|

市场调查报告书

商品编码

1910588

计划物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Project Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

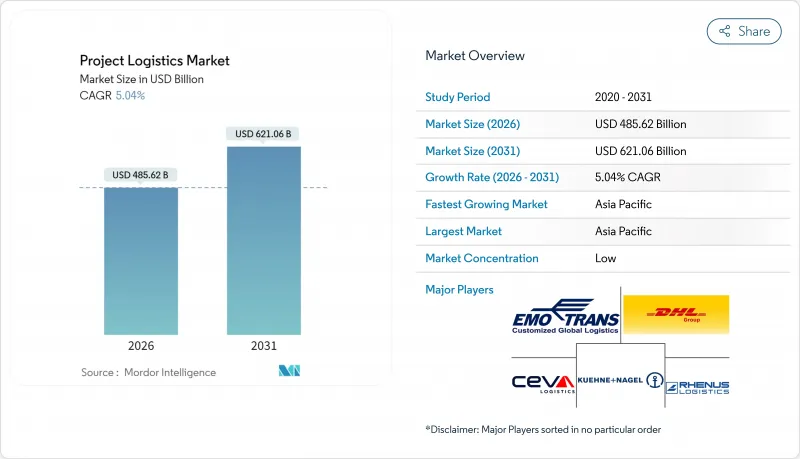

预计到 2026 年,计划物流市场规模将达到 4,856.2 亿美元,高于 2025 年的 4,623 亿美元。

预计到 2031 年将达到 6,210.6 亿美元,2026 年至 2031 年的复合年增长率为 5.04%。

可再生能源产能扩张、新兴经济体基础设施投资同步成长以及跨欧亚铁路走廊的成熟,正在扩大服务范围并提升单次运输价值。中型液化LNG接收站、氢气管道改造和模组化建设计划正在增加平均零件尺寸,从而推动对专用船舶、自航式模组化运输车和温控仓储设施的需求。同时,人工智慧驱动的路线优化平台正在将端到端成本降低10-15%,并缩短交付时间,使营运商能够更快地重新部署有限的资产。来自区域性专业营运商和技术主导新参与企业的竞争加剧,正在加速中型业者的整合,但市场集中度仍然较低,没有一家业者的市占率超过8%。持续存在的不利因素,包括运费波动、认证重型货物装卸人员短缺以及港口长期拥堵,正促使承运商投资于数位化视觉化工具、多模态枢纽和类比培训计画。

全球计划物流市场趋势与洞察

大型可再生能源计划推动了对专业物流的需求。

离岸风力发电和绿氢能走廊正在重塑航运格局。如今,涡轮机叶片长度超过100米,需要专为15-20兆瓦涡轮机设计的自升式运输船。 Venture Worldwide公司投资180亿美元的普拉克明液化天然气第三期扩建计划标誌着零件尺寸的升级,而德国将一条400公里长的天然气管道改造为氢气运输管道,则预示着一种新型低温货物的出现,这种货物必须保持在-253°C以下的温度。这些变化迫使营运商重新思考航线规划、船舶选择和库存分配。

新兴经济体的基础建设超级週期支撑长期成长

中国的「一带一路」倡议促成了东非一个价值100亿美元的港口项目和一个铁路网络的建设,该铁路网络将把运输时间缩短多达50%。同时,跨里海国际航线预计到2024年将运输27,000个标准箱,年增25倍。计划物流市场受益于此可预测的、持续数十年的资本投入,为船队扩张和区域仓库扩建提供了充分的理由。

前期投资巨大会阻碍市场进入。

一台1000吨级的履带起重机造价可能在5000万美元到1亿美元之间,而一艘风电场安装船的造价可能超过2亿美元。这些巨额投资阻碍了新进业者,迫使当地专业公司以高成本租赁设备,即使计划规模不断增长,利润率也受到限制。

细分市场分析

到2025年,运输业将占计划物流市场的60.45%,这反映了路线规划、重型装运船隻和超大货物护航船的关键作用。仓储、配送和库存管理虽然规模较小,但却是成长最快的细分市场,年复合成长率达5.18%。这一增长反映了模组化建筑的兴起,模组化建筑需要温控储存和同步装卸。随着一体化供应商将仓储与最后一公里组装相结合,仓储服务的计划物流市场规模预计将会扩大。实施自动化库存管理系统的营运商可以更清楚地了解组件的停留时间,从而减少閒置资金和逾期罚款。

随着服务种类日益丰富,对现场物流协调、报关和风险咨询的需求也随之成长。 Highland-Fairview 的物流超级中心正是这种一站式模式的典范,其 4000 万平方英尺的设施可满足复杂的货物流转需求。随着资产所有者将製造和安装等环节的责任外包,计划物流行业正从以运输为中心的合约模式转向以结果为导向的伙伴关係关係,从而提高客户留存率和费用收入潜力。

