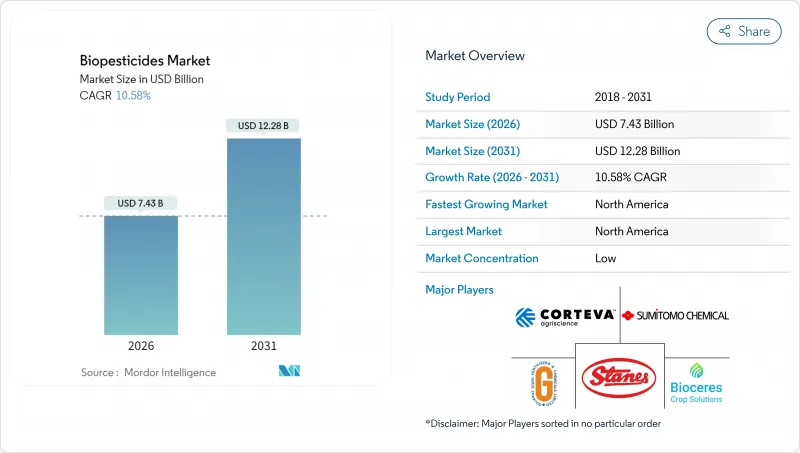

预计到 2026 年,生物农药市值将达到 74.3 亿美元,高于 2025 年的 67.2 亿美元,预计到 2031 年将达到 122.8 亿美元。

预计2026年至2031年年复合成长率(CAGR)为10.58%。

合成化学品监管力度的加大、有机农地的快速扩张以及发酵服务平台的兴起,正在加速微生物解决方案的商业化进程。巴西的《生物投入品协调法》将于2024年12月生效,该法将缩短生物产品的核准时间,其他新兴市场也开始效法。同时,北美种植者凭藉其成熟的受控环境农业基础设施以及在改革后的美国协调框架(USCF)下简化的审批流程,引领全球微生物解决方案的普及。杀虫剂抗药性的日益增强,尤其是在鳞翅目害虫中,正促使田间作物种植者和园艺种植者转向生物防治方法,以补充现有的化学农药。

全球生物农药市场趋势与洞察

加强全球对合成农药的监管

欧盟的「从农场到餐桌」策略旨在2030年将化学农药的使用量减少50%,这将显着促进生物农药的替代。同时,美国环保署(EPA)于2024年取消了多种有机磷农药的註册,提高了87%受访农户对生物农药的兴趣。巴西简化的生物农药核准流程显着缩短了审批时间,远低于合成农药,使生物农药生产商在避免延误方面具有成本效益优势。泰国和其他东南亚国家也在製定类似政策,这标誌着全球监管正在向更严格的方向转变。主要出口作物的残留限量合规性带来了切实的商业风险,买家正在敦促供应商减少对合成化学品的依赖。

扩大有机面积

受主要产区年增长率趋于稳定的推动,经认证的有机农地面积正在稳步增长。由于有机认证禁止使用合成投入品,生物农药已成为这些系统中主要的病虫害防治工具,为生物农药供应商创造了稳定的收入基础。有机产品的高零售价格使生产者能够在保持盈利的同时,有效控制每公顷的处理成本。有机供应链中可控环境农业(CEA)的扩张进一步推动了需求,因为室内农场从一开始就采用生物防治,以满足零残留品牌的要求。此外,对区域有机研究中心的投资也更支持了生物产品的推广,增强了人们对生物产品的信心。

与合成农药的成本比较

生物农药的每公顷处理成本仍然是传统产品的两到三倍,这主要是由于其活性成分浓度较低且施用週期更频繁。非洲和亚洲部分地区的商品作物种植者往往不愿意投资昂贵的投入品,即使高价出口管道可以涵盖这些成本。将降低抗性管理和残留检测成本纳入考虑的经济模型可以部分抵消价格差异,但此类分析尚未透过推广网络广泛传播。一些政府目前提供直接投入补贴以弥补价格差距,但补贴覆盖范围仍有限。

