|

市场调查报告书

商品编码

1910502

端点检测与反应 (EDR):市场占有率分析、产业趋势与统计、成长预测 (2026-2031)Endpoint Detection And Response (EDR) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

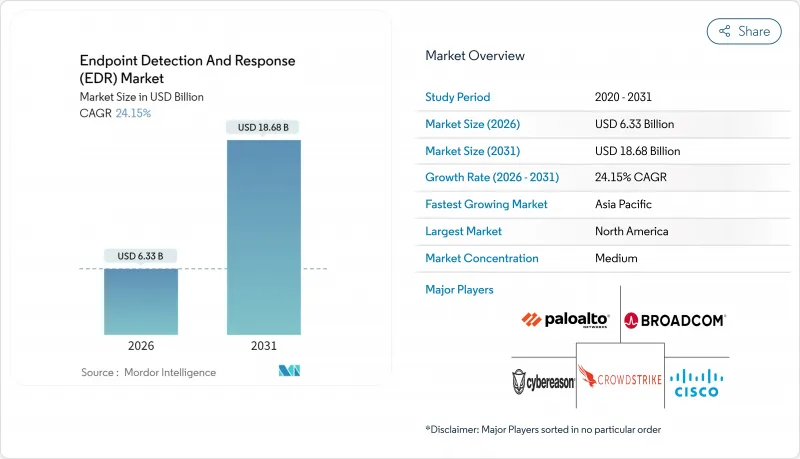

预计到 2026 年,终端检测与响应 (EDR) 市场规模将达到 63.3 亿美元。

这意味着从 2025 年的 51 亿美元成长到 2031 年的 186.8 亿美元,2026 年至 2031 年的年复合成长率(CAGR)为 24.15%。

美国联邦政府的强制规定推动了EDR(端点检测与回应)的成长,该规定要求所有民用机构在2024年9月前实施EDR,并要求在2025年1月后将覆盖范围扩展到云端工作负载和身分系统。此外,勒索软体即服务(RaaS)的商业化、向零信任安全营运中心的转型以及对统一代理架构的强劲需求,都在加速平台的普及。以Sophos和Palo Alto Networks的收购为例,供应商整合正在重塑竞争格局,而託管服务管道正在拓展其在对成本敏感的中小企业市场的影响力。内核级EDR工具包和人工智慧驱动的警报洪流等技术挑战虽然限制了利润率,但尚未扼杀整体成长动能。

全球端点检测与反应 (EDR) 市场趋势与洞察

联邦政府电子资料审查 (EDR) 强制令的快速扩展(第 14028 号行政命令)

14028号行政命令要求300多个美国联邦机构在2024年9月前实施全光谱侦测与回应(EDR)解决方案,并于2025年1月将范围扩大至云端工作负载与身分遥测。国防工业基地承包商也面临类似的要求,并在2024年将其EDR预算增加了三倍。关键基础设施供应商采用了FedRAMP授权的解决方案,以符合美国网路安全和基础设施安全局(CISA)的新绩效目标。州和地方政府也与联邦标准接轨,以确保获得津贴资格。因此,拥有政府云端认证的供应商被列为优先考虑对象。随着这项命令扩展到盟国,端点侦测与回应(EDR)市场正经历持续的合规主导成长。

勒索软体即服务 (RaaS) 的激增

诸如 LockBit 3.0 和 BlackCat 等商业勒索软体工具包降低了网路犯罪分子的准入门槛,导致 2024 年报告的勒索软体攻击事件达到 2323 起,平均赎金高达 530 万美元。在医疗保健产业遭受 389 起攻击,影响 4,500 万份病患记录后,监管机构加强了对 HIPAA 安全规则的解读,强制实施 EDR(端点侦测与回应)。由于业务中断成本是赎金的 23 倍,财务长们越来越将 EDR 投资视为营运风险保险。这种经济转变将推动端点检测与反应 (EDR) 市场在所有垂直领域持续实现两位数成长。

凭证窃取 EDR 工具包

诸如 EDRKillShifter 和 Terminator 之类的开放原始码框架利用内核钩子来停用或卸载端点代理,在实验室评估中实现了高达 90% 的规避成功率。这些框架售价低至 500 美元,它们扩大了攻击者的存取权限,迫使供应商开发高成本的防篡改技术,从而延长了产品发布週期。由于买家需要等待新的防御措施证明其能够抵御这些工具包,因此采购流程会暂时中断。虽然这会抑制短期成长,但却能促进端点检测与反应 (EDR) 市场的长期创新。

