|

市场调查报告书

商品编码

1907237

辐射固化涂料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Radiation Curable Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

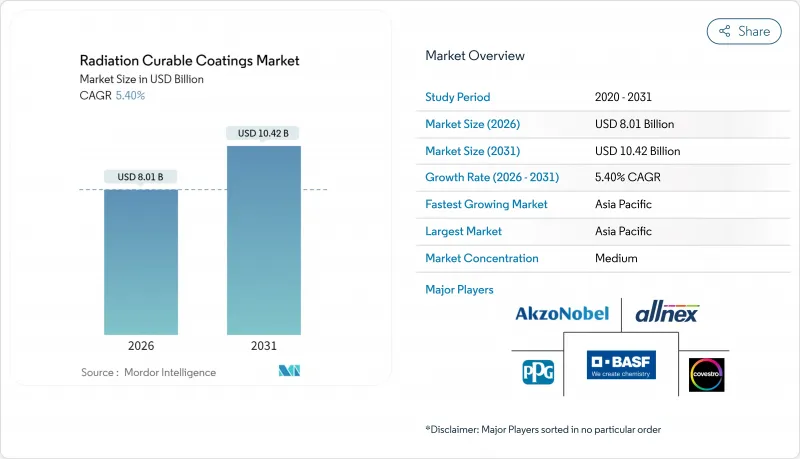

预计到 2026 年,辐射固化涂料市场规模将达到 80.1 亿美元,高于 2025 年的 76 亿美元。

预计到 2031 年将达到 104.2 亿美元,2026 年至 2031 年的复合年增长率为 5.4%。

市场参与企业将这一上升趋势归因于全球范围内日益严格的VOC法规、对节能生产方法的探索以及无溶剂化学品的稳步应用。亚太地区凭藉着监管协调和新的工业生产模式获得了区域优势。监管力道的加大正在加速市场采纳,美国环保署(EPA)针对气雾剂涂料製定的《美国挥发性有机化合物排放标准》将于2025年1月17日生效,合规期限延长至2027年1月17日,为製造商提供了24个月的宽限期来调整产品配方。

全球辐射固化涂料市场趋势及洞察

日益严格的VOC和碳中和法规加速了无溶剂紫外线/电子束光固化技术的普及。

全球监管机构不断收紧可接受的挥发性有机化合物 (VOC)阈值,推动辐射固化涂料市场朝向排放溶剂、100%固态配方发展。美国环保署 (EPA) 于 2025 年 1 月 17 日修订并实施了气雾剂涂料的国家 VOC排放标准,给予製造商两年的宽限期来重新评估其配方。加州空气资源委员会 (CARB) 正在实施类似的标准,该标准将水排除在外,并将某些化合物从「VOC 限值」的计算中豁免。这些法规有利于使用紫外线 (UV) 或电子束 (EB) 线进行即时固化的涂料製造商,无需使用溶剂烘箱。这降低了能源消耗并提高了工厂生产效率。虽然联邦标准规定工业维护涂料的 VOC 限值为 450 克/公升,但一些州正在努力将该限值降低至 100-250 克/公升,从而推动了对无溶剂技术的需求。

高通量包装和数位印刷生产线的需求

感压标籤、软包装和折迭纸盒的加工商依赖UV油墨来消除传统印刷机漫长的干燥过程,从而降低生产效率。即时固化的印刷品从生产线出来即可完全粘合,实现即时加工和排放——这对于准时制订单和个性化设计至关重要。产业刊物预测,到2025年,快速自动化、永续性和混合数位柔印工作流程将成为包装产业的主旋律。像INX International这样的设备供应商正在积极回应,推出符合食品接触标准并支援高遮盖力白色收缩套标的LED相容型能量固化油墨套装。这些解决方案正在巩固辐射固化涂料在印刷包装应用领域的市场地位。

