|

市场调查报告书

商品编码

1910477

锰:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Manganese - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

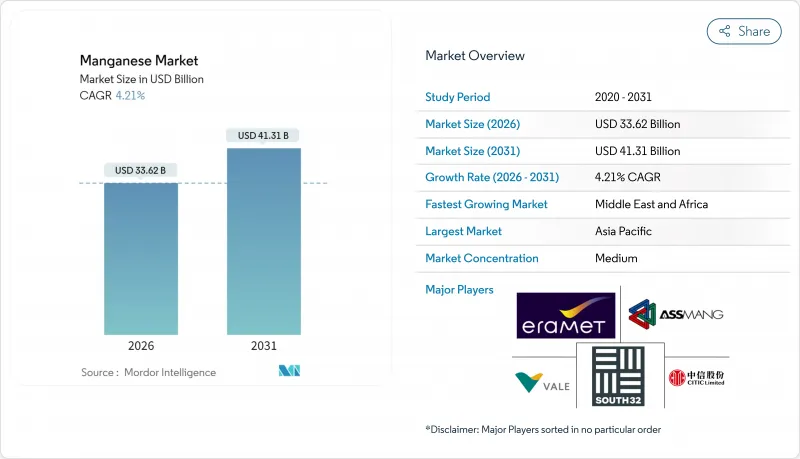

预计锰市场规模将从 2025 年的 322.6 亿美元成长到 2026 年的 336.2 亿美元,到 2031 年将达到 413.1 亿美元,2026 年至 2031 年的复合年增长率为 4.21%。

儘管传统钢合金仍占据主导地位,但电池级钢材和高纯度特殊钢材的快速成长正在重塑贸易路线,并刺激中国以外地区新的提炼投资。南32集团旗下GEMCO矿遭受飓风破坏,以及加彭的劳工动盪,导致矿石供应紧张,推高现货价格,并促使西方买家签订长期合约。欧洲和印度的氢基直接还原铁(DRI)计划正在增加每吨粗钢所需的锰铁消费量。同时,用于重型电动车的磷酸锰锂(LMFP)正极材料正在推动对高纯度锰的需求。美国和沙乌地阿拉伯政府正在补贴国内铁合金和硫酸锰的生产能力,以减少对中国提炼的依赖,这项政策措施可能进一步巩固锰市场成长超过GDP成长的局面。

全球锰市场趋势及展望

重型车辆的电气化将加速对高纯度锰的需求。

重型电动卡车和巴士越来越多地使用锰含量高于传统磷酸铁锂(LFP)阴极的液态金属磷酸铁锂(LMFP)阴极,这实际上提高了每千瓦时锰的用量。 Element 25公司位于路易斯安那州的冶炼厂由美国能源局(DOE)津贴,生产并供应高纯度硫酸锰,无需通过中国中间商。值得注意的是,汽车製造商现在愿意为可追溯的低碳原料支付溢价,这在锰市场中形成了双层定价结构。为此,欧美国家的政策奖励正在提振对电池级材料的需求,预计即使钢铁週期出现波动,这种需求仍将持续成长。在这种不断变化的市场格局下,传统矿业公司正在寻求下游扩张或与精炼商建立合作关係,以维持其市场地位。

钢铁製造商转向氢化直接还原铁(DRI)增加了对高碳锰铁的需求

与高炉炼铁製程相比,氢基直接还原铁电弧炉炼铁製程需要更高的锰添加量。这主要是由于直接还原铁球团矿的残余锰含量较低。瑞典和德国的先导工厂已证实,2024年运作后,需要增加合金添加量。印度的「国家绿色氢能计画」旨在2030年扩大绿色氢的生产,这可能会增加该国对锰铁的需求。使用低碳电力生产的锰铁供应商预计将从中受益匪浅,尤其是在欧盟碳边境调节税对进口的煤炭密集型锰矿征收附加税的情况下。合金消费量的激增不仅巩固了当前市场,也为锰市场的长期成长铺平了道路。

