|

市场调查报告书

商品编码

1906956

高密度聚苯乙烯(HDPE):市占率分析、产业趋势与统计、成长预测(2026-2031)High-density Polyethylene (HDPE) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

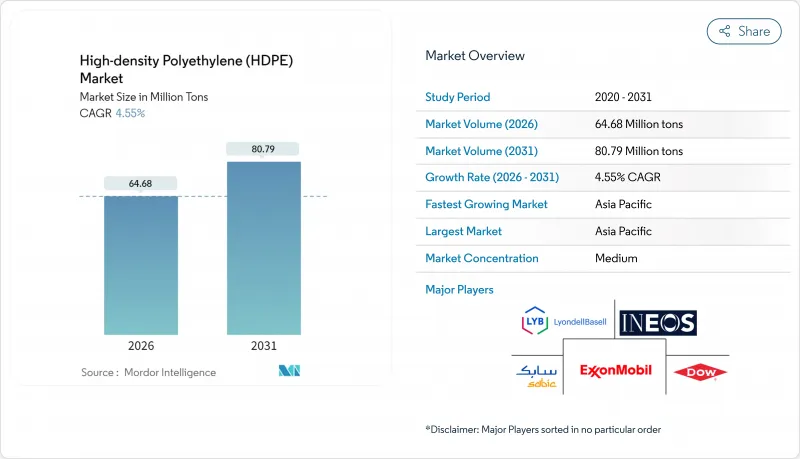

高密度聚苯乙烯(HDPE)市场预计将从 2025 年的 6,187 万吨增长到 2026 年的 6,468 万吨,预计到 2031 年将达到 8,079 万吨,2026 年至 2031 年的复合年增长率为 4.55%。

稳健的基础设施投资、不断扩展的化学回收供应链以及氢兼容管道系统的日益普及,都为这一增长轨迹提供了支撑。此外,由于高密度聚苯乙烯)材料固有的耐久性、耐化学性和可回收性,终端使用者对其解决方案持续保持浓厚的兴趣。印度和东南亚国协加速推动社会住宅计画、食品级吹塑成型成型技术在电子商务配送领域的应用,以及用于低碳天然气网的PE-100-RC管道网路的推广,都促进了HDPE潜在需求的成长。化学回收商将混合废弃物流转化为原生级再生HDPE(rHDPE),从而增强了供应安全,缓解了原材料价格波动,并支持了循环经济的需求。儘管竞争格局仍然较为分散,但将裂解装置与先进回收技术结合的垂直整合型製造商,在成本和永续性方面都保持优势。

全球高密度聚苯乙烯(HDPE)市场趋势及展望

水利基础设施维修计画中对承压和非承压塑胶管道的需求不断增长

由于HDPE管道拥有长达百年的使用寿命,且可采用非开挖施工,从而降低30-40%的土木工程成本,因此供水管网现代化计划优先选用HDPE管道。美国土木工程师协会强调了HDPE在老化输水管中的耐腐蚀性。印度自2024年起强制实施的全新聚乙烯品质标准将进一步提升HDPE在关键供水应用中的可靠性。计划设计人员青睐HDPE,因为柔软性,能够适应地基移动,从而降低洩漏风险。公共部门的资金筹措週期跨越多个五年计划,确保了管道需求的稳定,进而保证了HDPE市场的可预测成长。此外,非开挖施工方法的应用进一步降低了总安装成本,使HDPE在与混凝土和球墨铸铁管道的竞争中脱颖而出。

食品级吹塑成型包装在新兴电商通路的拓展

电子商务的快速发展对包装提出了更高的要求,即包装必须能够承受复杂的物流环境并保障食品品质。食品级高密度聚乙烯(HDPE)容器已通过严格的迁移测试并获得美国食品药物管理局(FDA)的批准,成为乳製品、调味品和常温饮料的首选包装。欧盟将于2025年3月生效的新规将要求食品接触塑胶具备全面的可追溯性,但HDPE生产商目前已达到这些标准。透过薄壁吹塑成型实现轻量化,减少了树脂用量,帮助企业实现排放目标并维持市场需求,从而增强了HDPE市场的韧性。

加强对一次性塑胶的监管和课税

包装法规的收紧正在降低欧洲和北美部分地区对一次性高密度聚乙烯(HDPE)产品的需求。然而,HDPE的可回收性降低了其在多次使用应用中的政策风险,而且完善的回收系统使其相比没有机械回收途径的多层薄膜更具吸引力。加工商正在重新设计瓶盖和分配系统,以符合重量限制,从而减少体积损失。因此,法规只是减缓而非逆转了HDPE市场的成长。

