|

市场调查报告书

商品编码

1910583

家用冷藏库和冷冻库:市场份额分析、行业趋势和统计数据、成长预测(2026-2031)Household Refrigerators And Freezers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

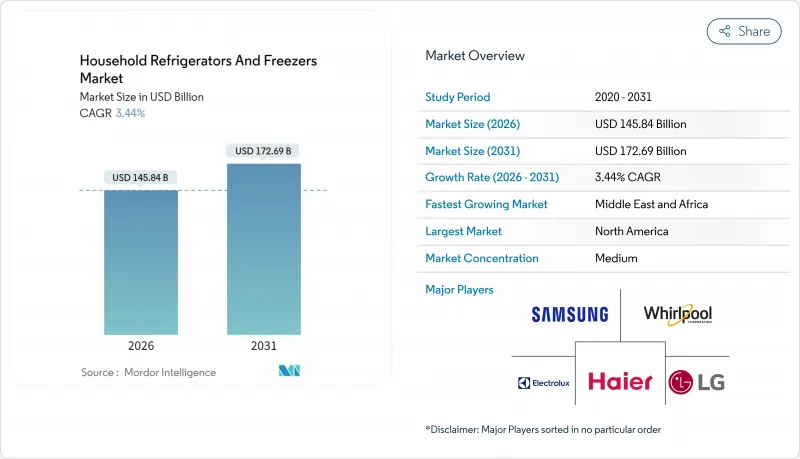

预计到 2026 年,家用冷藏库和冷冻库市场价值将达到 1,458.4 亿美元,高于 2025 年的 1,409.9 亿美元。

预计到 2031 年,该产业规模将达到 1,726.9 亿美元,2026 年至 2031 年的复合年增长率为 3.44%。

北美和欧盟的能源效率法规、高全球暖化潜值(GWP)冷媒的快速淘汰以及亚洲新兴国家的稳步都市化进程,共同推动了家用冰箱和冷柜市场的渐进式持续扩张。对智慧连网机型的需求不断增长,R600a和R290等天然冷媒的日益普及,以及成熟经济体持续的厨房维修週期,进一步促进了高级产品的市场需求。同时,由于半导体短缺和部分开发中国家电费上涨,生产前置作业时间延长,限制了更换週期。因此,领先的製造商正致力于加强内部零件采购,建造区域工厂以缩短供应链,并增加对人工智慧驱动的食品管理功能的研发投入。这些趋势共同推动了家用冷藏库和冷冻库市场的持续创新和价值成长。

全球家用冷藏库及冷冻库市场趋势及洞察

节能法规

在成熟经济体中,由于能源效率标准的日益严格,产品更新换代週期正在加速。美国能源局已最终确定2029年和2030年的冷藏库标准,要求年度能耗降低两位数百分比。同时,欧盟修订后的氟碳化合物法规将于2026年1月起禁止在家用电器中使用含氟冷媒,并敦促全面过渡到异丁烷或丙烷系统。主要原始设备製造商(OEM)已完成向天然气冷媒的过渡。通用电气家电公司(GE Appliances)已于2024年完成了R600a冷媒的多年推广,并指出其能源效率提升了10%,且臭氧消耗潜能值为零。诸如「能源之星」(ENERGY STAR)之类的配套标籤计划可以识别冷媒类型,并鼓励消费者选择全球暖化潜势值(GWP)更低的替代品。

新兴亚洲地区可支配所得不断增长

新兴亚洲市场首次购屋需求强劲,主要得益于中产阶级的壮大和都市化的加速。印度冷媒市场与家电普及率密切相关,预计未来五年将以6-8%的复合年增长率成长,这主要得益于低全球暖化潜值(GWP)冷媒的日益普及和家电拥有率的提高。中国政府于2025年1月扩大了八类家电的更换补贴计划,将直接惠及海尔等主要製造商,海尔约占国内冷藏库市场40-50%的份额。该地区的消费模式偏向大容量和多嵌入式设计,中国消费者也越来越倾向选择嵌入式冰箱,而嵌入式冰箱的平均价格是传统冰箱的1.4倍。复杂的监理合规也是一大挑战。印度于2021年批准了《基加利修正案》,该修正案将于2024年开始实施氢氟碳化合物(HFC)的逐步淘汰要求,这将为Refex Industries等供应商创造机会。该公司在 2024-2025 财年供应了 1370 公吨冷媒,其中包括透过与 LG 和 Voltas 的合作。

