|

市场调查报告书

商品编码

1910679

工业橡胶:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Industrial Rubber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

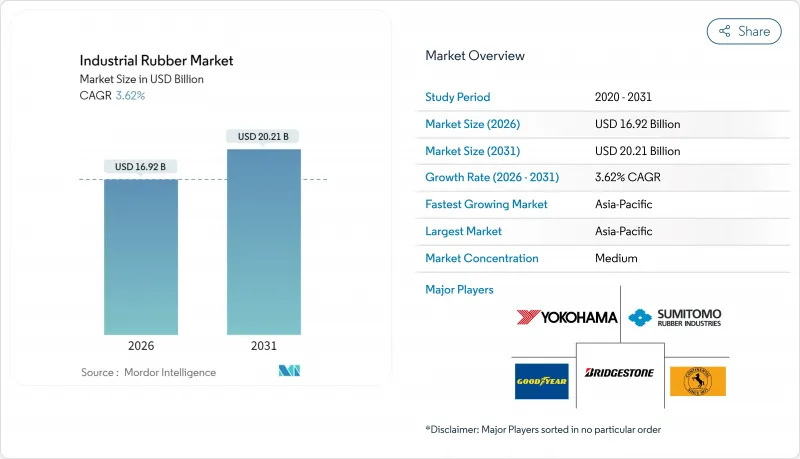

预计工业橡胶市场规模将从 2025 年的 163.3 亿美元成长到 2026 年的 169.2 亿美元,到 2031 年将达到 202.1 亿美元,2026 年至 2031 年的复合年增长率为 3.62%。

汽车、建筑、采矿和一般工业供应链对橡胶需求仍然强劲,合成橡胶凭藉其稳定的品质和规模优势,持续推动橡胶市场的发展。输送系统、传动设备和高压软管组件继续成为销售的主要驱动力,而生物基和再生橡胶替代品则稳步扩大了潜在需求。原油衍生原料价格波动和天然橡胶短缺影响橡胶供应的稳定性,能够平衡原料选择和回收能力的生产商可以降低收入波动。亚太地区占了市场的大部分份额,并受益于其集中的上游原料基地和下游製造地;而北美和欧洲则凭藉特种橡胶和监管方面的领先优势脱颖而出。

全球工业橡胶市场趋势与洞察

扩充用途:用作传送带和传动带

输送和动力传输系统是自动化物料搬运策略的基础,能够降低营运成本、减少事故发生率并提高能源效率。硬岩矿山、散货港口和小包裹分拣中心都指定使用多层阻燃输送带,即使在超过 200°C 的高温下也不会加速磨损。改良的橡胶化合物,例如丁腈橡胶混合物和芳香聚酰胺增强材料,与传统输送带相比,可将输送带寿命延长高达 25%。领先的製造商正在加速将智慧感测器阵列整合到输送带汽车胎体中,预测性维护计划已将计划外停机时间减少了约 35%。亚太地区的矿业和建筑材料供应商是最大的客户群体,但北美蓬勃发展的仓库和欧洲的回收设施也带来了不断增长的增值需求。

高压软管的需求不断增长

化学、石油天然气和先进製造业的扩张推动了对能够承受极端压力、快速弯曲和腐蚀性介质的软管的需求。领先的供应商正在开发氟橡胶、三元乙丙橡胶 (EPDM) 和氢化丁腈橡胶混合物,这些混合物能够承受超过 300 PSI 的压力和多种化学品的侵蚀,同时满足美国食品药物管理局 (FDA) 和欧盟食品接触法规的要求。製造商在开发复合材料的同时,也正在开发压接接头技术,以缩短组装时间并提高脉衝循环寿命。诸如Bridgestone在 2024 年收购 Klein Hose & Hydraulics 等策略性收购,标誌着企业正在努力建立产品和服务能力。客製化工程组件、现货产品和本地认证中心进一步增强了企业在这个多品种、小批量细分市场的竞争优势。

严格的环境法规

美国环保署 (EPA) 加强了轮胎和混合橡胶加工过程中有害空气污染物排放量限制在每吨 64 克以内,并强制要求工厂在 2027 年前维修。欧洲的反森林砍伐法规要求天然橡胶进口必须完全可追溯,这增加了采购成本和文件负担。加州对 6PPD 轮胎添加剂的调查引发了关于配方改良的讨论,因为人们担心其耐久性问题。同时,全球逐步淘汰 PFAS 的提案正在推动氟橡胶的开发平臺。合规成本对中小规模的橡胶生产商构成挑战,但对于率先采用清洁溶剂、闭合迴路清洁系统和生物基原料的企业而言,却能带来许多好处。

