|

市场调查报告书

商品编码

1907301

发泡聚苯乙烯(EPS):市占率分析、产业趋势与统计、成长预测(2026-2031)Expanded Polystyrene (EPS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

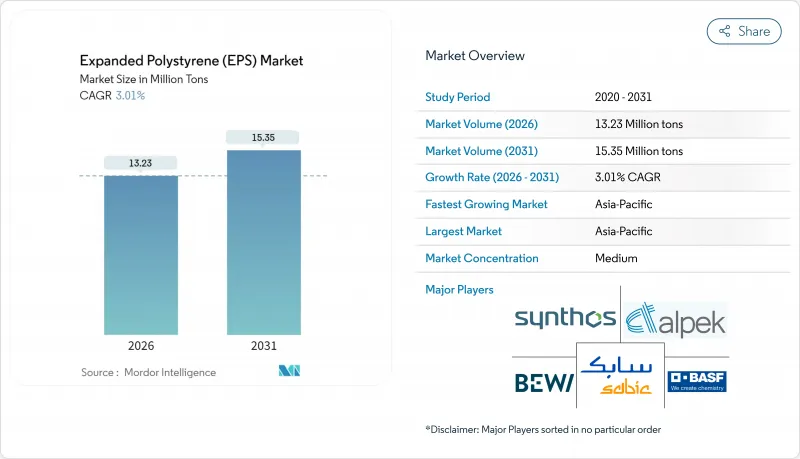

预计到 2026 年,发泡聚苯乙烯 (EPS) 市场规模将达到 1,323 万吨,高于 2025 年的 1,284 万吨。

预计到 2031 年产量将达到 1,535 万吨,2026 年至 2031 年的复合年增长率为 3.01%。

这一销售成长反映了建筑和包装行业消费量增加与苯乙烯加工过程中挥发性有机化合物 (VOC) 排放法规日益严格带来的成本压力之间的权衡。发泡聚苯乙烯市场受惠于其优异的导热性能与价格比,儘管模塑纸浆、生物泡棉和纸衬垫越来越受欢迎,但其需求仍保持稳定。亚太地区仍然是最大的单一市场,而北美则将这种材料用作电子商务的「最后一公里」隔热材料材料。企业策略正将重点转向化学回收通路和原料多角化,这显示循环经济合规性正在成为发泡聚苯乙烯市场新的竞争优势。

全球发泡聚苯乙烯(EPS)市场趋势与洞察

加快净零能耗建筑的建设进程

快速脱碳目标正在重新定义全球隔热材料规范。欧洲能源性能法规要求新建建筑接近零能耗,迫使建筑师寻找兼具低导热係数(λ值)和久经考验的耐久性的材料。灰色和银色EPS的导热係数比标准等级低20%,因此可以在符合U值标准的前提下建造更薄的墙体。日本2024年节能标准修订将收紧保温围护结构标准,进一步推动对石墨增强EPS解决方案的需求。随着建筑业主优先考虑降低营运成本,EPS越来越多地应用于连续隔热材料和承重断热板(SIP)中,从而巩固了EPS在高性能建筑市场的地位。

亚太新兴市场低温运输投资復苏

东南亚各国政府正投入数十亿美元用于低温运输物流,以防止食品变质并维持药品安全标准。由于其R值稳定性好、减震性能优异且单位运输成本最低,EPS包装箱和内衬正逐渐成为主流。越南的半导体组装厂使用EPS翻盖式容器来维持严格的温度范围,而区域疫苗宣传活动则依赖经过检验的EPS运输容器来保护对温度敏感的生物製药。

收紧苯乙烯挥发性有机化合物排放限值。

欧盟于2024年将职业环境中苯乙烯浓度限值降至20 ppm,要求製造商维修设备并加装减排系统,可能会使营运成本增加3-5%。同年,美国环保署(EPA)的执法力道也增加了40%,进一步加剧了合规风险。一些规模较小的加工企业可能因无力购买再生热氧化设备而退出市场,导致区域供应减少,并对整个发泡聚苯乙烯市场造成价格上涨压力。

