|

市场调查报告书

商品编码

1907247

三聚氰胺:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Melamine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

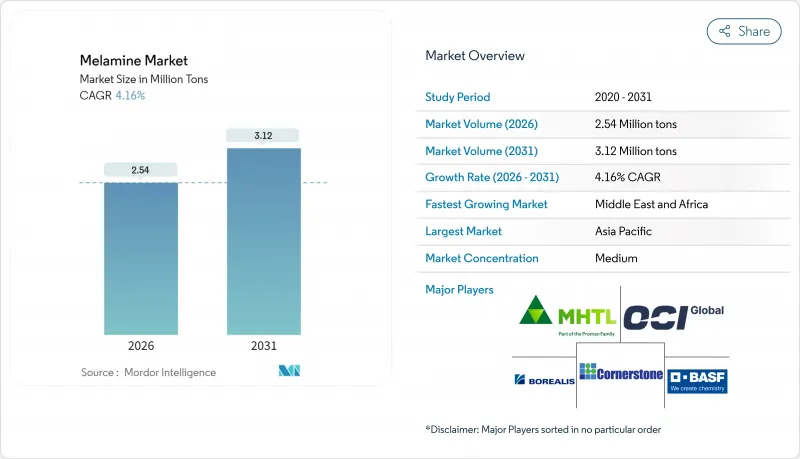

预计到 2026 年,三聚氰胺市场规模将达到 254 万吨,高于 2025 年的 244 万吨。

预计到 2031 年,产量将达到 312 万短吨,2026 年至 2031 年的复合年增长率为 4.16%。

亚太地区活跃的建设活动、北美和欧洲强劲的翻新和重建投资,以及多家工厂减产导致的全球供应趋紧,持续支撑着价格上涨和扩张。新兴市场对强化复合地板的快速接受度、超低甲醛释放树脂技术的进步,以及欧洲对高价值生物质平衡等级产品的采用,进一步推动了需求。在供应方面,卡达和中国的产能扩张部分抵销了欧洲的永久性停产,而持续的能源价格波动和高企的尿素原料价格则导致库存週期缩短,现货价格居高不下。将尿素追溯整合与碳减排蓝图相结合的供应商正在获得结构性成本优势和合规优势,从而推动区域自给自足策略和旨在消除三聚氰胺市场瓶颈的投资。

全球三聚氰胺市场趋势与洞察

新兴国家复合地板和家俱生产快速成长

中国、印度、越南和印尼的都市化以及中阶消费的成长,刺激了装饰层压板和家具升级的需求。中国2024年国家经济规划优先发展石化产业优化和下游一体化,推动了国内对三聚氰胺树脂的投资。产能的扩大确保了原料供应,使板材生产商能够从脲醛体系过渡到具有更佳防潮性能的三聚氰胺脲醛体系。印度化工产业的积极扩张,将新建的化肥联合企业与三聚氰胺衍生工厂连接起来,缩短了板材生产商的前置作业时间。塑合板产量不断增长,而传统上较少使用的木材,如桤木和桦木,需要高性能树脂才能达到黏合标准。这些因素共同支撑着三聚氰胺市场销量的稳定成长。

美国和欧盟建设业的復苏带动了对木材黏合剂的需求。

预计这两个地区的住宅开工量将在2024年趋于稳定,并在2026年之前保持温和成长。这将促进定向纤维板(OSB)和中密度纤维板(MDF)消费量的復苏,这两种板材都需要使用三聚氰胺增强黏合剂。欧盟建商也寻求符合REACH法规规定的甲醛排放限值(0.062 mg/m³)的板材等级,该法规将于2026年8月生效。北美生产商正在研发符合美国环保署《有毒物质管制法案》(TSCA)第六章规定的低排放量三聚氰胺-脲-甲醛树脂。欧洲客户越来越多地采用生物质平衡树脂,例如Finsa等早期采用者已整合了OCI的生物基三聚氰胺等级产品,与传统进口产品相比,其产品的碳足迹减少了约50%。