细分市场分析

到2025年,端点防护平台将占总收入的42.62%,凸显了企业对整合了防毒、防火墙和进阶侦测功能的单一供应商套件的依赖。云端原生EDR与云端工作负载保护相结合,是成长最快的细分市场,复合年增长率高达26.20%,这得益于微服务和无伺服器运算的普及,而传统代理无法保护这些技术。身分威胁侦测的整合标誌着市场正朝着全面的风险敞口管理方向发展,而託管式EDR和MDR管道即使对于中小企业也能提供企业级的覆盖范围。随着企业淘汰冗余的独立解决方案并采用整合式解决方案,与整合代理相关的端点检测与回应(EDR)市场规模预计将会扩大。

次要影响包括:资料共用API 的竞争加剧,这些 API 能够融合身分资讯、云端工作负载和端点遥测资料;以及对跨这些资料层面运行的行为分析的需求增加。能够提供具有跨域可见性的轻量级代理的供应商将在更新周期中获得优先供应商地位,而专注于单一产品的供应商则面临商品化的风险,除非它们整合或合併到更广泛的 XDR 生态系统中。这一趋势正在重塑端点检测与反应 (EDR) 市场的差异化标准。

到2025年,云端交付解决方案将占据端点侦测与回应 (EDR) 市场规模的66.48%,并随着远距办公使分散式IT成为常态,到2031年将以25.90%的复合年增长率持续成长。自动更新、集中式策略管理和扩充性的威胁情报来源为分散式办公室团队提供了强大的优势。国防和受监管的金融业仍在继续采用本地部署和空气间隙部署,这推动了对兼顾资料主权要求和现代检测能力的混合解决方案的需求。

当企业将工作负载迁移到 IaaS 平台时,力求在终端和虚拟机器之间实现同等的安全防护,这推动了对基于 SaaS 的检测解决方案的需求。付费使用制将资本支出转化为可预测的营运成本,这对成本负责人来说是一项关键优势。因此,终端检测与回应 (EDR) 市场的发展与云端采用率的成长趋势相呼应,只有在法规明确禁止云端处理的领域,本地专用节点才仍然具有意义。

区域分析

到2025年,北美将占据终端侦测与回应 (EDR) 市场37.02%的份额,共用第14028号行政命令的遵守以及私营部门威胁情报共享的进步。这项在2025年1月生效的行政命令将云端工作负载和身分系统纳入其适用范围,使可覆盖的终端范围扩大了一倍,并提升了供应商的收入前景。诸如CISA的自动化指标共用计划等措施正在增强安全营运中心 (SOC) 的遥测能力,在不增加负责人负担的情况下提高检测准确率。

随着中国、日本、印度和韩国推行全国性的网路安全现代化计划,预计到2031年,亚太地区的复合年增长率将达到26.10%。云端优先的基础设施部署、行动优先的工作模式以及日益增多的国家支援型网路攻击活动,正推动企业转向基于SaaS的EDR解决方案。中国《资料安全法》和印度《数位个人资讯保护法》等国家合规法规要求企业持续监控终端。拥有区域资料中心和本地威胁调查团队的供应商,在这个高速成长的终端侦测与回应(EDR)市场领域获得了竞争优势。

欧洲预计将在NIS2指令的推动下稳步发展。该指令于2024年10月将强制网路安全措施的范围扩大到18个关键领域。 GDPR的违规通知处罚进一步提升了EDR在经营团队的优先顺序。德国和法国正透过BSI和ANSSI框架主导EDR的普及,而英国则在其脱欧后的战略中优先考虑主权韧性和多边合作。在欧盟资助检测技术升级的推动下,东欧地区EDR的普及速度加快。儘管面临宏观经济压力,这些政策主导的趋势仍然维持对端点检测与回应产业的强劲需求。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 联邦政府电子资料审查 (EDR) 强制令的快速扩展(第 14028 号行政命令)

- 勒索软体即服务激增

- 向以身分为中心的零信任安全营运中心转型

- 整合代理平台的需求(降低成本)

- 云端工作负载保护整合激增

- 中小企业主导MSP/MDR通路的需求不断增长

- 市场限制

- 凭证窃取 EDR 杀手工具包

- 配置错误的AI模型会导致警报氾滥

- CrowdStrike式代理程式更新中断

- 开放原始码代理分支加剧了价格压力

- 产业价值链分析

- 监管环境

- 技术展望-基于图的相关性分析、生成式人工智慧系统

- 波特五力分析

第五章 市场规模与成长预测

- 按解决方案类型

- 端点保护平台(EPP+EDR)

- 云端原生 EDR/CWP 集成

- 身分威胁侦测与回应 (ITDR)

- 管理EDR/MDR

- 按部署模式

- 云端提供的

- 本机部署/空气间隙环境

- 按最终用户行业划分

- BFSI

- 卫生保健

- 资讯科技和电信

- 工业与国防

- 零售与电子商务

- 能源与公用事业

- 製造业

- 其他终端用户产业

- 按公司规模

- 小型企业

- 大公司

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东

- 以色列

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- CrowdStrike Holdings Inc.