细分市场分析

截至2025年,EPS将占发泡聚苯乙烯市场的95.12%,但灰色产品的市场预计将以更快的速度成长,到2031年复合年增长率将达到3.89%。德国和法国的建筑商正在指定使用石墨填充板材,以满足隔热性能标准(U值),而无需增加墙体厚度,这表明性能的提升即使在价格上涨的情况下也能推动需求。BASF等製造商已于2024年将Neopor的产能提高了40%,以满足建筑业的需求。同时,反光银色EPS产品正在渗透到工业隔热材料市场的表面温度超过80°C,从而在小规模但不断增长的特种市场中开闢了新的机会。通用包装仍然严重依赖白色发泡聚苯乙烯,因为物流买家优先考虑的是低初始成本。然而,随着建筑规范的日益严格,高隔热性能(高R值)的产品线预计将逐渐削弱白色EPS在发泡聚苯乙烯市场的主导地位。

白色EPS凭藉其成本优势,在电器缓衝、模压鱼箱和模组化建筑构件等领域巩固了其市场地位。灰色EPS虽然价格较高,但凭藉其在节能外墙系统中的应用,正逐渐赢得市场份额,其中石墨级EPS更是成为近零能耗建筑计划的首选。银色EPS由于适用于石化管道隔热材料和LNG接收站高温冷箱内衬,正经历稳健但盈利的成长。这些趋势表明,在高度同质化的发泡聚苯乙烯市场中,差异化的表现能够创造出具有竞争优势的价值领域。

发泡聚苯乙烯市场报告按产品类型(白色EPS、灰色EPS、银色EPS)、终端用户行业(建筑与施工、电气与电子、包装、其他终端用户行业)和地区(亚太地区、北美地区、欧洲地区、南美地区、中东和非洲)进行细分。市场预测以吨为单位。

区域分析

预计到2025年,亚太地区将占全球总吨位的66.75%,到2031年将以3.21%的复合年增长率成长。中国的都市化计画支撑了住宅开工量,而印度的「总理绿色力量计画」(PM Gati Shakti)正向道路和仓储计划投入数十亿卢比,从而带动了隔热材料需求的增长。在东南亚,尤其是在泰国和越南,为满足食品安全要求资金筹措的低温运输扩建,正在推动托盘式海鲜容器和疫苗冷藏箱对发泡聚苯乙烯(EPS)的需求。该地区垂直整合的苯乙烯生产联合体持续提供低成本供应,使当地生产商在整个发泡聚苯乙烯市场中拥有结构性优势。

北美是受电子商务和模组化建筑週期驱动的关键市场。在美国,各州的能源规范推动了连续保温材料的普及,工厂组合式墙板通常采用EPS芯材以缩短现场施工时间。在加拿大,魁北克省和安大略省数十亿美元的冷库建设带动了生鲜食品包装的订单,为该地区EPS需求提供了稳定的基础。墨西哥与北美市场相辅相成,不断增长的电子产品出口推动了对用于运输印刷基板的防静电EPS包装的需求。

儘管欧洲的废弃物减量法规日益严格,但EPS仍被用于欧盟绿色交易资助的大规模节能维修中。义大利的抗震维修激励措施和德国的《建筑能源法》促进了板材的销售,而英国蓬勃发展的宅配服务则抵消了因一次性刀叉餐具禁用模塑纸浆而导致的销售量下滑。沙乌地阿拉伯的石化产业扩张和巴西的基础设施走廊表明,随着物流网络的成熟,这些地区有望获得更大的市场份额。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 加快净零能耗建筑的建设进程

- 亚太新兴市场低温运输投资復苏

- 电子商务对最后一公里保温包装的需求日益增长

- 欧洲和日本的强制性隔震标准

- 模组化预製建筑的兴起

- 市场限制

- 收紧苯乙烯挥发性有机化合物(VOC)排放限值

- 模塑纸浆热感衬垫的普及速度迅速提升

- 欧盟「可回收设计」指令限制一次性EPS的使用。

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 进出口趋势

第五章 市场规模和成长预测(价值和数量)

- 依产品类型

- 白色 EPS

- 灰色和银色 EPS

- 按最终用户行业划分

- 建筑/施工

- 电气和电子设备

- 包装

- 其他终端用户产业(农业和汽车)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ASEAN

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 北欧国家

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Alpek SAB de CV

- BASF

- BEWi

- Epsilyte LLC

- Ineos

- Kaneka Corporation

- Ravago

- SABIC

- Shuangliang Group Co., Ltd.(Jiangsu Leasty Chemical Co.,Ltd.)