欧盟和北美收紧甲醛排放法规

欧盟0.062毫克/立方米的排放限值以及美国环保署《有毒物质控制法案》(TSCA)第六章相应的阈值均要求进行昂贵的认证、实验室检测和供应链文件编制。未能达到新标准的生产商将面临被市场淘汰的风险。虽然三聚氰胺-甲醛树脂的排放通常低于脲醛树脂,但合规认证的额外成本正在挤压利润空间,并吓退中小型加工商。瑞典更进一步,将排放限值设定为0.124毫克/立方米,这可能很快就会成为其他北欧市场的基准。

细分市场分析

预计到2025年,三聚氰胺树脂将保持64.70%的市场份额,成为装饰层压板、塑合板贴面和高压层压板的主要材料。亚太地区强劲的地板材料更换週期以及欧洲甲醛法规的压力将推动树脂市场在2031年之前持续成长。同时,儘管基数发泡体,但由于航太、电动车和铁路业优先考虑超轻型隔音材料,预计三聚氰胺泡棉市场规模将以4.72%的复合年增长率成长。发泡体製造商正在扩大连续块状和桶状泡沫的生产规模,以供应用于室内装饰的大尺寸面板。BASF的EcoBalanced计画表明,再生能源和生物质原料无需重新认证即可将产品碳足迹减少高达50%,这为致力于实现净零排放的原始设备製造商(OEM)提供了竞争优势。

树脂混炼商正致力于研发超低摩尔比体系,将甲醛排放降至0.05 mg/m³以下,以保障对欧盟的板材出口。拥有自有尿素回收设施和三聚氰胺反应器的综合生产商,能够确保原料的稳定供应,并利用规模经济在尿素价格波动时期维持利润率。 2024年Grupa Azoti的暂时停产凸显了依赖市售尿素和高成本气体的工厂的脆弱性。

三聚氰胺市场报告按产品类型(三聚氰胺晶体、三聚氰胺树脂、三聚氰胺泡沫及其他)、应用领域(层压板、木材黏合剂及其他)、终端用户产业(建筑与基础设施、家具与木工及其他)以及地区(亚太地区、北美地区、欧洲地区、南美地区、中东和非洲地区)进行细分。市场预测以吨为单位。

区域分析

到2025年,亚太地区将占据三聚氰胺市场51.05%的份额,这主要得益于中国庞大的树脂化产能和印度对装饰板材的稳定需求。山东和内蒙古的氨-尿素-三聚氰胺一体化生产联合体受益于煤炭或低成本天然气原料,进一步巩固了该地区的价格主导。日本和韩国对半导体和造船业使用的高纯度模塑料和吸音泡沫保持着高端市场需求。东南亚家具出口的快速成长推动了树脂投资的增加,儘管该地区仍依赖进口三聚氰胺晶体,但这有助于提高其自给自足能力。

北美是一个重要的市场,但其供应结构仍然供不应求,并依赖单一的国内生产商。飓风造成的停工和维护停产使板材和地板材料製造商面临供应中断的风险。对来自德国、卡达、特立尼达和多巴哥以及印度的产品征收的反补贴税限制了进口依赖。同时,建筑商正利用抵押房屋抵押贷款利率下调和基础设施支出增加的机会来维持板材消费,从而支撑了树脂需求的稳定。

儘管欧洲面临最严格的排放法规,但它在生物质平衡三聚氰胺领域拥有先发优势。中东和非洲地区虽然目前小规模,但成长率高达4.28%,卡达能源公司及其附属公司正利用当地丰富的低成本天然气原料扩大三聚氰胺产能。从拉斯拉凡出发的新型石化走廊旨在向亚洲和欧洲供应产品,但美国的关税限制了其直接进入北美市场。南美市场仍然保持着机会主义,在套利机会出现时,会从特立尼达和多巴哥以及欧洲进口现货货物。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 新兴经济体复合地板和家俱生产快速成长

- 美国和欧盟建设业的復苏正在推动对木材黏合剂的需求。

- 亚太地区产业扩张推动高压层压板和模塑料的发展

- 用于飞机和铁路声学的轻质耐热三聚氰胺泡沫

- 低碳尿素製三聚氰胺製程创新

- 市场限制

- 欧盟和北美收紧甲醛排放法规

- 生物基黏合剂替代品(大豆、木质素、液化木材)

