|

市场调查报告书

商品编码

1906941

邻苯二甲酐:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Phthalic Anhydride - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

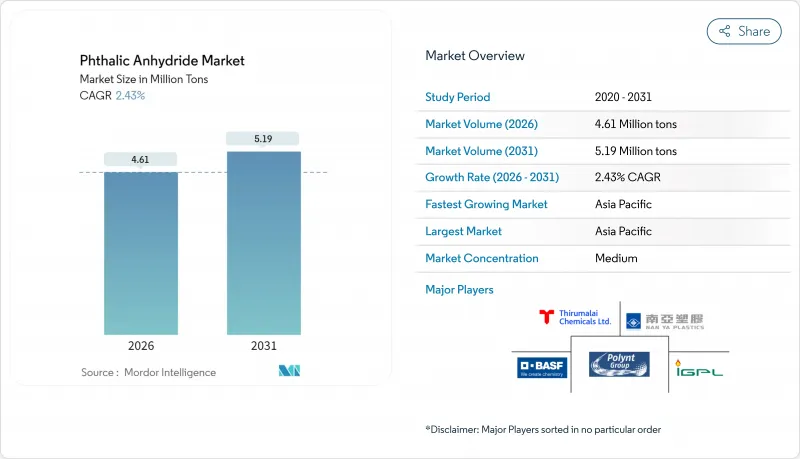

预计到 2026 年,邻苯二甲酐市场规模将达到 461 万吨,高于 2025 年的 450 万吨。预计到 2031 年,市场规模将达到 519 万吨,2026 年至 2031 年的复合年增长率为 2.43%。

这一转型标誌着一个成熟阶段,稳定的下游消费与日益严格的监管审查以及生物基替代品的逐步兴起之间实现了平衡。需求韧性源自于建筑相关的PVC应用、风力发电复合复合材料使用量的增加以及电动车的特殊需求。同时,原料价格波动,尤其是邻二甲苯的价格波动,仍影响生产经济效益,而亚洲产能的成长也持续挤压着全球利润率。因此,竞争策略的核心在于一体化生产、原料柔软性以及加速研发毒性较低的化学品。

全球邻苯二甲酐市场趋势及洞察

亚太地区对PVC建筑材料的需求激增

中国、印度、印尼和越南的建设活动持续推动PVC消费强劲成长,进而提振了对邻苯二甲酸二辛酯及相关酯类塑化剂的需求。中国沿海一体化石化产业集群提供成本效益高的原料供应和下游加工丛集,但持续的供应过剩导致2024年全国平均运转率仅57%。印度生产商,特别是IG Petrochemicals和Thirumalai Chemicals,正在扩大产能以应对国内供不应求和新的出口机会。预计中国2024年将出口约13.1万吨邻邻苯二甲酐,印证了该地区深厚的贸易联繫。 ISO 14001环境标准的逐步加强正促使生产商投资于余热回收和低氮氧化物燃烧器,以维持社会认可。

扩大不饱和聚酯树脂(UPE)在风力发电机叶片的应用

2024年至2025年间风电装置容量的激增带动了对用于玻璃纤维叶片的不饱和聚酯树脂的需求。欧洲的回收示范试验表明,在水泥窑中对废旧叶片进行共处理,既能提供热能,又能回收矿物成分用于水泥熟料生产。这些倡议可望减少预计在2050年累积的4,300万吨叶片废弃物,并维持对下一代风力涡轮机新型树脂的需求。由于邻邻苯二甲酐基树脂系统具有优异的抗疲劳性能,离岸风计划更倾向于使用此类树脂。同时,生物基配方的逐步研发主要仍处于试验阶段。国际能源总署(IEA)「净零排放蓝图」下的政策指引为复合材料原料需求的长期前景提供了支撑。