特种寡聚物和光引发剂高成本

与通用树脂相比,客製化寡聚物骨架和高纯度光引发剂会显着增加成本。 2025年美国对部分加拿大和墨西哥原料征收25%的关税,对许多中国产品征收10%的关税,由此产生的运费溢价进一步加剧了涂料製造商的采购预算压力,迫使多家公司重新评估其筹资策略。像太阳化学这样的配方商正在采取临时提价措施来抵消原材料成本的急剧上涨,这凸显了辐射固化涂料市场利润率面临的压力。

细分市场分析

到2025年,寡聚物凭藉其在漆膜硬度、柔软性和耐化学性方面发挥的关键作用,将占据辐射固化涂料市场45.12%的份额,引领价值链。随着越来越多的製造商采用聚酯、胺甲酸乙酯和环氧丙烯酸酯主链来满足多样化的终端应用需求,由寡聚物驱动的辐射固化涂料市场规模预计将稳定成长。 Allnex公司的UCECOAT 7856正是这一进步的体现,它提供了一种不含溶剂的分散体,适用于高光泽地板材料应用,且不含传统挥发性有机化合物(VOC)。

同时,随着LED专用光引发剂在低能量波长下性能更佳,并能保护线路操作人员免受高温灯壳的伤害,预计光引发剂的年复合增长率将达到6.78%。单体继续控制黏度和交联密度,而研究实验室则继续开发生物基甲基丙烯酸酯稀释剂,以减少对石化燃料的依赖。

由于维修成本低廉且拥有强大的全球分销网络,紫外线预计在2025年将占装置容量的69.10%。一些工厂正在用掺铁灯取代老旧的汞灯,从而提高了现有生产线的辐照度,并推迟了大规模维修。然而,与电子束设备相关的辐射固化涂料市场预计将以最快的速度成长,到2031年复合年增长率将超过6.97%,因为加工商看重其无需光引发剂固化、深层渗透和氧不敏感聚合等优势。电子束生产线现在能够处理阻隔包装中常见的高颜料含量体系,这引起了食品罐头製造商和防护涂料应用商的注意。

LED-UV光源最初仅限于窄幅标籤印刷机,如今也应用于大幅面图文印刷和工业拼花地板生产线,因为动作温度很少超过40°C。混合双固化方法融合了UV和湿气固化化学物质,确保在阴影凹陷处也能牢固粘合;而新型激光诱导光聚合设备则有望将曝光时间缩短至毫秒级,从而进一步提升生产效率。

辐射固化涂料市场报告按原料(寡聚物、单体、光引发剂、添加剂)、固化技术(紫外线灯、电子束等)、树脂化学(环氧丙烯酸酯、胺甲酸乙酯丙烯酸酯、聚酯丙烯酸酯等)、终端用户行业(木材和家具、包装和印刷油墨、电子和半导体等)以及地区(亚太地区分析。

区域分析

预计到2025年,亚太地区将占据主导地位,市场份额达到41.05%,复合年增长率(CAGR)为5.96%,这将使该地区走上双领先发展道路。中国、日本和印度在电子、包装和汽车行业主导,随着国内环保法规越来越接近欧洲标准,这些行业产生了稳定的原材料需求。家具、地板材料和塑胶消费品的积层製造产能正从越南中部扩展到中国东部沿海地区,这些地区经常使用UV固化木器漆和塑胶面漆。

北美拥有丰富的技术资源,美国环保署(EPA)的强制规定推动了无溶剂解决方案的发展,而加州则在全国挥发性有机化合物(VOC)法规方面发挥着领先作用。密西根州和安大略省的汽车製造商正在为内装零件整合LED-UV固化隧道,以降低能源消耗。然而,美国将于2025年实施的关税迫使固化树脂製造商加强后向整合,以降低波动风险。

欧洲的愿景聚焦于绿色交易和REACH法规的扩展,该法规将于2025年9月起禁止在美甲产品中使用TPO光引发剂。针对板材製造商的甲醛和包装废弃物法规将于2026年生效,这将进一步加强辐射固化化学技术的有利市场环境。