- 化肥市场中断导致尿素价格波动

- 价值链分析

- 监管环境

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 原料分析及趋势

- 生产过程

- 进出口趋势

- 价格趋势

- 专利分析

第五章 市场规模与成长预测

- 按产品形式

- 三聚氰胺晶体

- 三聚氰胺树脂(HPL、LPL、浸渍纸)

- 三聚氰胺泡沫

- 其他(浸渍装饰纸、阻燃混合物)

- 透过使用

- 层压材料

- 木工黏合剂

- 模塑化合物

- 油漆和涂料

- 阻燃剂和纺织树脂

- 按最终用户行业划分

- 建筑和基础设施

- 家具和木工

- 汽车/运输设备

- 化学品和涂料

- 家用电器和电气设备

- 其他的

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- BASF SE

- Borealis AG

- Cornerstone Chemical Company

- EuroChem Group

- Fushun Huaxing Petroleum Chemical Co., Ltd

- Grupa Azoty

- Gujarat State Fertilizers & Chemicals Ltd(GSFC)

- Henan Xinlianxin Chemicals Group Co. Ltd

- Hexion Inc.

- Methanol Holdings(Trinidad)Ltd(MHTL)

- Mitsui Chemicals Inc.

- Nissan Chemical Corporation

- OCI NV

- Prefere Resins Holding GmbH

- Qatar Melamine Company

- Sichuan Chemical Works Group Ltd

第七章 市场机会与未来展望

Melamine Market size in 2026 is estimated at 2.54 million tons, growing from 2025 value of 2.44 million tons with 2031 projections showing 3.12 million tons, growing at 4.16% CAGR over 2026-2031.

Strong construction activity in the Asia-Pacific region, resilient repair-and-remodel investment in North America and Europe, and tight global supply following multiple plant curtailments continue to support price realization and reinforce expansion. Demand is further boosted by the rapid adoption of laminated flooring in emerging economies, technological advancements that enable ultra-low formaldehyde-emission resins, and the premium adoption of biomass-balanced grades in Europe. On the supply side, capacity additions in Qatar and China partially offset permanent shutdowns in Europe, yet lingering energy volatility and urea feedstock spikes keep inventory cycles short and spot prices elevated. Suppliers that combine backward urea integration with carbon-reduction road maps gain a structural cost and regulatory compliance edge, encouraging regional self-sufficiency strategies and targeted debottlenecking investments across the melamine market.

Global Melamine Market Trends and Insights

Surge in laminated flooring and furniture production in emerging economies

Urbanization and growing middle-class spending in China, India, Vietnam, and Indonesia are stimulating a boom in decorative laminates and furniture upgrades. China's 2024 national economic plan prioritizes petrochemical optimization and downstream integration, which favors local investments in melamine resin. Capacity additions ensure feedstock availability, enabling panel producers to transition from urea-formaldehyde to melamine-urea-formaldehyde systems, which offer improved moisture resistance. India's aggressive chemical build-out couples new fertilizer complexes with derivative melamine plants, shortening lead times to panel firms. Particleboard output is growing, and lesser-used species, such as alder and birch, will require higher-performance resins to meet bonding standards. Together, these factors support steady volume gains for the melamine market.

Construction recovery in United States/European Union spurring wood-adhesive demand

Housing starts stabilized in 2024 and are expected to rise modestly through 2026 in both regions, reviving consumption of oriented strand board and medium-density fiberboard, which rely on melamine-enhanced adhesives. EU builders also seek panel grades that meet upcoming REACH formaldehyde limits of 0.062 mg/m3, effective August 2026. North American producers align with EPA TSCA Title VI, driving substitution toward lower-emission melamine-urea-formaldehyde formulations. European customers are increasingly specifying biomass-balanced resins, with early adopters such as Finsa integrating OCI's bio-melamine grades, which reduce the product's carbon footprint by roughly 50% compared to conventional imports.

Stricter formaldehyde-emission regulations in EU and North America

The EU limit of 0.062 mg/m3 and aligned EPA TSCA Title VI thresholds mandate expensive certification, laboratory testing, and supply-chain documentation. Producers unable to meet the new bar risk market exclusion. While melamine-formaldehyde typically exhibits lower emissions than urea-formaldehyde, the incremental cost to prove compliance compresses margins and deters smaller converters. Sweden has taken a further step with a 0.124 mg/m3 limit, which may soon serve as a benchmark for other Nordic markets.

