|

市场调查报告书

商品编码

1906992

聚酰亚胺(PI):市场占有率分析、产业趋势与统计、成长预测(2026-2031)Polyimides (PI) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

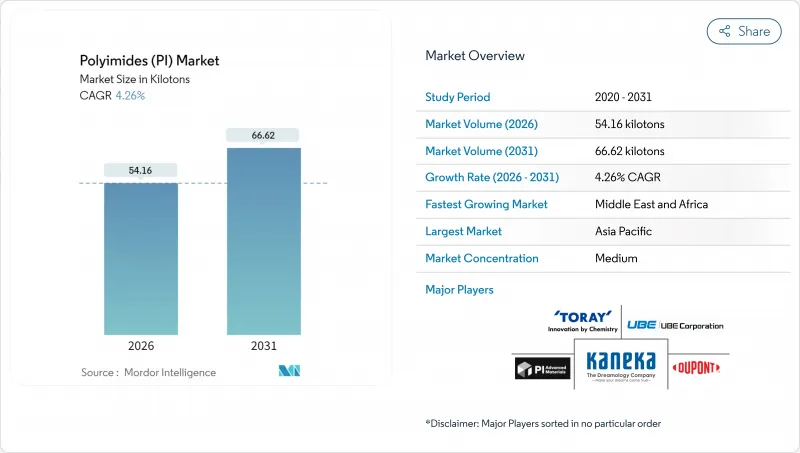

预计聚酰亚胺(PI)市场将从2025年的51.95千吨成长到2026年的54.16千吨,预计到2031年将达到66.62千吨,2026年至2031年的复合年增长率为4.26%。

高性能应用领域的持续需求支撑着这一成长趋势。先进封装技术,特别是高频宽记忆体堆迭和异构集成,使得聚酰亚胺薄膜在层间介质和应力缓衝层设计中继续占据核心地位。电动车动力传动系统的电气化程度不断提高,推动了基本客群的成长,因为800V系统因其介电稳定性而青睐聚酰亚胺介质。其低损耗角正切值能够保持毫米波频段的讯号完整性,从而加速了其在5G和早期6G基础设施中的应用。航太领域的商业化也是一个新的成长要素,聚酰亚胺被指定用于製造轻质绝缘毯,以确保其在极端温度下的耐久性。

全球聚酰亚胺(PI)市场趋势与洞察

电子设备的微型化和折迭式显示器的快速发展

在对更轻薄行动装置日益增长的需求推动下,聚酰亚胺基板对于下一代柔性电路和折迭式显示器至关重要。三星的测试证实,该薄膜在半径小于 1.4 毫米的情况下可承受超过 20 万次折迭而不会产生光学畸变。汽车驾驶座也利用聚酰亚胺的柔软性,采用可在 -40°C 至 150°C 温度范围内安全运行的曲面 OLED 面板。基于晶片组的半导体封装也受益于该材料,因为其低热膨胀係数能够吸收机械应力,避免脆性介电材料开裂。随着外形规格的不断创新,聚酰亚胺 (PI) 市场正经历着来自设计人员的强劲需求,他们对热稳定性和尺寸稳定性有着极高的要求。

电动车高压绝缘材料需求激增

电动车平台目前的工作电压超过 800V,远超传统绝缘材料的安全极限。聚酰亚胺薄膜的介电强度超过 250kV/mm,并且在 -40°C 至 200°C 的温度范围内经历 1000 次热循环后仍能保持其完整性。特斯拉正在其驱动马达中整合聚酰亚胺涂层铜绕组,以减少局部放电故障。向碳化硅逆变器的过渡(碳化硅逆变器的工作温度高于硅)进一步凸显了对耐高温聚合物封装的需求。随着电池容量的扩大,聚酰亚胺屏障也被应用于热失控抑制系统中,增强了聚酰亚胺市场的长期成长前景。