南美、中东和非洲的需求正在萌芽并稳定成长,跨国公司正在这些地区建立卫星涂层工厂,以避免运输成本和汇率风险。巴西的柔软性塑胶薄膜印刷计划和沙乌地阿拉伯的板材家具计划便是很好的例子,说明西方引入的环境法规如何加速技术转移。儘管当地的复合材料生产商仍然依赖进口寡聚物,但监管的逐步收紧表明,一旦基础设施和技术能力得到提升,这些地区可能会成为下一个成长中心。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 日益严格的VOC和碳中和法规将加速无溶剂紫外线/电子束技术的普及应用。

- 高通量包装和数位印刷生产线的需求

- 用于超薄电子产品和穿戴式装置的三防胶的发展

- 亚太地区家具和地板材料製造能力快速扩张

- 汽车内装件的原始设备製造商开始采用在线连续LED-UV固化工艺

- 市场限制

- 特种寡聚物和光引发剂高成本

- 欧盟REACH法规将酰基膦氧化物重新分类后,供应趋紧。

- 新型生物基包装基材的热敏感性

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按原料

- 寡聚物

- 单体

- 光引发剂

- 添加剂

- 透过固化技术

- 紫外线灯

- 电子束

- 混合/双重固化

- 微波/红外线

- 通过树脂化学

- 环氧丙烯酸酯

- 胺甲酸乙酯丙烯酸酯

- 聚酯丙烯酸酯

- 丙烯酸酯

- 其他(硅酮、乙烯基醚)

- 按最终用户行业划分

- 木材/家具

- 包装和印刷油墨

- 电子和半导体

- 汽车/运输设备

- 医疗设备

- 3D列印/积层製造

- 其他(光学、建筑)

- 按地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- 3M

- Akzo Nobel NV

- Allnex Netherlands BV

- Arkema

- Ashland

- Axalta Coating Systems LLC

- BASF

- Covestro AG

- Dymax Corporation

- Evonik Industries AG

- Henkel AG & Co. KGaA

- Lord Corporation

- Nippon Paint Holdings Co., Ltd.

- PPG Industries, Inc.

- Rahn AG

- The Sherwin-Williams Company

- Watson Coatings, Inc.

第七章 市场机会与未来展望

The Radiation Curable Coatings Market size in 2026 is estimated at USD 8.01 billion, growing from 2025 value of USD 7.60 billion with 2031 projections showing USD 10.42 billion, growing at 5.4% CAGR over 2026-2031.

Market participants attribute this upswing to stricter global VOC limits, the search for energy-efficient production methods, and steady uptake of solvent-free chemistries. Asia Pacific secured regional primacy on the back of regulatory harmonisation and new industrial output. Regulatory momentum accelerates market adoption as the EPA's National Volatile Organic Compound Emission Standards for aerosol coatings took effect January 17, 2025, with compliance deadlines extended to January 17, 2027, creating a 24-month window for manufacturers to reformulate products.

Global Radiation Curable Coatings Market Trends and Insights

Tightening VOC and Carbon-Neutrality Regulations Accelerate Solvent-Free UV/EB Adoption

Global regulators continue to narrow permissible VOC thresholds, a move that propels the radiation-curable coatings market toward 100% solids formulas that emit no solvents. The United States Environmental Protection Agency enforced updated National VOC Emission Standards for aerosol coatings on 17 January 2025, giving manufacturers a two-year window to reassess formulations. California's Air Resources Board operates parallel limits that exclude water and exempt compounds from "VOC regulatory" calculations. Together, these measures reward coaters that deploy UV or electron-beam (EB) lines capable of instant curing without solvent ovens, thereby trimming energy footprints and boosting plant throughput. Federal thresholds cap industrial maintenance coatings at 450 g/L, yet some states press down to 100-250 g/L, intensifying the appeal of solvent-free technologies.