- SIBUR International GmbH

- Sunde Group

- Sunpor

- Synthos

- TotalEnergies

- Versalis SpA

- Wuxi Xingda foam plastic new material Limited

第七章 市场机会与未来展望

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 加快净零能耗建筑的建设进程

- 亚太新兴市场低温运输投资復苏

- 电子商务对最后一公里保温包装的需求日益增长

- 欧洲和日本的强制性隔震标准

- 模组化预製建筑的兴起

- 市场限制

- 收紧苯乙烯挥发性有机化合物(VOC)排放限值

- 模塑纸浆热感衬垫的普及速度迅速提升

- 欧盟「可回收设计」指令限制一次性EPS的使用。

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 进出口趋势

第五章 市场规模和成长预测(价值和数量)

- 依产品类型

- 白色 EPS

- 灰色和银色 EPS

- 按最终用户行业划分

- 建筑/施工

- 电气和电子设备

- 包装

- 其他终端用户产业(农业和汽车)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ASEAN

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 北欧国家

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Alpek SAB de CV

- BASF

- BEWi

- Epsilyte LLC

- Ineos

- Kaneka Corporation

- Ravago

- SABIC

- Shuangliang Group Co., Ltd.(Jiangsu Leasty Chemical Co.,Ltd.)

- SIBUR International GmbH

- Sunde Group

- Sunpor

- Synthos

- TotalEnergies

- Versalis SpA

- Wuxi Xingda foam plastic new material Limited

第七章 市场机会与未来展望

Expanded Polystyrene market size in 2026 is estimated at 13.23 million tons, growing from 2025 value of 12.84 million tons with 2031 projections showing 15.35 million tons, growing at 3.01% CAGR over 2026-2031.

Volume growth reflects the push-pull between rising consumption in construction and packaging and the cost pressures generated by stringent volatile-organic-compound limits on styrene processing. The Expanded Polystyrene market continues to capitalize on its favorable thermal conductivity-to-price ratio, which keeps demand steady even as molded pulp, bio-foams, and paper-based liners scale up. Asia-Pacific remains the single largest outlet, while North America leverages the material for e-commerce last-mile insulation. Corporate strategies increasingly pivot on chemical recycling pathways and feedstock diversification, signaling that circular-economy compliance is an emerging competitive prerequisite across the Expanded Polystyrene market.

Global Expanded Polystyrene (EPS) Market Trends and Insights

Accelerated Push for Net-Zero-Ready Buildings

Rapid decarbonization targets are redrawing insulation specifications worldwide. Energy-performance mandates in Europe require near-zero-energy new builds, pushing architects toward materials that combine low λ-values with proven durability. Gray and silver EPS deliver up to 20% lower thermal conductivity than standard grades, enabling thinner wall assemblies without compromising U-value compliance. Japan's 2024 energy-efficiency revision tightens thermal-envelope criteria, further amplifying demand for graphite-enhanced Expanded Polystyrene market solutions. As building owners prioritize operating-cost reductions, EPS gains traction in continuous insulation and structural insulated panels, reinforcing the Expanded Polystyrene market's profile in the high-performance building segment.

Resurgent Cold-Chain Investments in Emerging APAC

Southeast Asian governments are funneling billions into cold-chain logistics to curb food spoilage and uphold drug-safety standards. EPS boxes and liners dominate because they combine R-value stability with shock absorption at the lowest delivered cost per unit. Semiconductor assembly hubs in Vietnam rely on EPS clamshells to maintain narrow thermal windows, while regional vaccine campaigns depend on validated EPS shippers to protect temperature-sensitive biologics.