- Microsoft Corporation(Defender for Endpoint)

- SentinelOne Inc.

- VMware by Broadcom(Carbon Black)

- Trend Micro Inc.

- Cisco Systems Inc.

- Palo Alto Networks Inc.(Cortex XDR)

- Sophos Group plc

- Bitdefender SRL

- Check Point Software Technologies Ltd.

- Kaspersky Lab JSC

- McAfee LLC

- Elastic NV

- Cybereason Inc.

- Trellix(Musarubra US LLC)

- Fortinet Inc.(FortiEDR)

- ESET spol. s ro

- WithSecure Plc

- Red Canary Inc.

- Huntress Labs Inc.

第七章 市场机会与未来展望

The endpoint detection and response market size in 2026 is estimated at USD 6.33 billion, growing from 2025 value of USD 5.1 billion with 2031 projections showing USD 18.68 billion, growing at 24.15% CAGR over 2026-2031.

Growth is propelled by binding U.S. federal mandates that require all civilian agencies to deploy EDR by September 2024 and, from January 2025, to extend coverage to cloud workloads and identity systems. Ransomware-as-a-service commercialization, the pivot to zero-trust security operations centers, and strong demand for unified-agent architectures further accelerate platform adoption. Vendor consolidation, highlighted by Sophos and Palo Alto Networks acquisitions, is reshaping competitive dynamics while managed service channels expand reach into the cost-sensitive SME segment. Technical headwinds such as kernel-level EDR-killer toolkits and AI-driven alert floods temper margins yet have not derailed overall momentum.

Global Endpoint Detection And Response (EDR) Market Trends and Insights

Soaring Federal EDR Mandates (EO 14028)

Executive Order 14028 forced more than 300 U.S. federal agencies to implement full-spectrum EDR by September 2024, then broadened the scope in January 2025 to include cloud workloads and identity telemetry. Contractors to the defense industrial base mirrored these requirements, quadrupling EDR budgets in 2024, while critical-infrastructure operators adopted FedRAMP-authorized solutions to align with new CISA performance goals. State and local governments are now harmonizing with federal benchmarks to secure grant eligibility. Vendors holding government cloud certifications, therefore, enjoy preferential shortlists. As mandates spill into allied nations, the endpoint detection and response market gains an enduring compliance-driven stimulus.

Ransomware-as-a-Service Explosion

Commercialized ransomware kits such as LockBit 3.0 and BlackCat lowered the barrier to entry for cybercriminals, driving 2,323 reported ransomware events in 2024 and lifting average ransom demands to USD 5.3 million. Healthcare bore 389 of those incidents affecting 45 million patient records, causing regulators to tighten HIPAA security-rule interpretations that now favour mandatory EDR. CFOs increasingly view EDR spend as operational-risk insurance because business interruption costs reach 23 times the ransom payout. This economics shift sustains double-digit expansion of the endpoint detection and response market across all verticals.

Credential-Stealing EDR-Killer Toolkits

Open-source frameworks like EDRKillShifter and Terminator exploit kernel hooks to blind or uninstall endpoint agents, achieving up to 90% bypass success in lab evaluations. Availability for as little as USD 500 widens attacker access, forcing vendors into costly tamper-proof engineering sprints and lengthening release cycles. Temporary procurement delays arise when buyers wait for proof that new defenses defeat these toolkits, trimming short-term expansion yet reinforcing long-term innovation in the endpoint detection and response market.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Identity-Centred Zero-Trust SOC

- Demand for Unified Agent Platform (Cost Down)

- Mis-Configured AI Models Causing Alert Flood

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Endpoint Prevention Platform accounted for 42.62% of 2025 revenue, underscoring enterprise reliance on single-vendor suites that unify antivirus, firewall, and advanced detection. Cloud-native EDR bundled with cloud workload protection is the fastest-growing subsegment at 26.20% CAGR, benefiting from microservice adoption and serverless compute that traditional agents cannot secure. Identity threat detection integration signals the market's evolution toward holistic exposure management, while managed EDR and MDR channels bring enterprise-grade coverage to smaller firms. The endpoint detection and response market size tied to unified agents is projected to multiply as organizations decommission overlapping point solutions in favour of a consolidated stack.