半导体供应不稳定

持续的半导体短缺已将高端冷藏库的前置作业时间延长至六个月以上。据Thermador公司称,包括对开门冰箱在内的所有主要品类都受到电源管理积体电路和微控制器供不应求的限制。这种影响不仅限于高端品牌,还波及整体现代冷藏库系统节能智慧功能所必需的半导体和电子元件。在与冷藏库共用供应链的印度空调市场,零件短缺可能导致单价上涨18-24美元(1500-2000卢比,涨幅4-5%)。此外,压缩机短缺和BIS认证延迟也使每台冰箱的成本增加了12-14.50美元(1000-1200卢比)。中国製造商正在透过供应链多元化来应对这项挑战。海尔在全球拥有143个製造地,而美的则营运40多个大型生产设施,降低了物流和贸易风险。

细分市场分析

到2025年,上置式冷冻冷藏库将主导家用冷藏库和冷冻库市场,占42.79%的市场份额,这主要得益于其价格优势和紧凑的面积。然而,法式对开门冰箱细分市场预计将在2031年之前保持最高的复合年增长率(CAGR),达到8.37%,这主要受消费者对更宽敞的内部空间、更宽的搁架和更先进的温控区域的追求所驱动。三星2025年推出的Bespoke AI法式对开门冰箱产品线整合了混合压缩机、珀尔帖冷却技术和食物识别视觉软体,这项组合在提升产品感知价值的同时,也满足了即将实施的能源标准。虽然并排式冰箱因其生鲜食品和冷冻食品比例均衡而在北美仍然很受欢迎,但下置式冷冻冰箱正受到注重健康的消费者的青睐,他们更看重的是能够轻鬆取用食材。目前,壁厚减薄是冰箱创新的方向。惠而浦的SlimTech真空隔热技术透过将柜体壁厚度减少66%,同时增加25%的内部容积,直接解决了都市区空间有限的问题。消费者对一体化厨房的需求日益增长,使得能够与橱柜无缝融合的多门冰箱更具优势,从而扩大了家用冷藏库和冷冻库市场的高端机会。

次要趋势包括互联功能和抗菌内胆的普及。 LG的门中门「敲击」面板使用户能够提前查看内部物品,从而减少冷气流失和年度能耗。内建的UV-C紫外线杀菌模组可有效抑制异味和细菌滋生。根据中国零售分析公司预测,2024年上半年,多门冰箱将占线上销售额的58%以上,印证了全球冰箱设计向分门式布局的转变趋势。为了确保更高的利润率,製造商正根据生活风格主题(例如家庭、健康、都会生活)对产品线进行细分。预计到2031年,这些多方面的设计变革将显着推动家用冷藏库和冷冻库市场规模的成长。

区域分析

北美地区推动了营收成长,预计到2025年将占据家用冷藏库和冷冻库市场31.05%的份额,这主要得益于市场饱和、强劲的更换週期以及对智慧功能的需求。三星和LG都专注于美国製造的嵌入式产品,分别利用其Dacor和Signature Kitchen Suite品牌与建筑商建立合作关係,并实现了两位数的溢价成长。通用电气家电计画在2029年投资30亿美元,扩大在美国11家工厂的冷藏库产能,展现持续的回流动能。儘管该地区3.74%的复合年增长率低于全球平均水平,但由于其稳定且不断改善的价格结构,它仍然是家用冷藏库和冷冻库市场中盈利能力最强的地区。亚太地区正经历最快的复合年增长率,达到6.32%,这主要得益于都市化、首次购屋者的需求以及本地製造业投资。预计2024年,中国家电出货量将达到44.8亿台,年增20.8%。这反映了出口多元化和国内补贴机制。印度的家用电器产业正受益于中产阶级的壮大,儘管人均普及率仍然较低。与此同时,零件短缺推高了价格。当地法规鼓励使用天然冷媒,而印度基于《基加利协议》逐步淘汰氢氟碳化合物(HFC)的倡议,正在推动中檔机型采用R290冷媒,进一步契合了应对气候变迁的措施。