细分市场分析

合成橡胶(主要为苯乙烯-丁二烯基橡胶)将继续占据工业橡胶市场的主导地位,预计到2025年将占市场份额的70.54%,这主要得益于汽车製造商、机械设备製造商和基础设施建设者对在宽温度范围内保持稳定性能的需求。催化剂和工艺的重大创新提高了橡胶的拉伸强度、耐磨性和耐油性,使其性能能够满足严格的OEM规格要求。从废弃轮胎和抛光材料中回收的再生橡胶正以4.78%的复合年增长率增长,这主要得益于其与原生材料相比可节省30-50%的成本,以及对循环经济日益增长的需求。混炼商正在重新设计配方,以在不影响硫化速度的前提下,容纳高达25%的再生橡胶含量,有助于减少整体废弃物。天然橡胶供应对于搭乘用轮胎的耐用性和重型越野车的抓地力仍然至关重要,但东南亚的生产商正面临着因病害导致的产量下降问题。由植物来源的生物基合成橡胶(特别是生物丁二烯和聚异戊二烯)正在进行中试规模测试,有望缓解资源压力并减少碳足迹。

到2025年,挤出成型将占据工业橡胶市场44.70%的份额,尤其适用于软管、型材和密封条的连续生产,这些产品对尺寸精度和废品率要求极高。现代螺桿设计可将产量提高15%,而即时黏度监测系统则可加快换模速度。射出成型成型和压缩成型受益于多腔模具和自动脱模机器人,在汽车衬套和隔振装置的大量生产中仍然发挥关键作用。积层製造作为一项新兴技术,预计将以4.05%的复合年增长率实现最快增长,其利用3D列印热塑性聚氨酯晶格製造轻量化、复杂形状的零件,应用于航太、国防和医疗领域。光聚合异戊二烯树脂的进步使得断裂伸长率超过200%的弹性体零件成为可能,并将功能原型生产时间从数週缩短至数天。压延製程凭藉精密辊压系统提供的精确厚度控制,持续为特种板材市场、屋顶膜材、储槽衬里和隔膜板提供支援。

区域分析

预计到2025年,亚太地区将占据工业橡胶市场58.60%的份额,年复合成长率达4.00%。这得归功于从人工林到橡胶化合物的完整供应链、大规模的轮胎生产能力以及广泛的基础设施规划。在中国,电动车的普及(约占新车销售的三分之一)正在推动对特种轮胎和密封胶的需求。泰国和印尼的天然橡胶产量占全球总产量的60%以上,但病虫害爆发和劳动力短缺给产量带来了压力。两国政府正透过机械化支持树液采集和下游加工的现代化。印度正透过扩大国内橡胶化合物生产厂规模和推广再生橡胶回收网络来改善其进出口平衡。

北美经济维持约5%的年成长率,这主要得益于航太、页岩能源和物流基础建设的推动。美国约90%的天然橡胶需求依赖进口,而关于国内银胶菊种植的政策讨论正在升温,以增强供应的韧性。在加拿大,关键矿产开采的扩张带动了对传送带和软管的需求,而墨西哥则正吸引原始设备製造商(OEM)的投资,以使其供应链更靠近美国消费区。

欧洲的需求结构正受到严格的环境法规和生物基材料快速商业化的影响。欧盟的反森林砍伐法规要求橡胶进口必须可追溯,并鼓励贸易商采用电子帐簿。德国和法国率先引入了蒲公英天然橡胶试点农场,与东南亚橡胶相比,减少了运输排放。东欧的轮胎工厂正获得大量资金注入,用于在国内生产大尺寸电动车轮胎,从而在运输不确定性加剧的情况下减少对亚洲进口的依赖。

随着基础设施计划开闢新的需求通道,拉丁美洲和中东/非洲在全球市场的份额正稳步增长。巴西已恢復公共工程支出,主要用于桥樑维修和港口扩建,从而推动了对橡胶轴承和软管组件的需求。波湾合作理事会(GCC)正在加速摆脱对油气的依赖,实现经济多元化,其石化联合企业指定使用耐酸性气体的三元乙丙橡胶(EPDM)密封件和丁腈橡胶软管。撒哈拉以南非洲的铜矿和锂矿开采前景支撑了对输送带的需求,但计划开发取决于政治稳定和资金筹措管道。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 扩展用途,用作传送带和动力传输带