快速采用磷酸铁锂(LFP)抑制阴极级锰的成长

2024年,搭乘用电动车製造商将采用更高比例的磷酸锂铁锂(LFP)正极材料,取代锰基材料,这使得近期正极材料的需求前景不明朗。磷酸铁锂的兴起意味着硫酸锰需求的下降。如果磷酸铁锂的市占率在2028年之前持续成长,电池锰产业的表现可能会低于先前的预期。生产商正在透过提升提炼的产能来应对这项挑战,使其能够将锰转化为用于炼钢添加剂的电解金属,但这种柔软性的提升也带来了资本支出的增加。因此,儘管磷酸铁锂也在同步发展,但锰市场的成长仍受到限制。

细分市场分析

至2025年,合金将占锰市场需求的67.75%,这主要得益于成品钢中添加锰铁和硅锰合金。欧洲和印度氢化直接还原铁(DRI)产能的扩张推动了合金用量的增加,从而支撑了锰市场销售的稳定成长。电解锰预计将成长6.17%,主要受便携式电子产品和新兴电网储能计划需求的驱动。其他终端用途,包括饲料、水处理和陶瓷,也随着GDP的成长而同步成长,为锰市场提供了稳定的销售。电解(EMD)的復苏,主要得益于锌锰电池的需求,并引起了加州能源部(DOE)公用事业规模先导计画的关注。此外,面临欧盟碳关税的钢铁製造商正在增加对经认证的低碳合金的需求,从而在更广泛的商品市场中创造了一个高端细分市场。

本锰市场报告按应用领域(合金、电解二氧化锰、电解金属、其他应用)、终端用户行业(工业、建筑、储能及电力、其他终端用户行业)、矿石等级(电池级、高纯度级、标准级、工业级)和地区(亚太地区等)对市场进行分析。市场预测以美元以金额为准。

区域分析

到2025年,亚太地区将占全球锰市场的54.20%,这主要得益于中国对钢铁和电池材料的强劲需求。印度也做出了显着贡献,这得益于基础设施投资以及塔塔钢铁和印度金属氧化物有限公司(MOIL)硅锰业务的扩张。日本和韩国已成为电解金属产业的主要参与者,并向全部区域出口高纯度产品。资源丰富的非洲由于精炼能力有限,国内锰矿加工能力有限,大部分锰矿用于出口。预计到2031年,中东和非洲锰市场将以5.86%的复合年增长率成长,这主要得益于南非放宽铁路运输限制的倡议以及沙乌地阿拉伯的下游投资。

预计到2025年,北美在全球锰需求中所占份额较小,但路易斯安那州Element 25冶炼厂的运作有望提升这一份额,因为在地采购正在增加。加拿大正积极开发魁北克省的锰矿矿床,墨西哥钢铁厂也正在扩大产能以满足美国汽车製造商的需求。欧洲的锰需求份额中等,但面临碳边境调节机制(CBAM)带来的挑战,买方正转向挪威的水力发电,以获取合金和再生材料。特别是Eramet旗下的「eraLow」品牌,已与欧盟使用再生能源的扁钢製造商签订了合约。

儘管南美洲在全球锰需求中所占份额较小,但巴西却是合金消费和出口的领头羊,其主要出口产品来自淡水河谷的阿祖尔矿。同时,阿根廷蓬勃发展的锂产业间接推动了锰的需求,尤其是正极材料的需求。发展区域电池供应链的努力可望提高南美洲的锰加工能力,进而可能重塑锰市场动态。拉丁美洲国家能否在价值链中向上攀升,将取决于基础建设和绿色能源政策。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 重型车辆的电气化将加速对高纯度锰的需求

- 钢铁厂改用氢化直接还原铁会增加碳氢化合物锰铁的使用量。

- 西方原始设备製造商 (OEM) 与 HPMSM 签订的承购协议有助于实现供应来源多元化。

- 印度和东协对基础设施级硅锰的需求

- 地缘政治动盪导致矿产供应中断(例如加彭和澳洲),推高矿产价格。

- 市场限制

- 快速采用磷酸铁锂将抑制阴极级锰需求的成长。

- 南非矿石港口瓶颈限制了出口量

- 高碳铁合金的二氧化碳排放需缴纳碳边境税。

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 透过使用

- 合金

- 电解锰

- 电解金属

- 其他用途

- 按最终用途行业划分

- 产业

- 建造

- 储能和电力

- 其他最终用途领域

- 按矿石品位

- 电池级

- 高纯度

- 标准级

- 技术级

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- African Rainbow Minerals Limited.