欧洲预计将以2.84%的复合年增长率实现温和成长,充满挑战的经济状况和监管转型虽然增加了合规成本,但也刺激了创新。欧盟的《氟碳化合物法规》将于2026年1月起禁止在家用冷藏库中使用含氟温室气体,这给产业带来了直接的转型压力。然而,像博世家电(BSH)这样的製造商正在大力投资以符合新规,包括在墨西哥新建一家製冷工厂,并扩大研发投入(总额近8.5亿欧元/9.18亿美元)。欧洲产业协会强调,监管碎片化、电力成本是美国两到三倍的高昂成本以及关键材料供应链集中等因素,都带来了严峻的竞争挑战。中东和非洲地区预计将以6.87%的复合年增长率实现最快增长,这得益于战略投资,例如夏普在埃及投资3000万美元成立合资企业,以及海尔在该地区26.8%的销售额增长。这主要归功于当地生产和产品开发,以适应不稳定的电力基础设施。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 主流节能法规

- 新兴亚洲国家可支配所得不断成长

- 都市区的住宅增长和厨房维修

- 全通路零售的兴起

- 碳中和冷媒的引入,却鲜少受到关注。

- 基于人工智慧的压缩机预测性维护

- 市场限制

- 半导体供应链波动

- 开发中国家的高电费

- 稀土元素磁铁价格波动风险

- 在线二手家电市场的扩张

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按类型

- 上置式冷冻冷藏库

- 底部开启式冷冻库附冷藏库

- 对开门冷藏库

- 法式对开门冷藏库

- 按产能

- 少于300公升

- 300至500升

- 超过500公升

- 透过分销管道

- 多品牌商店

- 专卖店

- 在线的

- 其他分销管道

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 秘鲁

- 智利

- 阿根廷

- 南美洲其他地区

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 比荷卢经济联盟(比利时、荷兰、卢森堡)

- 北欧国家(丹麦、芬兰、冰岛、挪威、瑞典)

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 东南亚(新加坡、马来西亚、泰国、印尼、越南、菲律宾)

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Whirlpool Corp.

- Haier Smart Home Co.

- LG Electronics Inc.

- Samsung Electronics Co.

- Electrolux AB

- Panasonic Corp.

- Bosch-Siemens Hausgerate GmbH

- Midea Group

- Hisense Co.

- Hitachi Global Life Solutions

- GE Appliances(Haier)

- Liebherr-Hausgerate

- Sub-Zero Group

- Arcelik AS(Beko, Grundig)

- Godrej Appliances

- Sharp Corp.

- TCL Technology

- PC Richard & Son(private label)

- Glen Dimplex(Home Appliances)

- SMEs & Local Players(collective)

第七章 市场机会与未来展望

The household refrigerators and freezers market size in 2026 is estimated at USD 145.84 billion, growing from 2025 value of USD 140.99 billion with 2031 projections showing USD 172.69 billion, growing at 3.44% CAGR over 2026-2031.

