|

市场调查报告书

商品编码

1906903

液晶聚合物(LCP):市场占有率分析、产业趋势与统计、成长预测(2026-2031)Liquid Crystal Polymers (LCP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

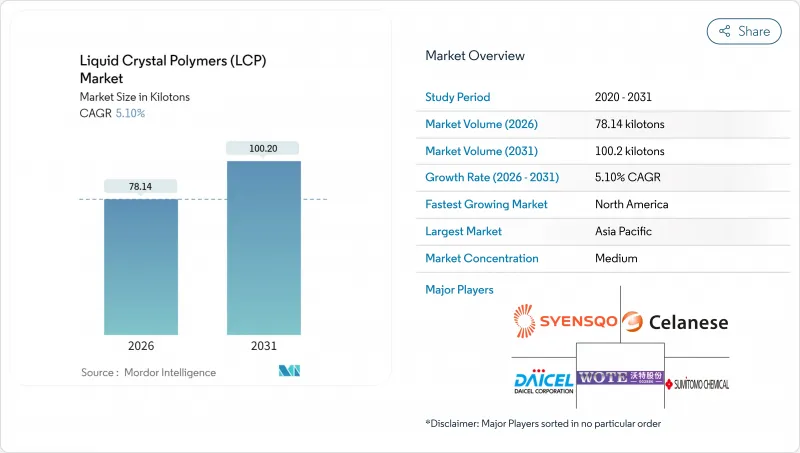

液晶聚合物(LCP)市场预计将从 2025 年的 74.35 千吨成长到 2026 年的 78.14 千吨,预计到 2031 年将达到 100.2 千吨,2026 年至 2031 年的复合年增长率为 5.10%。

这一上升趋势由三大相互关联的支柱驱动:5G网路硬体的稳定部署、向电池式电动车的加速转型以及整个产业对高频电子组件小型化的不懈追求。所有这些终端应用都要求聚合物在热应力下保持尺寸精度,在毫米波频宽内具有极低的电损耗,并在较长的使用寿命内保持其机械完整性。推动其普及的驱动力是产量而非价格。设计工程师主要选择液晶聚合物(LCP)等级,因为它们具有低介电常数、低损耗因子和优异的耐湿性。这使得液晶聚合物(LCP)市场成为新一代天线模组、高压逆变器封装以及柔性高密度互连的关键材料。能够确保特种二元酸和二硫代氨基甲酸酯稳定供应的公司,将能够抓住下游需求成长带来的显着销售成长机会。

全球液晶聚合物(LCP)市场趋势与洞察

SMT元件和5G射频模组的小型化

宽频天线研究表明,在毫米波频段,液晶聚合物(LCP)基板的介电常数小于3.5,损耗角正切小于0.004,这使得28GHz基地台能够实现紧凑型阵列单元,且不会造成讯号劣化。此材料沿机器方向的收缩率仅为0.05%,从而在用于MIMO波束成形的细线电路中保持电阻控制。为满足中国新增70万个5G基地台以及美国营运商对现有基地台维修的需求,Polyplastics公司已将其聚合产能扩大至2025年达到2.5万吨。儘管介电常数公差要求严格,但由于其在传统射出成型设备上的加工成本低廉,液晶聚合物(LCP)市场仍然是无线模组大规模生产的理想选择。这为满足6G性能要求的原始设备製造商(OEM)创造了一个增强设计柔软性的生态系统。

电动车电力电子领域金属的轻量化替代品

此热响应等级的材料与铜汇流排的热膨胀係数(0.1-2.0×10⁻⁵/°C)相匹配,并能消除剪切应力,从而劣化800V逆变器中焊点的劣化。能量转换研究证实,LCP冷却板在200A充电速率下,可达到36%的减重,同时保持电池模组温度均匀性在±2°C以内。塞拉尼斯推出了一种用于微型基板对板连接器的超流体等级材料,可在-40°C至150°C的温度范围内承受3000次热循环而不发生翘曲。汽车製造商的排碳权策略鼓励零件轻量化,从而将液晶聚合物(LCP)市场从引擎室感测器扩展到驱动电压组件。供应协议将设计支援与回收材料回收方案相结合,以帮助原始设备製造商(OEM)实现其循环经济目标。