计划物流市场报告按服务(运输、仓储、配送及库存管理、其他服务)、货物类型(超大货物、重型货物、散装货物、其他)、最终用户(石油天然气、发电及输电、建筑及基础设施、其他)和地区(北美、南美、亚太、欧洲、中东和非洲)进行细分。市场预测以美元以金额为准。

区域分析

亚太地区占全球收入的38.60%,这主要得益于中国「一带一路」沿线港口的蓬勃发展、印度高速公路网的建设以及澳洲可再生矿产资源。预计到2024年,跨里海航线的货运量将增加25倍,达到27,000标准箱,凸显了开发替代通道、减少对苏伊士运河依赖的重要性。区域各国政府正在资助内陆堆场和数位化海关窗口的建设,使承运商能够加快货物週转速度并降低滞期费。

北美位居第二,这主要得益于一系列走廊开发项目,例如墨西哥湾沿岸液化天然气产能的扩张、一条40吉瓦的可再生能源管道以及耗资64亿美元的戈迪·豪国际大桥(计划于2025年底通车)。加拿大北极贸易走廊的Hudson湾铁路维修将缩短运输时间,从而促进关键矿产出口。审批程序的改革提高了运输时间表的确定性,鼓励物流公司签订长期包车协议。

欧洲、中东和非洲构成了一幅成熟和新兴运输路线交织的图景。德国400公里长的氢气管道改造计画正在开闢新的货物运输类别,而埃及的港口扩建和沙乌地阿拉伯的陆桥计画则刺激了对重型沿海起重机的需求。中国支持的东非港口,包括坦尚尼亚的巴加莫约港,正在重塑贸易路线,并吸引区域专家建立支线服务。南美洲的矿业走廊和可再生能源计画正在开闢前沿机会,为规避风险的营运商带来丰厚回报。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 大型可再生能源计划(离岸风电、绿氢能走廊)

- 新兴经济体的基础建设超级週期

- 模组化建造和预製工厂规模化

- 中型液化天然气出口终端数量迅速增加(美国墨西哥湾沿岸、西非)

- 透过「一带一路」倡议推动跨欧亚铁路走廊走向成熟

- 人工智慧驱动的路线和风险优化平台

- 市场限制

- 重型运输资产需要高额的初始资本投入。

- 货运和燃油成本波动对利润率造成压力。

- 重型起重作业人员严重短缺

- 港口许可证和壅塞延误

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 新冠疫情与地缘政治事件的影响

第五章 市场规模与成长预测

- 透过服务

- 运输

- 路

- 铁路

- 航空

- 海

- 仓储管理、物流和库存管理

- 附加价值服务及更多

- 运输

- 按货物类型

- 超大货物(非标准货物)

- 重型货物

- 散货

- 其他的

- 按最终用户行业划分

- 石油天然气、采矿和采石

- 能源生产和输送

- 建筑和基础设施

- 製造和工业工厂

- 航太/国防

- 其他(海事/造船、通讯等)

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 秘鲁

- 智利

- 阿根廷

- 南美洲其他地区

- 亚太地区

- 印度

- 中国

- 日本

- 澳洲

- 韩国

- 东南亚(新加坡、马来西亚、泰国、印尼、越南、菲律宾)

- 亚太其他地区

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 比荷卢经济联盟(比利时、荷兰、卢森堡)

- 北欧国家(丹麦、芬兰、冰岛、挪威、瑞典)

- 其他欧洲

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Deutsche Post DHL

- Rhenus Logistics

- CEVA Logistics

- Kuehne+Nagel

- EMO Trans

- Hellmann Worldwide Logistics

- CH Robinson

- NMT Global Project Logistics

- Rohlig Logistics

- Expeditors International

- Kerry Logistics

- DSV A/S

- Fagioli group

- FLS Transportation

- Megalift

- Express Global Logistics(EXG)

- Yusen Logistics

- Geodis

- Crane Worldwide Logistics

- Transworld

第七章 市场机会与未来展望

Project logistics market size in 2026 is estimated at USD 485.62 billion, growing from 2025 value of USD 462.30 billion with 2031 projections showing USD 621.06 billion, growing at 5.04% CAGR over 2026-2031.