- 高压软管的需求不断增长

- 电动主导对轻量化汽车零件的需求正在成长。

- 新兴国家基础建设发展进展

- 向生物基合成橡胶过渡

- 市场限制

- 严格的环境法规

- 原物料价格波动与原油价格相关

- 再生橡胶的迅速普及正在蚕食新的需求。

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按橡胶类型

- 天然橡胶

- 合成橡胶

- 再生橡胶

- 透过流程

- 挤出成型

- 模具和铸造

- 日历管理

- 3D列印/积层製造

- 透过使用

- 输送机

- 动力传动带

- 高压软管

- 其他用途(屋顶材料、管材、捲材等)

- 按最终用户行业划分

- 汽车/运输设备

- 建筑和基础设施

- 采矿和金属

- 工业机械及设备

- 化工/石油化工

- 航太/国防

- 电气和电子设备

- 其他的

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 泰国

- 印尼

- 越南

- 马来西亚

- 菲律宾

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧国家

- 土耳其

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 南非

- 奈及利亚

- 埃及

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Bando Chemical Industries, LTD.

- Bridgestone Industrial

- China Petrochemical Corporation(Sinopec)

- ContiTech Deutschland GmbH

- Denka Company Limited

- ENEOS Materials Corporation

- Parker Hannifin Corp

- SIBUR Holding PJSC

- Sumitomo Rubber Industries, Ltd.

- The Goodyear Tire & Rubber Company

- THE YOKOHAMA RUBBER CO., LTD.

- Trelleborg AB

- Trinseo

- TSRC

- UBE Corporation

第七章 市场机会与未来展望

The industrial rubber market is expected to grow from USD 16.33 billion in 2025 to USD 16.92 billion in 2026 and is forecast to reach USD 20.21 billion by 2031 at 3.62% CAGR over 2026-2031.

Demand remains firmly anchored in automotive, construction, mining and general-industrial supply chains, with synthetic grades supplying consistent quality and scale advantages. Conveyor systems, transmission equipment and high-pressure hose assemblies continue to pull large volumes, while bio-based and reclaimed alternatives steadily widen addressable demand. Supply-side resilience is shaped by volatile crude-derived feedstocks and natural-rubber shortages; producers that balance raw-material optionality with recycling capabilities reduce earnings volatility. Asia-Pacific, holding a decisive majority share, benefits from integrated upstream raw-material bases and downstream manufacturing density, whereas North America and Europe differentiate through specialty rubber grades and regulatory compliance leadership.

Global Industrial Rubber Market Trends and Insights

Increasing application as conveyor & transmission belts

Conveyor and transmission systems underpin automated material-handling strategies that lower operating costs, cut accident frequency and boost energy efficiency. Hard-rock mining, bulk-cargo ports and parcel-sorting hubs specify multi-ply, flame-retardant belts that handle temperatures exceeding 200 °C without accelerated abrasion. Upgraded rubber compounds, often nitrile-blended or aramid-reinforced, extend belt life by up to 25% compared with conventional compounds. Major producers increasingly integrate smart-sensor arrays into belt carcasses, enabling predictive-maintenance programs that reduce unscheduled downtime by nearly 35%. Asia-Pacific miners and construction material suppliers represent the largest customer pool, but value-added demand is rising in North America's warehousing boom and Europe's recycling facilities.

Growing demand for high-pressure hoses

Expanding chemical, oil-and-gas and advanced-manufacturing activity elevates the need for hoses that tolerate extreme pressure, rapid flexing and aggressive media. Leading suppliers formulate fluoroelastomer, EPDM and hydrogenated nitrile blends to withstand over 300 PSI and multi-chemical exposure while meeting FDA and EU food-contact regulations. Producers complement compound development with crimp-coupling innovations that shorten assembly times and improve impulse-cycle life. Strategic acquisitions-such as Bridgestone's 2024 purchase of Cline Hose & Hydraulics-illustrate the push to own both product and service footprints. Custom-engineered assemblies, ship-to-stock delivery models and local certification centers round out competitive advantages in this high-mix application space.

Stringent environmental regulations

The U.S. EPA tightened National Emission Standards for Hazardous Air Pollutants in tire and mixed-rubber processing, capping volatile organics at 64 g per tonne and compelling plant retrofits by 2027. Europe's Deforestation Regulation obliges full traceability for natural-rubber imports, raising procurement costs and documentation burdens. California's investigation into 6PPD tire additives forces compound reformulation discussions amid durability concerns, while global proposals to phase out PFAS push fluoroelastomer R&D pipelines. Compliance outlays challenge smaller compounders but reward early adopters of cleaner solvents, closed-loop wash systems and bio-based feedstocks.

