|

市场调查报告书

商品编码

1910630

智慧马达:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Smart Motors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

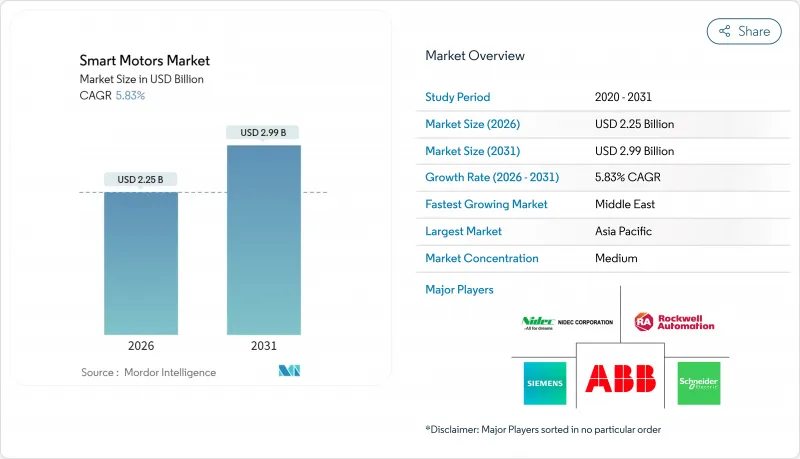

2025年智慧马达市值为21.3亿美元,预计到2031年将达到29.9亿美元,高于2026年的22.5亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 5.83%。

随着製造商、商业建筑业主和基础设施营运商寻求降低能源成本并提高运转率,边缘人工智慧、先进电力电子和工业自动化平台的日益整合正在加速其应用。此外,对马达效率的监管要求、对预测性维护日益增长的关注以及确保马达网路安全的需求也进一步推动了市场需求,而这些需求在企业资料技术领域占据着举足轻重的地位。儘管技术仍存在一定程度的分散性,但竞争格局已然清晰。能够将控制逻辑、边缘分析和安全连接整合到紧凑型机壳中的供应商正在迅速抢占市场份额。在资料中心冷却、离岸风电系统和自主移动机器人等领域,紧凑型高性能驱动器能够显着提高生产力,因此市场机会正在不断扩大。

全球智慧马达市场趋势与洞察

透过与边缘人工智慧集成,实现智慧马达控制的设备内优化

边缘人工智慧正在将马达智慧从集中式PLC转移到能够在本地执行推理的嵌入式微控制器。意法半导体(STMicroelectronics)的STM32系列整合了人工智慧加速器,可将响应延迟从毫秒级降低到微秒级。德克萨斯(TI)的C2000即时装置运行机器学习模型,可在故障发生前30天侦测到轴承和绕组故障,使维修人员能够在不中断生产的情况下安排维修。瑞萨电子在机器人组装单元的马达驱动器中实施了自适应扭矩演算法,并观察到效率提高了15-20%。这种效果在诸如取放机器人等应用中尤其重要,因为瞬时运动曲线决定了吞吐量。边缘处理透过将运行资料保留在本地,也满足了资料主权法规的要求。

欧洲和中国的强制性工业能效标准

欧盟法规 2019/1781 提高了大多数工业应用领域 IE3 电机的最低标准,并建议在高能耗环境下使用 IE4-IE5 电机,从而有效地推动了智慧驾驶融入合规战略。中国的「十四五」规划目标是到 2025 年将工业能源强度降低 13.5%,并将智慧马达定位为核心推动因素。 IEC 60034-30-1 和 IEC 60034-2-1 提供了製造商必须满足的分类标准和调查方法。因此,在冶金、水泥和化学等行业(电机消耗的电力消耗的 70%),工业工厂正越来越多地将资本预算重新分配给高效能、配备丰富感测器的驱动系统。由于智慧马达可以即时记录和报告能源性能,从而便于合规检验,因此监管最低标准的实施正在加速智慧马达的普及应用。