Capacity additions in renewable energy, synchronized infrastructure super-cycles in emerging economies, and the maturation of trans-Eurasian rail corridors are broadening service scope while lifting value per shipment. Mid-scale LNG terminals, hydrogen pipeline conversions, and modular construction projects are enlarging average component dimensions, boosting demand for specialized vessels, self-propelled modular transporters, and climate-controlled storage. In parallel, AI-enabled route-optimization platforms are trimming end-to-end costs by 10-15% and shortening delivery windows, allowing operators to redeploy scarce assets faster. Heightened competition, driven by regional specialists and technology-first entrants, is accelerating consolidation among mid-tier firms, yet market concentration remains low because no single provider exceeds 8% share. Persistent headwinds volatile freight rates, certified heavy-lift labor shortages, and chronic port congestion are pushing carriers to invest in digital visibility tools, multi-modal hubs, and simulation-based training programs.

Global Project Logistics Market Trends and Insights

Renewable-Energy Mega-Projects Drive Specialized Logistics Demand

Offshore wind farms and green-hydrogen corridors are rewriting transport blueprints. Turbine blades now surpass 100 meters, necessitating jack-up vessels designed for 15-20 MW turbines. Venture Global's USD 18 billion phase-three expansion at Plaquemines LNG embodies the boom in component scale, while Germany's conversion of 400 kilometers of natural-gas pipeline to hydrogen service signals a new class of cryogenic cargo that must be kept below -253 °C. These shifts require operators to recalibrate route planning, vessel selection, and inventory staging.

Infrastructure Super-Cycles in Emerging Economies Sustain Long-Term Growth

China's Belt and Road Initiative has spawned a USD 10 billion East-African port program and rail links that cut transit times by up to 50%. Simultaneously, the Trans-Caspian International Transport Route moved 27,000 TEU in 2024, a 25-fold jump over the prior year. The project logistics market benefits from this predictable, multi-decade capital pipeline that justifies fleet expansion and regional depot build-outs.

High Upfront Capital Requirements Constrain Market Entry

A 1,000-tonne crawler crane can cost USD 50-100 million, and wind-installation vessels exceed USD 200 million. These sums deter new entrants and force regional specialists to lease gear at premiums, curbing margin upside even as project volumes rise.

Other drivers and restraints analyzed in the detailed report include:

- Modular Construction Transforms Project Delivery Models

- Mid-Scale LNG Export Terminals Create Regional Hubs

- Volatile Freight and Fuel Costs Pressure Operating Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation captured 60.45% of the project logistics market in 2025, reflecting the indispensable role of route engineering, heavy-lift vessels, and escorts for oversized cargo. Warehousing, distribution, and inventory management, though smaller, is the fastest-expanding slice at a 5.18% CAGR. The uptick mirrors modular builds that need climate-controlled laydown yards and synchronized staging. The project logistics market size for warehousing services is set to climb as integrated providers bundle storage with last-mile assembly. Operators deploying automated inventory systems gain visibility over component dwell times, curbing idle capital and penalties.

A wider service mix also elevates demand for on-site logistics coordination, customs brokerage, and risk advisory. Highland Fairview's logistics megacenter embodies this one-stop model, offering 40 million square feet tailored for complex cargo streams. As asset owners outsource cradle-to-installation responsibility, the project logistics industry pivots from move-centric contracts to outcome-driven partnerships, raising stickiness and fee potential.

The Project Logistics Market Report is Segmented by Service (Transportation, Warehousing, Distribution & Inventory Management, Other Services), Cargo Type (Oversized, Heavy-Lift, Breakbulk, Others), End-User (Oil & Gas, Energy Generation/Transmission, Construction and Infrastructure, and More), and Geography (North America, South America, Asia-Pacific, Europe, Middle East and Africa). Market Forecasts are Provided in Value (USD).

Geography Analysis

Asia-Pacific contributes 38.60% of global revenue, supported by China's Belt and Road ports, India's highways, and Australia's renewable-minerals surge. The Trans-Caspian route's 25-fold volume jump to 27 000 TEU in 2024 underscores alternate corridors that reduce reliance on Suez passages. Regional governments fund inland depots and digital customs windows, enabling carriers to rotate assets faster and clip demurrage fees.

North America ranks second, driven by LNG build-outs along the Gulf, 40-GW renewable-energy pipelines, and corridor upgrades such as the USD 6.4 billion Gordie Howe International Bridge that will open in late 2025. Canada's Arctic Trade Corridor advances through Hudson Bay Railway refurbishments that shave transit times and unlock critical-mineral exports. Favorable permitting reforms bolster schedule certainty, encouraging logistics firms to lock in long-term charter commitments.

Europe, the Middle East, and Africa compose a mosaic of mature and emerging lanes. Germany's 400-kilometer hydrogen-pipeline conversion pioneers a new cargo category, while Egypt's port expansions and Saudi Arabia's Landbridge escalate demand for coastal heavy-lift cranes. China-backed East-African ports, including Bagamoyo in Tanzania, redirect trade loops and invite regional specialists to establish feeder services. South America's mining corridor and renewable plans open frontier opportunities that reward risk-ready operators.