高价优质布料与耐高温尼龙和PPS布料的比较

聚苯硫( LPS)能够承受250°C的连续使用,且原料成本降低35-50%,因此在家用电子电器的通用连接器中被广泛应用。一级汽车供应商正在协商双模策略,并将耐高温尼龙作为绝缘性能要求不高的非关键机壳部件的预设材料。射出成型需要将料筒温度控制在±2°C以内,模具温度超过300°C,这增加了能耗和生产週期成本,阻碍了其在新兴市场的普及。虽然近期生物基变体已将溢价降低了8-10%,但大规模生产零件的价格仍远未达到与传统材料持平。这种成本差异持续阻碍液晶聚合物(LCP)市场在通用电子产品领域的广泛渗透。

细分市场分析

热致液晶材料预计在2025年占总产量的92.58%,与现有供应链及传统熔融加工设备相容。这些材料在280至340°C的温度范围内流动时仍能保持其晶体结构,具有固有的阻燃性,无需在超薄连接器中添加卤素基添加剂。热响应液晶聚合物具有低于3.2的等向性介电常数,是亚太地区5G智慧型手机天线基板的首选材料。 2025年,Serenes推出了一款生物基含量达60%的产品,符合UL 94 V-0标准,加速了永续性进程。溶剂型液晶聚合物虽然目前市占率小规模(以体积计仅7.42%),但其年复合成长率预计将达到7.12%,因为航太复合材料需要拉伸强度高于3.2 GPa的溶液纺丝纤维。製造商正投资溶剂回收设备以降低营运成本,但资本投资障碍限制了溶剂型生产能力,使其仅限于少数几家一体化製造商。随着积层製造製造商在流变型长丝认证方面取得进展,用于3D列印雷达罩的液晶聚合物(LCP)市场规模预计将会扩大,尤其是在国防平台领域。

本液晶聚合物 (LCP) 报告按产品类型(热致液晶聚合物和溶剂致液晶聚合物)、终端用户产业(航太、汽车、电气电子、工业机械及其他终端用户产业)和地区(北美、南美、欧洲、亚太、中东和非洲)进行细分。市场预测以数量(吨)和价值(美元)为单位。

区域分析

亚太地区保持主导地位,预计2025年将占全球价值的72.45%,这得益于其完善的电子生态系统,缩短了从聚合到成品模组的前置作业时间。中国政府对5G基地台建设的补贴确保了稳定的需求,而日本汽车零件供应商则继续采用液晶聚合物(LCP)製造雷达连接器,以满足零缺陷的要求。宁波週边的生产群集利用接近性港口的优势,帮助出口到欧洲行动电话製造商的供应商降低物流成本。

到2031年,北美将以5.98%的复合年增长率成为成长最快的地区,这主要得益于无线通讯业者升级中频宽频谱,部署大规模MIMO阵列,而这些阵列需要低损耗基板。住友化学于2025年收购了Syensqo的Neato树脂资产,其中包括位于德克萨斯州的一条试验生产线,这增强了国防电子产品的国内供应安全。主要的航太製造商正在利用这些在地采购资源,对航空电子设备中铝EMI屏蔽的LCP替代品进行认证,此举符合政府支持的製造业回流政策。

欧洲保持了温和的个位数成长,这主要得益于燃料电池堆开发商优先考虑氢气环境下的耐化学腐蚀性能。汽车製造商正在将液晶聚合物(LCP)集管板整合到其800V逆变器设计中,以满足欧盟2019/631号法规规定的2027年二氧化碳排放目标。匈牙利和瑞典超级工厂的建设提高了高压电池机壳的产能,从而提振了该地区对液晶聚合物(LCP)的需求。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- SMT元件和5G射频模组的小型化

- 电动车电力电子领域金属的轻量化替代品

- 高频柔性电路的需求快速成长

- 用于穿戴式/植入式医疗感测器的液晶聚合物薄膜

- LCP膜在PEM燃料电池和氢电解的应用

- 市场限制

- 与耐高温尼龙和PPS相比,价格溢价较高。

- 复杂模具中的焊接强度不足和异向性收缩

- 特殊二酸/二胺上游供应集中化

- 价值链分析

- 监管环境

- 波特五力模型

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 终端用户产业趋势

- 航太(航太零件生产收入)

- 汽车(汽车生产)

- 建筑与施工(新增建筑面积)

- 电气电子设备(电气电子设备生产收入)

- 包装(塑胶包装数量)

第五章 市场规模及成长预测(价值及数量)

- 依产品类型

- 热致液晶聚合物

- 石化 LCP

- 按最终用户行业划分

- 航太

- 车

- 电气和电子设备

- 工业和机械

- 其他终端用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 马来西亚

- 亚太其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Avient Corporation

- Celanese Corporation

- HUAMI NEW MATERIAL

- Kingfa Sci.&Tech. Co.,Ltd.