网路化马达系统中的网路安全漏洞

将数千台驱动器连接到乙太网路会扩大攻击者可攻击的面。美国标准与技术研究院 (NIST) 警告称,电机网路分段不当可能导致攻击者从单一驱动器横向移动到工厂的整体控制层。 ICS-CERT 在 2024 年发布的警报中记录了恶意软体事件,其中受损的逆变器导致速度异常,损坏了泵浦和生产批次。即时性限制使修补程式的修復变得复杂,因为驱动器无法容忍标准IT安全工具相关的通讯延迟。因此,化学、水务和电力企业通常会推迟智慧马达的部署,直到供应商展示其驱动器专用的安全协定堆迭并通过 IEC 62443 认证。

细分市场分析

2025年,变频驱动器在智慧马达市场占据主导地位,市占率高达47.82%,长期以来一直是马达连接自动化网路的主要方式。然而,整合式马达驱动组件预计将以6.85%的复合年增长率成为成长最快的产品,因为买家看重的是能够安装整合了电力电子、控制设备和感测器的单一密封单元。这种方法减少了对外部机柜的需求,缩短了布线距离,从而缩小了工厂面积。这对于食品、饮料和製药加工企业来说极具吸引力,尤其是那些需要接受健康和安全审核、对裸露电缆配线架有较高要求的企业。此外,整合式驱动器还能轻鬆通过电磁相容性测试,节省数週的设计迭代时间。

碳化硅 (SiC) 和氮化镓 (GaN) 电晶体技术的进步,使得装置能够以更高的开关频率运作并降低损耗,从而实现了几年前还会导致过热的更高密度封装。 ABB 的整合解决方案每公升功率比分立式解决方案高出 30-40%,同时还整合了振动、温度和电流感测器,并将分析资料传输到边缘 PC。这些诊断功能使维修团队能够从每月巡检转变为基于状态的维护计划,从而降低人事费用并防止意外故障。虽然独立逆变器在维修专案中仍然很受欢迎,但由于其生命週期成本优势,整合解决方案在新计画中也越来越受欢迎。工厂自动化供应商越来越多地在集成电机中预装多重通讯协定韧体,使用户可以通过软体更新而非硬体更换来重新配置通信,从而进一步加速了集成解决方案的普及。

截至2025年,1-10kW功率范围的智慧马达占了智慧马达市场60.74%的份额。这主要归功于中型机械设备(例如输送机、搅拌机和压缩机)在离散製造和流程製造业的持续普及。此输出范围的马达由于在长运作週期内可累积节能,因此能够快速收回投资。然而,1kW以下功率范围的马达应用最为广泛,其销量以7.02%的复合年增长率成长。实验室自动化、医疗诊断和取放式送料器等应用需要超紧凑型驱动装置,这些驱动器需具备精细的速度控制、低杂讯和高定位精度。在这些应用中,小功率智慧电机取代了简单的阴极电机和步进电机,显着提高了出货量。

整合化趋势与高功率领域类似,但更重视功率密度。德克萨斯展示了一款参考设计,采用紧凑型 C2000 微控制器、闸极驱动器和磁场定向控制韧体,所有这些都可以在一个手掌大小的机壳内控制三相电流。低于 1kW 的驱动装置也为建筑自动化开闢了更广泛的应用场景,例如风机盘管、智慧百叶窗和暖通空调水循环系统中的微型水泵。分散式楼宇设备的数量可能高达数千台,因此即使是小型马达也能影响整个市场。同时,10kW 以上的系统仍然较保守。石油钻井平台和矿山优先考虑系统的稳健性和可靠的性能,而不是尖端的控制技术,这导致升级週期更长。

区域分析

到2025年,亚太地区将占全球收入的37.42%,这主要得益于中国降低工业能源强度的努力以及印度与生产连结奖励计画(PIs),该措施旨在为先进自动化提供补贴。日本机器人单元製造商需要抖动小于毫秒级的伺服,推动了对高性能智慧驱动器的需求。同时,韩国造船厂正在整合使用寿命长达25年或以上的耐盐马达。台湾和中国当地半导体代工厂的快速成长进一步推动了对低振动、高纯度无尘室马达的需求。在地采购缩短了供应链,使亚洲原始设备製造商(OEM)能够在不牺牲功能的前提下,以低于国际竞争对手的价格销售产品。