细分市场分析

生物杀菌剂仍将是生物农药市场的核心组成部分,预计到2025年将占总收入的46.92%。这反映了芽孢桿菌和木霉菌株在谷物、果树和保护地蔬菜中经过实践验证的优异性能。可湿性粉剂和油性分散剂的配方创新提高了产品的货架稳定性,从而促进了其在温暖气候地区的广泛应用。该领域的广泛效用增强了经销商的信心,并促使其在零售通路中占据更大的货架空间。儘管生物杀虫剂目前的市场份额落后,但预计将以11.86%的复合年增长率增长,超过其他类别。随着种植者寻求新的防治鳞翅目害虫抗药性的方法,生物杀虫剂的应用正在不断增加。近期监管文件显示,2024年生物农药的应用量将增加35%,这意味着在预测期内将有更多选择。

第二代生物除草剂目前仍属于小众市场,但随着企业将新型创业投资分离株与助剂结合以增强宿主特异性,其商业性发展动能日益强劲。儘管受面积限制,产量仍然小规模,但它们为抗除草剂杂草提供了差异化的解决方案,吸引了风险投资的关注。其他生物农药(如杀线虫剂和杀软体动物剂)则针对高价值的特种作物,在这些作物上,持续的产量足以抵消较高的投入成本。总而言之,这些多样化的生物农药形式代表着生物农药市场技术范围的持续扩展。

《生物农药市场报告》依形态(生物杀菌剂、生物除草剂、生物杀虫剂等)、作物类型(经济作物、园艺作物等)及地区(非洲、亚太地区、欧洲、中东、北美等)细分。市场预测以价值(美元)和数量(公吨)为单位。

区域分析

复合年增长率(CAGR)指的是年均复合成长率,北美地区为12.05%。至2025年,北美地区将维持39.12%的收入份额,成为各地区中复合年增长率最高的地区。这巩固了北美地区作为生物农药市场规模最大且成长最快的地区的双重地位。美国环保署(EPA)审查流程的简化、各州层级的激励计画以及零售商对零残留采购的坚定承诺,都在加速生物农药的普及应用。美国受控环境农业(CEA)业务正在将生物农药应用于绿叶蔬菜、番茄和草莓等作物,从而提供了稳定的需求基础。加拿大有机农地的扩张以及墨西哥以出口为导向的园艺产业的发展,也进一步推动了北美地区生物农药的普及应用。

在欧盟「从农场到餐桌」战略的推动下,欧洲也跟进。欧洲生物防治市场成长显着,如今已占据作物保护产品销售总额的相当大一部分。严格的核准流程耗时数年,虽然延缓了产品更新,但却确保了高品质的资料包,并增强了种植者的信心。北部成员国高度重视减少谷物中的农药残留,而地中海地区则在园艺和葡萄栽培中广泛应用生物防治剂。

南美洲正经历最强劲的成长,这主要得益于巴西市场的扩张以及生物材料核准的协调统一等有利的监管改革。许多巴西生产商目前已将生物製品作为常规用途,推动市场年增率远高于全球平均水准。阿根廷的等效性核准和智利的公共研究经费进一步推动了该地区的成长动能。亚太地区展现出巨大的潜力,这得益于有机农地的扩张和政府永续性政策的推动,但由于监管时间表不一和技术应用有限,进展较为分散。中东和非洲是尚处于起步阶段的市场,捐助者资助的计画和多国示范计画正为未来的需求播下种子。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

