|

市场调查报告书

商品编码

1907216

辐射探测、监测和安全:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)Radiation Detection, Monitoring, And Safety - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

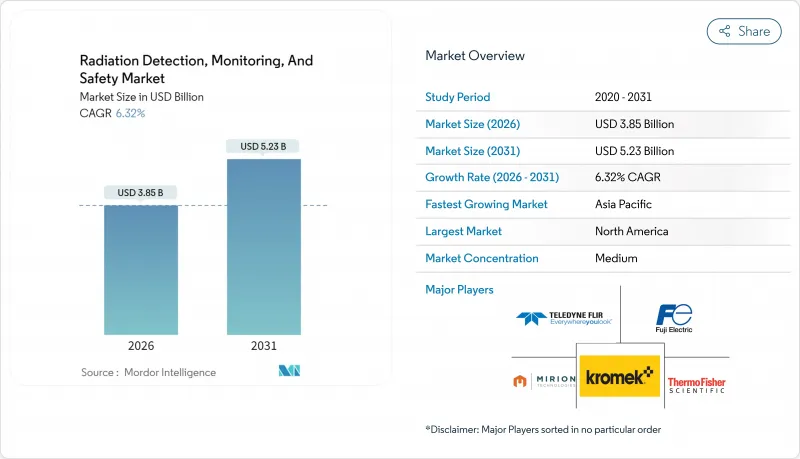

预计到 2026 年,辐射探测、监测和安全市场规模将达到 38.5 亿美元,高于 2025 年的 36.2 亿美元。

预计到 2031 年将达到 52.3 亿美元,2026 年至 2031 年的复合年增长率为 6.32%。

这一增长趋势主要受核医学检测的扩展、监管要求强制进行持续环境监测以及半导体检测器性能的快速提升所驱动。此外,边境管制、紧急应变和关键基础设施日益增长的安全需求也推动了市场发展,而老旧核子反应炉的退役则进一步增加了对监测系统的需求。辐射探测、监测和安全市场正凭藉其双重用途的价值提案(将民用医疗保健投资与国家安全支出连结起来)建构起强大的收入基础。北美公用事业公司、欧洲核能退役专案以及亚太地区的核能发电厂建设正在加速传统探测平台的更新换代。数位化连接、预测分析和云端原生架构如今已成为高级产品的差异化优势,为售后软体收入和持续服务合约提供了支撑。

全球辐射探测、监测及安全市场趋势及洞察

癌症和慢性病发生率上升

预计到2050年,全球癌症病例将达到3,500万例,为精密剂量测定係统提供了广泛的潜在市场。放射治疗科室倾向于使用能够捕捉剂量率高频波动并满足亚毫秒束流监测精度要求的固态检测器。自适应治疗计画平台产生的数据量日益增长,临床医师也越来越依赖即时回馈迴路来调整分次剂量。这促使医疗系统为多通道剂量检验架、冗余场校准器和基于云端的剂量配准软体分配预算,从而建立一个扩展辐射探测、监测和安全市场的生态系统。供应商的策略重点在于模组化检测器头和人工智慧辅助的品质保证仪錶盘,以提高直线加速器的运转率。

扩大核子医学和放射治疗程序

2024年,核医检测将年增12%,主要受锕-225和镏-177等治疗性诊断同位素的推动。放射性药物中心需要空气传播的α粒子监测器、用于热室的γ能谱仪以及可与设施LIMS资料库自动同步的个人剂量计。靠近患者群体的分散式迴旋加速器网路增加了屏蔽柜、去污通道和洩漏测试套件的采购点。美国FDA 21 CFR第361部分规定的标准化要求采用了同位素特定的校准通讯协定,从而确保了检测器重新校准服务供应商的持续外包机会。这些趋势推高了平均售价(ASP),并扩大了售后市场的收入前景。