到2031年,中东地区将以6.35%的复合年增长率引领产业发展。沙乌地阿拉伯的「2030愿景」计划将向石化、采矿和绿色氢能计划注入数十亿美元,每个计画都指定采用具备先进诊断功能的马达系统,以最大限度地减少前往偏远沙漠地区的维护次数。阿联酋的高层建筑正在采用智慧空调驱动装置,以满足永续性评估标准。沿岸地区的近海海水淡化厂正在采用耐腐蚀智慧电机,透过在发生严重故障之前检测轴承磨损来保护水生产。

在北美,製造业回流趋势正推动新型自动化工厂投入运作,同时老旧设备也不断更新换代。美国联邦政府对高效电机的税收优惠政策与加州和纽约州的建筑规范相辅相成。这些规范强制要求在功率超过一定马力的暖通空调系统中使用变速驱动器。基于美国国家标准与技术研究院 (NIST) 框架的网路安全要求正在推动市场对符合 IEC 62443-4-2 认证标准的驱动器的需求。在欧洲,2019/1781 号法规已全面实施,该法规要求即使是小规模工坊也必须更换不符合 IE3 标准的马达。德国汽车集团率先采用支援 PROFINET 的智慧驱动器来控制和协调喷漆车间的输送机和焊接机器人。东欧凭藉着低廉的劳动成本,正崛起为契约製造中心,并成为智慧电机供应商极具潜力的投资目的地。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 透过与边缘人工智慧集成,实现智慧马达控制的设备内优化

- 欧洲和中国的强制性工业能效标准

- 商业建筑空调系统的快速电气化

- 自主移动机器人与AGV领域应用日益广泛

- 离岸风力发电机俯仰偏航系统的日益普及

- SiC/GaN功率元件降低整合式马达和驱动器封装的成本

- 市场限制

- 网路化马达系统中的网路安全漏洞

- 碎片化的通讯协定环境限制了互通性

- 电力电子元件供应链长期受阻

- 基于状态的维护分析中的技能差距

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 宏观经济因素的影响

第五章 市场规模与成长预测

- 按组件

- 变速驱动

- 引擎

- 整合马达驱动

- 按额定输出

- 小于1千瓦

- 1~10kW

- 10千瓦或以上

- 透过通讯协定

- Ethernet/IP

- PROFINET

- Modbus TCP

- 其他通讯协定

- 透过使用

- 产业

- 石油和天然气

- 金属和采矿

- 水和污水处理

- 食品/饮料

- 化学品

- 其他行业

- 商业的

- 暖通空调和建筑自动化

- 资料中心

- 其他商业领域

- 车

- 航太/国防

- 产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 其他欧洲

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 中东

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 北美洲

第六章 竞争情势

- 策略趋势

- 市占率分析

- 公司简介

- Siemens AG

- Schneider Electric SE

- ABB Ltd

- Rockwell Automation Inc.

- Nidec Corporation

- Safran Electrical and Power

- Nanotec Electronic GmbH and Co. KG

- Turntide Technologies Inc.

- Fuji Electric Co. Ltd

- Moog Inc.

- Dunkermotoren GmbH(Ametek Inc.)

- Shanghai Moons'Electric Co. Ltd

- WEG SA

- Yaskawa Electric Corporation

- Parker Hannifin Corporation

- SEW-Eurodrive GmbH and Co KG

- Brook Crompton Holdings Ltd

- Bonfiglioli Riduttori SpA

- Emerson Electric Co.

- Applied Motion Products Inc.

第七章 市场机会与未来展望

The smart motors market was valued at USD 2.13 billion in 2025 and estimated to grow from USD 2.25 billion in 2026 to reach USD 2.99 billion by 2031, at a CAGR of 5.83% during the forecast period (2026-2031).

The heightened convergence of edge artificial intelligence, advanced power electronics, and industrial automation platforms is accelerating adoption as manufacturers, commercial building owners, and infrastructure operators seek to reduce energy bills and enhance uptime. Demand is further driven by regulatory mandates on motor efficiency, growing interest in predictive maintenance, and the need to secure motor networks that now reside firmly within enterprise information-technology perimeters. While the technology remains moderately fragmented, the direction of competition is clear: vendors that can integrate control logic, edge analytics, and secure connectivity within compact housings are rapidly capturing market share. Opportunities are expanding in data center cooling, offshore wind systems, and autonomous mobile robotics, where compact, high-performance drives provide measurable productivity gains.