- 调查方法

第二章 报告

第三章执行摘要和主要发现

第四章:主要产业趋势

- 有机耕作面积

- 人均有机产品支出

- 法律规范

- 阿根廷

- 澳洲

- 巴西

- 加拿大

- 中国

- 埃及

- 法国

- 德国

- 印度

- 印尼

- 伊朗

- 义大利

- 日本

- 墨西哥

- 荷兰

- 奈及利亚

- 菲律宾

- 俄罗斯

- 南非

- 西班牙

- 泰国

- 土耳其

- 英国

- 美国

- 越南

- 价值炼和通路分析

- 市场驱动因素

- 加强全球对合成农药的监管

- 扩大有机农业面积

- 对传统化学农药的抗药性日益增强

- 政府对生物农药的诱因与快速核准制度

- 可控制环境农业(CEA)的发展

- 降低发酵即服务规模化生产的门槛

- 市场限制

- 与合成农药相比,高成本

- 保存期限短,高度依赖低温运输

- 微生物生产中原物料价格的波动

- 缺乏统一的现场绩效KPI

第五章 市场规模和成长预测(价值和数量)

- 按形式

- 生物杀菌剂

- 生物除草剂

- 生物农药

- 其他生物农药

- 按作物类型

- 经济作物

- 园艺作物

- 田间作物

- 按地区

- 非洲

- 按国家/地区

- 埃及

- 奈及利亚

- 南非

- 其他非洲地区

- 按国家/地区

- 亚太地区

- 按国家/地区

- 澳洲

- 中国

- 印度

- 印尼

- 日本

- 菲律宾

- 泰国

- 越南

- 亚太其他地区

- 按国家/地区

- 欧洲

- 按国家/地区

- 法国

- 德国

- 义大利

- 荷兰

- 俄罗斯

- 西班牙

- 土耳其

- 英国

- 其他欧洲地区

- 按国家/地区

- 中东

- 按国家/地区

- 伊朗

- 沙乌地阿拉伯

- 其他中东地区

- 按国家/地区

- 北美洲

- 按国家/地区

- 加拿大

- 墨西哥

- 美国

- 北美其他地区

- 按国家/地区

- 南美洲

- 按国家/地区

- 阿根廷

- 巴西

- 南美洲其他地区

- 按国家/地区

- 非洲

第六章 竞争情势

- 关键策略倡议

- 市占率分析

- 公司简介

- 公司简介

- Bayer AG

- BASF SE

- Syngenta Group

- Corteva Agriscience

- FMC Corporation

- Valent BioSciences LLC(Sumitomo Chemical Co., Ltd.)

- Certis USA LLC(Mitsui and Co., Ltd.)

- Koppert BV

- Andermatt Group AG

- Marrone Bio Innovations Inc.(Bioceres Crop Solutions Corp.)

- Seipasa SA

- T.Stanes and Company Limited

- UPL Ltd.

- Atlantica Agricola

- Gujarat State Fertilizers and Chemicals Ltd.

第七章:CEO们需要思考的关键策略问题

The biopesticides market size in 2026 is estimated at USD 7.43 billion, growing from 2025 value of USD 6.72 billion with 2031 projections showing USD 12.28 billion, growing at 10.58% CAGR over 2026-2031.

Heightened regulatory scrutiny of synthetic chemistries, rapid expansion of organic farmland, and the emergence of fermentation-as-a-service platforms are converging to accelerate the commercialization of microbial-based solutions. Brazil's unified bioinputs law, effective December 2024, has already shortened approval timelines for biological products, providing momentum that other emerging markets are beginning to emulate. At the same time, North American growers lead global adoption because of a mature controlled-environment agriculture infrastructure and streamlined reviews under the reformed United States Coordinated Framework. Intensifying insecticide resistance, especially in lepidopteran pests, is steering both row-crop and horticultural producers toward biological modes of action that complement existing chemistries.