繁重的多司法管辖区合规负担

检测器原始设备製造商 (OEM) 必须获得 FDA 510(k)核准、达到 IEC 60601-2-45 性能指标要求并获得 CE 认证,而每项认证都需要单独进行生物相容性、电磁相容性 (EMC) 和辐射模式测试。光是这些认证就足以大幅增加研发预算,迫使小规模的创新企业转向授权授权或小众学术市场。并行认证流程阻碍了韧体的快速更新,并减缓了设备在多个国家/地区部署后的功能推出速度。这导致设计采纳週期长达四年以上,降低了辐射探测、监测和安全市场新技术投资的净现值 (NPV),并限制了近期收入成长。

细分市场分析

到2025年,辐射探测和监测系统将占总收入的50.74%,为需要持续检验辐射状况的医院、公共产业和国防组织提供采购预算支援。在辐射探测、监测和安全市场中,探测平台预计将与预测分析模组同步成长,这些模组能够建议预防性维护週期。受ISO 2919防护设备标准统一化的推动,包括铅防护衣、去污室和自动屏蔽门在内的安全设备预计将以7.55%的复合年增长率超越传统增长速度。将即时伽马探测器与电动屏蔽帘整合的解决方案缩短了从警报到屏蔽的时间,并提高了ALARA(尽可能合理地降低辐射剂量)原则的合规性。供应商正在利用交叉销售的协同效应。医院通常会在订购闪烁探测器的同时订阅剂量计,而核子反应炉运营商则会将周界防护门与就地避难通风系统捆绑销售。监管要求推动了采购的紧迫性,限制了价格弹性,并维持了辐射探测、监控和安全行业中高价 SKU 的稳定销售。

云端仪錶板的增强功能、地理标记警报视觉化、基于角色的存取控制以及自动化合规报告生成,使检测设备不再只是普通的通用设备。 SaaS 迭加功能带来了显着的毛利率,甚至超过了硬体本身的毛利率,从而构建了一个与硬体无关的生态系统。因此,通路合作伙伴更倾向于储备整合了 NaI(Tl)、CZT 和中子模组的多重通讯协定网关,这些网关整合在一个监控人机介面 (HMI) 中。即时分析进一步降低了误报率,从而减少了高成本的疏散事件。这些增值解决方案巩固了 Detection Solutions 在辐射侦测、监测和安全市场的领先地位。

区域分析

北美地区预计到2025年将维持30.05%的收入份额,这反映了其现有的核能发电厂数量、广泛的国防安全保障基础设施以及率先采用相关技术的医疗保健系统。美国国家实验室正在投入津贴,以缩小碲锌镉(CZT)检测器的体积;加拿大自然资源部(NRCan)的框架正在津贴研究核子反应炉环境监测系统的升级。墨西哥放射性药物出口的成长推动了对同位素生产用热室监测器的需求增加。 ANSI N42标准下的跨境标准化正在提高设备互通性,并增强区域辐射探测、监测和安全市场的规模经济效益。

亚太地区以8.05%的复合年增长率实现了最快增长,这主要得益于中国计划在2060年运作150座核子反应炉。北京「中国製造2025」政策中蕴含的本土化要求鼓励合资企业发展碲锌镉(CZT)晶圆代工厂,从而降低进口关税和供应链脆弱性。日本在福岛第一核能发电厂后管理体制正在资助在核子反应炉设施周围安装20公里长的伽马射线防护网。同时,印度核能部正在资助为区域城市的癌症治疗病房安装低成本的辐射探测器。韩国正在扩大其18兆电子伏迴旋加速器网络,这将进一步增加服务医院的数量,巩固亚太地区作为全球辐射探测、监测和安全市场成长引擎的地位。

在欧洲,德国、比利时和西班牙的退役计划推动了均衡成长,从而催生了对机载α粒子监测器和废弃物桶分析系统的专业需求。法国在维持高比例核能发电的同时,专注于延长核电厂寿命的升级改造,这些改造必须符合法国核安局(ASN)严格的地震风险标准。 《欧洲核能共同体条约》(Euratom)规范了采购标准,并允许签订多年预算週期的大型跨境合约。中东欧国家正在对前苏联时代的科学研究核子反应炉进行现代化改造,需要包含训练服务的承包侦测系统。