Demand for High-Throughput Packaging and Digital Printing Lines

Converters running pressure-sensitive labels, flexible packaging, and folding cartons rely on UV inks to eliminate the long drying stages that slow conventional presses. Instant-cure prints exit the line fully bonded, permitting immediate finishing and shipment, vital for just-in-time orders and personalised designs. Trade journals foresee rapid automation, sustainability compliance, and hybrid digital-flexo workflows defining packaging in 2025. Equipment suppliers such as INX International have responded with LED-compatible energy-curable ink sets that satisfy food-contact protocols and support high-opacity whites for shrink sleeves. These solutions strengthen the position of the radiation-curable coatings market within print-for-pack applications.

High Cost of Specialised Oligomers and Photoinitiators

Tailored oligomer backbones and high-purity photoinitiators add notable expense compared with commodity resins. Freight surcharges arising from 2025 US tariffs, 25% on selected Canadian and Mexican inputs, and 10% on many Chinese goods have further strained coating producers' procurement budgets, prompting several companies to re-engineer sourcing strategies. Sun Chemical and peer formulators adopted temporary price surcharges to offset the spike in raw-material outlays, highlighting margin pressure across the Radiation curable coatings market.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Ultra-Thin Electronic and Wearable Device Conformal Coatings

- Rapid Expansion of Asia Pacific Furniture and Flooring Manufacturing Capacity

- Supply Tightness After EU REACH Reclassification of Acyl-Phosphine Oxides

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Oligomers steered the value chain with 45.12% radiation curable coatings market share in 2025, underpinned by their decisive role in film hardness, flexibility, and chemical resistance. The radiation-curable coatings market size tied to oligomers is expected to widen steadily as producers exploit polyester-, urethane-, and epoxy-acrylated backbones to serve contrasting end-use demands. Allnex's UCECOAT 7856 exemplifies progress, delivering a solvent-free dispersion for high-gloss flooring that eliminates traditional VOCs.

In parallel, photoinitiators are projected to chart a 6.78% CAGR because LED-specific grades thrive under lower-energy wavelengths, safeguarding line operators from high-temperature lamp housings. Monomers continue to regulate viscosity and cross-link density, with laboratories channeling bio-based methacrylate diluents to cut fossil dependence.

UV lamps accounted for 69.10% of the 2025 installed capacity thanks to simple retrofit economics and a robust global distributor network. Plants replacing ageing mercury bulbs with iron-doped variants have squeezed higher irradiance out of existing lines, postponing large-scale overhauls. However, the radiation-curable coatings market size associated with electron-beam units could expand the fastest, potentially topping 6.97% CAGR to 2031 as converters weigh the merits of photoinitiator-free curing, deep-film penetration, and oxygen-insensitive polymerisation. EB lines now handle thick pigmented systems common in barrier packaging, spurring interest among food canners and protective-coatings applicators.

LED-UV sources, once confined to narrow-web label presses, now illuminate wide-format graphics and industrial parquet lines because operating temperatures rarely exceed 40 °C. Hybrid dual-cure set-ups merge UV and moisture-curable chemistries to ensure adhesion in shadowed recesses, whereas novel laser-induced photopolymerisation units promise second-level productivity leaps by cutting exposure times to milliseconds.

The Radiation Curable Coatings Report is Segmented by Raw Material (Oligomers, Monomers, Photoinitiators, and Additives), Curing Technology (UV Lamp, Electron Beam, and More), Resin Chemistry (Epoxy Acrylate, Urethane Acrylate, Polyester Acrylate, and More), End-User Industry (Wood and Furniture, Packaging and Printing Inks, Electronics and Semiconductor, and More), and Geography (Asia-Pacific, North America, Europe, and More).

Geography Analysis

Asia Pacific holds a commanding role with a 41.05% 2025 share and a 5.96% CAGR outlook that places the region on a dual leadership trajectory. China, Japan, and India dominate electronics, packaging, and automotive sectors, delivering constant feedstock demand as domestic environmental regulations increasingly mirror European norms. Additive capacity for furniture, flooring, and plastic consumer goods is expanding from central Vietnam to eastern coastal China, keeping UV-curable wood lacquers and plastic topcoats in high rotation.