- Anglo American plc

- Assore Limited(Assmang Proprietary Limited)

- BHP

- CITIC LIMITED

- Consolidated Minerals Limited.

- Element 25 Limited

- Eramet

- Giyani Metals Corp

- Jupiter Mines Limited

- Manganese Metal Company(Pty)Ltd.

- MOIL LIMITED

- Ningxia Tianyuan Manganese Industry Group Co. Ltd

- NIPPON DENKO CO. LTD

- OM Holdings Ltd.

- POSCO M-TECH.

- South32

- Tata Steel

- Vale

- Vibrantz

第七章 市场机会与未来展望

The Manganese market is expected to grow from USD 32.26 billion in 2025 to USD 33.62 billion in 2026 and is forecast to reach USD 41.31 billion by 2031 at 4.21% CAGR over 2026-2031.

Traditional steel-grade alloys still dominate; however, rapid growth in battery-grade and high-purity specialties is reshaping trade routes and prompting new refinery investments outside China. Cyclone damage at South32's GEMCO mine and labor unrest in Gabon have tightened ore supply, elevating spot prices and prompting Western buyers to secure long-term contracts. Hydrogen-based direct reduced iron (DRI) projects in Europe and India are raising ferromanganese intensity per tonne of crude steel, while lithium-manganese-iron-phosphate (LMFP) cathodes for heavy-duty electric vehicles are expanding high-purity manganese demand. Governments in the United States and Saudi Arabia are subsidizing domestic ferroalloy and sulfate capacity to reduce dependence on Chinese refining, a policy trend likely to reinforce above-GDP expansion in the Manganese market.

Global Manganese Market Trends and Insights

Electrification of Heavy-Duty Vehicles Accelerates HP-Mn Demand

Heavy-duty electric trucks and buses are increasingly turning to LMFP cathodes, which have a higher manganese content than traditional LFP chemistries, effectively increasing the manganese usage per kilowatt-hour. Element 25's Louisiana refinery, backed by a U.S. DOE grant, will produce and supply high-purity manganese sulfate, circumventing Chinese intermediaries. In a notable shift, automakers are now willing to pay a premium for feedstock that is both traceable and low-carbon, leading to the establishment of a two-tier pricing structure in the manganese market. As a result of these developments, Western policy incentives are driving up demand for battery-grade supplies, ensuring continued growth even amid fluctuations in steel cycles. This evolving landscape is prompting traditional ore miners to either move downstream or collaborate with refiners, all in an effort to maintain their market foothold.

Steelmakers' Switch to Hydrogen-DRI Raises HC FeMn Intensity

Hydrogen-based DRI-EAF pathways necessitate more manganese additions compared to blast-furnace routes, primarily because DRI pellets have a lower residual manganese content. Pilot plants in Sweden and Germany validated these increased alloy additions during their 2024 commissioning. India's National Green Hydrogen Mission, which aims to boost green hydrogen production by 2030, could increase the country's demand for ferromanganese. Suppliers of ferromanganese harnessing low-carbon power are set to gain significantly, especially as EU carbon border taxes impose penalties on coal-intensive grade imports. This surge in alloy consumption not only strengthens the current market but also paves the way for the long-term growth of the Manganese market.

Rapid LFP Adoption Curbs Cathode-Grade Mn Growth

In 2024, passenger EV manufacturers increased the share of LFP cathodes, displacing manganese-based chemistries and casting a shadow on the immediate demand for cathode-grade materials. A rise in LFP translates to a reduction in manganese sulfate demand. Should LFP's market share continue to increase by 2028, the battery-grade manganese sector may fall short of previous projections. While producers are adapting by crafting refineries that can switch to electrolytic metals for steel additives, this added flexibility comes with a hike in capital expenses. As a result, the Manganese market's growth is being restrained, even as LMFP sees parallel advancements.

