|

市场调查报告书

商品编码

1906920

直链烷基苯(LAB):市场占有率分析、产业趋势与统计、成长预测(2026-2031)Linear Alkyl Benzene (LAB) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

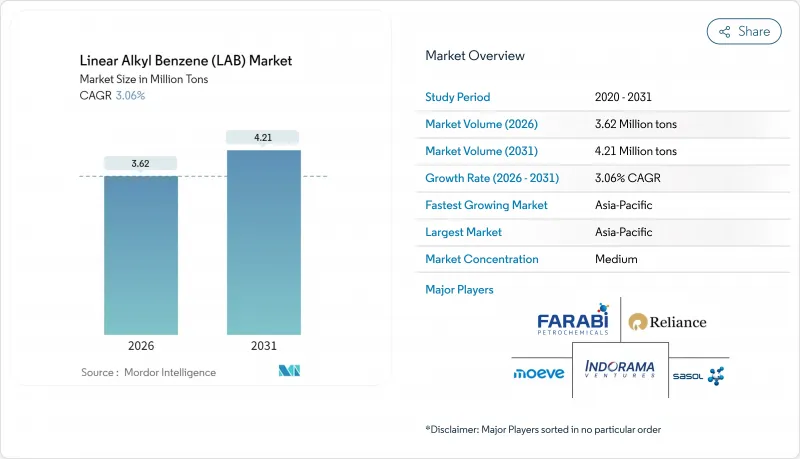

2025年,直链烷基苯市场价值为351万吨,预计2031年将达到421万吨,高于2026年的362万吨。

预计在预测期(2026-2031 年)内,复合年增长率将达到 3.06%。

线性烷基苯作为线性磺酸盐磺酸盐的主要前体,其稳定的需求支撑着这一增长,而消费者和监管机构对可生物降解的阴离子界面活性剂而非传统支链清洁剂的偏好日益增强,也推动了这一增长。人口稠密的新兴经济体中清洁剂渗透率的提高、疫情后人们对家庭和机构卫生持续关注,以及对数位化设备升级的持续投资,都为线性烷基苯市场带来了更多机会。拥有强大的苯和石蜡一体化能力的生产商将增强其成本优势,而持续的数位化设备维修将带来降低碳排放和提高製程安全性的双重效益。同时,对冷媒添加剂等高附加价值细分应用的探索将推动产量成长,并降低对相对成熟的清洁剂价值链的依赖。

全球线性烷基苯(LAB)市场趋势与洞察

新兴经济体清洁剂渗透率不断上升

新兴经济体的清洁剂消费量正持续缩小与已开发地区的差距,每年新增数百万洗衣用户。在家庭清洁剂更换週期中,预包装合成清洁剂比传统肥皂更受欢迎。这是因为基于线性烷基苯(LAS)的配方在农村和郊区常见的硬水环境中表现出更优异的性能。包装清洁剂也采用小小袋,以适应低收入群体的购买习惯,从而为线性烷基苯市场创造了稳定的需求来源。在印度,政府的卫生宣传活动和不断扩大的零售网路正在推动清洁剂在全部区域的普及。撒哈拉以南非洲和部分中东经济体也出现了类似的趋势,进一步扩大了潜在基本客群。这些趋势共同构成了一个结构性成长平台,将在中期内支持线性烷基苯市场的扩张。

监管机构推动可生物降解的LAS表面活性剂

环境监管机构正在收紧清洁剂的降解标准,加速向基于直链烷基苯的界面活性剂(LAS)过渡。欧盟的REACH法规结构强调了直链LAS相比支链LAS具有更高的降解速率,这使得直链烷基苯成为符合法规要求的理想原料。由于污水处理成本不断上升,水资源紧张地区也开始采用类似的排放标准。品牌所有者透过将清洁剂和清洁剂标註为「可生物降解」来将合规性转化为市场价值,从而支撑更高的平均售价。认证机构在评估界面活性剂的选择时会参考ISO 14852和ASTM D-2667测试方法,这进一步巩固了直链烷基苯的需求优势。随着各国调整其化学品策略以符合《巴黎协定》,生物基界面活性剂正成为跨国公司不可或缺的组成部分,从而巩固了其长期需求前景。