Other drivers and restraints analyzed in the detailed report include:

- EV-led boom in lightweight automotive components

- Infrastructure build-out in emerging economies

- Volatile crude-oil-linked feedstock prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Synthetic grades, dominated by styrene-butadiene, retained a commanding 70.54% share of the industrial rubber market in 2025 as automakers, machinery OEMs and infrastructure builders demanded consistent performance across broad temperature windows. Extensive catalyst and process innovations boost tensile strength, abrasion resistance and oil tolerance, aligning properties with stringent OEM specifications. Reclaimed rubber, harvested from devulcanized end-of-life tires and buffings, expands at a 4.78% CAGR on the back of 30-50% cost savings versus virgin feedstocks and mounting circular-economy mandates. Compounders re-engineer formulations to accommodate reclaimed content of up to 25% without compromising cure kinetics, thereby moderating overall scrap. Natural-rubber supply remains central to passenger-tire elasticity and heavy-haul off-road grip, yet producers wrestle with disease-related yield drops in Southeast Asia. Bio-based synthetic routes, particularly bio-butadiene and polyisoprene from plant sugars, advance pilot-scale trials that promise to ease resource pressures while shrinking carbon footprints.

Extrusion held 44.70% share of the industrial rubber market size in 2025, favored for continuous production of hoses, profiles and sealing strips where dimensional accuracy and low scrap rates are critical. State-of-the-art screw designs increase throughput 15% and support real-time viscosity monitoring systems that cut change-over time. Injection and compression molding retain vital roles for high-volume automotive bushings and vibration isolators, benefitting from multi-cavity tooling and automated demolding robotics. Additive manufacturing, while only emerging, records the fastest 4.05% CAGR as aerospace, defense and medical users exploit 3D-printed thermoplastic polyurethane lattices for lightweight, complex geometries. Advances in photopolymerizable isoprene resins yield elastomeric parts with elongation at break surpassing 200%, bringing functional prototypes within days rather than weeks. Calendaring sustains specialty sheet markets, roofing membranes, tank linings and diaphragm sheets, thanks to microscopic gauge control afforded by precision-roll systems.

The Industrial Rubber Market Report is Segmented by Rubber Type (Natural Rubber, Synthetic Rubber, and More), Process (Extrusion, Molding and Casting, and More), Application (Conveyor Belts, Transmission Belts, and More), End-User Industry (Automotive and Transportation, Construction and Infrastructure, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained 58.60% share of the industrial rubber market in 2025 and is advancing at a 4.00% CAGR, underscored by its integrated plantation-to-compound supply chains, large-scale tire capacities, and vast infrastructure programs. China drives demand through EV adoption rates approaching one-third of new car sales, heightening traction for specialty tire and sealing compounds. Thailand and Indonesia together account for more than 60% of global natural-rubber output, but yields are strained by disease incidence and labor shortages, prompting government support for mechanized tapping and downstream processing upgrades. India tightens its import-export balance by expanding domestic mixing houses and encouraging reclaimed-rubber collection networks.

North America sustains mid-single-digit growth anchored in aerospace, shale-energy and logistics construction. The U.S. imports roughly 90% of its natural-rubber needs, sparking policy discourse around domestic guayule cultivation to improve supply resilience. Canada's mining expansion in critical minerals feeds conveyor-belt and hose demand, while Mexico captures OEM investments relocating supply chains closer to U.S. consumer bases.

Europe's demand profile is shaped by strict environmental regulations and rapid commercialization of bio-based materials. The EU Deforestation Regulation compels traceability for rubber imports, catalyzing digital ledger adoption among traders. Germany and France pioneer dandelion-based natural-rubber pilot farms that lower transport emissions compared with Southeast-Asian supply. Eastern European tire plants receive significant capital infusions to produce larger-rim EV tires domestically, reducing reliance on Asian imports amid shipping volatility.

Latin America and Middle East & Africa collectively contribute a modest but rising share as infrastructure projects launch new demand corridors. Brazil restarts public-works spending focused on bridge retrofits and port expansion, increasing calls for rubber bearings and hose assemblies. The Gulf Cooperation Council accelerates industrial diversification beyond hydrocarbons, with petrochemical complexes specifying EPDM seals and nitrile hoses resistant to sour gas exposure. Sub-Saharan African mining prospects in copper and lithium underpin conveyor-belt demand, yet project rollouts hinge on political stability and financing access.

- Bando Chemical Industries, LTD.

- Bridgestone Industrial

- China Petrochemical Corporation (Sinopec)

- ContiTech Deutschland GmbH

- Denka Company Limited

- ENEOS Materials Corporation

- Parker Hannifin Corp

- SIBUR Holding PJSC

- Sumitomo Rubber Industries, Ltd.