Global Biopesticides Market Trends and Insights

Stricter Global Curbs on Synthetic Pesticides

The European Union's Farm to Fork Strategy targets a 50% cut in chemical pesticide use by 2030, prompting a measurable substitution effect in favor of biologicals. Complementing this, the United States Environmental Protection Agency (EPA) cancelled several organophosphate registrations in 2024, which has increased biological awareness among 87% of surveyed row-crop growers. Brazil's streamlined approval process now takes significantly less time for biologicals compared to synthetics, creating a cost-of-delay advantage for biopesticide manufacturers. Thailand and other Southeast Asian nations are drafting comparable policies, illustrating the global reach of regulatory momentum. Across major export crops, residue-limit compliance has become a tangible business risk, so buyers are pressuring suppliers to reduce dependence on synthetic chemistries.

Expansion of Organic Farming Acreage

Certified organic farmland has been steadily increasing, supported by consistent annual growth across major producing regions. Since organic certification prohibits synthetic inputs, biologicals serve as the primary pest-management option in these systems, creating a reliable revenue base for biopesticide vendors. The premium retail pricing associated with organic products allows growers to manage higher per-hectare treatment costs while maintaining profitability. The expansion of controlled-environment agriculture (CEA) within organic supply chains further drives demand, as indoor farms adopt biological controls from the outset to meet residue-free branding requirements. Additionally, investment in regional organic research centers is enhancing extension support for biological products, boosting adoption confidence.

Higher Cost Versus Synthetic Pesticides

Per-hectare treatment costs for biologicals remain two to three times higher than conventional products, primarily because of lower active-ingredient density and more frequent application cycles. Commodity crop growers in Africa and parts of Asia hesitate to invest in premium inputs, even though premium export channels may cover those costs. Economic modeling that factors in resistance management and residue-testing savings can partially offset price gaps, but such analyses are not yet widely distributed through extension networks. Several governments now offer direct input subsidies to bridge the pricing differential, but program scope is still limited.

Other drivers and restraints analyzed in the detailed report include:

- Rising Resistance to Conventional Chemistries

- Government Biopesticide Incentives and Fast-Track Approvals

- Shorter Shelf Life and Cold-Chain Dependence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Biofungicides generated 46.92% of 2025 revenue and continue to anchor the biopesticides market size, reflecting proven field performance of Bacillus and Trichoderma strains across cereals, fruits, and protected vegetables. Innovation in wettable-powder and oil-dispersion formulations has improved shelf stability, which supports penetration in warmer climates. The segment's broad utility has built distributor confidence, encouraging wider shelf allocation in retail channels. Bioinsecticides trail in current share but are forecast to advance at a 11.86% CAGR, outpacing other categories. Adoption is rising as growers seek new modes of action to counter lepidopteran resistance. Recent regulatory submissions show a 35% rise in bioinsecticide dossiers in 2024, supplying a pipeline that will expand choices over the forecast window.

Second-generation bioherbicides remain niche but show commercial momentum as companies pair novel microbial isolates with adjuvants that improve host specificity. While limited acreage uptake keeps volume small, the category attracts venture capital because it offers a differentiated solution to herbicide-resistant weeds. Other biopesticides, including nematicides and molluscicides, target high-value specialty crops where yield preservation justifies higher inputs. Together, these diverse forms demonstrate the expanding technical scope of the biopesticides market.

The Biopesticides Market Report is Segmented by Form (Biofungicides, Bioherbicides, Bioinsecticides, and More), Crop Type (Cash Crops, Horticultural Crops, and More), and Geography (Africa, Asia-Pacific, Europe, Middle East, North America, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Geography Analysis

North America retained 39.12% revenue in 2025 and posted the fastest regional CAGR at 12.05%, underscoring its dual status as both the largest and fastest-growing territory for the biopesticides market. Streamlined EPA reviews, state-level incentive programs, and strong retailer commitments to residue-free sourcing combine to accelerate uptake. United States CEA operations integrate biological pest control in leafy greens, tomatoes, and strawberries, providing a steady baseline of demand. Canada's organic acreage expansion and Mexico's export-oriented horticulture further expand regional use.