细分市场分析

到2025年,片材和薄膜将占高密度聚乙烯(HDPE)市场份额的40.65%,这主要得益于稳定的包装需求以及下游加工商对吹膜工艺日益熟练的掌握。永续包装的目标正在推动单一材料薄膜设计的发展,而HDPE薄膜优于混合聚合物薄膜。

儘管管道和管材在HDPE市场中所占比例小规模,但预计在2026年至2031年间,其复合年增长率将达到6.07%,成为该细分市场中成长最快的领域。这主要得益于供水基础设施维修、氢气天然气管网建设以及非开挖式翻新工程的推动。日益严格的洩漏损失罚款公共产业采用具有均质焊接接头和百年使用寿命的HDPE管道。工业薄膜、地工止水膜和手提袋等产品完善了HDPE产品组合,在建筑支出放缓的情况下,支撑了树脂的基准需求。

高密度聚苯乙烯(HDPE) 市场报告按应用(管道和管材、板材和薄膜、硬质产品、其他应用)、树脂等级(PE-80、PE-100、PE-100-RC、其他)、最终用户行业(包装、建筑和施工、农业、运输、电气和电子等)以及地区(亚太地区、北美、欧洲、南美、中东和电子等)以及地区(亚太地区、北美、欧洲、欧洲和中东地区)。

区域分析

亚太地区预计到2025年将占据全球高密度聚乙烯(HDPE)市场42.30%的份额,并预计到2031年将以5.55%的复合年增长率增长,这主要得益于中国下游薄膜出口的增长和印度基础设施建设的蓬勃发展。该地区的综合生产商受益于煤製烯烃转化和石脑油裂解装置的柔软性,从而能够缓解乙烯价格的波动。然而,供应过剩时期给区域利润率带来了压力,导致需要进行计划性维护以减少库存。

北美高密度聚乙烯(HDPE)市场受益于以乙烷为主的原料供应以及化学回收领域投资热潮带来的再生树脂供应成长。儘管其成长速度低于亚太地区,但对高附加价值管道、薄膜和医用级产品的需求支撑着市场收入。

欧洲是一个政策主导,随着氢能网路的扩展,高密度聚乙烯(HDPE)正被用于PE-100-RC管道计划和化学品回收合作项目中,以确保可回收原材料的供应。儘管由于禁止使用一次性塑胶的政策,对薄壁硬质包装的需求正在下降,但HDPE凭藉其高可回收性,在可重复使用、可回收的包装箱和化学品桶领域仍然占据着重要地位。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 水利基础设施维修计画中对承压和非承压塑胶管道的需求不断增长

- 食品级吹塑成型包装在新兴电商通路的拓展

- 东南亚国协和印度持续投入公共住宅和大量基础建设。

- 氢气天然气网的部署需要PE-100-RC管道

- 化学回收厂将混合废弃物流转化为原生级 RHDPE。

- 市场限制

- 加强对一次性塑胶的监管和课税

- 乙烯原料价格波动与原油价格相关

- 加速消费品硬质包装材料向聚丙烯(PP)无规共聚物的转化

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

第五章 市场规模与成长预测

- 透过使用

- 管道和管材

- 片材和薄膜

- 硬产品

- 其他用途

- 依树脂等级

- PE-80

- PE-100

- PE-100-RC

- 超高分子量聚乙烯(HDPE)

- 按最终用户行业划分

- 包装

- 建筑/施工

- 农业

- 运输

- 电气和电子设备

- 工业机械

- 其他终端用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ASEAN

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- BASF

- Borealis AG

- Braskem

- Chevron Phillips Chemical

- Dow

- Exxon Mobil Corporation

- Formosa Plastics Corporation, USA

- Indian Oil Corporation

- INEOS

- LG Chem

- LyondellBasell Industries Holdings BV

- Mitsui Chemicals, Inc.

- NOVA Chemicals Corporate

- PTT Global Chemical Public Company Limited

- Qatar Chemical Company Ltd

- Reliance Industries Limited

- SABIC

- Sasol

- Sinopec

- TotalEnergies

- Westlake Corporation

第七章 市场机会与未来展望

The High-density Polyethylene (HDPE) market is expected to grow from 61.87 Million tons in 2025 to 64.68 Million tons in 2026 and is forecast to reach 80.79 Million tons by 2031 at 4.55% CAGR over 2026-2031.