North America remains technology-rich, with EPA edicts steering solvent-free adoption and California acting as a bellwether for national VOC limits. Automotive OEMs in Michigan and Ontario now integrate LED-UV tunnels for interior trims to achieve energy-footprint reductions. The US tariff regime introduced in 2025 has, however, prompted curing-resin producers to strengthen domestic backward integration to buffer volatility.

Europe's vision focuses on the Green Deal and REACH expansions, which have banned TPO photoinitiators in nail products since September 2025. The incoming 2026 formaldehyde rules for panel producers and the Packaging and Packaging Waste Regulation reinforce market conditions favourable to radiation-curable chemistries.

Across South America, the Middle East, and Africa, demand is emergent yet steady as multinationals deploy satellite coating facilities to sidestep freight and currency risk. Projects in Brazil for flexible plastic film printing and in Saudi Arabia for panel furniture underscore how environmental codes imported from Europe and North America accelerate technology transfer. While local formulators still rely on imported oligomers, gradual regulatory tightening suggests these regions will constitute the next growth flank once infrastructure and skills deepen.

- 3M

- Akzo Nobel N.V.

- Allnex Netherlands B.V.

- Arkema

- Ashland

- Axalta Coating Systems LLC

- BASF

- Covestro AG

- Dymax Corporation

- Evonik Industries AG

- Henkel AG & Co. KGaA

- Lord Corporation

- Nippon Paint Holdings Co., Ltd.

- PPG Industries, Inc.

- Rahn AG

- The Sherwin-Williams Company

- Watson Coatings, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening VOC and Carbon?Neutrality Regulations Accelerate Solvent-Free UV/EB Adoption

- 4.2.2 Demand for High-Throughput Packaging and Digital Printing Lines

- 4.2.3 Growth in Ultra-Thin Electronic and Wearable Device Conformal Coatings

- 4.2.4 Rapid Expansion of Asia Pacific Furniture and Flooring Manufacturing Capacity

- 4.2.5 OEM Shift to In-Line LED-UV Curing for Automotive Interior Parts

- 4.3 Market Restraints

- 4.3.1 High Cost of Specialized Oligomers and Photoinitiators

- 4.3.2 Supply Tightness after EU REACH Reclassification of Acyl-Phosphine Oxides

- 4.3.3 Thermal Sensitivity of Emerging Bio-Based Packaging Substrates

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts

- 5.1 By Raw Material

- 5.1.1 Oligomers

- 5.1.2 Monomers

- 5.1.3 Photoinitiators

- 5.1.4 Additives

- 5.2 By Curing Technology

- 5.2.1 UV Lamp

- 5.2.2 Electron Beam

- 5.2.3 Hybrid / Dual-Cure

- 5.2.4 Microwave / Infra-red

- 5.3 By Resin Chemistry

- 5.3.1 Epoxy Acrylate

- 5.3.2 Urethane Acrylate

- 5.3.3 Polyester Acrylate

- 5.3.4 Acrylic Ester

- 5.3.5 Others (Silicone, Vinyl Ether)

- 5.4 By End-User Industry

- 5.4.1 Wood and Furniture

- 5.4.2 Packaging and Printing Inks

- 5.4.3 Electronics and Semiconductor

- 5.4.4 Automotive and Transportation

- 5.4.5 Medical Devices

- 5.4.6 3D Printing/Additive Manufacturing

- 5.4.7 Others (Optical, Construction)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Allnex Netherlands B.V.

- 6.4.4 Arkema

- 6.4.5 Ashland

- 6.4.6 Axalta Coating Systems LLC

- 6.4.7 BASF

- 6.4.8 Covestro AG

- 6.4.9 Dymax Corporation

- 6.4.10 Evonik Industries AG

- 6.4.11 Henkel AG & Co. KGaA

- 6.4.12 Lord Corporation

- 6.4.13 Nippon Paint Holdings Co., Ltd.

- 6.4.14 PPG Industries, Inc.

- 6.4.15 Rahn AG

- 6.4.16 The Sherwin-Williams Company

- 6.4.17 Watson Coatings, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment