|

市场调查报告书

商品编码

1910667

包装印刷:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Packaging Printing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

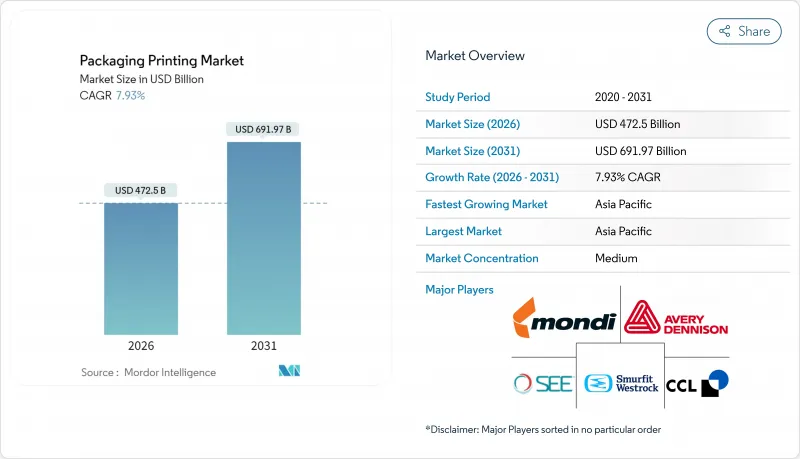

预计到 2026 年,包装印刷市场规模将达到 4,725 亿美元,高于 2025 年的 4,377.8 亿美元,预计到 2031 年将达到 6919.7 亿美元,2026 年至 2031 年的复合年增长率为 7.93%。

快速的数位转型、蓬勃发展的电子商务以及严格的永续性政策正在重塑技术选择、基材选择和区域投资重点。儘管柔版印刷凭藉其长版印刷的高生产率在大批量生产中仍保持优势,但品牌所有者现在更倾向于采用数位平台进行小批量生产,以支援SKU多样化、可变数据和智慧包装功能。随着加工商寻求低能耗和高速加工,UV固化油墨技术正日益普及,而RFID包装则提高了供应链的可视性。在策略层面,加工商正在将混合印刷生产线、本地化微型工厂和闭合迴路材料方案相结合,以在印刷品质、速度和环境影响决定品牌忠诚度的市场中保护利润。

全球包装印刷市场趋势与洞察

具备RFID功能和数位印刷的需求

物联网连接的蓬勃发展正将每个包装转变为一个资料节点。高价值药品正逐渐成为标配,并配备嵌入式RFID的感压标籤。数位印刷机无需更换印版即可整合序号,从而降低单位成本并实现即时认证。消费者应用程式读取这些标识符,以显示产品来源资讯和会员优惠,加深用户互动并协助产品召回管理。将柔版印刷的高效性与在线连续喷墨模组相结合的加工商,正满足可追溯性要求,并凭藉快速响应赢得合约。

不断扩大的电子商务包装量

直接面向消费者的物流优先考虑轻便的包装形式,以保护产品、突出图案并快速送达。像Gelato这样的客製印刷网路将配送距离缩短了90%,证明了透过从类比设备过渡到数位工作流程来扩大本地生产的可行性。小批量生产(通常少于1万件)降低了传统胶印的竞争力,促使企业投资高速喷墨印刷机和碳粉印刷机,以实现隔天交货的商店市级印刷品质。包装印刷市场受益于开箱影片提供的免费广告,这鼓励品牌更频繁地更新其设计。

高资本投资需求

一条高速八色柔版印刷生产线造价高达294万美元,需要辅助切断机、装版机和溶剂回收设备。东南亚的小型加工商正在推迟升级,眼看品牌所有者对公差要求越来越高,他们的设备将面临淘汰的风险。虽然有租赁方案,但高利率推高了总拥有成本。这促使财力雄厚的集团收购家族式工厂,得以扩张并协商更有利的基材合约。

细分市场分析

到2025年,柔版印刷将占据包装印刷市场34.78%的份额,这主要得益于其在胶片和纸张捲筒纸上无与伦比的印刷速度。混合印刷平台如今将喷墨单元堆迭在柔版印刷单元上,从而实现连续码和区域图形的印刷,而不会降低印刷速度。随着加工商追求更短的交货时间和更丰富的产品种类,数位印刷设备到2031年将以10.15%的复合年增长率成长。凹版印刷在高端烟草和化妆品领域仍占据着一席之地,因为在这些领域,图像的保真度足以弥补滚筒雕刻的成本。胶印主要应用于折迭纸盒,而网版印刷和其他一些小众印刷方式则专注于触感光油和金属效果。

投资数据也印证了这一趋势:2025年安装的包装生产线将配备预测性维护感测器,从而减少18%的计划外停机时间;基于云端的色彩伺服器将实现工厂间实时协调图稿;采用混合模式的加工商报告称,准备工作废弃物减少了28%,促销包装的上市时间缩短了一半。为此,设备供应商正将印刷机与工作流程软体捆绑销售,以获取业务收益并提高包装印刷市场的售后利润率。

截至2025年,溶剂型系统在包装印刷市场仍占39.62%的份额。然而,随着LED灯将电力消耗降低至每平方公尺0.3-0.5千瓦时(相较之下,热风干燥机的能耗为每平方公尺1.2-1.8千瓦时),UV固化油墨的出货量正以9.52%的复合年增长率成长。水性油墨在纸基应用领域成长最快,因为食品接触法规对挥发性有机化合物(VOC)的含量有限制。乳胶和LED-UV技术使得一些以前无法用汞灯固化的应用成为可能,例如收缩标籤和热敏薄膜。

在混合生产环境中,总成本模型更有利于UV固化。 UV固化可以省去洗版站,减少溶剂库存,并可按需固化,进而减少在製品。树脂挥发性仍然是一个风险,但多供应商合作和内部配方可以部分抵消价格波动。油墨供应商正在投资研发通过可堆肥性测试的生物基单体和光引发剂,使化学技术的进步与包装印刷市场面临的永续性挑战相契合。

区域分析

亚太地区将引领全球生产,预计到2024年,该地区新增印刷机装置量将占全球一半以上。中国加工企业正在增设多层包装袋生产线,以满足国内零食需求。印度在生产连结奖励计画计划下提供资本投资激励。越南和泰国的软包装生产商受益于近岸外包,为服装出口商提供快速吊牌和塑胶袋。跨境投资正在提升区域技术水平,与日本油墨生产商的合资企业则有助于提高产品品质的稳定性。

北美企业正积极拥抱科技与合规。对数位瓦楞纸印刷机的投资使当日达电商包装盒的产能提升了两倍。各州立法机构引入生产者延伸责任制(EPR)收费机制,以表彰可回收的印刷材料。美国印刷加工商在UV-LED改造方面处于领先地位,据称可节能25%。加拿大与美国食品药物管理局(FDA)协调食品接触限制,促进跨境采购。同时,墨西哥正吸引着寻求在美墨加协定(USMCA)下享受免税准入的顶级品牌。

欧洲在监管方面引领潮流。该地区设定的88%包装可回收率目标正推动品牌指南转向单一材料复合材料,而这需要使用特殊油墨。德国机械出口产品正利用工业4.0的即时黏度控制等功能,而义大利印刷机製造商则正在将在线连续冷烫印技术标准化,以吸引高端品牌。东欧,尤其是波兰,以低于西方国家的人事费用消化过剩产能,同时维持高技能水准。荷兰的创新津贴正在资助纸质阻隔包装的试点生产线,从而维持包装印刷市场的良好发展势头。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 具备RFID功能和数位印刷的需求

- 不断扩大的电子商务包装量

- 永续性:推广环保油墨和基材

- 新兴市场的消费繁荣

- 品牌拥有者采用智慧包装序列化

- 在地化、客製印刷微型工厂的兴起

- 市场限制

- 需要大量资金投入

- 复杂多元的全球印刷法规

- 光引发剂和树脂价格波动

- 熟练柔版印刷操作人员短缺

- 产业价值链分析

- 监管环境

- 技术展望

- 影响市场的宏观经济因素

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 产业生态系分析

第五章 市场规模与成长预测

- 透过印刷技术

- 胶印

- 凹版印刷

- 柔版印刷

- 数位印刷

- 其他印刷技术

- 按墨水类型

- 溶剂型油墨

- UV固化油墨

- 水性油墨

- 乳胶墨水

- LED-UV油墨

- 透过包装材料

- 标籤

- 塑胶容器和薄膜

- 玻璃容器

- 金属罐和铝箔

- 纸和纸板箱

- 软包装袋

- 瓦楞纸箱和托盘

- 按最终用途行业划分

- 食品/饮料

- 製药和医疗保健

- 化妆品和个人护理

- 家用和工业用途

- 电子电器设备

- 其他终端用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 南美洲其他地区

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 越南

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Amcor plc

- Smurtfit WestRock

- Tetra Pak Group

- Mondi plc

- Huhtamaki Oyj

- CCL Industries Inc.

- Avery Dennison Corporation

- Sealed Air Corporation

- International Paper Company

- Stora Enso Oyj

- Sonoco Products Company

- Georgia-Pacific LLC

- Constantia Flexibles GmbH

- Mayr-Melnhof Karton AG

- Ahlstrom-Munksj Oyj

- Clondalkin Group Holdings BV

- Autajon Group SA

- SATO Holdings Corp.

- Rotocontrol GmbH

第七章 市场机会与未来展望

packaging printing market size in 2026 is estimated at USD 472.5 billion, growing from 2025 value of USD 437.78 billion with 2031 projections showing USD 691.97 billion, growing at 7.93% CAGR over 2026-2031.

Rapid digital transformation, soaring e-commerce activity, and stringent sustainability policies are reshaping technology selection, substrate choice, and regional investment priorities. Flexography keeps its volume edge thanks to productivity on long runs, yet brand owners now favor digital platforms for short batches that support SKU proliferation, variable data, and smart-pack functionality. UV-curable ink chemistry gains ground as converters look for lower energy use and faster throughput, while RFID-enabled packs strengthen supply-chain visibility. At a strategic level, converters combine hybrid press lines, localized micro-factories, and closed-loop material programs to defend margins in a market where brand loyalty depends on print quality, speed, and environmental footprint.

Global Packaging Printing Market Trends and Insights

Demand for RFID-enabled and Digital Printing

Widespread IoT connectivity is turning each package into a data node, and pressure-sensitive labels embedded with RFID are now common on high-value pharmaceuticals. Digital presses integrate serialized codes without plate changes, cutting unit costs and enabling real-time authentication. Consumer-facing apps read these identifiers to reveal provenance or loyalty offers, deepening engagement while assisting recall management. Converters that combine flexo efficiency with inline inkjet modules meet traceability mandates and win contracts that reward responsiveness.

Expansion of E-commerce Packaging Volumes

Direct-to-consumer logistics prioritize lightweight formats that protect goods, showcase graphics, and arrive swiftly. Print-on-demand networks such as Gelato's cut shipping distance by 90%, proving localized production scales once digital workflows replace analog set-up. Shorter run lengths - often below 10,000 units - push traditional offset out of contention, encouraging investment in high-speed inkjet and toner machines that deliver shelf-ready quality overnight. The packaging printing market benefits as every unboxing video becomes free advertising, pushing brands to refresh artwork more often.

High Capital Investment Requirements

A high-speed eight-color flexo line costs up to USD 2.94 million and demands auxiliary slitters, plate mounters, and solvent-recovery units. Smaller converters in Southeast Asia delay upgrades, risking obsolescence as brand owners insist on tighter tolerances. Leasing programs exist, but interest rates elevate the total cost of ownership. Consolidation, therefore, accelerates deep-pocketed groups buying family-run shops to unlock scale and negotiate better substrate contracts.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability Push for Eco-friendly Inks and Substrates

- Emerging-Market Consumption Boom

- Complex and Varying Global Printing Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flexography held a 34.78% share of the packaging printing market size in 2025, supported by unrivaled speed on film and paper webs. Hybrid press platforms now layer inkjet stations onto flexo units, enabling serial codes and regional graphics without slowing the run. Digital equipment records a 10.15% CAGR through 2031 as converters chase shorter cycles and SKU proliferation. Rotogravure retains a niche status in premium tobacco and cosmetics, where image fidelity justifies cylinder engraving costs. Offset lithography concentrates on folding cartons, while screen printing and other niche methods address tactile varnishes and metallic effects.

Investment data confirms the trajectory. Pack lines installed in 2025 feature predictive-maintenance sensors that cut unplanned downtime by 18%, and cloud-based color servers align artwork across plants in real time. Converters adopting the hybrid model report making ready waste down by 28% and TTM (time to market) halved for promotional packs. As such, equipment suppliers bundle workflow software with presses, locking in service revenue and strengthening aftermarket margins within the packaging printing market.

Solvent systems maintained a 39.62% share of the packaging printing market size in 2025. Yet UV-curable ink volumes rise at 9.52% CAGR as LED lamps curb power draw to 0.3-0.5 kWh per square meter versus 1.2-1.8 kWh for thermal ovens. Aqueous formulations grow fastest in paper-heavy segments where food contact regulations restrict VOCs. Latex and LED-UV chemistries address shrink labels and heat-sensitive films once off-limits to mercury-lamp curing.

Total-cost models favor UV in high-mix environments: plate washout stations disappear, inventory of solvents shrinks, and cure-on-demand lowers WIP. Resin volatility remains a risk, but multi-sourcing and in-house blending partly offset spikes. Ink suppliers invest in bio-based monomers and photoinitiators that pass compostability tests, aligning chemistry advances with the sustainability agenda permeating the packaging printing market.

The Packaging Printing Market Report is Segmented by Printing Technology (Offset Lithography, Rotogravure, and More), Ink Type (Solvent-Based Ink and More), Packaging Material (Labels, Plastic Containers and Films, Glass Containers, Metal Cans and Foils, and More), End-Use Industry (Food and Beverage, Pharmaceutical and Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific leads global output, housing more than half of new press installations in 2024. China's converters add multi-layer pouch lines to feed domestic snack demand, while India offers incentives for capital purchases under its Production-Linked Incentive scheme. Flexible packaging makers in Vietnam and Thailand gain from near-shoring, serving apparel exporters that need rapid swing tags and polybags. Cross-border investments elevate regional know-how, and joint ventures with Japanese ink suppliers improve quality consistency.

North American operators' position on technology and compliance. Investments in digital corrugated presses triple capacity for same-day e-commerce boxes, and state legislatures adopt extended producer responsibility fees that reward recyclable prints. U.S. converters also pioneer UV-LED retrofits, claiming 25% energy savings. Canada harmonizes food-contact limits with the FDA, easing cross-border sourcing, while Mexico attracts Tier-1 brands searching for tariff-free access under USMCA.the

Europe sets the regulatory tempo. The bloc's 88% packaging recycling target nudges brand guidelines toward mono-material laminates that rely on specialized inks. German machinery exports leverage Industrie 4.0 features such as real-time viscosity control, and Italian press builders bundle in-line cold-foil to court luxury houses. Eastern Europe, notably Poland, captures overflow work as labor rates undercut Western peers, yet workforce skills remain high. Innovation grants in the Netherlands fund pilot lines for paper-based barrier packs, sustaining momentum in the packaging printing market.

- Amcor plc

- Smurtfit WestRock

- Tetra Pak Group

- Mondi plc

- Huhtamaki Oyj

- CCL Industries Inc.

- Avery Dennison Corporation

- Sealed Air Corporation

- International Paper Company

- Stora Enso Oyj

- Sonoco Products Company

- Georgia-Pacific LLC

- Constantia Flexibles GmbH

- Mayr-Melnhof Karton AG

- Ahlstrom-Munksj Oyj

- Clondalkin Group Holdings BV

- Autajon Group SA

- SATO Holdings Corp.