Strong infrastructure spending, widening chemical-recycling supply chains, and rising adoption of hydrogen-ready pipe systems anchor this trajectory, while the material's intrinsic durability, chemical resistance, and recyclability keep end-users committed to high-density polyethylene solutions. Accelerated public-housing programs across India and ASEAN, expanding food-grade blow-molding in e-commerce distribution, and the rollout of PE-100-RC pipe networks for low-carbon gas grids collectively widen the HDPE market's addressable demand. Chemical recyclers diverting mixed-waste streams into virgin-grade rHDPE strengthen supply security, temper feedstock volatility, and reinforce circular-economy mandates. Moderately fragmented competition persists, yet vertically integrated producers that pair cracker capacity with advanced recycling retain cost and sustainability advantages.

Global High-density Polyethylene (HDPE) Market Trends and Insights

Rising Demand for Pressure and Non-Pressure Plastic Pipes in Water-Infrastructure Retrofit Programmes

Water-network modernisation projects prioritise HDPE pipes because they combine a 100-year service life with trenchless installation capability that cuts civil works costs by 30-40%. The American Society of Civil Engineers underscores HDPE's corrosion resistance for ageing distribution lines. India's 2024 quality-standard mandate for virgin polyethylene reinforces material integrity in critical water applications. Project designers favour HDPE because its flexibility accommodates ground movement, reducing leakage risk. Public-sector funding cycles spanning multiple five-year plans guarantee steady pipe volumes, ensuring predictable growth for the HDPE market. Integration of trenchless methods further differentiates HDPE from concrete and ductile-iron alternatives by lowering total installed costs.

Expansion of Food-Grade Blow-Molded Packaging in Emerging E-Commerce Channels

Rapid e-commerce penetration demands packaging that survives complex logistics while protecting food quality. Food-grade HDPE containers pass stringent migration tests and hold FDA clearance, making them default choices for dairy, condiments, and shelf-stable beverages. European Union regulations, effective March 2025, require extensive traceability for food-contact plastics, a standard that HDPE producers already meet. Weight-reduction via thin-wall blow-molding lowers resin usage, aligns with corporate emission targets, and sustains demand, reinforcing the HDPE market's resilience.

Escalating Anti-Single-Use-Plastic Regulations and Taxation

Tighter packaging rules compress demand for disposable HDPE articles in Europe and parts of North America. However, HDPE's recyclability mitigates policy risk in multi-use applications, and well-established collection streams preserve its appeal versus multi-layer films that lack mechanical-recycling pathways. Converters are redesigning closures and dispensing systems to remain within weight thresholds, limiting volume loss. Consequently, regulation restrains but does not reverse HDPE market growth.

Other drivers and restraints analyzed in the detailed report include:

- Sustained Public-Housing and Mega-Infrastructure Spend Across ASEAN and India

- Roll-out of Hydrogen-Ready Gas Grids Requiring PE-100-RC Pipes

- Volatile Crude-Oil-Linked Ethylene Feedstock Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sheets and Films held 40.65% of the 2025 HDPE market share, underpinned by steady packaging demand and downstream converter familiarity with blown-film processes. Sustainable packaging targets stimulate mono-material film designs that favour HDPE over mixed polymers.

Pipes and Tubes, although a smaller slice of the HDPE market size, posted the sharpest 6.07% CAGR for 2026-2031 on the back of water-infrastructure retrofits, hydrogen-ready gas grids, and trenchless renewals. Rising leak-loss penalties push utilities toward HDPE piping thanks to its homogenous fusion joints and 100-year service life. Industrial films, geomembranes, and carrier bags round out the portfolio, sustaining baseline resin offtake when construction spending softens.

The High-Density Polyethylene (HDPE) Market Report is Segmented by Application (Pipes and Tubes, Sheets and Films, Rigid Articles, and Other Applications), Resin Grade (PE-80, PE-100, PE-100-RC, and More), End-User Industry (Packaging, Building and Construction, Agriculture, Transportation, Electrical and Electronics, and More), and Geography ( Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific controlled 42.30% of the 2025 HDPE market share and is forecast to record a 5.55% CAGR to 2031, propelled by Chinese downstream film exports and India's infrastructure boom. Integrated producers in the region benefit from coal-to-olefins and naphtha-cracker flexibility, buffering ethylene volatility. However, oversupply periods have compressed regional margins, prompting scheduled maintenance to balance inventories.

North America's HDPE market benefits from ethane-advantaged feedstock and a wave of chemical-recycling investments that elevate circular-resin availability. While growth rates are lower than Asia-Pacific, value-added pipe, film, and medical-grade demand sustains profit pools.

Europe remains policy-driven; its hydrogen-network build-out channels HDPE into PE-100-RC pipe projects and chemical-recycling alliances that secure recycled feedstock. Anti-single-use-plastic mandates depress thin-wall rigid packaging volumes, yet high recyclability keeps HDPE firmly in multi-use, returnable crates and chemical drums.