原材料价格波动给利润率带来压力。

直链烷基苯生产商依赖苯和烷烃,而这两种原料的价格与全球原油价格密切相关。季度价格波动往往会挤压非一体化生产商的转换价差。库存持有策略可以缓解这种影响,但无法完全消除风险,尤其是在期货曲线倒挂的情况下。一体化炼油厂虽然处于更有利的地位,但仍面临着因避险成本和炼油厂计划停产而导致的供应中断风险。新兴亚洲企业在结算原料进口时,也面临美元外汇波动带来的额外挑战。原料价格持续波动会降低规划的透明度,抑制可自由支配的资本投资,并削弱直链烷基苯市场的近期成长动能。

细分市场分析

界面活性剂应用预计将在2025年占总产量的96.78%,巩固了线性烷基苯作为日常清洁产品关键成分的地位。线性烷基苯(LAS)在清洁剂和液体清洁剂配方中,尤其是在消费广泛地区普遍存在的硬水条件下,其卓越的性能是推动其占据主导地位的主要原因。其他应用领域也以4.48%的复合年增长率成长,成长率超过整体市场,主要得益于配方师对冷却剂添加剂和特定工业清洁剂的探索。从盈利角度来看,界面活性剂的需求确保了产能的高运转率,而向特种应用领域的多元化发展则提高了利润率,并帮助生产商抵御清洁剂市场週期性波动的影响。

生产製程规范对C10-C13炼长分布有严格的要求,促使企业加强对原料精炼的投资,以满足高端线性烷基苯(LAS)的要求。近期研究表明,硫酸洗涤处理能够减少烯烃杂质,从而提高清洁剂的白度并降低配方稳定剂的用量。汽车冷却液供应商优先考虑高氧化稳定性,并将新技术引入传统上以大众市场主导的市场。这些不断发展的性能标准延长了数位化工厂的使用寿命,并持续生产出比传统氢氟酸(HF)製程纯度更高的产品。总而言之,这些趋势再次印证了界面活性剂的重要性,同时促进了利基市场的稳定成长,并确保了线性烷基苯市场的均衡扩张。

线性烷基苯市场报告按应用领域(界面活性剂及其他应用)、终端用户行业(清洁剂、轻型洗碗精、工业清洁剂清洁剂、家用清洁剂其他终端用户行业)和地区(亚太地区、北美地区、欧洲地区、南美地区以及中东和非洲地区)进行细分。市场预测以公吨为单位。

区域分析

预计亚太地区将在2025年以53.72%的市占率引领全球,并在2031年之前维持4.12%的复合年增长率。消费者人口结构变化和都市化,以及包装清洁剂使用量的增加,正在推动苯供应的成长。中国、印度和中东的综合芳烃生产设施确保了苯的稳定供应和具有竞争力的成本。近期启动的烷烃脱氢装置计划进一步增强了该地区的自给自足能力,并降低了进口依赖性和运输风险。中国沿海地区的产业丛集降低了原料和成品的末端物流成本,并将当地的汽油级烯烃快速转化为高纯度的直链烷基苯。

儘管欧洲的生产成长缓慢,但它在製定最佳环境标准方面发挥着至关重要的作用。欧盟委员会的《大规模生产的有机化学品》参考文件加强了废水和排放指南,加速了现有工厂向Detal製程的维修。西班牙和比利时的生产商已经完成了产能升级,并提高了高纯度产品的产量,同时降低了能源消耗。总部位于该地区的消费品牌正在采用“生命週期评估,包括生产前评估”,这巩固了他们对Detal製程生产的表面活性剂的优先采购地位。

在北美,丰富的页岩原料供应使得苯和烷烃的价格结构性地保持低位且稳定。然而,不断上涨的氢氟酸监管成本加剧了竞争压力,并引发了将资金重新分配至下游生产线的讨论。美国沿岸地区的生产商正在探索下游线性烷基苯(LAS)一体化的优势,以降低价格波动并在中间环节创造附加价值。美国《通货膨胀控制法案》带来的监管透明度使得节能维修能够转化为排碳权。这些因素共同作用,正稳定且策略性地推动线性烷基苯市场的发展。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 新兴经济体清洁剂渗透率不断上升