Global Smart Motors Market Trends and Insights

Convergence of Smart Motor Controls with Edge AI for On-Device Optimization

Edge AI is moving motor intelligence from centralized PLCs toward embedded microcontrollers that can execute inference locally. STMicroelectronics' STM32 family now integrates AI accelerators that cut response latency from milliseconds to microseconds. Texas Instruments' C2000 real-time devices run machine-learning models that flag bearing or winding failures up to 30 days before breakdown, allowing maintenance staff to schedule repairs without disrupting production. Renesas Electronics measured 15-20% efficiency improvements after loading adaptive torque algorithms onto motor drives serving robotic assembly cells. These gains are significant in applications such as pick-and-place robotics, where split-second motion profiles determine throughput. Edge processing also addresses data sovereignty rules by keeping operational data on-premises.

Mandates on Industrial Energy Efficiency Standards in Europe and China

The European Union's Regulation 2019/1781 raises the minimum standard for IE3 motors for most industrial applications and promotes IE4-IE5 in high-consumption settings, effectively drawing intelligent drives into compliance strategies. China's 14th Five-Year Plan targets a 13.5% cut in industrial energy intensity by 2025, naming smart motors as core enablers. IEC 60034-30-1 and IEC 60034-2-1 supply the classification and test methodology that manufacturers must satisfy. Industrial plants in metallurgy, cement, and chemicals-where motors absorb as much as 70% of electricity-are therefore reshuffling capital budgets toward high-efficiency, sensor-rich drives. Regulatory floors accelerate adoption because smart motors can log and report energy performance in real time, validating compliance audits.

Cybersecurity Vulnerabilities in Networked Motor Systems

Linking thousands of drives onto Ethernet networks expands the attack surface that adversaries can exploit. NIST warns that poorly segmented motor networks can allow lateral movement from a single drive to plant-wide control layers. ICS-CERT alerts from 2024 documented malware incidents in which compromised inverters caused speed excursions, damaging pumps and production batches. Real-time constraints complicate patching because drives cannot tolerate the communication latency associated with standard IT security tools. As a result, chemical, water, and power utilities often defer smart motor rollouts until vendors demonstrate drive-native security stacks certified under IEC 62443.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Electrification of HVAC Systems in Commercial Buildings

- Increasing Adoption in Autonomous Mobile Robots and AGVs

- Fragmented Communication Protocol Ecosystem Limiting Interoperability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Variable speed drives dominated the smart motors market with a 47.82% share in 2025, as they have long served as the principal link between motors and automation networks. Integrated motor-drive packages, however, are experiencing the fastest 6.85% CAGR because buyers value the ability to install a single, sealed unit that combines power electronics, controls, and sensors. The approach eliminates external cabinets and reduces wiring runs, resulting in a cleaner plant floor footprint that appeals to food, beverage, and pharmaceutical processors, particularly those subject to hygiene or safety audits that penalize exposed cable trays. Integrated drives also pass electromagnetic-compatibility tests more readily, saving weeks in design iterations.

Advances in silicon carbide and gallium nitride transistors, operating at higher switching frequencies and lower losses, now permit dense packaging that would have overheated just a few years ago. ABB's integrated solutions deliver 30-40% more power per liter than discrete counterparts while embedding vibration, temperature, and current sensors that stream analytics data to edge PCs. These diagnostics help maintenance teams transition from monthly route-based inspections to condition-based plans, trimming labor and preventing surprise failures. In retrofit environments, stand-alone inverters continue to sell steadily, while new greenfield projects increasingly default to integrated form factors because lifecycle economics favor them. As more factory automation vendors preload multi-protocol firmware onto integrated motors, users gain the flexibility to reconfigure communications through software updates rather than hardware swaps, further stimulating adoption.

The 1-10 kW tranche retained a 60.74% share of the smart motors market size in 2025, as mid-range machines-such as conveyors, mixers, and compressors-remain prevalent across both discrete and process industries. Motors in this band see rapid payback when energy savings compound across long duty cycles. Nonetheless, adoption momentum is strongest below 1 kW, where unit sales are expanding at a 7.02% CAGR. Laboratory automation, medical diagnostics, and pick-and-place feeders require ultra-compact drives that mix fine speed control with low acoustic noise and high positional accuracy. Here, fractional-horsepower smart motors replace simple shaded-pole or stepper designs, resulting in a dramatic increase in shipment volumes.