Energy-efficiency mandates in North America and the European Union, the rapid phase-out of high-GWP refrigerants, and steady urbanization across emerging Asia together underpin this moderate yet durable expansion. Rising demand for smart-connected models, wider adoption of natural refrigerants such as R600a and R290, and ongoing kitchen renovation cycles in mature economies further stimulate premium product uptake. At the same time, semiconductor shortages continue to lengthen production lead times, while elevated electricity tariffs in several developing countries temper replacement cycles. Leading manufacturers are therefore doubling down on in-house component sourcing, building regional factories to shorten supply chains, and intensifying R&D outlays targeting AI-driven food-management functions. These dynamics collectively sustain innovation while supporting incremental value growth throughout the household refrigerators and freezers market.

Global Household Refrigerators And Freezers Market Trends and Insights

Energy-Efficiency Regulations

Mandatory efficiency upgrades are accelerating replacement cycles across mature economies. The U.S. Department of Energy has finalized refrigerator standards taking effect in 2029 and 2030, demanding double-digit percentage cuts in annual energy use. In parallel, the EU's revised F-Gas Regulation bans fluorinated refrigerants in domestic units from January 2026, prompting full conversion to isobutane or propane systems. Leading OEMs have already transitioned to natural gases; GE Appliances finished a multiyear R600a roll-out during 2024, citing 10% efficiency gains and zero ozone-depletion potential. Complementary labelling schemes such as ENERGY STAR now spotlight refrigerant type, nudging consumers toward low-GWP alternatives.

Rising Disposable Income in Emerging Asia

Emerging Asian markets demonstrate robust first-time purchase demand driven by middle-class expansion and urbanization trends. India's refrigerant market, closely tied to appliance penetration, is forecast to grow 6-8% CAGR over the next five years as adoption of low-GWP refrigerants increases alongside appliance ownership. China's government trade-in subsidy program for eight home appliance categories, expanded in January 2025, directly benefits major manufacturers like Haier, which holds an estimated 40-50% share in the domestic refrigeration segment. The region's demand patterns favor larger-capacity units and multi-door configurations, with Chinese consumers increasingly selecting embedded (built-in) designs that command average prices 1.4x conventional models. Regulatory compliance adds complexity, as India's ratification of the Kigali Amendment in 2021 initiated HFC phase-down requirements in 2024, creating opportunities for suppliers like Refex Industries, which supplied 1,370 MT of refrigerants in FY24-25 with partnerships including LG and Voltas.

Semiconductor Supply Volatility

Persistent chip shortages extend refrigerator led times to upward of six months for high-end brands. Thermador notes that every major category, including side-by-side units, remains constrained owing to power-management IC and microcontroller gaps. The impact extends beyond premium brands, as semiconductors and electronic components are integral to modern refrigeration systems' energy efficiency and smart features. India's air conditioning market, which shares component supply chains with refrigeration, faces component shortages that may increase unit prices by USD 18-24 (Rs 1,500-2,000) (4-5%), with compressor shortages and BIS certification delays adding USD 12 -14.50 (Rs 1,000-1,200) per unit. Chinese manufacturers are responding through supply chain diversification, with Haier expanding to 143 global manufacturing centers and Midea operating over 40 major production bases to mitigate logistics and trade risks.

Other drivers and restraints analyzed in the detailed report include:

- Urban Housing Growth & Kitchen Renovations

- Omnichannel Retail Expansion

- High Electricity Tariffs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Top-freezer units accounted for 42.79% of the household refrigerators and freezers market share in 2025, anchoring sales through their price advantage and compact footprint. Yet the French-door sub-segment is forecast to register the highest 8.37% CAGR through 2031 as consumers gravitate toward spacious interiors, wide shelves, and advanced climate zones. Samsung's 2025 Bespoke AI French-door portfolio integrates hybrid compressor-Peltier cooling and Food Recognition Vision software, a combination that elevates perceived value while meeting forthcoming energy benchmarks. Side-by-side configurations remain popular in North America for their balanced fresh-to-frozen ratio, whereas bottom-freezer models gain traction among wellness-focused buyers prioritizing eye-level produce access. Innovation now targets wall-thickness reduction; Whirlpool's SlimTech vacuum insulation trims cabinet walls by 66% and boosts interior volume by 25%, directly addressing urban space constraints. Growing demand for integrated kitchens further favors multi-door units that blend seamlessly with cabinetry, broadening premium opportunities within the household refrigerators and freezers market.