儘管中东和非洲地区仍处于发展初期,但在战略港口引入中子货物扫描仪以及基于迴旋加速器的放射性药物实验室的运作,预示着新兴地区辐射探测、监测和安全市场的中期增长前景良好。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 癌症和慢性病发生率上升

- 核子医学和放射治疗程序的扩展

- 监管机构推动即时环境监测

- 小型化物联网剂量计

- 利用无人机进行大面积放射线测绘

- 全球老旧核子反应炉的退役

- 市场限制

- 跨多个司法管辖区的严格合规负担

- 持证辐射安全管理人员短缺

- 光谱级检测器需要高资本投入

- 氦-3和闪烁晶体供应链的可变性

- 产业价值链分析

- 宏观经济因素如何影响市场

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依产品类型

- 发现与监测

- 安全

- 透过检测器技术

- 充气式(盖革-米勒计数器、比例计数器、电离室)

- 闪烁(NaI(Tl)、CsI、LaBr3、塑胶)

- 半导体(HPGe、CZT、SiPM)

- 个人剂量计(TLD、OSL、电子式)

- 按最终用户行业划分

- 医疗保健

- 能源/电力(核能、常规)

- 国防安全保障/国防部

- 工业(石油和天然气、采矿、製造业)

- 研究机构和学术研究中心

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Mirion Technologies Inc.

- Thermo Fisher Scientific Inc.

- Teledyne FLIR LLC

- Fuji Electric Co., Ltd.

- Unfors RaySafe AB

- Arktis Radiation Detectors Ltd.

- Kromek Group plc

- Berthold Technologies GmbH & Co. KG

- Alpha-Spectra, Inc.

- Radiation Detection Company

- Centronic Ltd.

- Burlington Medical LLC

- Amray Group Ltd.

- Atomtex SPE

- Polimaster Ltd.

- Smiths Detection Group Ltd.

- Ludlum Measurements, Inc.

- Hitachi-Aloka Medical, Ltd.

- General Atomics Electronic Systems

- Else Nuclear srl

- Silena Group srl

第七章 市场机会与未来展望

The radiation detection, monitoring, and safety market size in 2026 is estimated at USD 3.85 billion, growing from 2025 value of USD 3.62 billion with 2031 projections showing USD 5.23 billion, growing at 6.32% CAGR over 2026-2031.

The expansion of nuclear-medicine procedures, regulatory mandates for continuous environmental surveillance, and rapid advancements in semiconductor-based detector performance underpin this trajectory. Heightened security concerns reinforce demand across border control, first-responder, and critical infrastructure segments, while aging reactor fleets drive the need for decommissioning-linked monitoring deployments. The radiation detection, monitoring, and safety market benefits from a dual-use value proposition that aligns civilian healthcare investments with national-security spending, creating a resilient revenue base. North American utilities, European nuclear-phase-out programs, and Asia-Pacific build-outs collectively accelerate replacement cycles for legacy detection platforms. Digital connectivity, predictive analytics, and cloud-native architectures now distinguish premium offerings, supporting aftermarket software revenues and recurring service contracts.

Global Radiation Detection, Monitoring, And Safety Market Trends and Insights

Rising Incidence of Cancer and Chronic Diseases

Cancer prevalence is climbing toward 35 million global cases by 2050, enlarging the addressable base for precision dosimetry systems.Radiotherapy departments now specify sub-millisecond beam-monitoring accuracy, favoring semiconductor detectors that capture high-frequency fluctuations in dose rate. Adaptive treatment planning platforms amplify data-generation volumes, and clinicians increasingly rely on real-time feedback loops to tune fractionated doses. Health systems, therefore, budget for multi-channel dose-verification racks, redundant field calibrators, and cloud-hosted dose-registry software, an ecosystem that broadens the radiation detection, monitoring, and safety market. Vendor strategies focus on modular detector heads and AI-assisted QA dashboards that enhance linear-accelerator uptime.