Tightening VOC Emission Ceilings on Styrene

The EU lowered occupational styrene limits to 20 ppm in 2024, forcing manufacturers to retrofit abatement systems that can add 3-5% to operating costs. EPA enforcement actions in the United States climbed 40% the same year, raising compliance risk. Smaller converters lacking capital for regenerative thermal oxidizers may exit, narrowing regional supply and nudging prices upward across the Expanded Polystyrene market.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Last-Mile Insulated Packaging Boom

- Mandatory Seismic Insulation Codes in Europe and Japan

- EU "Design for Recycling" Mandates Curbing Single-Use EPS

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

White EPS accounted for 95.12% of the Expanded Polystyrene market in 2025, yet gray variants are on track to expand faster at 3.89% CAGR through 2031. Builders in Germany and France specify graphite-infused panels to meet U-values without thicker walls, illustrating how performance upgrades redirect demand even when prices are higher. Manufacturers such as BASF added 40% Neopor capacity in 2024 to satisfy this construction pull. Concurrently, reflective silver EPS grades penetrate industrial insulation niches where surface temperatures exceed 80 °C, tapping small but growing specialized opportunities. Commodity packaging still leans heavily on white foam because logistics buyers prioritize low upfront cost. As building codes tighten, however, higher-R-value lines will gradually chip away at white EPS dominance within the Expanded Polystyrene market.

White EPS's cost edge keeps it entrenched in appliance cushioning, molded fish crates, and block-molded architectural shapes. Gray EPS, despite its premium, secures volume through energy-efficient facade systems, ensuring that every new near-zero-energy project allocates tonnage to graphite grades. The expansion of silver EPS stays modest but lucrative, given its fit for petrochemical pipe insulation and high-temperature cold-box linings in LNG terminals. These trends confirm that differentiated performance creates defensible value pockets, even inside a largely commoditized Expanded Polystyrene market.

The Expanded Polystyrene Market Report is Segmented by Product Type (White EPS and Gray and Silver EPS), End-User Industry (Building and Construction, Electrical and Electronics, Packaging, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific secured 66.75% of global tonnage in 2025 and is projected to rise at a 3.21% CAGR to 2031. China's urbanization pipeline sustains housing starts, while India's PM Gati Shakti program channels billions into road and warehousing projects, translating into higher insulation demand. Southeast Asia, led by Thailand and Vietnam, bankrolls cold-chain expansion to meet food-safety directives, pulling incremental EPS volumes for pallet-sized fish boxes and vaccine coolers. The region's vertically integrated styrene complexes keep delivering costs low, giving local producers a structural advantage across the Expanded Polystyrene market.

North America is a significant market, driven by e-commerce and modular construction cycles. U.S. state-level energy codes increasingly require continuous-insulation layers, and factory-assembled wall panels frequently embed EPS cores to accelerate job-site completion. Canada's multibillion-dollar cold-storage builds in Quebec and Ontario drive fresh packaging orders, ensuring a dependable baseline for regional EPS demand. Mexico rounds out the North American picture with rising electronics exports, necessitating anti-static EPS packs for printed-circuit-board transit.

Europe confronts stricter waste-reduction rules but still leans on EPS for deep-energy retrofits funded by the EU Green Deal. Italy's seismic-retrofit incentives and Germany's Building Energy Act sustain panel sales, while the United Kingdom's booming meal-delivery services offset volume lost to molded-pulp bans in single-use cutlery. Petrochemical expansions in Saudi Arabia and infrastructure corridors in Brazil suggest these territories could increase their shares as logistics networks mature.

- Alpek SAB de CV

- BASF

- BEWi

- Epsilyte LLC

- Ineos

- Kaneka Corporation

- Ravago

- SABIC

- Shuangliang Group Co., Ltd. (Jiangsu Leasty Chemical Co.,Ltd.)