Other drivers and restraints analyzed in the detailed report include:

- Industrial expansion in Asia-Pacific boosting HPL and molding compounds

- Lightweight heat-resistant melamine foams for aerospace and rail acoustics

- Bio-based adhesive substitutes (soy, lignin, liquefied wood)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Melamine resins retained a 64.70% market share of melamine in 2025, serving as the backbone for decorative laminates, particleboard overlays, and high-pressure laminates. Robust flooring replacement cycles in Asia-Pacific and formaldehyde compliance pressures in Europe underpin growth for resins through 2031. In parallel, the melamine market size for foam is projected to expand at a 4.72% CAGR, albeit from a lower base, because aerospace, EV, and rail sectors prioritize ultra-light acoustic insulation. Foam manufacturers are scaling continuous blocks and bun stock production to supply large panels for interior trimming. BASF's EcoBalanced launch demonstrates how renewable electricity and biomass feedstock can deliver up to 50% lower product carbon footprint without requalification, a competitive differentiator for Original Equipment Manufacturers targeting Net Zero.

Resin formulators are focusing on ultra-low molar ratio systems to reduce formaldehyde emissions below 0.05 mg/m3, thereby protecting panel exports to the EU. Integrated producers that own urea capture and melamine reactors achieve feedstock security and leverage economies of scale to safeguard margins when urea volatility peaks. Grupa Azoty's temporary shutdown in 2024 highlights the exposure of plants that rely on merchant urea and high-cost gas inputs.

The Melamine Market Report is Segmented by Product Form (Melamine Crystals, Melamine Resins, Melamine Foam, and Others), Application (Laminates, Wood Adhesives, and More), End-User Industry (Construction and Infrastructure, Furniture and Woodworking, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific controlled 51.05% melamine market share in 2025, underpinned by China's vast resinification capacity and steady Indian demand for decorative panels. Integrated ammonia-urea-melamine complexes in Shandong and Inner Mongolia benefit from coal or low-cost gas feedstock, reinforcing regional price leadership. Japan and South Korea maintain a premium niche demand for high-purity molding compounds and acoustic foams used in the semiconductor and shipbuilding industries. Southeast Asia's fast-growing furniture exports attract incremental resin investment, boosting regional self-sufficiency despite reliance on imported melamine crystals.

North America is a significant market but remains structurally short, relying on a single domestic producer. Hurricane-related outages and maintenance downtime expose panel and flooring manufacturers to supply disruptions. Import reliance is moderated by countervailing duties placed on products from Germany, Qatar, Trinidad and Tobago, and India. Builders, meanwhile, capitalize on mellower mortgage rates and infrastructure spending to sustain panel consumption, underpinning stable resin demand.

Europe grapples with the strictest emission rules yet enjoys an early-mover advantage in biomass-balanced melamine. The Middle-East and Africa, while currently small, exhibit the highest growth rate of 4.28%, as QatarEnergy and its affiliates push melamine capacity linked to abundant, low-cost gas feedstock. New petrochemical corridors from Ras Laffan aim to serve Asian and European offtakers, yet U.S. duties constrain direct North American access. South America remains opportunistic, drawing spot cargoes from Trinidad and Tobago and Europe when arbitrage allows.

- BASF SE

- Borealis AG

- Cornerstone Chemical Company

- EuroChem Group

- Fushun Huaxing Petroleum Chemical Co., Ltd

- Grupa Azoty

- Gujarat State Fertilizers & Chemicals Ltd (GSFC)

- Henan Xinlianxin Chemicals Group Co. Ltd

- Hexion Inc.

- Methanol Holdings (Trinidad) Ltd (MHTL)

- Mitsui Chemicals Inc.