欧盟和美国基于毒性的邻苯二甲酸酯法规

美国环保署 (EPA) 于 2025 年完成了对邻苯二甲酸二异壬酯 (DINP) 和邻苯二甲酸二异丁酯 (DIDP) 的《有毒物质控制法案》(TSCA)累积评估,指出其在某些喷涂应用中存在不合理的观点。同时,针对邻苯二甲酸丁酯 (BBP)、邻苯二甲酸二(2-乙基己基)酯 (DEHP)、邻苯二甲酸二丁酯 (DBP) 和邻苯二甲酸二异丁酯 (DIBP) 的累积评估草案将引入全面的暴露视角,并可能导致更广泛的监管。在欧盟,欧洲化学品管理局 (ECHA) 的监管需求评估将邻苯二甲酸酐列为 REACH 法规下的限制候选物质,针对某些商用或消费应用。由于监管、替代测试和工人培训的合规成本不断上升,促使柔性聚氯乙烯 (PVC) 混炼商积极检测 1,2-环己烷二羧酸酯和柠檬酸盐。虽然中期需求下降仅限于小众涂料和密封剂领域,但长期的不确定性正在阻碍北美和西欧对新塑化剂线的投资。

细分市场分析

2025年,萘基邻苯二甲酸酐市场需求占比高达83.08%,主要得益于中国高密度煤焦油蒸馏网络和成熟的固定台反应器技术。该领域资本支出优势和供应稳定性使其平均出厂价格比中国当地二甲苯基邻苯二甲酸酐价格低8-10%。因此,儘管有週期性供应过剩,萘基邻苯二甲酸酐装置的运转率仍能维持在80%左右。同时,受中东和北美地区利用炼油产品进行芳烃一体化生产的推动,预计到2031年,邻二甲苯基邻苯二甲酸酐装置的复合年增长率将达到3.28%,超过整个邻邻苯二甲酐市场的成长速度。先进的液相氧化反应器能够降低消费量和废水排放,进而改善环境足迹。

最终,区域供应情况将决定原料的选择。波湾合作理事会(GCC)成员国的生产商正在利用过剩的芳烃重整油,而印度公司则将进口的邻二甲苯与其自身生产的萘结合使用,以规避外汇波动风险。环境法规也是需要考虑的因素。邻二甲苯生产过程产生的焦油废弃物较少,因此更容易符合越南和菲律宾新的危险废弃物法规。

邻苯二甲酐报告按原料(邻二甲苯和萘)、应用(塑化剂、醇酸树脂、不饱和聚酯树脂和其他应用)、终端用户行业(汽车、电气和电子、油漆和涂料、塑胶和其他终端用户行业)以及地区(亚太地区、北美、欧洲、南美以及中东和非洲)进行细分。

区域分析

预计到2025年,亚太地区将占全球整体的61.10%,并在2031年之前以3.02%的复合年增长率成长。中国在山西、陕西和内蒙古的煤化工综合产业园区,以及江苏沿海芳烃联合体,使其拥有无可比拟的成本优势。政府对先进环保法规的激励措施正在推动催化焚烧炉和冷凝水回收装置的维修,进一步降低排放强度。

欧洲面临监管日益严格和成本上升的双重挑战。 REACH法规合规文件和能源价格波动推高了营运成本,并促使小规模独立工厂关闭。BASF计画于2025年对其路德维希港工厂进行精简,便是这一趋势的例证。然而,欧洲仍然是风力涡轮机叶片复合材料的生产中心,并持续支撑着对高规格UPE的需求。北美仍保持着自给自足,专注于特种等级产品,并为墨西哥快速成长的汽车线束产业提供供应。 TSCA政策的不确定性限制了大规模的再投资,但高纯度等级产品和MOF前体等细分市场提供了较高的利润率。在中东和非洲,消费量虽然仍仅占全球总量的一小部分,但正从较低的基数持续成长。沙乌地阿拉伯和阿拉伯联合大公国(阿联酋)正在利用有利的石脑油和芳烃资源,它们在朱拜勒新建的一体化计划还包括安装一套下游邻邻苯二甲酐装置。非洲的需求主要集中在埃及、南非和奈及利亚,这主要得益于基础建设对PVC管道和电缆绝缘层的需求成长。南美洲的需求持续温和成长。巴西从亚洲大量进口UPE作为其PVC和醇酸树脂工厂的原料,而阿根廷正在进军风力涡轮机叶片製造业,预计将推动对UPE的需求。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 亚太地区对PVC建筑材料的需求快速成长

- 扩大UPE在风力发电机叶片中的应用

- 电动汽车电线电缆对塑化剂的需求不断增长

- 亚洲PAN製造商扩大产能(降低成本)

- 采用聚丙烯腈基金属有机框架(MOFs)进行碳捕获、利用与封存(CCUS)

- 市场限制

- 欧盟和美国基于毒性的邻苯二甲酸酯法规

- 生物基无水涂料的广泛应用

- 挥发性邻二甲苯原料价格

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 技术趋势概述

- 定价分析

- 进出口趋势

第五章 市场规模与成长预测

- 按原料

- 邻二甲苯

- 萘

- 透过使用

- 塑化剂

- 醇酸树脂

- 不饱和聚酯树脂

- 其他用途(染料、颜料、杀虫剂等)

- 按最终用户行业划分

- 车

- 电气和电子设备

- 油漆和涂料

- 塑胶

- 其他终端用户产业(化工、农业等)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- AEKYUNG

- BASF

- EMCO Dyestuff

- IG Petrochemicals Ltd.

- Koppers Inc.

- LANXESS

- MITSUBISHI GAS CHEMICAL COMPANY, INC.

- NAN YA PLASTICS CORPORATION

- Paari Chem Resources

- Perstorp

- Polynt SpA

- Shandong Hongxin Chemical Co., Ltd.

- Stepan Company

- Thirumalai Chemicals

- UPC Technology Corporation

第七章 市场机会与未来展望

Phthalic Anhydride market size in 2026 is estimated at 4.61 Million tons, growing from 2025 value of 4.5 Million tons with 2031 projections showing 5.19 Million tons, growing at 2.43% CAGR over 2026-2031.

This trajectory indicates a maturing phase in which steady downstream consumption balances intensifying regulatory oversight and a gradual rise of bio-based substitutes. Demand resilience stems from construction-linked PVC applications, expanding composite use in wind energy, and specialized requirements in electric vehicles. At the same time, production economics remain exposed to feedstock swings, particularly for ortho-xylene, while increased Asian capacity keeps global margins under pressure. Competitive strategies therefore revolve around integrated production footprints, feedstock flexibility, and accelerated innovation in lower-toxicity chemistries.

Global Phthalic Anhydride Market Trends and Insights

Surge in PVC-Based Construction Demand in APAC

Construction activity across China, India, Indonesia, and Vietnam maintains a robust pull on PVC consumption, elevating demand for dioctyl phthalate and related ester plasticizers. Integrated petrochemical complexes in coastal China deliver cost-efficient feedstock and consolidate downstream processing clusters, although countrywide utilization averaged only 57% in 2024 owing to persistent oversupply. Indian producers, notably IG Petrochemicals and Thirumalai Chemicals, are boosting capacity to address local deficit and emerging export prospects. China exported around 131,000 tons of phthalic anhydride in 2024, underscoring deep regional trade ties. Incremental tightening of ISO 14001 environmental requirements is prompting producers to invest in waste-heat recovery and low-NOx burners to sustain social license to operate.

Expansion of UPE Use in Wind-Turbine Blades

Wind-energy installations rose sharply in 2024 and 2025, amplifying demand for unsaturated polyester resins used in glass-fiber blades. European recycling pilots demonstrate that co-processing spent blades in cement kilns can reclaim mineral content for clinker production while supplying thermal energy. Such initiatives mitigate the projected 43 million tons of cumulative blade waste by 2050 and sustain virgin resin needs for next-generation turbines. Offshore projects favor phthalic-anhydride-based resin systems because of proven fatigue resistance, while incremental bio-based formulations remain largely in developmental trials. Policy clarity under the International Energy Agency's net-zero road map supports long-range visibility for composite raw-material demand.

Toxicity-Driven Phthalate Regulations in EU and US

The U.S. EPA finalized TSCA risk evaluations for DINP and DIDP in 2025, citing unreasonable risks in specific spray applications. Parallel draft cumulative assessments covering BBP, DEHP, DBP, and DIBP introduce a holistic exposure lens that may yield broader restrictions. In the European Union, ECHA's Assessment of Regulatory Needs has listed phthalic anhydrides for possible restriction under REACH, targeting certain professional or consumer uses. Compliance costs for monitoring, alternative testing, and worker training are climbing, and formulators of flexible PVC are actively trialing 1,2-cyclohexane dicarboxylic esters and citrates. While mid-term demand erosion is limited to niche coatings and sealants, long-term uncertainty hinders investment in new plasticizer lines in North America and Western Europe.

Other drivers and restraints analyzed in the detailed report include:

- Rising EV Wire-and-Cable Plasticizer Needs

- Adoption of PAN-Based MOFs for CCUS

- Shift Toward Bio-Based Anhydrides in Coatings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Naphthalene supported 83.08% of phthalic anhydride market demand in 2025, buoyed by dense Chinese coal-tar distillation networks and established fixed-bed reactor technology. The segment's CAPEX advantage and supply security underpin average ex-plant costs that trend 8-10% below o-xylene-based production within mainland China. As a result, naphthalene-oriented plants consistently post utilization rates near 80% despite cyclical oversupply. Ortho-xylene, however, is forecast to advance at a 3.28% CAGR through 2031, outpacing overall phthalic anhydride market growth as integrated aromatics complexes in the Middle East and North America capitalize on refinery by-products. Advanced liquid-phase oxidation reactors reduce energy intensity and effluent load, improving environmental footprints.

Regional availability ultimately dictates feedstock choice. Gulf Cooperation Council producers exploit aromatic reformate surplus, whereas Indian players hedge between imported o-xylene and captive naphthalene to cushion forex swings. Environmental regulations are another consideration: o-xylene processes generate lower tar waste streams, easing compliance with emerging hazardous-waste statutes in Vietnam and the Philippines.

The Phthalic Anhydride Report is Segmented by Raw Material (Ortho-Xylene and Naphthalene), Application (Plasticizers, Alkyd Resins, Unsaturated Polyester Resins, and Other Applications), End-User Industry (Automotive, Electrical and Electronics, Paints and Coatings, Plastics, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific controlled 61.10% of global volume in 2025 and will expand at a 3.02% CAGR through 2031. Integrated coal-chemicals parks in Shanxi, Shaanxi, and Inner Mongolia, coupled with coastal aromatics complexes in Jiangsu, give China unmatched cost leadership. Government incentives for advanced environmental controls are spurring retrofits to catalytic incinerators and condensate recovery units, curbing emissions intensity.

Europe confronts regulatory and cost headwinds. REACH dossiers and energy-price volatility lift operating expenses, pushing smaller standalone units toward closure; BASF's Ludwigshafen line rationalization in 2025 is emblematic of this trend. Yet the continent remains central to wind-blade composite production, sustaining demand for high-spec UPE. North America maintains self-sufficiency, focusing on specialty grades and supplying Mexico's burgeoning automotive harness sector. TSCA policy uncertainty tempers large-scale reinvestment, but niche opportunities in high-purity grades and MOF precursors offer higher margins. In the Middle-East and Africa, consumption remains a fraction of global totals but grows off a low base. Saudi Arabia and the UAE leverage advantaged naphtha and aromatics streams, and new integrated projects in Jubail include provision for downstream phthalic anhydride units. African demand centers on Egypt, South Africa, and Nigeria, aligned with PVC pipe and cable-insulation growth for infrastructure initiatives. South America's trajectory stays moderate; Brazil imports bulk volumes from Asia to feed hosting PVC and alkyd resin plants, while Argentina ventures into wind-blade fabrication, creating incremental UPE demand.

- AEKYUNG

- BASF

- EMCO Dyestuff

- IG Petrochemicals Ltd.

- Koppers Inc.

- LANXESS

- MITSUBISHI GAS CHEMICAL COMPANY, INC.

- NAN YA PLASTICS CORPORATION

- Paari Chem Resources

- Perstorp

- Polynt S.p.A.

- Shandong Hongxin Chemical Co., Ltd.

- Stepan Company

- Thirumalai Chemicals

- UPC Technology Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in PVC-Based Construction Demand in APAC

- 4.2.2 Expansion of UPE Use in Wind-Turbine Blades

- 4.2.3 Rising Electric-Vehicle Wire-And-Cable Plasticizer Needs

- 4.2.4 Capacity Expansions by Asian PAN Producers (Lower Costs)

- 4.2.5 Adoption of PAN-Based Metal-Organic Frameworks for CCUS

- 4.3 Market Restraints

- 4.3.1 Toxicity-Driven Phthalate Regulations in EU and US

- 4.3.2 Shift Toward Bio-Based Anhydrides in Coatings

- 4.3.3 Volatile O-Xylene Feedstock Prices

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Technological Snapshot

- 4.7 Pricing Analysis

- 4.8 Import and Export Trends

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Raw Material

- 5.1.1 Ortho-xylene

- 5.1.2 Naphthalene

- 5.2 By Application

- 5.2.1 Plasticizers

- 5.2.2 Alkyd Resins

- 5.2.3 Unsaturated Polyester Resins

- 5.2.4 Other Applications (Dyes and Pigments, Insecticides, etc.)

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Electrical and Electronics

- 5.3.3 Paints and Coatings

- 5.3.4 Plastics

- 5.3.5 Other End-user Industries (Chemicals, Agriculture, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AEKYUNG

- 6.4.2 BASF

- 6.4.3 EMCO Dyestuff

- 6.4.4 IG Petrochemicals Ltd.

- 6.4.5 Koppers Inc.

- 6.4.6 LANXESS

- 6.4.7 MITSUBISHI GAS CHEMICAL COMPANY, INC.

- 6.4.8 NAN YA PLASTICS CORPORATION

- 6.4.9 Paari Chem Resources

- 6.4.10 Perstorp

- 6.4.11 Polynt S.p.A.

- 6.4.12 Shandong Hongxin Chemical Co., Ltd.

- 6.4.13 Stepan Company

- 6.4.14 Thirumalai Chemicals

- 6.4.15 UPC Technology Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

邻苯二甲酐市场规模、份额及成长分析(依生产流程、应用、最终用户及地区划分)-2026-2033年产业预测

邻苯二甲酐市场规模、份额及成长分析(依生产流程、应用、最终用户及地区划分)-2026-2033年产业预测 邻邻苯二甲酐市场依产品等级、纯度、製造流程、应用、终端用户产业及销售管道-2025-2032年全球预测

邻邻苯二甲酐市场依产品等级、纯度、製造流程、应用、终端用户产业及销售管道-2025-2032年全球预测 全球邻邻苯二甲酐市场

全球邻邻苯二甲酐市场 邻苯二甲酐市场报告:2031 年趋势、预测与竞争分析

邻苯二甲酐市场报告:2031 年趋势、预测与竞争分析 邻邻苯二甲酐市场 - 2025 年至 2030 年预测

邻邻苯二甲酐市场 - 2025 年至 2030 年预测 邻邻苯二甲酐市场规模、份额、趋势分析报告:按技术、按应用、按最终用途、按地区、细分市场预测,2024-2030 年

邻邻苯二甲酐市场规模、份额、趋势分析报告:按技术、按应用、按最终用途、按地区、细分市场预测,2024-2030 年 全球邻苯二甲酸酐市场(2016-2036)

全球邻苯二甲酸酐市场(2016-2036) 全球邻苯二甲酐市场 2024-2028

全球邻苯二甲酐市场 2024-2028