溶剂浇铸中遵守VOC排放法规的成本

欧洲工业排放指令基准值和加州南海岸空气品质管理区 (SCAQMD) 的规定将挥发性有机化合物 (VOC) 的排放限制在 20 mg/m³。使用N-甲基吡咯烷酮的溶剂浇铸聚酰亚胺生产线需要安装再生式热氧化器 (RTO),每条生产线的成本高达数百万美元。由于投资回收期超过五年,人们开始转向水基酰亚胺化学。然而,儘管环境问题迫在眉睫,水基酰亚胺的产量比率仍然很低,限制了其快速普及。

细分市场分析

到2025年,电气和电子应用将占聚酰亚胺(PI)市场份额的36.42%,这印证了该材料在柔性印刷电路和半导体封装领域的悠久历史。随着晶片级架构的普及(这种架构依靠薄膜来增加互连层),预计该领域的收入将持续成长。汽车产业的需求主要来自电动车马达绝缘材料和电池隔热材料。工业机械产业重视高温密封剂的耐化学腐蚀性能,而航太产业则需要耐辐射层压材料。

其他终端用户产业虽然规模较小,但预计成长速度更快,复合年增长率将达到5.18%,到2031年将为聚酰亚胺市场贡献超过15.6千吨。值得关注的成长领域包括建筑规范强制要求使用阻燃建筑幕墙系统,以及医疗设备製造商采用耐灭菌聚合物。随着这些应用的成熟,它们对家用电子电器的依赖性将降低,从而降低聚酰亚胺整体市场的周期性风险。

聚酰亚胺市场报告按终端用户产业(汽车、电气电子、包装、工业机械、航太、建筑及其他终端用户产业)、形态(薄膜、树脂、纤维及其他)和地区(亚太地区、北美、欧洲、南美、中东和非洲)进行细分。市场预测以数量(吨)和价值(美元)为单位。

区域分析

到2025年,亚太地区将占全球需求的40.55%,并将继续保持柔性PCB製造和折迭式显示器组装的中心地位。中国在规模方面贡献巨大,而日本正在完善超低缺陷化学技术,以供应半导体后端封装企业。韩国领先的显示器企业保持大规模的产能。马来西亚等东南亚国家正在吸收跨国电子集团的转移投资,从而加强支撑聚酰亚胺市场的区域丛集。

北美市场成长稳定但幅度不大。该地区在航太和国防计划领域占据主导地位,在这些项目中,经飞行认证的薄膜价格通常是普通产品的三倍。高速网路部署正在刺激当地对层压板的需求。联邦政府对国内半导体工厂的激励措施预计将进一步推动对树脂的需求,但特种聚合物加工人才短缺限制了市场的快速扩张。

欧洲的前景与北美类似。聚酰亚胺绝缘材料被应用于汽车电气化和海上风力发电机逆变器,但能源价格上涨和严格的挥发性有机化合物(VOC)法规推高了改造成本。政策制定者正在考虑采取措施,透过补贴新增产能来建立自给自足的供应链,但预计在可预见的未来,欧洲仍将依赖进口。

中东和非洲地区虽然目前绝对吨位小规模,但正以6.05%的复合年增长率成长,这主要得益于海湾国家向高科技製造业的多元化发展。大型资料中心和5G部署需要高频PCB,而聚酰亚胺芯材是其主要需求。基础设施现代化也促使电缆製造商采用耐高温绝缘材料。儘管投资框架尚不成熟,该地区主要依赖进口原料,目前正与亚洲化工集团探讨合资事宜。预计在预测期内,聚酰亚胺市场将建立试点生产线以满足区域需求。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电子设备的微型化和折迭式显示器的蓬勃发展

- 电动车高压绝缘材料需求激增

- 采用5G/6G高频印刷电路基板

- 在太空中扩展轻型隔热罩

- 中国主导的产能扩张正在降低价格壁垒

- 市场限制

- 易挥发性二酐及二胺原料价格波动;

- 溶剂浇铸製程中挥发性有机化合物 (VOC)排放法规合规成本

- 东亚以外地区的加工技术差距

- 价值链分析

- 波特五力模型

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 法律规范

- 阿根廷

- 澳洲

- 巴西

- 加拿大

- 中国

- EU

- 印度

- 日本

- 马来西亚

- 墨西哥

- 奈及利亚

- 俄罗斯

- 沙乌地阿拉伯

- 南非

- 韩国

- 阿拉伯聯合大公国

- 英国

- 美国

- 终端用户产业趋势

- 航太(航太零件生产收入)

- 汽车(汽车生产)

- 建筑与施工(新增建筑面积)

- 电气电子设备(电气电子设备生产收入)

- 包装(塑胶包装数量)

第五章 市场规模和成长预测(价值和数量)

- 按最终用户行业划分

- 车

- 电气和电子设备

- 包装

- 工业和机械

- 航太

- 建筑/施工

- 其他终端用户产业

- 按形式

- 电影

- 树脂

- 纤维

- 其他的

- 按地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 马来西亚

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 法国

- 义大利

- 英国

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 奈及利亚

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Arakawa Chemical Industries,Ltd.

- Arkema

- China Wanda Group

- DUNMORE

- DuPont

- JIAOZUO TIANYI TECHNOLOGY CO.,LTD

- Kaneka Corporation

- Kolon Industries Inc.

- Mitsui Chemicals Inc.

- PI Advanced Materials Co., Ltd.

- Shenzhen Ruihuatai Film Technology Co., Ltd.

- SKC

- Taimide Tech. Inc.

- Toray Industries Inc

- UBE Corporation

第七章 市场机会与未来展望

第八章:执行长面临的关键策略挑战

The Polyimides market is expected to grow from 51.95 kilotons in 2025 to 54.16 kilotons in 2026 and is forecast to reach 66.62 kilotons by 2031 at 4.26% CAGR over 2026-2031.

Persistent demand from high-performance applications underpins this trajectory. Advanced semiconductor packaging, notably high-bandwidth memory stacks and heterogeneous integration, keeps polyimide films at the center of interlayer dielectric and stress-buffer designs. Electric-vehicle power-train electrification is widening the customer base as 800 V systems favor polyimide dielectrics for insulation stability. Adoption in 5G and early 6G infrastructure is accelerating because low-loss tangent values preserve signal integrity at millimeter-wave frequencies. Space-sector commercialization adds another growth vector as lightweight thermal blankets specify polyimides for durability under extreme temperatures.

Global Polyimides (PI) Market Trends and Insights

Electronics Miniaturization and Foldable-Display Boom

Demand for thinner, lighter portable devices has made polyimide substrates indispensable for next-generation flexible circuits and foldable displays. Samsung testing shows films survive more than 200,000 folds at radii down to 1.4 mm without optical distortion. Automotive cockpits are adopting curved OLED panels that operate safely between -40 °C and 150 °C, again relying on polyimide flexibility. Chiplet-based semiconductor packages likewise benefit because the material's low coefficient of thermal expansion absorbs mechanical stresses that would crack brittle dielectrics. As form-factor innovation continues, the polyimides market gains resilient demand from designers that cannot compromise on thermal or dimensional stability.

EV High-Voltage Insulation Demand Surge

Electric-vehicle platforms now operate above 800 V, pushing traditional insulation materials beyond safe limits. Polyimide films provide dielectric strengths exceeding 250 kV mm-1 and retain that integrity after 1,000 thermal cycles between -40 °C and 200 °C. Tesla integrates polyimide-wrapped copper windings to mitigate partial-discharge failures in traction motors. The shift to silicon-carbide inverters, which run hotter than silicon, further entrenches the need for high-temperature polymer packaging. As battery capacities scale, thermal runaway containment systems also specify polyimide barriers, enhancing long-term growth prospects for the polyimides market.

VOC-Emission Compliance Costs for Solvent Casting

Industrial Emissions Directive thresholds in Europe and SCAQMD rules in California cap volatile organic compound emissions at 20 mg m-3. Solvent-cast polyimide lines using N-methyl-2-pyrrolidone must therefore install regenerative thermal oxidizers costing several million dollars per line. Payback stretches beyond five years, prompting a shift toward water-based imide chemistries. However, production yields remain lower, restraining rapid adoption despite environmental urgency.

Other drivers and restraints analyzed in the detailed report include:

- 5G/6G High-Frequency PCB Adoption

- Space-Sector Lightweight Thermal Shielding Expansion

- Processing Skill Gap Outside East Asia

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electrical and electronics applications commanded 36.42% of the polyimides market share in 2025, underscoring the material's historical role in flexible printed circuits and semiconductor packaging. Revenues here will keep expanding as chiplet architectures multiply interconnect layers that rely on thin films. Automotive follows, propelled by electric-vehicle motor insulation and battery thermal barriers. Industrial machinery values chemical resistance in high-temperature seals, while aerospace relies on radiation-resistant laminates.

Other end-user industries accounted for a smaller but faster-growing slice, posting a 5.18% CAGR that will push their contribution to the polyimides market size above 15.6 kilotons by 2031. Building-construction codes specifying flame-retardant facade systems and medical-device makers adopting sterilization-resistant polymers are two visible frontiers. As these applications mature, dependency on consumer electronics will dilute, lowering cyclical risk for the wider polyimides market.

The Polyimides Report is Segmented by End User Industry (Automotive, Electrical and Electronics, Packaging, Industrial and Machinery, Aerospace, Building and Construction, and Other End-User Industries), Form (Film, Resin, Fiber, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons) and Value (USD).

Geography Analysis

Asia-Pacific anchored 40.55% of global demand in 2025 and remains the epicenter of flexible-PCB fabrication and foldable-display assembly. China contributes scale, while Japan perfects ultra-low-defect chemistries that feed semiconductor back-end packaging houses. South Korea's display giants sustain large captive consumption. Southeast Asian nations such as Malaysia are absorbing relocation investment from multinational electronics groups, strengthening the regional cluster that underwrites the polyimides market.

North America shows steady but less spectacular volume growth. The region excels in aerospace and defense projects, where flight-qualified films priced at triple commodity levels are commonplace. High-speed network deployments are stimulating local laminate demand. Federal incentives for domestic semiconductor fabs should spur incremental resin off-take, yet talent shortages in specialty polymer processing temper rapid expansion.

Europe's outlook mirrors that of North America. Automotive electrification and offshore wind-turbine inverters adopt polyimide insulation, yet energy prices and stringent VOC rules raise conversion costs. Policymakers are weighing supply-chain autonomy measures that could subsidize new capacity, but near-term reliance on imports persists.

The Middle East and Africa, presently small in absolute tonnage, advances at a 6.05% CAGR as Gulf states diversify into high-tech manufacturing. Large-scale data centers and 5G rollouts demand high-frequency PCBs that favor polyimide cores, and infrastructure modernization pushes cable manufacturers to specify higher-temperature insulations. Investment frameworks remain nascent, so most material is imported, though joint ventures with Asian chemical groups are under negotiation. Over the forecast horizon, the polyimides market may see pilot lines established to tap regional demand.

- Arakawa Chemical Industries,Ltd.

- Arkema

- China Wanda Group

- DUNMORE

- DuPont

- JIAOZUO TIANYI TECHNOLOGY CO.,LTD

- Kaneka Corporation

- Kolon Industries Inc.

- Mitsui Chemicals Inc.

- PI Advanced Materials Co., Ltd.

- Shenzhen Ruihuatai Film Technology Co., Ltd.

- SKC

- Taimide Tech. Inc.

- Toray Industries Inc

- UBE Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electronics miniaturisation and foldable-display boom

- 4.2.2 EV high-voltage insulation demand surge

- 4.2.3 5 G/6 G high-frequency PCB adoption

- 4.2.4 Space-sector lightweight thermal shielding expansion

- 4.2.5 China-led capacity additions lowering price barriers

- 4.3 Market Restraints

- 4.3.1 Volatile dianhydride and diamine feedstock pricing

- 4.3.2 VOC-emission compliance costs for solvent casting

- 4.3.3 Processing skill gap outside East Asia

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Regulatory Framework

- 4.6.1 Argentina

- 4.6.2 Australia

- 4.6.3 Brazil

- 4.6.4 Canada

- 4.6.5 China

- 4.6.6 European Union

- 4.6.7 India

- 4.6.8 Japan

- 4.6.9 Malaysia

- 4.6.10 Mexico

- 4.6.11 Nigeria

- 4.6.12 Russia

- 4.6.13 Saudi Arabia

- 4.6.14 South Africa

- 4.6.15 South Korea

- 4.6.16 United Arab Emirates

- 4.6.17 United Kingdom

- 4.6.18 United States

- 4.7 End-use Sector Trends

- 4.7.1 Aerospace (Aerospace Component Production Revenue)