Europe follows closely, propelled by the European Union's Farm to Fork Strategy. The European biocontrol market has grown significantly, representing a notable portion of total crop-protection sales. Stringent approval processes extend over several years, slowing product turnover but ensuring high-quality data packages that bolster grower trust. Northern member states emphasize residue reduction in cereals, while Mediterranean regions employ biologicals heavily in horticulture and viticulture.

South America delivers the most dynamic growth, led by Brazil's expanding market and favorable regulatory reforms that unify bioinput approvals. A significant portion of Brazilian growers now report routine biological use, and annual market expansion vastly outstrips the global average. Argentina's equivalency recognition and Chile's public research funding enhance regional momentum. Asia-Pacific registers strong potential tied to rising organic acreage and government sustainability mandates, yet progress is fragmented by variable regulatory timelines and limited technical extension. Africa and the Middle East represent early-stage markets where donor-funded programs and multinational demonstrations seed future demand.

- Bayer AG

- BASF SE

- Syngenta Group

- Corteva Agriscience

- FMC Corporation

- Valent BioSciences LLC (Sumitomo Chemical Co., Ltd.)

- Certis USA LLC (Mitsui and Co., Ltd.)

- Koppert B.V.

- Andermatt Group AG

- Marrone Bio Innovations Inc. (Bioceres Crop Solutions Corp.)

- Seipasa SA

- T.Stanes and Company Limited

- UPL Ltd.

- Atlantica Agricola

- Gujarat State Fertilizers and Chemicals Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Australia

- 4.3.3 Brazil

- 4.3.4 Canada

- 4.3.5 China

- 4.3.6 Egypt

- 4.3.7 France

- 4.3.8 Germany

- 4.3.9 India

- 4.3.10 Indonesia

- 4.3.11 Iran

- 4.3.12 Italy

- 4.3.13 Japan

- 4.3.14 Mexico

- 4.3.15 Netherlands

- 4.3.16 Nigeria

- 4.3.17 Philippines

- 4.3.18 Russia

- 4.3.19 South Africa

- 4.3.20 Spain

- 4.3.21 Thailand

- 4.3.22 Turkey

- 4.3.23 United Kingdom

- 4.3.24 United States

- 4.3.25 Vietnam

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Stricter global curbs on synthetic pesticides

- 4.5.2 Expansion of organic farming acreage

- 4.5.3 Rising resistance to conventional chemistries

- 4.5.4 Government bio-pesticide incentives and fast-track approvals

- 4.5.5 Growth of controlled-environment agriculture (CEA)