Integration trends mirror those in higher ratings but with heightened emphasis on power density. Texas Instruments demonstrates reference designs featuring a tiny C2000 microcontroller, gate drivers, and field-oriented control firmware, all housed within a palm-sized enclosure that can still manage three-phase currents. Below 1 kW drives also unlock broader building automation use cases, including fan-coil units, smart blinds, and micro-pumps in HVAC hydronic loops. Because distributed building devices number in the thousands, even small motors collectively move the market needle. Above-10 kW systems, in contrast, stay conservative; oil rigs and mines value ruggedness and proven performance over bleeding-edge controls, so upgrades follow longer refresh cycles.

The Smart Motors Market Report is Segmented by Component (Variable Speed Drive, Integrated Motor-Drive, and More), Power Rating (Below 1 KW, 1-10 KW, and More), Communication Protocol (Ethernet/IP, PROFINET, and More), Application (Industrial, Commercial, Automotive, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

The Asia Pacific region held 37.42% of global revenue in 2025, underscored by China's push to reduce industrial-energy intensity and India's Production Linked Incentive schemes, which channel subsidies toward advanced automation. Japanese robotic cell makers require servos with sub-millisecond jitter, fueling demand for high-performance smart drives, while South Korean shipyards integrate ruggedized motors to endure salt-laden atmospheres over 25-year lifecycles. Taiwan and mainland China, home to booming semiconductor foundries, add further pull for low-vibration, high-purity clean-room motors. Local supply chains shorten lead times, letting Asian OEMs undercut foreign rivals on pricing without sacrificing features.

The Middle East is the pacesetter with a 6.35% CAGR through 2031. Saudi Arabia's Vision 2030 plans channel billions into petrochemical, mining, and green-hydrogen projects, each specifying motor systems with advanced diagnostics to minimize maintenance trips to remote desert sites. United Arab Emirates mega-buildings adopt intelligent HVAC drives to comply with sustainability ratings. Offshore desalination plants along the Gulf rely on corrosion-resistant smart motors that flag bearing wear before catastrophic failures, protecting water output.

North America continues to upgrade legacy assets as reshoring trends bring new automated factories online. U.S. federal tax incentives for efficient motors complement California and New York building codes, which mandate the use of variable-speed drives in HVAC systems over certain horsepower thresholds. Cybersecurity stipulations under the NIST framework elevate demand for drives certified to IEC 62443-4-2. In Europe, Regulation 2019/1781 is in full effect, obliging even small workshops to swap out sub-IE3 motors. German automotive groups are early adopters of PROFINET-enabled smart drives to control and coordinate paint-shop conveyors and welding robots. Eastern Europe, with its lower labor costs, is emerging as a contract-manufacturing hub and a successive investment wave for smart motor suppliers.

- Siemens AG

- Schneider Electric SE

- ABB Ltd

- Rockwell Automation Inc.

- Nidec Corporation

- Safran Electrical and Power

- Nanotec Electronic GmbH and Co. KG

- Turntide Technologies Inc.

- Fuji Electric Co. Ltd

- Moog Inc.

- Dunkermotoren GmbH (Ametek Inc.)

- Shanghai Moons' Electric Co. Ltd

- WEG S.A.

- Yaskawa Electric Corporation

- Parker Hannifin Corporation

- SEW-Eurodrive GmbH and Co KG

- Brook Crompton Holdings Ltd

- Bonfiglioli Riduttori S.p.A.

- Emerson Electric Co.

- Applied Motion Products Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Convergence of Smart Motor Controls with Edge AI for On-Device Optimization

- 4.2.2 Mandates on Industrial Energy Efficiency Standards in Europe and China

- 4.2.3 Rapid Electrification of HVAC Systems in Commercial Buildings

- 4.2.4 Increasing Adoption in Autonomous Mobile Robots and AGVs

- 4.2.5 Rising Deployment in Offshore Wind Turbine Pitch and Yaw Systems

- 4.2.6 Declining Cost of Integrated Motor-Drive Packages Due to SiC/GaN Power Devices