- Kuraray Co., Ltd.

- Ningbo Jujia New Material Technology Co., Ltd

- Daicel Corporation

- RTP Company

- SABIC

- Shenzhen WOTE Advanced Materials Co., Ltd.

- Sumitomo Chemical Co., Ltd.

- Syensqo

- Toray Industries, Inc.

- UENO FINE CHEMICALS INDUSTRY,LTD.

第七章 市场机会与未来展望

第八章:执行长面临的关键策略挑战

The Liquid Crystal Polymers Market is expected to grow from 74.35 kilotons in 2025 to 78.14 kilotons in 2026 and is forecast to reach 100.2 kilotons by 2031 at 5.10% CAGR over 2026-2031.

This upward curve rests on three interconnected pillars: the steady roll-out of 5G network hardware, the accelerating shift toward battery-electric vehicles, and the industry-wide drive to miniaturize high-frequency electronic assemblies. Each of these end-uses requires polymers that maintain dimensional accuracy under thermal stress, exhibit negligible electrical loss at millimeter-wave frequencies, and retain mechanical integrity over long service lives. Volume rather than price determines adoption, because design engineers primarily choose LCP grades for their low dielectric constants, low dissipation factors, and excellent moisture resistance. Against that backdrop, the liquid crystal polymer market has become a critical input for next-generation antenna modules, high-voltage inverter packages, and flexible high-density interconnects. Firms able to secure reliable feedstocks of specialty diacids and diols position themselves to capture outsized volumes as downstream demand rises.

Global Liquid Crystal Polymers (LCP) Market Trends and Insights

Miniaturization of SMT Components & 5G RF Modules

Wideband antenna studies show that LCP substrates sustain dielectric constants below 3.5 and loss tangents under 0.004 at mmWave frequencies, enabling compact array elements for 28 GHz base stations without signal degradation. The material exhibits machine-direction shrinkage as low as 0.05%, maintaining impedance control in fine-line circuits used for Multiple-Input and Multiple-Output (MIMO) beam-forming. Polyplastics lifted polymerization capacity to 25,000 tons in 2025 to satisfy handset and infrastructure demand as China adds 700,000 new 5G base stations and United States operators retrofit legacy sites. Despite tight dielectric tolerances, cost-effective processing on conventional injection equipment keeps the liquid crystal polymer market attractive for high-volume radio modules. The resulting ecosystem strengthens design flexibility for original equipment manufacturers (OEMs) targeting 6G-ready performance envelopes.

Lightweight Substitution for Metals in EV Power-electronics

Thermotropic grades match the 0.1-2.0 X 10-5/°C coefficient of thermal expansion of copper busbars, eliminating shear stress that degrades solder joints in 800 V inverters. Energy-conversion research confirms that LCP cooling plates achieve a 36% weight saving while maintaining +-2°C temperature uniformity across battery modules at 200 A charge rates. Celanese introduced ultra-high-flow variants for miniature board-to-board connectors that survive 3,000 thermal cycles between -40°C and 150°C without warpage. Automakers' carbon-credit strategies reward component light-weighting, expanding the liquid crystal polymer market beyond under-hood sensors into traction voltage assemblies. Supply agreements now bundle design support and recyclate take-back options to satisfy OEM circularity targets.