Expanding Nuclear Medicine and Radiotherapy Procedures

Nuclear medicine examinations grew 12% year-over-year in 2024, propelled by theranostic isotopes such as actinium-225 and lutetium-177.Radiopharmaceutical hubs require air-borne alpha-particle monitors, hot-cell gamma spectrometers, and personal dosimeters that auto-synchronize with facility LIMS databases. Decentralized cyclotron networks, positioned closer to patient populations, multiply procurement nodes for shielding cabinets, de-contamination portals, and leak-testing kits. Standardization under U.S. FDA 21 CFR Part 361 obliges isotope-specific calibration protocols, ensuring recurring outsourcing opportunities for detector-recalibration service providers. These trends elevate ASPs (average selling prices) and extend aftermarket revenue visibility.

Stringent Multi-Jurisdictional Compliance Burden

Detector OEMs must clear FDA 510(k) dossiers, satisfy IEC 60601-2-45 performance metrics, and attain CE marking conformity, each requiring discrete biocompatibility, EMC, and radiation pattern tests. Documentation alone inflates research and development budgets, steering smaller innovators toward licensing deals or niche academic markets. Parallel certification tracks hinder agile firmware updates once fielded devices enter multi-country footprints, slowing feature rollouts. The result is elongated design-win cycles that can exceed four years, diluting NPV on new technology investments and tempering near-term revenue acceleration within the radiation detection, monitoring, and safety market.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Real-Time Environmental Monitoring

- Miniaturization and IoT-Enabled Dosimeters

- Shortage of Certified Radiation Safety Officers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Detection and monitoring systems generated 50.74% of 2025 revenue, anchoring procurement budgets for hospitals, utilities, and defense agencies that must continuously validate dose conditions. Within the radiation detection, monitoring, and safety market size, detection platforms are projected to grow alongside predictive analytics modules that recommend proactive maintenance intervals. Safety equipment, encompassing lead-lined apparel, decontamination booths, and automated containment doors, is outpacing historical norms with a 7.55% CAGR, buoyed by harmonized ISO 2919 protective device standards. Integrated offerings that unite real-time g-ray probes with motorized shielding curtains shorten alarm-to-containment times and improve ALARA (as low as reasonably achievable) compliance. Vendors leverage cross-selling synergies: hospitals ordering scintillation probes often append badge-dosimetry subscriptions, while reactor operators bundle perimeter portals with shelter-in-place ventilation systems. Price elasticity remains modest, as regulatory obligations heighten procurement urgency, ensuring premium SKUs maintain a steady pull-through across the radiation detection, monitoring, and safety industry.

The expanded functionality of cloud dashboards, geo-tagged alarm visualization, role-based access, and automated compliance report generation pushes detection gear beyond commodity status. SaaS overlays carry significant gross margin, outstripping hardware rates and encouraging hardware-agnostic ecosystems. Consequently, channel partners favor stocking multi-protocol gateways that integrate NaI(Tl), CZT, and neutron modules under one supervisory HMI. Real-time analytics further reduces false-positive occurrences, trimming costly evacuation incidents. Such value-added solutions reinforce the leadership of detection solutions within the broader radiation detection, monitoring, and safety market.

The Radiation Detection, Monitoring and Safety Market Report is Segmented by Product Type (Detection and Monitoring and Safety), Detector Technology (Gas-Filled, Scintillation, and More), End-User Industry (Medical and Healthcare, Energy and Power, Homeland Security and Defence, Industrial, and More), and Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained a 30.05% revenue lead in 2025, reflecting entrenched nuclear-power fleets, extensive homeland-security infrastructures, and early-adopter healthcare systems. U.S. national laboratories are funneling research and development grants into CZT detector miniaturization, while the Canadian NRCan framework is subsidizing environmental-monitoring upgrades at research reactors. Mexico's expanding radiopharmaceutical exports add incremental volume for isotope-production hot-cell monitors. Cross-border standardization under ANSI N42 enhances equipment interoperability, thereby reinforcing economies of scale within the regional radiation detection, monitoring, and safety market.