- Nissan Chemical Corporation

- OCI NV

- Prefere Resins Holding GmbH

- Qatar Melamine Company

- Sichuan Chemical Works Group Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in laminated flooring and furniture production in emerging economies

- 4.2.2 Construction recovery in United States/European union spurring wood-adhesive demand

- 4.2.3 Industrial expansion in APAC boosting HPL and molding compounds

- 4.2.4 Lightweight heat-resistant melamine foams for aero and rail acoustics

- 4.2.5 Low-carbon urea-to-melamine process innovations

- 4.3 Market Restraints

- 4.3.1 Stricter formaldehyde-emission regulations in European Union and North America

- 4.3.2 Bio-based adhesive substitutes (soy, lignin, liquefied wood)

- 4.3.3 Urea-price volatility tied to fertilizer-market disruptions

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

- 4.7 Feedstock Analysis and Trends

- 4.8 Production Process

- 4.9 Import-Export Trends

- 4.10 Price Trends

- 4.11 Patent Analysis

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Form

- 5.1.1 Melamine Crystals

- 5.1.2 Melamine Resins (HPL, LPL, Impregnated Paper)

- 5.1.3 Melamine Foam

- 5.1.4 Others (Impregnated Decor Paper, Flame-retardant Blends)

- 5.2 By Application

- 5.2.1 Laminates

- 5.2.2 Wood Adhesives

- 5.2.3 Molding Compounds

- 5.2.4 Paints and Coatings

- 5.2.5 Flame-retardants and Textile Resins

- 5.3 By End-user Industry

- 5.3.1 Construction and Infrastructure

- 5.3.2 Furniture and Woodworking

- 5.3.3 Automotive and Transportation

- 5.3.4 Chemicals and Coatings

- 5.3.5 Appliances and Electrical

- 5.3.6 Others

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Russia

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Borealis AG

- 6.4.3 Cornerstone Chemical Company

- 6.4.4 EuroChem Group

- 6.4.5 Fushun Huaxing Petroleum Chemical Co., Ltd

- 6.4.6 Grupa Azoty

- 6.4.7 Gujarat State Fertilizers & Chemicals Ltd (GSFC)

- 6.4.8 Henan Xinlianxin Chemicals Group Co. Ltd

- 6.4.9 Hexion Inc.

- 6.4.10 Methanol Holdings (Trinidad) Ltd (MHTL)

- 6.4.11 Mitsui Chemicals Inc.

- 6.4.12 Nissan Chemical Corporation

- 6.4.13 OCI NV

- 6.4.14 Prefere Resins Holding GmbH

- 6.4.15 Qatar Melamine Company

- 6.4.16 Sichuan Chemical Works Group Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

三聚氰胺市场规模、份额和成长分析(按形态、应用、最终用途和地区划分)-2026-2033年产业预测

三聚氰胺市场规模、份额和成长分析(按形态、应用、最终用途和地区划分)-2026-2033年产业预测 三聚氰胺板市场-全球产业规模、份额、趋势、机会和预测,按产品类型、配销通路、最终用途产业、地区和竞争细分,2020-2030 年三聚氰胺市场-全球产业规模、份额、趋势、机会及预测(依销售通路、最终用途、地区及竞争情况划分,2020-2030 年)

三聚氰胺板市场-全球产业规模、份额、趋势、机会和预测,按产品类型、配销通路、最终用途产业、地区和竞争细分,2020-2030 年三聚氰胺市场-全球产业规模、份额、趋势、机会及预测(依销售通路、最终用途、地区及竞争情况划分,2020-2030 年) 三聚氰胺市场(按产品类型、应用、最终用户和地区划分),2026 年至 2032 年

三聚氰胺市场(按产品类型、应用、最终用户和地区划分),2026 年至 2032 年 三聚氰胺全球市场需求,预测分析(2018-2034)

三聚氰胺全球市场需求,预测分析(2018-2034) 三聚氰胺泡棉块市场:按应用、按最终用户、按分销管道、按生产工艺、按密度、按价格分布、按地区

三聚氰胺泡棉块市场:按应用、按最终用户、按分销管道、按生产工艺、按密度、按价格分布、按地区 三聚氰胺泡沫块市场报告:2031 年趋势、预测与竞争分析

三聚氰胺泡沫块市场报告:2031 年趋势、预测与竞争分析 三聚氰胺市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测三聚氰胺市场-2024年至2029年预测

三聚氰胺市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测三聚氰胺市场-2024年至2029年预测 三聚氰胺全球市场2024-2028

三聚氰胺全球市场2024-2028