High Price Premium vs. High-temperature Nylons and PPS

Polyphenylene sulfide delivers 250°C continuous service at 35-50% lower raw-material cost, steering commodity connectors away from LCP in consumer electronics. Automotive Tier 1 suppliers negotiate dual-tooling strategies so that non-critical housings default to high-temperature nylons when dielectric performance is non-essential. Injection setups for LCP require +-2°C barrel control and mold temperatures above 300°C, raising energy consumption and cycle-time costs, discouraging adoption in emerging economies. Recent bio-based variants narrow the premium by 8-10%, yet price parity remains distant for high-volume parts. This cost gap continues to slow the broader penetration of the liquid crystal polymer market into commodity electronics.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Demand for High-frequency Flexible Circuits

- LCP Films for Wearable/implantable Medical Sensors

- Weld-line Weakness and Anisotropic Shrinkage in Complex Molds

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thermotropic grades accounted for 92.58% of 2025 volume, underscoring their entrenched supply chains and compatibility with conventional melt-processing equipment. These materials flow at 280-340°C yet retain their crystalline order, yielding inherent flame retardancy and eliminating the need for halogen additives in ultrathin connectors. Consistent isotropic dielectric values below 3.2 make thermotropic LCPs the preferred choice for antenna substrates in 5G smartphones across the Asia-Pacific region. Sustainability gained momentum in 2025 when Celanese introduced a 60% bio-content variant that did not compromise its UL 94 V-0 ratings. Lyotropic LCP, though only 7.42% by volume, benefits from a 7.12% CAGR as aerospace composites demand solution-spun fibers with tensile strengths above 3.2 GPa. Manufacturers invest in solvent recovery units to reduce operating costs, but CAPEX hurdles limit lyotropic capacity to a handful of integrated producers. As additive manufacturers qualify lyotropic filaments for 3D-printed radomes, the liquid crystal polymer market size in this sub-segment is expected to expand, particularly in defense platforms.

The Liquid Crystal Polymer Report is Segmented by Product Type (Thermotropic LCP and Lyotropic LCP), End-User Industry (Aerospace, Automotive, Electrical and Electronics, Industrial and Machinery, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons) and Value (USD).

Geography Analysis

The Asia-Pacific region retained its leadership position, accounting for 72.45% of the 2025 value, bolstered by dedicated electronics ecosystems that compress lead times from polymerization to finished modules. Government subsidies in China for 5G base-station roll-outs ensure stable offtake, while Japan's automotive tier suppliers continue to specify LCP in radar connectors to meet zero-defect mandates. Production clusters around Ningbo benefit from port proximity, cutting logistics costs for exporters serving European handset makers.

North America posted the fastest 5.98% CAGR to 2031 as wireless carriers upgraded mid-band spectrum with massive MIMO arrays that require low-loss substrates. Sumitomo Chemical's 2025 acquisition of Syensqo's neat-resin assets included pilot lines in Texas, reinforcing domestic supply security for defense electronics. Aerospace primes leverage these local sources to qualify LCP replacements for aluminum EMI shields in avionics, aligning with stimulus-backed on-shoring agendas.

Europe maintained mid-single-digit growth, driven by fuel-cell stack developers that value LCP's chemical resilience in hydrogen environments. Automotive OEMs incorporate LCP header plates in 800 V inverter designs to meet 2027 CO2 fleet targets under EU (European Union) Regulation 2019/631. Deployment of gigafactories in Hungary and Sweden signals incremental capacity for high-voltage battery enclosures, widening regional demand for the liquid crystal polymer market.

- Avient Corporation

- Celanese Corporation

- HUAMI NEW MATERIAL

- Kingfa Sci.&Tech. Co.,Ltd.

- Kuraray Co., Ltd.

- Ningbo Jujia New Material Technology Co., Ltd

- Daicel Corporation

- RTP Company

- SABIC

- Shenzhen WOTE Advanced Materials Co., Ltd.

- Sumitomo Chemical Co., Ltd.

- Syensqo

- Toray Industries, Inc.