- 4.7.2 Automotive (Automobile Production)

- 4.7.3 Building and Construction (New Construction Floor Area)

- 4.7.4 Electrical and Electronics (Electrical and Electronics Production Revenue)

- 4.7.5 Packaging(Plastic Packaging Volume)

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By End User Industry

- 5.1.1 Automotive

- 5.1.2 Electrical and Electronics

- 5.1.3 Packaging

- 5.1.4 Industrial and Machinery

- 5.1.5 Aerospace

- 5.1.6 Building and Construction

- 5.1.7 Other End-user Industries

- 5.2 By Form

- 5.2.1 Film

- 5.2.2 Resin

- 5.2.3 Fiber

- 5.2.4 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 Australia

- 5.3.1.6 Malaysia

- 5.3.1.7 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 Italy

- 5.3.3.4 United Kingdom

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Nigeria

- 5.3.5.4 South Africa

- 5.3.5.5 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Arakawa Chemical Industries,Ltd.

- 6.4.2 Arkema

- 6.4.3 China Wanda Group

- 6.4.4 DUNMORE

- 6.4.5 DuPont

- 6.4.6 JIAOZUO TIANYI TECHNOLOGY CO.,LTD

- 6.4.7 Kaneka Corporation

- 6.4.8 Kolon Industries Inc.

- 6.4.9 Mitsui Chemicals Inc.

- 6.4.10 PI Advanced Materials Co., Ltd.

- 6.4.11 Shenzhen Ruihuatai Film Technology Co., Ltd.

- 6.4.12 SKC

- 6.4.13 Taimide Tech. Inc.

- 6.4.14 Toray Industries Inc

- 6.4.15 UBE Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

8 Key Strategic Questions for CEOs

聚酰亚胺泡棉市场分析与预测(至2035年):类型、产品类型、技术、应用、材料类型、最终用户、组件、安装类型、解决方案

聚酰亚胺泡棉市场分析与预测(至2035年):类型、产品类型、技术、应用、材料类型、最终用户、组件、安装类型、解决方案 改质聚酰亚胺市场按应用产业、最终用途、产品类型、形式和技术划分-2026-2032年全球预测聚酰亚胺树脂市场按应用、终端用途产业、形态和製造流程划分-2026年至2032年全球预测螺旋缠绕聚酰亚胺管材市场:按最终用途产业、产品类型、应用和销售管道- 全球预测(2026-2032年)

改质聚酰亚胺市场按应用产业、最终用途、产品类型、形式和技术划分-2026-2032年全球预测聚酰亚胺树脂市场按应用、终端用途产业、形态和製造流程划分-2026年至2032年全球预测螺旋缠绕聚酰亚胺管材市场:按最终用途产业、产品类型、应用和销售管道- 全球预测(2026-2032年) 聚酰亚胺市场-2026-2031年预测

聚酰亚胺市场-2026-2031年预测 聚酰亚胺清漆市场规模、份额及成长分析(按类型、终端用户产业、应用及地区划分)-2026-2033年产业预测

聚酰亚胺清漆市场规模、份额及成长分析(按类型、终端用户产业、应用及地区划分)-2026-2033年产业预测 热塑性聚酰亚胺市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2025-2033 年)

热塑性聚酰亚胺市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2025-2033 年) 聚酰亚胺清漆:全球市占率及排名、总收入及需求预测(2025-2031年)聚酰亚胺(PI)-全球市占率及排名、总收入及需求预测(2025-2031年)光敏聚酰亚胺(PSPI):全球市场份额和排名、总销售额和需求预测(2025-2031 年)

聚酰亚胺清漆:全球市占率及排名、总收入及需求预测(2025-2031年)聚酰亚胺(PI)-全球市占率及排名、总收入及需求预测(2025-2031年)光敏聚酰亚胺(PSPI):全球市场份额和排名、总销售额和需求预测(2025-2031 年)