Second-order effects include heightened competition for data-sharing APIs that enable identity, cloud workload, and endpoint telemetry fusion, as well as rising demand for behavioural analytics that operate across these data planes. Vendors able to deliver lightweight agents with cross-domain visibility earn favoured-supplier status in renewal cycles. Conversely, point-product specialists risk commoditization unless they integrate or merge into broader XDR ecosystems. This dynamic is reshaping differentiation criteria inside the endpoint detection and response market.

Cloud-delivered solutions controlled 66.48% of the endpoint detection and response market size in 2025 and will continue expanding at a 25.90% CAGR to 2031 as remote work normalizes decentralized IT. Automatic updates, centralized policy, and elastic threat-intelligence feeds provide compelling advantages for distributed workforces. On-prem and air-gapped deployments persist in defense and regulated finance, driving hybrid offerings that reconcile data-sovereignty mandates with modern detection capabilities.

Enterprises shifting workloads to infrastructure-as-a-service platforms seek parity of protection across endpoints and virtual machines, amplifying demand for SaaS-delivered detection. Consumption-based pricing converts capital outlays into predictable operating expenses, a key benefit for cost controllers. The endpoint detection and response market, therefore, mirrors the broader cloud adoption curve, with specialized on-prem nodes retaining relevance only where regulation explicitly forbids cloud processing.

The Endpoint Detection and Response Market Report is Segmented by Solution Type (Endpoint Prevention Platform, Cloud-Native EDR/CWP-Integrated, and More), Deployment Model (Cloud-Delivered, On-prem/Air-gapped), End-User Vertical (BFSI, Healthcare, and More), Enterprise Size (Small and Medium Enterprises, Large Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held a 37.02% endpoint detection and response market share in 2025 owing to Executive Order 14028 compliance and sophisticated private-sector threat intelligence sharing. The January 2025 order that added cloud workloads and identity systems effectively doubled the addressable endpoint universe, enhancing vendor revenue outlook. Programs such as CISA's Automated Indicator Sharing feed enrich SOC telemetry, sharpening detection without excessive analyst workload.

Asia-Pacific is projected to log a 26.10% CAGR through 2031 as China, Japan, India, and South Korea roll out nationwide cybersecurity modernization programs. Cloud-first infrastructure deployments, mobile-first workforces, and escalating state-sponsored attack activity pivot organizations toward SaaS-delivered EDR. Domestic compliance statutes such as China's Data Security Law and India's Digital Personal Data Protection Act compel continuous endpoint visibility. Vendors with regional data centers and local threat hunting teams gain competitive traction in this high-growth quadrant of the endpoint detection and response market.

Europe delivers steady expansion under the NIS2 Directive, which broadened mandatory cyber controls across 18 critical sectors in October 2024. GDPR's breach-notification fines further elevate EDR to boardroom priority. Germany and France spearhead adoption via BSI and ANSSI frameworks, while the U.K.'s post-Brexit strategy emphasizes sovereign resilience and multilateral partnerships. Eastern Europe accelerates through EU funding tranches that subsidize detection technology upgrades. These policy-driven dynamics maintain a healthy pipeline for the endpoint detection and response industry despite macroeconomic pressures.

- CrowdStrike Holdings Inc.

- Microsoft Corporation (Defender for Endpoint)

- SentinelOne Inc.

- VMware by Broadcom (Carbon Black)

- Trend Micro Inc.

- Cisco Systems Inc.

- Palo Alto Networks Inc. (Cortex XDR)

- Sophos Group plc

- Bitdefender SRL

- Check Point Software Technologies Ltd.

- Kaspersky Lab JSC

- McAfee LLC

- Elastic N.V.

- Cybereason Inc.

- Trellix (Musarubra US LLC)

- Fortinet Inc. (FortiEDR)

- ESET spol. s r.o.

- WithSecure Plc

- Red Canary Inc.