- 4.5.6 Fermentation-as-a-service lowering scale-up barriers

- 4.6 Market Restraints

- 4.6.1 Higher cost versus synthetic pesticides

- 4.6.2 Shorter shelf life and cold-chain dependence

- 4.6.3 Feed-stock price volatility for microbial production

- 4.6.4 Absence of uniform field-performance KPIs

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Form

- 5.1.1 Biofungicides

- 5.1.2 Bioherbicides

- 5.1.3 Bioinsecticides

- 5.1.4 Other Biopesticides

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Geography

- 5.3.1 Africa

- 5.3.1.1 By Country

- 5.3.1.1.1 Egypt

- 5.3.1.1.2 Nigeria

- 5.3.1.1.3 South Africa

- 5.3.1.1.4 Rest of Africa

- 5.3.1.1 By Country

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Country

- 5.3.2.1.1 Australia

- 5.3.2.1.2 China

- 5.3.2.1.3 India

- 5.3.2.1.4 Indonesia

- 5.3.2.1.5 Japan

- 5.3.2.1.6 Philippines

- 5.3.2.1.7 Thailand

- 5.3.2.1.8 Vietnam

- 5.3.2.1.9 Rest of Asia-Pacific

- 5.3.2.1 By Country

- 5.3.3 Europe

- 5.3.3.1 By Country

- 5.3.3.1.1 France

- 5.3.3.1.2 Germany

- 5.3.3.1.3 Italy

- 5.3.3.1.4 Netherlands

- 5.3.3.1.5 Russia

- 5.3.3.1.6 Spain

- 5.3.3.1.7 Turkey

- 5.3.3.1.8 United Kingdom

- 5.3.3.1.9 Rest of Europe

- 5.3.3.1 By Country

- 5.3.4 Middle East

- 5.3.4.1 By Country

- 5.3.4.1.1 Iran

- 5.3.4.1.2 Saudi Arabia

- 5.3.4.1.3 Rest of Middle East

- 5.3.4.1 By Country

- 5.3.5 North America

- 5.3.5.1 By Country

- 5.3.5.1.1 Canada

- 5.3.5.1.2 Mexico

- 5.3.5.1.3 United States

- 5.3.5.1.4 Rest of North America

- 5.3.5.1 By Country

- 5.3.6 South America

- 5.3.6.1 By Country

- 5.3.6.1.1 Argentina

- 5.3.6.1.2 Brazil

- 5.3.6.1.3 Rest of South America

- 5.3.6.1 By Country

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global-Level Overview, Market-Level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Bayer AG

- 6.4.2 BASF SE

- 6.4.3 Syngenta Group

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Valent BioSciences LLC (Sumitomo Chemical Co., Ltd.)

- 6.4.7 Certis USA LLC (Mitsui and Co., Ltd.)

- 6.4.8 Koppert B.V.

- 6.4.9 Andermatt Group AG

- 6.4.10 Marrone Bio Innovations Inc. (Bioceres Crop Solutions Corp.)

- 6.4.11 Seipasa SA

- 6.4.12 T.Stanes and Company Limited

- 6.4.13 UPL Ltd.

- 6.4.14 Atlantica Agricola

- 6.4.15 Gujarat State Fertilizers and Chemicals Ltd.

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

生物农药市场:按类型、作物、配方、应用和销售管道划分-2026-2032年全球市场预测

生物农药市场:按类型、作物、配方、应用和销售管道划分-2026-2032年全球市场预测 全球生物农药市场规模、份额、趋势和成长分析报告(2026-2034年)

全球生物农药市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球生物农药市场报告

2026年全球生物农药市场报告 生物农药市场规模、份额和趋势分析报告:按产品、作物类型、来源、应用、地区和细分市场划分 - 预测,2026-2033年

生物农药市场规模、份额和趋势分析报告:按产品、作物类型、来源、应用、地区和细分市场划分 - 预测,2026-2033年 生物製药市场-全球产业规模、份额、趋势、机会、预测:按类型、作物类型、应用、製剂、地区和竞争格局划分,2021-2031年农业生物农药市场按类型、作用方式、应用、作物类型和剂型划分-2026-2032年全球预测芽孢桿菌作物保护市场按作物类型、配方类型、应用方法、最终用户和销售管道划分-2026-2032年全球预测

生物製药市场-全球产业规模、份额、趋势、机会、预测:按类型、作物类型、应用、製剂、地区和竞争格局划分,2021-2031年农业生物农药市场按类型、作用方式、应用、作物类型和剂型划分-2026-2032年全球预测芽孢桿菌作物保护市场按作物类型、配方类型、应用方法、最终用户和销售管道划分-2026-2032年全球预测 日本生物农药市场报告(按产品类型(生物除草剂、生物杀虫剂、生物杀菌剂及其他)、应用(作物用、非作物用)和地区划分,2026-2034)

日本生物农药市场报告(按产品类型(生物除草剂、生物杀虫剂、生物杀菌剂及其他)、应用(作物用、非作物用)和地区划分,2026-2034) 全球生物肥料和生物农药市场:预测至2032年-按产品类型、形态、应用方法、作物类型和地区分類的分析生物农药:主要国家天然农药市场分析

全球生物肥料和生物农药市场:预测至2032年-按产品类型、形态、应用方法、作物类型和地区分類的分析生物农药:主要国家天然农药市场分析