- The Goodyear Tire & Rubber Company

- THE YOKOHAMA RUBBER CO., LTD.

- Trelleborg AB

- Trinseo

- TSRC

- UBE Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing application as conveyor & transmission belts

- 4.2.2 Growing demand for high-pressure hoses

- 4.2.3 EV-led boom in lightweight automotive components

- 4.2.4 Infrastructure build-out in emerging economies

- 4.2.5 Shift to bio-based synthetic rubbers

- 4.3 Market Restraints

- 4.3.1 Stringent environmental regulations

- 4.3.2 Volatile crude-oil-linked feedstock prices

- 4.3.3 Rapid uptake of reclaimed rubber cannibalising virgin demand

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Rubber Type

- 5.1.1 Natural Rubber

- 5.1.2 Synthetic Rubber

- 5.1.3 Reclaimed Rubber

- 5.2 By Process

- 5.2.1 Extrusion

- 5.2.2 Molding and Casting

- 5.2.3 Calendaring

- 5.2.4 3-D Printing / Additive Manufacturing

- 5.3 By Application

- 5.3.1 Conveyor Belts

- 5.3.2 Transmission Belts

- 5.3.3 Pressure Hoses

- 5.3.4 Other Application (Roofing, Tubes, Rolls, etc.)

- 5.4 By End-User Industry

- 5.4.1 Automotive and Transportation

- 5.4.2 Construction and Infrastructure

- 5.4.3 Mining and Metals

- 5.4.4 Industrial Machinery and Equipment

- 5.4.5 Chemical and Petrochemical

- 5.4.6 Aerospace and Defence

- 5.4.7 Electrical and Electronics

- 5.4.8 Others

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Thailand

- 5.5.1.6 Indonesia

- 5.5.1.7 Vietnam

- 5.5.1.8 Malaysia

- 5.5.1.9 Philippines

- 5.5.1.10 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Turkey

- 5.5.3.9 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 South Africa

- 5.5.5.5 Nigeria

- 5.5.5.6 Egypt

- 5.5.5.7 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Bando Chemical Industries, LTD.

- 6.4.2 Bridgestone Industrial

- 6.4.3 China Petrochemical Corporation (Sinopec)

- 6.4.4 ContiTech Deutschland GmbH

- 6.4.5 Denka Company Limited

- 6.4.6 ENEOS Materials Corporation

- 6.4.7 Parker Hannifin Corp

- 6.4.8 SIBUR Holding PJSC

- 6.4.9 Sumitomo Rubber Industries, Ltd.

- 6.4.10 The Goodyear Tire & Rubber Company

- 6.4.11 THE YOKOHAMA RUBBER CO., LTD.

- 6.4.12 Trelleborg AB

- 6.4.13 Trinseo

- 6.4.14 TSRC

- 6.4.15 UBE Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-needs assessment

- 7.2 Introducing New Manufacturing Techniques to Reduce Hazardous Waste

工业橡胶市场:依产品类型、材料类型、製造流程和最终用途产业划分-2026-2032年全球市场预测

工业橡胶市场:依产品类型、材料类型、製造流程和最终用途产业划分-2026-2032年全球市场预测 全球工业橡胶製品市场规模、份额、趋势和成长分析报告(2026-2034年)

全球工业橡胶製品市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球工业橡胶市场报告

2026年全球工业橡胶市场报告 工业橡胶市场规模、份额和成长分析(按类型、产品类型、产品加工和地区划分)-2026-2033年产业预测

工业橡胶市场规模、份额和成长分析(按类型、产品类型、产品加工和地区划分)-2026-2033年产业预测 工业橡胶市场-全球产业规模、份额、趋势、机会及预测(按类型、应用、地区和竞争细分,2020-2030 年)

工业橡胶市场-全球产业规模、份额、趋势、机会及预测(按类型、应用、地区和竞争细分,2020-2030 年) 全球工业橡胶市场(依最终使用流程、类型、产品、应用和地区划分)-预测至2030年

全球工业橡胶市场(依最终使用流程、类型、产品、应用和地区划分)-预测至2030年 全球工业橡胶市场:产业分析、规模、占有率、成长、趋势和预测(2024-2031 年)全球工业橡胶市场规模(按类型、产品、应用、地区、范围和预测)

全球工业橡胶市场:产业分析、规模、占有率、成长、趋势和预测(2024-2031 年)全球工业橡胶市场规模(按类型、产品、应用、地区、范围和预测)