- BASF

- Borealis AG

- Braskem

- Chevron Phillips Chemical

- Dow

- Exxon Mobil Corporation

- Formosa Plastics Corporation, U.S.A.

- Indian Oil Corporation

- INEOS

- LG Chem

- LyondellBasell Industries Holdings B.V.

- Mitsui Chemicals, Inc.

- NOVA Chemicals Corporate

- PTT Global Chemical Public Company Limited

- Qatar Chemical Company Ltd

- Reliance Industries Limited

- SABIC

- Sasol

- Sinopec

- TotalEnergies

- Westlake Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Pressure and Non-Pressure Plastic Pipes in Water-Infrastructure Retrofit Programmes

- 4.2.2 Expansion of Food?Grade Blow-Moulded Packaging in Emerging E-Commerce Channels

- 4.2.3 Sustained Public-Housing and Mega-Infrastructure Spend across ASEAN and India

- 4.2.4 Roll-Out of Hydrogen-Ready Gas Grids Requiring PE-100-RC Pipes

- 4.2.5 Chemical Recycling Plants Shifting Mixed-Waste Streams into Virgin-Grade RHDPE

- 4.3 Market Restraints

- 4.3.1 Escalating Anti-Single-Use-Plastic Regulations and Taxation

- 4.3.2 Volatile Crude-Oil-Linked Ethylene Feedstock Pricing

- 4.3.3 Accelerated Materials-Switch to PP Random Copolymers in Consumer Rigid Packaging

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Application

- 5.1.1 Pipes and Tubes

- 5.1.2 Sheets and Films

- 5.1.3 Rigid Articles

- 5.1.4 Other Applications

- 5.2 By Resin Grade

- 5.2.1 PE-80

- 5.2.2 PE-100

- 5.2.3 PE-100-RC

- 5.2.4 Ultra-High-Molecular-Weight HDPE

- 5.3 By End-User Industry

- 5.3.1 Packaging

- 5.3.2 Building and Construction

- 5.3.3 Agriculture

- 5.3.4 Transportation

- 5.3.5 Electrical and Electronics

- 5.3.6 Industrial Machinery

- 5.3.7 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF

- 6.4.2 Borealis AG

- 6.4.3 Braskem

- 6.4.4 Chevron Phillips Chemical

- 6.4.5 Dow

- 6.4.6 Exxon Mobil Corporation

- 6.4.7 Formosa Plastics Corporation, U.S.A.

- 6.4.8 Indian Oil Corporation

- 6.4.9 INEOS

- 6.4.10 LG Chem

- 6.4.11 LyondellBasell Industries Holdings B.V.

- 6.4.12 Mitsui Chemicals, Inc.

- 6.4.13 NOVA Chemicals Corporate

- 6.4.14 PTT Global Chemical Public Company Limited

- 6.4.15 Qatar Chemical Company Ltd

- 6.4.16 Reliance Industries Limited

- 6.4.17 SABIC

- 6.4.18 Sasol

- 6.4.19 Sinopec

- 6.4.20 TotalEnergies

- 6.4.21 Westlake Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

高密度均聚物市场:依通路、加工技术、应用类型、产品等级及最终用途产业划分-全球预测,2026-2032年

高密度均聚物市场:依通路、加工技术、应用类型、产品等级及最终用途产业划分-全球预测,2026-2032年 2026年全球高密度聚苯乙烯管道市场报告2026年全球高密度聚苯乙烯(HDPE)瓶市场报告2026年全球高密度聚苯乙烯市场报告2026年全球高密度聚苯乙烯(HDPE)防漏地工止水膜市场报告

2026年全球高密度聚苯乙烯管道市场报告2026年全球高密度聚苯乙烯(HDPE)瓶市场报告2026年全球高密度聚苯乙烯市场报告2026年全球高密度聚苯乙烯(HDPE)防漏地工止水膜市场报告 2025-2029年全球高密度聚苯乙烯(HDPE)市场

2025-2029年全球高密度聚苯乙烯(HDPE)市场 先进高密度聚乙烯树脂市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2026-2033 年)高密度聚苯乙烯市场(按类型、应用和分销管道)—2025-2032 年全球预测

先进高密度聚乙烯树脂市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2026-2033 年)高密度聚苯乙烯市场(按类型、应用和分销管道)—2025-2032 年全球预测 高密度聚苯乙烯(HDPE)包装市场-2025年至2030年的预测

高密度聚苯乙烯(HDPE)包装市场-2025年至2030年的预测 高密度聚苯乙烯的印度市场:各流程,各用途,各最终用途产业,各地区,机会,预测(2019年度~2033年度)

高密度聚苯乙烯的印度市场:各流程,各用途,各最终用途产业,各地区,机会,预测(2019年度~2033年度)