- 推动可生物降解的LAS表面活性剂的监管

- 后新冠时代卫生管理与清洁的彻底性

- 透过 Detail-2 修改来减少 LAB 的碳足迹

- LAB在电动车冷却液添加剂包的应用

- 市场限制

- 原料(苯和石蜡)价格波动

- HF路线遵守环境法规的成本

- 东协向棕榈油基MES清洁剂的过渡

- 价值链分析

- 价格概览

- 贸易分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 透过使用

- 界面活性剂

- 其他用途

- 按最终用户行业划分

- 洗衣精

- 轻型清洁剂

- 工业清洁剂

- 家用清洁剂

- 其他终端用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- CNPC(Fushun Petrochemical)

- Egyptian Petrochemicals Holding Company(ECHEM)

- Farabi Petrochemicals Company

- Formosan Union Chemical Corp.

- Indian Oil Corporation Ltd

- Indorama Ventures Public Company Limited

- ISU Chemical

- JINTUNG Petrochemical Co., Ltd

- Kinef

- Moeve

- NIRMA

- PT Unggul Indah Cahaya Tbk

- QatarEnergy

- Reliance industries Limited

- SBK HOLDING

- Sasol

- Tamilnadu Petroproducts Limited

- Thai Oil Public Company Limited

第七章 市场机会与未来展望

The Linear Alkyl Benzene Market was valued at 3.51 Million tons in 2025 and estimated to grow from 3.62 Million tons in 2026 to reach 4.21 Million tons by 2031, at a CAGR of 3.06% during the forecast period (2026-2031).

Steady demand for linear alkyl benzene as the key precursor to linear alkyl benzene sulfonate underpins this growth as consumers and regulators favor biodegradable anionic surfactants over legacy branched-chain detergents. Rising detergent penetration across populous emerging economies, a sustained post-pandemic focus on household and institutional hygiene, and continued investments in upgraded Detal units collectively widen the linear alkyl benzene market opportunity set. Producers with secure benzene and paraffin integration deepen cost leadership, while ongoing Detal retrofits provide dual benefits of lower carbon intensity and improved process safety. Meanwhile, the pursuit of value-added niche applications such as coolant additives augments incremental volume growth and reduces reliance on the relatively mature detergent value chain.

Global Linear Alkyl Benzene (LAB) Market Trends and Insights

Rising Detergent Penetration in Emerging Economies

Emerging economies continue to close the detergent consumption gap with industrialized regions, adding millions of new wash-day users each year. Household upgrade cycles favor packaged synthetic detergents over traditional soap bars because LAS-based formulations excel in hard-water conditions that prevail in rural and peri-urban zones. Packaged detergents also leverage smaller sachet formats that align with low-income purchasing habits, creating a stable volume pull for the linear alkyl benzene market. In India, government sanitation campaigns and expanded retail access raise detergent adoption rates across rural districts. Similar dynamics in sub-Saharan Africa and selected Middle Eastern economies further enlarge the prospective customer base. Together these trends embed a structural growth floor that supports linear alkyl benzene market expansion over the medium term.

Regulatory Push for Biodegradable LAS Surfactants

Environmental regulators tighten degradability benchmarks for cleaning agents, accelerating the shift toward LAS derived from linear alkyl benzene. The European Union's REACH framework highlights faster breakdown of straight-chain LAS compared with branched analogs, making linear alkyl benzene a compliance-friendly feedstock. Water-stressed regions adopt similar discharge norms as wastewater treatment costs climb. Brand owners translate compliance into marketing premiums by labeling laundry and dishwashing detergents as biodegradable, supporting higher average selling prices. Certification bodies reference ISO 14852 and ASTM D-2667 methods when vetting surfactant choices, reinforcing the demand advantage enjoyed by linear alkyl benzene. As countries align with Paris-aligned chemical strategies, bio-favored surfactants become indispensable for multinationals, cementing the long-term demand outlook.