- 4.3 Market Restraints

- 4.3.1 Cybersecurity Vulnerabilities in Networked Motor Systems

- 4.3.2 Fragmented Communication Protocol Ecosystem Limiting Interoperability

- 4.3.3 Prolonged Supply Chain Constraints for Power Electronics Components

- 4.3.4 Skills Gap in Condition-Based Maintenance Analytics

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

- 4.8 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Variable Speed Drive

- 5.1.2 Motor

- 5.1.3 Integrated Motor-Drive

- 5.2 By Power Rating

- 5.2.1 Below 1 kW

- 5.2.2 1-10 kW

- 5.2.3 Above 10 kW

- 5.3 By Communication Protocol

- 5.3.1 Ethernet/IP

- 5.3.2 PROFINET

- 5.3.3 Modbus TCP

- 5.3.4 Other Communication Protocol

- 5.4 By Application

- 5.4.1 Industrial

- 5.4.1.1 Oil and Gas

- 5.4.1.2 Metal and Mining

- 5.4.1.3 Water and Wastewater

- 5.4.1.4 Food and Beverage

- 5.4.1.5 Chemicals

- 5.4.1.6 Other Industrial

- 5.4.2 Commercial

- 5.4.2.1 HVAC and Building Automation

- 5.4.2.2 Data Centers

- 5.4.2.3 Other Commercial

- 5.4.3 Automotive

- 5.4.4 Aerospace and Defense

- 5.4.1 Industrial

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.3.1 Siemens AG

- 6.3.2 Schneider Electric SE

- 6.3.3 ABB Ltd

- 6.3.4 Rockwell Automation Inc.

- 6.3.5 Nidec Corporation

- 6.3.6 Safran Electrical and Power

- 6.3.7 Nanotec Electronic GmbH and Co. KG

- 6.3.8 Turntide Technologies Inc.

- 6.3.9 Fuji Electric Co. Ltd

- 6.3.10 Moog Inc.

- 6.3.11 Dunkermotoren GmbH (Ametek Inc.)

- 6.3.12 Shanghai Moons' Electric Co. Ltd

- 6.3.13 WEG S.A.

- 6.3.14 Yaskawa Electric Corporation

- 6.3.15 Parker Hannifin Corporation

- 6.3.16 SEW-Eurodrive GmbH and Co KG

- 6.3.17 Brook Crompton Holdings Ltd

- 6.3.18 Bonfiglioli Riduttori S.p.A.

- 6.3.19 Emerson Electric Co.

- 6.3.20 Applied Motion Products Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球机器人智慧马达市场报告

2026年全球机器人智慧马达市场报告 工业智慧马达市场:2026-2032年全球市场预测(依产品类型、额定功率、技术、通讯协定、应用、销售管道和最终用户产业划分)智慧马达市场:按马达类型、电压、功率等级、连接方式、最终用途和分销管道划分-2026-2032年全球预测智慧整合马达市场:依马达类型、额定功率、终端用户产业、控制技术和整合度划分,全球预测,2026-2032年

工业智慧马达市场:2026-2032年全球市场预测(依产品类型、额定功率、技术、通讯协定、应用、销售管道和最终用户产业划分)智慧马达市场:按马达类型、电压、功率等级、连接方式、最终用途和分销管道划分-2026-2032年全球预测智慧整合马达市场:依马达类型、额定功率、终端用户产业、控制技术和整合度划分,全球预测,2026-2032年 日本智慧工业马达市场规模、份额、趋势及预测(按马达类型、连接性和智慧化程度、额定功率、终端用户产业和地区划分),2026-2034年

日本智慧工业马达市场规模、份额、趋势及预测(按马达类型、连接性和智慧化程度、额定功率、终端用户产业和地区划分),2026-2034年 智慧马达:全球市场份额和排名、总收入和需求预测(2025-2031年)2025 年至 2033 年智慧型马达市场规模、份额、趋势及预测(按组件、产品、应用和地区)

智慧马达:全球市场份额和排名、总收入和需求预测(2025-2031年)2025 年至 2033 年智慧型马达市场规模、份额、趋势及预测(按组件、产品、应用和地区) 智慧汽车市场:2025-2030 年预测

智慧汽车市场:2025-2030 年预测 全球智慧马达市场:2024年

全球智慧马达市场:2024年 智慧型马达市场,按组件类型、应用、电压类型、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

智慧型马达市场,按组件类型、应用、电压类型、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测