- Deutsche Post DHL

- Rhenus Logistics

- CEVA Logistics

- Kuehne + Nagel

- EMO Trans

- Hellmann Worldwide Logistics

- C.H. Robinson

- NMT Global Project Logistics

- Rohlig Logistics

- Expeditors International

- Kerry Logistics

- DSV A/S

- Fagioli group

- FLS Transportation

- Megalift

- Express Global Logistics (EXG)

- Yusen Logistics

- Geodis

- Crane Worldwide Logistics

- Transworld

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Renewable-energy mega-projects (offshore wind, green-hydrogen corridors)

- 4.2.2 Infrastructure super-cycles in emerging economies

- 4.2.3 Up-scaling of modular construction and prefabricated plants

- 4.2.4 Surge in mid-scale LNG export terminals (U.S. Gulf, West Africa)

- 4.2.5 Belt-and-Road trans-Eurasian rail corridors maturing

- 4.2.6 AI-enabled route and risk optimization platforms

- 4.3 Market Restraints

- 4.3.1 High upfront capex for heavy-lift assets

- 4.3.2 Volatile freight and fuel costs eroding margins

- 4.3.3 Acute shortage of certified heavy-lift operators

- 4.3.4 Port-side permit and congestion delays

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of COVID-19 and Geo-Political Events

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Service

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Air

- 5.1.1.4 Sea

- 5.1.2 Warehousing, Distribution and Inventory Management

- 5.1.3 Value-added Services and Others

- 5.1.1 Transportation

- 5.2 By Cargo Type

- 5.2.1 Oversized (Out-of-Gauge) Cargo

- 5.2.2 Heavy-Lift Cargo

- 5.2.3 Breakbulk Cargo

- 5.2.4 Others

- 5.3 By End-User Industry

- 5.3.1 Oil and Gas, Mining and Quarrying

- 5.3.2 Energy Generation and Transmission (Includes Renewable Energy)

- 5.3.3 Construction and Infrastructure

- 5.3.4 Manufacturing and Industrial Plants

- 5.3.5 Aerospace and Defense

- 5.3.6 Others (Maritime and Shipbuilding, Telecommunications, etc.)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 Europe

- 5.4.4.1 United Kingdom

- 5.4.4.2 Germany

- 5.4.4.3 France

- 5.4.4.4 Spain

- 5.4.4.5 Italy

- 5.4.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.4.8 Rest of Europe

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab of Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East And Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Deutsche Post DHL

- 6.4.2 Rhenus Logistics

- 6.4.3 CEVA Logistics

- 6.4.4 Kuehne + Nagel

- 6.4.5 EMO Trans

- 6.4.6 Hellmann Worldwide Logistics

- 6.4.7 C.H. Robinson

- 6.4.8 NMT Global Project Logistics

- 6.4.9 Rohlig Logistics

- 6.4.10 Expeditors International

- 6.4.11 Kerry Logistics

- 6.4.12 DSV A/S

- 6.4.13 Fagioli group

- 6.4.14 FLS Transportation

- 6.4.15 Megalift

- 6.4.16 Express Global Logistics (EXG)

- 6.4.17 Yusen Logistics

- 6.4.18 Geodis

- 6.4.19 Crane Worldwide Logistics

- 6.4.20 Transworld

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

计划物流市场:依服务类型、运输方式、服务模式、货物类型及最终用户产业划分-2026-2032年全球预测按服务类型、运输方式、供应商类型和最终用户产业分類的端到端物流服务市场-2026-2032年全球预测

计划物流市场:依服务类型、运输方式、服务模式、货物类型及最终用户产业划分-2026-2032年全球预测按服务类型、运输方式、供应商类型和最终用户产业分類的端到端物流服务市场-2026-2032年全球预测 全球计划物流市场规模、份额、产业分析报告:2025 年至 2032 年按模式、服务、最终用途产业和地区分類的展望与预测

全球计划物流市场规模、份额、产业分析报告:2025 年至 2032 年按模式、服务、最终用途产业和地区分類的展望与预测 计划物流市场规模、份额和趋势分析报告:按服务、运输方式、最终用途产业、地区和细分市场预测,2025-2033 年

计划物流市场规模、份额和趋势分析报告:按服务、运输方式、最终用途产业、地区和细分市场预测,2025-2033 年 计划物流,全球市场 2025-2029

计划物流,全球市场 2025-2029 中国计划物流:市场占有率分析、产业趋势与统计、成长预测(2025-2030)

中国计划物流:市场占有率分析、产业趋势与统计、成长预测(2025-2030) 专案物流市场、机会、成长动力、产业趋势分析与预测,2024-2032

专案物流市场、机会、成长动力、产业趋势分析与预测,2024-2032