- Rotocontrol GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for RFID-enabled and Digital Printing

- 4.2.2 Expansion of E-commerce Packaging Volumes

- 4.2.3 Sustainability Push for Eco-friendly Inks and Substrates

- 4.2.4 Emerging-market Consumption Boom

- 4.2.5 Brand-owner Adoption of Smart Pack Serialization

- 4.2.6 Rise of Localised Print-on-Demand Micro-Factories

- 4.3 Market Restraints

- 4.3.1 High Capital Investment Requirements

- 4.3.2 Complex and Varying Global Printing Regulations

- 4.3.3 Volatile Photoinitiator and Resin Prices

- 4.3.4 Shortage of Skilled Flexographic Press Operators

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 The Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Industry Ecosystem Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Printing Technology

- 5.1.1 Offset Lithography

- 5.1.2 Rotogravure

- 5.1.3 Flexography

- 5.1.4 Digital Printing

- 5.1.5 Other Printing Technologies

- 5.2 By Ink Type

- 5.2.1 Solvent-based Ink

- 5.2.2 UV-curable Ink

- 5.2.3 Aqueous Ink

- 5.2.4 Latex Ink

- 5.2.5 LED-UV Ink

- 5.3 By Packaging Material

- 5.3.1 Labels

- 5.3.2 Plastic Containers and Films

- 5.3.3 Glass Containers

- 5.3.4 Metal Cans and Foils

- 5.3.5 Paper and Paperboard Cartons

- 5.3.6 Flexible Pouches

- 5.3.7 Corrugated Boxes and Trays

- 5.4 By End-Use Industry

- 5.4.1 Food and Beverage

- 5.4.2 Pharmaceutical and Healthcare

- 5.4.3 Cosmetics and Personal Care

- 5.4.4 Household and Industrial

- 5.4.5 Electronics and Electrical

- 5.4.6 Other End-Use Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Vietnam

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Smurtfit WestRock

- 6.4.3 Tetra Pak Group

- 6.4.4 Mondi plc

- 6.4.5 Huhtamaki Oyj

- 6.4.6 CCL Industries Inc.

- 6.4.7 Avery Dennison Corporation

- 6.4.8 Sealed Air Corporation

- 6.4.9 International Paper Company

- 6.4.10 Stora Enso Oyj

- 6.4.11 Sonoco Products Company

- 6.4.12 Georgia-Pacific LLC

- 6.4.13 Constantia Flexibles GmbH

- 6.4.14 Mayr-Melnhof Karton AG

- 6.4.15 Ahlstrom-Munksj Oyj

- 6.4.16 Clondalkin Group Holdings BV

- 6.4.17 Autajon Group SA

- 6.4.18 SATO Holdings Corp.

- 6.4.19 Rotocontrol GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

包装印刷市场分析及预测(至2035年):依类型、产品类型、服务、技术、应用、材料类型、製程、最终用户及解决方案划分

包装印刷市场分析及预测(至2035年):依类型、产品类型、服务、技术、应用、材料类型、製程、最终用户及解决方案划分 全球包装印刷市场规模、份额、趋势和成长分析报告(2026-2034)

全球包装印刷市场规模、份额、趋势和成长分析报告(2026-2034) 2026年全球包装印刷市场报告2026年全球包装油墨和涂料市场报告

2026年全球包装印刷市场报告2026年全球包装油墨和涂料市场报告 包装印刷市场-全球产业规模、份额、趋势、机会及预测(依印刷技术、材料、应用、印刷油墨、地区及竞争格局划分,2021-2031年)全球包装印刷市场-2026-2031年预测

包装印刷市场-全球产业规模、份额、趋势、机会及预测(依印刷技术、材料、应用、印刷油墨、地区及竞争格局划分,2021-2031年)全球包装印刷市场-2026-2031年预测 包装印刷市场规模、份额及成长分析(按包装类型、印刷技术、印刷油墨、应用和地区划分)-2026-2033年产业预测

包装印刷市场规模、份额及成长分析(按包装类型、印刷技术、印刷油墨、应用和地区划分)-2026-2033年产业预测 包装油墨和涂料市场规模、份额和成长分析(按类型、技术、应用和地区划分)-2026-2033年产业预测包装印刷市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2024-2032 年)3D列印包装市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2024-2032)

包装油墨和涂料市场规模、份额和成长分析(按类型、技术、应用和地区划分)-2026-2033年产业预测包装印刷市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2024-2032 年)3D列印包装市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2024-2032)