Asia-Pacific records the fastest trajectory at an 8.05% CAGR, underwritten by China's plan to commission 150 reactors before 2060. The localization mandate embedded in Beijing's Made-in-China 2025 policy promotes joint-venture fabrication plants for CZT wafers, reducing import tariffs and mitigating supply-chain fragility. Japan's post-Fukushima regulatory regime finances perimeter gamma-ray meshes extending 20 km around reactor sites, while India's Department of Atomic Energy funds low-cost survey meters for cancer-therapy wards in tier-two cities. South Korea's expanding 18-MeV cyclotron network further widens the addressable hospital count, reinforcing the Asia-Pacific region's status as the global growth engine for the radiation detection, monitoring, and safety market.

Europe exhibits balanced growth as decommissioning projects in Germany, Belgium, and Spain create specialized demand for alpha-in-air monitors and waste-drum assay systems. France, maintaining a strong nuclear-electricity share, focuses on life-extension upgrades that must meet ASN's stringent seismic-risk criteria. The Euratom treaty standardizes procurement specifications, enabling cross-border volume contracts that leverage multi-year budget cycles. Central and Eastern European nations, modernizing Soviet-era research reactors, seek turnkey detection suites bundled with training services.

The Middle East and Africa, although nascent, are deploying neutron-cargo scanners at strategic ports and commissioning cyclotron-based radiopharmacy labs, foreshadowing medium-term momentum for the radiation detection, monitoring, and safety market in emerging geographies.

- Mirion Technologies Inc.

- Thermo Fisher Scientific Inc.

- Teledyne FLIR LLC

- Fuji Electric Co., Ltd.

- Unfors RaySafe AB

- Arktis Radiation Detectors Ltd.

- Kromek Group plc

- Berthold Technologies GmbH & Co. KG

- Alpha-Spectra, Inc.

- Radiation Detection Company

- Centronic Ltd.

- Burlington Medical LLC

- Amray Group Ltd.

- Atomtex SPE

- Polimaster Ltd.

- Smiths Detection Group Ltd.

- Ludlum Measurements, Inc.

- Hitachi-Aloka Medical, Ltd.

- General Atomics Electronic Systems

- Else Nuclear s.r.l.

- Silena Group s.r.l.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising incidence of cancer and chronic diseases

- 4.2.2 Expanding nuclear medicine and radiotherapy procedures

- 4.2.3 Regulatory push for real-time environmental monitoring

- 4.2.4 Miniaturisation and IoT-enabled dosimeters

- 4.2.5 UAV-based wide-area radiation mapping

- 4.2.6 De-commissioning of ageing nuclear reactors worldwide

- 4.3 Market Restraints

- 4.3.1 Stringent multi-jurisdictional compliance burden

- 4.3.2 Shortage of certified radiation safety officers

- 4.3.3 High capex for spectroscopic-grade detectors

- 4.3.4 Supply-chain volatility for He-3 and scintillator crystals

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Detection and Monitoring

- 5.1.2 Safety

- 5.2 By Detector Technology

- 5.2.1 Gas-Filled (Geiger-Muller, Proportional, Ion-Chambers)

- 5.2.2 Scintillation (NaI(Tl), CsI, LaBr3, Plastic)

- 5.2.3 Semiconductor (HPGe, CZT, SiPM)

- 5.2.4 Personal Dosimeters (TLD, OSL, Electronic)

- 5.3 By End-user Industry

- 5.3.1 Medical and Healthcare

- 5.3.2 Energy and Power (Nuclear, Conventional)

- 5.3.3 Homeland Security and Defence

- 5.3.4 Industrial (Oil and Gas, Mining, Manufacturing)

- 5.3.5 Research and Academic Laboratories

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Spain

- 5.4.3.4 Russia

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Egypt

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global overview, Market overview, Core Segments, Financials, Strategic Info, Market Share, Products and Services, Recent Developments)

- 6.4.1 Mirion Technologies Inc.