Second-tier trends include connectivity adoption and antimicrobial interiors. LG's door-in-door "knock" panels let users preview contents, cutting cold-air loss and lowering annual consumption, while built-in UV-C modules promise odor and germ suppression. Chinese retail analytics show that multi-door styles surpassed 58% online share in 2024H1, reinforcing a global pivot toward compartmentalized layouts. Manufacturers are therefore segmenting lines by lifestyle themes, family, wellness, and urban loft to command higher margins. These multifaceted design shifts collectively underpin the French-door segment's outsize contribution to household refrigerators and freezers market size expansion through 2031.

The Household Refrigerators and Freezers Market Report is Segmented by Type (Top-Freezer Refrigerators, Bottom-Freezer Refrigerators, Side-By-Side Refrigerators, French Door Refrigerators), Capacity (Less Than 300 Litres, 300 - 500 Litres, Greater Than 500 Litres), Distribution Channel (Multi-Branded Stores, and Other), and Geography (North America and Other). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led revenue with a 31.05% household refrigerators and freezers market share in 2025, sustained by near-saturated ownership, brisk replacement cycles, and demand for smart features. Samsung and LG both prioritized the U.S.-built-in segment, leveraging Dacor and Signature Kitchen Suite, respectively, to secure builder partnerships and achieve double-digit premium growth. GE Appliances committed USD 3 billion through 2029 to expand fridge output across 11 domestic plants, underlining continued reshoring momentum. Although the region's 3.74% CAGR trails global averages, steady price-mix gains keep it the largest profit pool in the household refrigerators and freezers market. APAC delivers the fastest 6.32% CAGR, propelled by urbanization, first-time purchasing, and local manufacturing investments. China shipped 4.48 billion home appliances in 2024, up 20.8% year-on-year, reflecting export diversification and domestic subsidy schemes. India's appliances segment, still at low per-capita penetration, benefits from an expanding middle class even as component shortages nudge prices higher. Regional regulations favor natural refrigerants; India's Kigali-based HFC phase-down fosters uptake of R290 in mid-capacity models, reinforcing climate alignment.

Europe faces moderate growth at a 2.84% CAGR amid challenging economic conditions and regulatory transitions that increase compliance costs while driving innovation. The EU F-gas Regulation's January 2026 prohibition on fluorinated greenhouse gases in domestic refrigerators creates immediate transition pressure, though manufacturers like BSH have invested heavily in compliance, including a new refrigeration factory in Mexico and enhanced R&D spending approaching €850 million (USD 918 million). European industry associations emphasize competitiveness challenges from fragmented regulations, high electricity costs 2-3x US levels, and supply chain concentration for critical materials. The Middle East & Africa region exhibits the fastest forecast growth at 6.87% CAGR, supported by strategic investments like Sharp's USD 30 million joint venture in Egypt and Haier's 26.8% revenue growth in the region, driven by localized production and products adapted to unreliable power infrastructure.

- Whirlpool Corp.

- Haier Smart Home Co.

- LG Electronics Inc.

- Samsung Electronics Co.

- Electrolux AB

- Panasonic Corp.

- Bosch-Siemens Hausgerate GmbH

- Midea Group

- Hisense Co.

- Hitachi Global Life Solutions

- GE Appliances (Haier)

- Liebherr-Hausgerate

- Sub-Zero Group

- Arcelik A.S. (Beko, Grundig)

- Godrej Appliances

- Sharp Corp.