Other drivers and restraints analyzed in the detailed report include:

- Western OEM Off-Take Deals for HPMSM Diversify Supply

- Infrastructure-Grade Silico-Manganese Demand in India and ASEAN

- Ore-Port Bottlenecks in South Africa Cap Export Volumes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Alloys accounted for 67.75% of the manganese market demand in 2025, primarily driven by the addition of ferromanganese and silicomanganese to finished steel. With rising hydrogen-DRI capacities in Europe and India, alloy intensity has increased, supporting steady volume growth. Electrolytic manganese dioxide is poised for 6.17% growth, driven by demand from portable electronics and emerging grid-storage initiatives. Other end-uses, including feed, water treatment, and ceramics, are growing in tandem with GDP, providing volume stability to the manganese market. The resurgence of EMD is largely attributed to zinc-manganese batteries, which have caught the attention of utility-scale pilots in California's DOE. Additionally, steelmakers grappling with EU carbon tariffs are increasingly seeking certified low-carbon alloys, creating a premium niche in the broader commodity market.

The Manganese Market Report is Segmented by Application (Alloys, Electrolytic Manganese Dioxide, Electrolytic Manganese Metals, and Other Applications), End-Use Sector (Industrial, Construction, Power Storage and Electricity, and Other End-Use Sectors), Ore Grade (Battery Grade, High Purity Grade, Standard Grade, and Technical Grade), and Geography (Asia-Pacific, and More). Market Forecasts are Provided in Value (USD).

Geography Analysis

The Asia-Pacific region absorbed 54.20% of the global manganese market in 2025, primarily driven by China's demand, which was largely for steel and battery materials. India, buoyed by infrastructure investments and expansions in silico-manganese at Tata Steel and MOIL, also made significant contributions. Japan and South Korea have established themselves as key players in the electrolytic manganese metal industry, exporting high-purity products throughout the region. Despite being resource-rich, Africa processed only a small portion of its manganese ore domestically, with the bulk exported, a consequence of its limited refining capacity. The Middle East and Africa Manganese market is forecast to grow at a 5.86% CAGR to 2031, driven by South Africa's efforts to alleviate rail constraints and Saudi Arabia's push for downstream investments.

North America accounted for a smaller share of global manganese demand in 2025. However, with the commissioning of Element 25's refinery in Louisiana, the localization of battery-grade supply could bolster this share. Canada is actively pursuing manganese deposits in Quebec, while Mexican steel mills are ramping up capacity to cater to U.S. automotive clients. Europe, holding a moderate share, grapples with challenges from the Carbon Border Adjustment Mechanism (CBAM), nudging buyers towards Norwegian hydro-powered alloys and recycled feedstock. Notably, Eramet's "eraLow" brand is capitalizing on renewable electricity to secure contracts with EU flat-steel producers.

South America, contributing a smaller portion to global manganese demand, sees Brazil leading in alloy consumption and exports from Vale's Azul mine. Meanwhile, Argentina's burgeoning lithium sector is indirectly driving up demand for manganese, particularly for cathode precursors. With regional efforts to cultivate battery supply chains, there's potential for increased intra-continental processing, reshaping the Manganese market dynamics. The trajectory of Latin American nations moving up the value chain will hinge on infrastructure enhancements and green energy initiatives.

- African Rainbow Minerals Limited.

- Anglo American plc

- Assore Limited (Assmang Proprietary Limited)

- BHP

- CITIC LIMITED

- Consolidated Minerals Limited.

- Element 25 Limited

- Eramet

- Giyani Metals Corp

- Jupiter Mines Limited

- Manganese Metal Company (Pty) Ltd.

- MOIL LIMITED

- Ningxia Tianyuan Manganese Industry Group Co. Ltd

- NIPPON DENKO CO. LTD

- OM Holdings Ltd.

- POSCO M-TECH.