Feedstock Price Volatility Pressures Margins

Linear alkyl benzene producers rely on benzene and paraffin, whose price trajectories remain tethered to global crude oil swings. Quarter-to-quarter price variability tends to compress conversion spreads for non-integrated manufacturers. Inventory holding strategies mitigate but do not eliminate exposure, especially when forward curves invert. Integrated refiners fare better, yet they still confront hedging costs and occasional supply disruptions linked to refinery turnarounds. Emerging Asian players bear the additional challenge of currency fluctuations against the U.S. dollar when settling feedstock imports. Persistent input turbulence undermines planning visibility, discourages discretionary capital spending, and introduces a drag on short-term linear alkyl benzene market growth momentum.

Other drivers and restraints analyzed in the detailed report include:

- Post-COVID Hygiene and Cleaning Intensity

- Detal-2 Retrofits Cutting LAB Carbon Footprint

- HF-Route Environmental Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surfactant production accounted for 96.78% of the 2025 volume, reinforcing the linear alkyl benzene market position as an essential building block for everyday cleaning agents. This overwhelming share is anchored in the proven performance of LAS in powder and liquid detergent formulations, particularly under hard-water conditions that prevail across vast consumption territories. Other Applications outpace the headline market at 4.48% CAGR as formulators explore coolant additive packages and select industrial cleaners. From a profitability standpoint, surfactant demand ensures high asset utilization; however, diversification into specialty uses offers margin accretion and shields producers from cyclical detergent swings.

Process specifications dictate narrow C10-C13 chain-length distributions, encouraging producers to invest in feedstock purification to meet premium LAS requirements. Recent studies show that sulfuric acid wash treatments cut olefinic contaminants, thereby raising detergent brightness scores and reducing formulation stabilizer loadings. Producers supplying automotive coolant blends emphasize high oxidative stability, injecting new technical parameters into what was once a volume-driven market. These evolving performance criteria extend the life cycle of Detal plants that consistently deliver purer cuts than their HF predecessors. Taken together, these trends reinforce the primacy of surfactants while simultaneously cultivating a measured growth path for niche outlets, ensuring balanced expansion for the linear alkyl benzene market.

The Linear Alkyl Benzene Report is Segmented by Application (Surfactant and Other Applications), End-User Industry (Laundry Detergents, Light-Duty Dishwashing Liquids, Industrial Cleaners, Household Cleaners, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific dominates with a 53.72% share in 2025 and is set to grow at a 4.12% CAGR through 2031. Consumer demographics combine with urbanization to expand packaged detergent usage, while integrated aromatics complexes in China, India, and the Middle East ensure secure benzene supply at competitive cost. Recent paraffin dehydrogenation projects further reinforce regional self-sufficiency, lowering import dependence and freight exposure. Industry clusters in coastal China reduce last-mile logistics costs for both raw materials and finished goods, rapidly converting local gasoline-range olefins into high-purity linear alkyl benzene.

Europe registers modest volume growth but plays a pivotal role in setting best-practice environmental norms. The European Commission's Large Volume Organic Chemicals reference document strengthens effluent and emissions guidelines, accelerating Detal retrofits across legacy plants. Producers in Spain and Belgium have already completed capacity upgrades that boost high-purity yields while trimming energy intensity. Consumer brands headquartered in the region adopt cradle-to-gate life-cycle assessments, solidifying procurement preferences for Detal-produced surfactants.

North America benefits from ample shale-derived feedstock streams that offer structurally low benzene and paraffin costs. Competitive pressure nevertheless mounts as HF compliance costs climb, prompting debate over capital redeployment toward Detal lines. Gulf Coast producers weigh the merits of downstream LAS integration to capture additional value and mitigate volatility at the intermediate stage. Regulatory visibility provided by the U.S. Inflation Reduction Act paves the way for carbon-credit monetization of energy-efficient retrofits. Collectively, these factors produce a steady but strategically significant contribution to the linear alkyl benzene market.

- CNPC (Fushun Petrochemical)

- Egyptian Petrochemicals Holding Company (ECHEM)

- Farabi Petrochemicals Company

- Formosan Union Chemical Corp.