- TCL Technology

- P.C. Richard & Son (private label)

- Glen Dimplex (Home Appliances)

- SMEs & Local Players (collective)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream Energy-efficiency Regulations

- 4.2.2 Rising Disposable Income in Emerging Asia

- 4.2.3 Urban Housing Growth & Kitchen Renovations

- 4.2.4 Omnichannel Retail Expansion

- 4.2.5 Under-the-Radar Carbon-Neutral Refrigerant Adoption

- 4.2.6 AI-Enabled Predictive Maintenance for Compressors

- 4.3 Market Restraints

- 4.3.1 Supply-Chain Volatility for Semiconductors

- 4.3.2 High Electricity Tariffs in Developing Nations

- 4.3.3 Rare-Earth Magnet Price Shocks

- 4.3.4 Growing Second-Hand Appliance Market Online

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Top-freezer Refrigerators

- 5.1.2 Bottom-freezer Refrigerators

- 5.1.3 Side-by-Side Refrigerators

- 5.1.4 French Door Refrigerators

- 5.2 By Capacity

- 5.2.1 Less than 300 Litres

- 5.2.2 300 - 500 Liters

- 5.2.3 Greater than 500 Liters

- 5.3 By Distribution Channel

- 5.3.1 Multi-branded Stores

- 5.3.2 Specialty Stores

- 5.3.3 Online

- 5.3.4 Other Distribution Channels

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.4.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.4.3.8 Rest of Europe

- 5.4.4 APAC

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East & Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East & Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Whirlpool Corp.

- 6.4.2 Haier Smart Home Co.

- 6.4.3 LG Electronics Inc.

- 6.4.4 Samsung Electronics Co.

- 6.4.5 Electrolux AB

- 6.4.6 Panasonic Corp.

- 6.4.7 Bosch-Siemens Hausgerate GmbH

- 6.4.8 Midea Group

- 6.4.9 Hisense Co.

- 6.4.10 Hitachi Global Life Solutions

- 6.4.11 GE Appliances (Haier)

- 6.4.12 Liebherr-Hausgerate

- 6.4.13 Sub-Zero Group

- 6.4.14 Arcelik A.S. (Beko, Grundig)

- 6.4.15 Godrej Appliances

- 6.4.16 Sharp Corp.

- 6.4.17 TCL Technology

- 6.4.18 P.C. Richard & Son (private label)

- 6.4.19 Glen Dimplex (Home Appliances)

- 6.4.20 SMEs & Local Players (collective)

7 Market Opportunities & Future Outlook

- 7.1 Connected-Home Interoperability Platforms

- 7.2 Circular-Economy Certified Refurbishment Programs

家用冷藏库和冷冻库市场:依压缩机类型、技术、容量、销售管道和产品类型划分-2026-2032年全球市场预测

家用冷藏库和冷冻库市场:依压缩机类型、技术、容量、销售管道和产品类型划分-2026-2032年全球市场预测 家用冷藏库和冷冻库市场分析及预测(至2035年):按类型、产品类型、技术、应用、材质、最终用户、功能、安装类型和设备划分

家用冷藏库和冷冻库市场分析及预测(至2035年):按类型、产品类型、技术、应用、材质、最终用户、功能、安装类型和设备划分 家用冷藏库和冷冻库市场规模、份额和成长分析(按类型、技术、最终用户、分销管道和地区划分)—2026-2033年产业预测

家用冷藏库和冷冻库市场规模、份额和成长分析(按类型、技术、最终用户、分销管道和地区划分)—2026-2033年产业预测 家用冰箱及冰柜市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

家用冰箱及冰柜市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 家用冰箱和冷冻库市场按类型、容量、分销管道和地区划分

家用冰箱和冷冻库市场按类型、容量、分销管道和地区划分 北美家用冰箱和冷冻库市场规模、份额和趋势分析报告:2025-2030 年按设备、结构、容量、价格分布范围、地区和细分市场进行的预测

北美家用冰箱和冷冻库市场规模、份额和趋势分析报告:2025-2030 年按设备、结构、容量、价格分布范围、地区和细分市场进行的预测 2024-2028年全球家用冰箱冷冻库市场

2024-2028年全球家用冰箱冷冻库市场