- South32

- Tata Steel

- Vale

- Vibrantz

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electrification of heavy-duty vehicles accelerates HP-Mn demand

- 4.2.2 Steelmakers' switch to hydrogen-DRI raises HC FeMn intensity

- 4.2.3 Western OEM off-take deals for HPMSM diversify supply

- 4.2.4 Infrastructure-grade silico-manganese demand in India and ASEAN

- 4.2.5 Geo-political ore disruptions (Gabon, Australia) lift prices

- 4.3 Market Restraints

- 4.3.1 Rapid LFP adoption curbs cathode-grade Mn growth

- 4.3.2 Ore-port bottlenecks in South Africa cap export volumes

- 4.3.3 High-carbon ferroalloy CO2-footprint faces carbon-border taxes

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Application

- 5.1.1 Alloys

- 5.1.2 Electrolytic Manganese Dioxide

- 5.1.3 Electrolytic Manganese Metals

- 5.1.4 Other Applications

- 5.2 By End-use Sector

- 5.2.1 Industrial

- 5.2.2 Construction

- 5.2.3 Power Storage and Electricity

- 5.2.4 Other End-use Sectors

- 5.3 By Ore Grade

- 5.3.1 Battery Grade

- 5.3.2 High Purity Grade

- 5.3.3 Standard Grade

- 5.3.4 Technical Grade

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/ Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 African Rainbow Minerals Limited.

- 6.4.2 Anglo American plc

- 6.4.3 Assore Limited (Assmang Proprietary Limited)

- 6.4.4 BHP

- 6.4.5 CITIC LIMITED

- 6.4.6 Consolidated Minerals Limited.

- 6.4.7 Element 25 Limited

- 6.4.8 Eramet

- 6.4.9 Giyani Metals Corp

- 6.4.10 Jupiter Mines Limited

- 6.4.11 Manganese Metal Company (Pty) Ltd.

- 6.4.12 MOIL LIMITED

- 6.4.13 Ningxia Tianyuan Manganese Industry Group Co. Ltd

- 6.4.14 NIPPON DENKO CO. LTD

- 6.4.15 OM Holdings Ltd.

- 6.4.16 POSCO M-TECH.

- 6.4.17 South32

- 6.4.18 Tata Steel

- 6.4.19 Vale

- 6.4.20 Vibrantz

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

锰矿开采市场:2026-2032年全球市场预测(依产品类型、纯度、加工方法、矿山类型和应用划分)锰市场:全球市场按产品类型、纯度等级、技术、形态和应用分類的预测 - 2026-2032 年电解二氧化锰市场:按产品类型、製造流程、原料来源、应用和终端用户产业分類的全球预测,2026年至2032年

锰矿开采市场:2026-2032年全球市场预测(依产品类型、纯度、加工方法、矿山类型和应用划分)锰市场:全球市场按产品类型、纯度等级、技术、形态和应用分類的预测 - 2026-2032 年电解二氧化锰市场:按产品类型、製造流程、原料来源、应用和终端用户产业分類的全球预测,2026年至2032年 全球硅锰市场规模、份额、趋势和成长分析报告(2026-2034年)

全球硅锰市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球硅锰市场报告2026年全球锰铁市场报告

2026年全球硅锰市场报告2026年全球锰铁市场报告 全球锰铁市场-产业规模、份额、趋势、机会及预测(依等级、应用、生产方法、区域及竞争格局划分,2021-2031年预测)

全球锰铁市场-产业规模、份额、趋势、机会及预测(依等级、应用、生产方法、区域及竞争格局划分,2021-2031年预测) 锰市场规模、份额和成长分析(按类型、矿石品位、形态、应用、最终用途和地区划分)-2026-2033年产业预测

锰市场规模、份额和成长分析(按类型、矿石品位、形态、应用、最终用途和地区划分)-2026-2033年产业预测 电解二氧化锰市场规模、份额及成长分析(按类型、等级、电解製程、应用、最终用户及地区划分)-2026-2033年产业预测

电解二氧化锰市场规模、份额及成长分析(按类型、等级、电解製程、应用、最终用户及地区划分)-2026-2033年产业预测 氧化锰(MnO):全球市场份额和排名、总收入和需求预测(2025-2031 年)

氧化锰(MnO):全球市场份额和排名、总收入和需求预测(2025-2031 年)