- Huntress Labs Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Soaring Federal EDR Mandates (EO 14028)

- 4.2.2 Ransomware-as-a-Service Explosion

- 4.2.3 Shift to Identity-centred Zero-Trust SOC

- 4.2.4 Demand for Unified Agent Platform (Cost Down)

- 4.2.5 Surge in Cloud Workload Protection Integration

- 4.2.6 SMB-led MSP/MDR Channel Pull

- 4.3 Market Restraints

- 4.3.1 Credential-stealing EDR-killer Toolkits

- 4.3.2 Mis-configured AI Models causing Alert Flood

- 4.3.3 CrowdStrike-style Agent Update Outages

- 4.3.4 Open-source Agent Forks Driving Price Pressure

- 4.4 Industrial Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook - Graph-based Correlation, Gen-AI SOC

- 4.7 Porter's Five Forces Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Solution Type

- 5.1.1 Endpoint Prevention Platform (EPP + EDR)

- 5.1.2 Cloud-native EDR / CWP-Integrated

- 5.1.3 Identity-Threat Detection and Response (ITDR)

- 5.1.4 Managed EDR / MDR

- 5.2 By Deployment Model

- 5.2.1 Cloud-Delivered

- 5.2.2 On-prem / Air-gapped

- 5.3 By End-User Vertical

- 5.3.1 BFSI

- 5.3.2 Healthcare

- 5.3.3 IT and Telecom

- 5.3.4 Industrial and Defense

- 5.3.5 Retail and e-Commerce

- 5.3.6 Energy and Utilities

- 5.3.7 Manufacturing

- 5.3.8 Other End-User Vertical

- 5.4 By Enterprise Size

- 5.4.1 Small and Medium Enterprises (SME)

- 5.4.2 Large Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CrowdStrike Holdings Inc.

- 6.4.2 Microsoft Corporation (Defender for Endpoint)

- 6.4.3 SentinelOne Inc.

- 6.4.4 VMware by Broadcom (Carbon Black)

- 6.4.5 Trend Micro Inc.

- 6.4.6 Cisco Systems Inc.

- 6.4.7 Palo Alto Networks Inc. (Cortex XDR)

- 6.4.8 Sophos Group plc

- 6.4.9 Bitdefender SRL

- 6.4.10 Check Point Software Technologies Ltd.

- 6.4.11 Kaspersky Lab JSC

- 6.4.12 McAfee LLC

- 6.4.13 Elastic N.V.

- 6.4.14 Cybereason Inc.

- 6.4.15 Trellix (Musarubra US LLC)

- 6.4.16 Fortinet Inc. (FortiEDR)

- 6.4.17 ESET spol. s r.o.

- 6.4.18 WithSecure Plc

- 6.4.19 Red Canary Inc.

- 6.4.20 Huntress Labs Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

基于卫星的甲烷检测市场:按感测器类型、轨道类型、部署模式、资料产品和应用划分-全球预测,2026-2032年

基于卫星的甲烷检测市场:按感测器类型、轨道类型、部署模式、资料产品和应用划分-全球预测,2026-2032年 乳房红外线检测器市场规模、份额和成长分析:按技术类型、应用、最终用户、分销管道和地区划分 - 2026-2033 年行业预测三重红外线氢焰探测器市场:按探测器类型、安装类型、应用、最终用户和分销管道划分 - 全球预测 2026-2032全球耐腐蚀热熔管道黏合剂市场(按黏合剂类型、层体系、应用方法、形态和最终用途产业划分)预测(2026-2032年)气泡检测器市场按类型、技术、销售管道和应用划分,全球预测(2026-2032年)远端自动抄表系统市场(按组件、电錶类型、通讯技术、部署类型和最终用户划分),全球预测,2026-2032年

乳房红外线检测器市场规模、份额和成长分析:按技术类型、应用、最终用户、分销管道和地区划分 - 2026-2033 年行业预测三重红外线氢焰探测器市场:按探测器类型、安装类型、应用、最终用户和分销管道划分 - 全球预测 2026-2032全球耐腐蚀热熔管道黏合剂市场(按黏合剂类型、层体系、应用方法、形态和最终用途产业划分)预测(2026-2032年)气泡检测器市场按类型、技术、销售管道和应用划分,全球预测(2026-2032年)远端自动抄表系统市场(按组件、电錶类型、通讯技术、部署类型和最终用户划分),全球预测,2026-2032年 氢气洩漏检测器市场-2025-2030年预测

氢气洩漏检测器市场-2025-2030年预测 多角度光散射(MALS)检测器:全球市场份额和排名、总收入和需求预测(2025-2031年)

多角度光散射(MALS)检测器:全球市场份额和排名、总收入和需求预测(2025-2031年) 多角度光散射 (MALS)检测器市场:全球至 2025 年

多角度光散射 (MALS)检测器市场:全球至 2025 年 全球气泡探测器市场

全球气泡探测器市场