- 6.4.2 Thermo Fisher Scientific Inc.

- 6.4.3 Teledyne FLIR LLC

- 6.4.4 Fuji Electric Co., Ltd.

- 6.4.5 Unfors RaySafe AB

- 6.4.6 Arktis Radiation Detectors Ltd.

- 6.4.7 Kromek Group plc

- 6.4.8 Berthold Technologies GmbH & Co. KG

- 6.4.9 Alpha-Spectra, Inc.

- 6.4.10 Radiation Detection Company

- 6.4.11 Centronic Ltd.

- 6.4.12 Burlington Medical LLC

- 6.4.13 Amray Group Ltd.

- 6.4.14 Atomtex SPE

- 6.4.15 Polimaster Ltd.

- 6.4.16 Smiths Detection Group Ltd.

- 6.4.17 Ludlum Measurements, Inc.

- 6.4.18 Hitachi-Aloka Medical, Ltd.

- 6.4.19 General Atomics Electronic Systems

- 6.4.20 Else Nuclear s.r.l.

- 6.4.21 Silena Group s.r.l.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

携带式多功能辐射检测器市场:按检测器类型、便携性、销售管道、最终用户和应用划分——全球预测,2026-2032年

携带式多功能辐射检测器市场:按检测器类型、便携性、销售管道、最终用户和应用划分——全球预测,2026-2032年 非电离辐射电磁场 (EMF) 检测、测量和安全市场分析及预测(至 2035 年),按类型、产品、服务、技术、组件、应用、最终用户、安装类型和解决方案划分

非电离辐射电磁场 (EMF) 检测、测量和安全市场分析及预测(至 2035 年),按类型、产品、服务、技术、组件、应用、最终用户、安装类型和解决方案划分 2025-2029年全球辐射侦测、监测与安全市场

2025-2029年全球辐射侦测、监测与安全市场 辐射探测、监测和安全市场-全球产业规模、份额、趋势、机会及预测(按产品、探测类型、防护类型、最终用户、地区和竞争格局划分,2021-2031年)伽玛射线辐射检测器市场:按技术、产品类型、应用、最终用户和销售管道,全球预测(2026-2032年)光学辐射安全测试系统市场按产品类型、技术、波长范围、应用和最终用户划分 - 全球预测(2026-2032 年)

辐射探测、监测和安全市场-全球产业规模、份额、趋势、机会及预测(按产品、探测类型、防护类型、最终用户、地区和竞争格局划分,2021-2031年)伽玛射线辐射检测器市场:按技术、产品类型、应用、最终用户和销售管道,全球预测(2026-2032年)光学辐射安全测试系统市场按产品类型、技术、波长范围、应用和最终用户划分 - 全球预测(2026-2032 年) 半导体辐射检测器市场-2026-2031年预测超高纯锗单晶市场:依应用、终端用户产业、成长技术、纯度等级、晶体尺寸及晶体取向划分-2026-2032年全球预测

半导体辐射检测器市场-2026-2031年预测超高纯锗单晶市场:依应用、终端用户产业、成长技术、纯度等级、晶体尺寸及晶体取向划分-2026-2032年全球预测 2025年全球深空辐射监测市场报告辐射检测、监测和安全市场(按产品类型、检测类型、技术类型、配置、应用和销售管道)——全球预测 2025-2030

2025年全球深空辐射监测市场报告辐射检测、监测和安全市场(按产品类型、检测类型、技术类型、配置、应用和销售管道)——全球预测 2025-2030