- Indian Oil Corporation Ltd

- Indorama Ventures Public Company Limited

- ISU Chemical

- JINTUNG Petrochemical Co., Ltd

- Kinef

- Moeve

- NIRMA

- PT Unggul Indah Cahaya Tbk

- QatarEnergy

- Reliance industries Limited

- S.B.K HOLDING

- Sasol

- Tamilnadu Petroproducts Limited

- Thai Oil Public Company Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising detergent penetration in emerging economies

- 4.2.2 Regulatory push for biodegradable LAS surfactants

- 4.2.3 Post-COVID hygiene and cleaning intensity

- 4.2.4 Detal-2 retrofits cutting LAB carbon footprint

- 4.2.5 LAB use in EV coolant additive packages

- 4.3 Market Restraints

- 4.3.1 Feedstock (benzene and paraffin) price volatility

- 4.3.2 HF-route environmental compliance costs

- 4.3.3 ASEAN shift to palm-based MES detergents

- 4.4 Value Chain Analysis

- 4.5 Price Overview

- 4.6 Trade Analysis

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Application

- 5.1.1 Surfactant

- 5.1.2 Other Applications

- 5.2 By End-User Industry

- 5.2.1 Laundry Detergents

- 5.2.2 Light-Duty Dishwashing Liquids

- 5.2.3 Industrial Cleaners

- 5.2.4 Household Cleaners

- 5.2.5 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 CNPC (Fushun Petrochemical)

- 6.4.2 Egyptian Petrochemicals Holding Company (ECHEM)

- 6.4.3 Farabi Petrochemicals Company

- 6.4.4 Formosan Union Chemical Corp.

- 6.4.5 Indian Oil Corporation Ltd

- 6.4.6 Indorama Ventures Public Company Limited

- 6.4.7 ISU Chemical

- 6.4.8 JINTUNG Petrochemical Co., Ltd

- 6.4.9 Kinef

- 6.4.10 Moeve

- 6.4.11 NIRMA

- 6.4.12 PT Unggul Indah Cahaya Tbk

- 6.4.13 QatarEnergy

- 6.4.14 Reliance industries Limited

- 6.4.15 S.B.K HOLDING

- 6.4.16 Sasol

- 6.4.17 Tamilnadu Petroproducts Limited

- 6.4.18 Thai Oil Public Company Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

全球线性烷基苯(LAB)市场规模、份额、趋势和成长分析报告(2026-2034年)

全球线性烷基苯(LAB)市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球线性烷基苯市场报告2026年全球线性烷基苯磺酸盐市场报告

2026年全球线性烷基苯市场报告2026年全球线性烷基苯磺酸盐市场报告 短链直链烷基苯磺酸盐市场按产品类型、分销管道、终端用户产业和应用划分-全球预测,2026-2032年

短链直链烷基苯磺酸盐市场按产品类型、分销管道、终端用户产业和应用划分-全球预测,2026-2032年 线性烷基苯(LAB)全球市场、产能、需求、定价及市场展望(至2034年)按纯度等级、製造流程、应用和终端用户产业分類的线性烷基苯市场—2025-2032年全球预测

线性烷基苯(LAB)全球市场、产能、需求、定价及市场展望(至2034年)按纯度等级、製造流程、应用和终端用户产业分類的线性烷基苯市场—2025-2032年全球预测 直链烷基苯 (LAB) 的全球市场 (~2050年):用途·纯度·终端用户·各地区

直链烷基苯 (LAB) 的全球市场 (~2050年):用途·纯度·终端用户·各地区 全球直链烷基苯市场规模研究,按应用(直链烷基苯磺酸盐 (LAS)、其他应用)和 2022-2032 年区域预测

全球直链烷基苯市场规模研究,按应用(直链烷基苯磺酸盐 (LAS)、其他应用)和 2022-2032 年区域预测 线性烷基苯 (LAB) 全球市场分析:工厂产能、生产、运营效率、需求/供应、最终用户行业、销售渠道、区域需求、对外贸易、公司份额 (2015-2032)

线性烷基苯 (LAB) 全球市场分析:工厂产能、生产、运营效率、需求/供应、最终用户行业、销售渠道、区域需求、对外贸易、公司份额 (2015-2032)