- UENO FINE CHEMICALS INDUSTRY,LTD.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Miniaturization of SMT Components & 5G RF Modules

- 4.2.2 Lightweight Substitution for Metals in EV Power-electronics

- 4.2.3 Surge in Demand for High-frequency Flexible Circuits

- 4.2.4 LCP Films for Wearable/implantable Medical Sensors

- 4.2.5 Use of LCP Membranes in PEM Fuel-cells and Hydrogen Electrolysers

- 4.3 Market Restraints

- 4.3.1 High Price Premium vs. High-temperature Nylons and PPS

- 4.3.2 Weld-line Weakness and Anisotropic Shrinkage in Complex Molds

- 4.3.3 Concentrated Upstream Supply of Specialty Diacids/diols

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 End-use Sector Trends

- 4.7.1 Aerospace (Aerospace Component Production Revenue)

- 4.7.2 Automotive (Automobile Production)

- 4.7.3 Building and Construction (New Construction Floor Area)

- 4.7.4 Electrical and Electronics (Electrical and Electronics Production Revenue)

- 4.7.5 Packaging(Plastic Packaging Volume)

5 Market Size & Growth Forecasts (Value and Volume)

- 5.1 By Product Type

- 5.1.1 Thermotropic LCP

- 5.1.2 Lyotropic LCP

- 5.2 By End-User Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Electrical and Electronics

- 5.2.4 Industrial and Machinery

- 5.2.5 Other End-user Industries

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 United Kingdom

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 South Korea

- 5.3.4.5 Australia

- 5.3.4.6 Malaysia

- 5.3.4.7 Rest of Asia-Pacific

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Nigeria

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)**/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Avient Corporation

- 6.4.2 Celanese Corporation

- 6.4.3 HUAMI NEW MATERIAL

- 6.4.4 Kingfa Sci.&Tech. Co.,Ltd.

- 6.4.5 Kuraray Co., Ltd.

- 6.4.6 Ningbo Jujia New Material Technology Co., Ltd

- 6.4.7 Daicel Corporation

- 6.4.8 RTP Company

- 6.4.9 SABIC

- 6.4.10 Shenzhen WOTE Advanced Materials Co., Ltd.

- 6.4.11 Sumitomo Chemical Co., Ltd.

- 6.4.12 Syensqo

- 6.4.13 Toray Industries, Inc.

- 6.4.14 UENO FINE CHEMICALS INDUSTRY,LTD.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

8 Key Strategic Questions for CEOs

2026年全球液晶聚合物纤维(LCP纤维)市场研究报告

2026年全球液晶聚合物纤维(LCP纤维)市场研究报告 聚合物分散液晶薄膜市场:按薄膜类型、技术、应用和最终用途产业分類的全球预测(2026-2032年)

聚合物分散液晶薄膜市场:按薄膜类型、技术、应用和最终用途产业分類的全球预测(2026-2032年) 液晶聚合物全球市场报告(2026)

液晶聚合物全球市场报告(2026) 液晶聚合物市场-全球产业规模、份额、趋势、机会及预测(按类型、终端用户产业、地区及竞争格局划分,2021-2031年)HTN液晶显示器市场按产品类型、等级、销售管道、应用和最终用户划分,全球预测(2026-2032)PDLC建筑用光控膜市场:按产品规格、安装类型、应用、最终用户和分销管道分類的全球预测(2026-2032年)汽车液晶调光膜市场:依薄膜类型、车辆类型、应用和销售管道,全球预测,2026-2032年环己酮液晶中间体市场依生产方法、纯度等级、物理形态、应用、终端用户产业及通路划分,全球预测(2026-2032年)碳纤维增强液晶聚合物市场:依加工技术、产品形式、纤维含量、纤维长度、终端应用产业及销售管道,全球预测,2026-2032年纤维增强液晶聚合物市场(依纤维类型、製造流程、形状、等级和应用划分)-全球预测,2026-2032年

液晶聚合物市场-全球产业规模、份额、趋势、机会及预测(按类型、终端用户产业、地区及竞争格局划分,2021-2031年)HTN液晶显示器市场按产品类型、等级、销售管道、应用和最终用户划分,全球预测(2026-2032)PDLC建筑用光控膜市场:按产品规格、安装类型、应用、最终用户和分销管道分類的全球预测(2026-2032年)汽车液晶调光膜市场:依薄膜类型、车辆类型、应用和销售管道,全球预测,2026-2032年环己酮液晶中间体市场依生产方法、纯度等级、物理形态、应用、终端用户产业及通路划分,全球预测(2026-2032年)碳纤维增强液晶聚合物市场:依加工技术、产品形式、纤维含量、纤维长度、终端应用产业及销售管道,全球预测,2026-2032年纤维增强液晶聚合物市场(依纤维类型、製造流程、形状、等级和应用划分)-全球预测,2026-2032年