- SIBUR International GmbH

- Sunde Group

- Sunpor

- Synthos

- TotalEnergies

- Versalis S.p.A.

- Wuxi Xingda foam plastic new material Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated push for net-zero ready buildings

- 4.2.2 Resurgent cold-chain investments in emerging APAC

- 4.2.3 E-commerce last-mile insulated packaging boom

- 4.2.4 Mandatory seismic insulation codes in Europe and Japan

- 4.2.5 Modular prefab construction uptake

- 4.3 Market Restraints

- 4.3.1 Tightening VOC emission ceilings on styrene

- 4.3.2 Rapid scale-up of molded pulp thermal liners

- 4.3.3 EU "Design for Recycling" mandates curbing single-use EPS

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Import-Export Trends

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Product Type

- 5.1.1 White EPS

- 5.1.2 Gray and Silver EPS

- 5.2 By End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Electrical and Electronics

- 5.2.3 Packaging

- 5.2.4 Other End-user Industries (Agriculture and Automotive)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Nordic Countries

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Alpek SAB de CV

- 6.4.2 BASF

- 6.4.3 BEWi

- 6.4.4 Epsilyte LLC

- 6.4.5 Ineos

- 6.4.6 Kaneka Corporation

- 6.4.7 Ravago

- 6.4.8 SABIC

- 6.4.9 Shuangliang Group Co., Ltd. (Jiangsu Leasty Chemical Co.,Ltd.)

- 6.4.10 SIBUR International GmbH

- 6.4.11 Sunde Group

- 6.4.12 Sunpor

- 6.4.13 Synthos

- 6.4.14 TotalEnergies

- 6.4.15 Versalis S.p.A.

- 6.4.16 Wuxi Xingda foam plastic new material Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Bio-based and Chemically Recycled EPS Roadmap

发泡聚苯乙烯市场报告:依产品、终端用途产业及地区划分(2026-2034 年)

发泡聚苯乙烯市场报告:依产品、终端用途产业及地区划分(2026-2034 年) 发泡聚苯乙烯市场:依形态、等级、最终用途产业、通路和应用程式划分-2026-2032年全球市场预测发泡聚苯乙烯增密设备市场:按机器类型、操作模式、类别、应用和最终用户划分 - 全球预测 2026-2032

发泡聚苯乙烯市场:依形态、等级、最终用途产业、通路和应用程式划分-2026-2032年全球市场预测发泡聚苯乙烯增密设备市场:按机器类型、操作模式、类别、应用和最终用户划分 - 全球预测 2026-2032 发泡聚苯乙烯市场-全球产业规模、份额、趋势、机会及预测(依产品类型、最终用途、地区及竞争格局划分,2021-2031年)

发泡聚苯乙烯市场-全球产业规模、份额、趋势、机会及预测(依产品类型、最终用途、地区及竞争格局划分,2021-2031年) 欧洲发泡聚苯乙烯(EPS)市场份额分析、产业趋势、统计和成长预测(2026-2031)

欧洲发泡聚苯乙烯(EPS)市场份额分析、产业趋势、统计和成长预测(2026-2031) 发泡聚苯乙烯包装市场规模、份额和成长分析(按产品类型、最终用途产业、密度、形状、应用和地区划分)-2026-2033年产业预测

发泡聚苯乙烯包装市场规模、份额和成长分析(按产品类型、最终用途产业、密度、形状、应用和地区划分)-2026-2033年产业预测 珠状聚苯乙烯(EPS)泡沫包装市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2024-2032 年)

珠状聚苯乙烯(EPS)泡沫包装市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2024-2032 年) 2025-2029年全球发泡聚苯乙烯市场

2025-2029年全球发泡聚苯乙烯市场 全球发泡聚苯乙烯市场:市场规模、份额、趋势分析(按产品、应用和地区)、细分市场预测(2025-2033)

全球发泡聚苯乙烯市场:市场规模、份额、趋势分析(按产品、应用和地区)、细分市场预测(2025-2033) 包装用发泡聚苯乙烯市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

包装用发泡聚苯乙烯市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测