|

市场调查报告书

商品编码

1910680

浸渍树脂:市场份额分析、行业趋势和统计数据、成长预测(2026-2031)Impregnating Resins - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

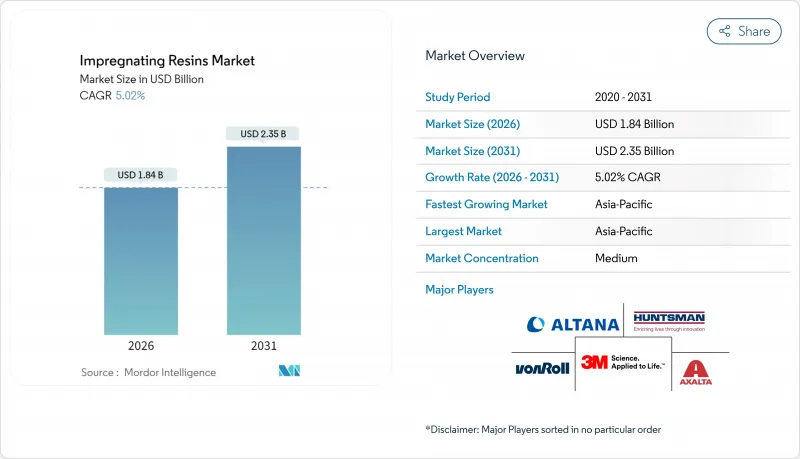

预计到 2025 年,浸渍树脂市场价值将达到 17.5 亿美元,到 2026 年将成长至 18.4 亿美元,到 2031 年将成长至 23.5 亿美元,在预测期(2026-2031 年)内复合年增长率为 5.02%。

马达、发电机、变压器和电力电子模组对高效电绝缘材料的强劲需求推动了这一市场扩张。原始设备製造商 (OEM) 越来越多地指定采用真空压力浸渍 (VPI) 系统,以提高介电强度并降低局部放电损耗,从而确保可再生能源和电动车平台的持久性能。大型离岸风力发电机、高压电动车的普及以及智慧电网的日益复杂化,都推动了高品质液体绝缘材料未来多年的采购需求。对先进 VPI 设备的持续资金需求有利于拥有垂直整合的树脂和机械产品线的成熟製造商,并逐步提高浸渍树脂市场的集中度。

全球浸渍树脂市场趋势及展望

对高效电动机的需求正在成长

全球法规正推动工业马达损耗限制的日益严格。在美国,能源部修订的法规规定了各功率等级的最低额定效率。这些基准值促使马达绕组采用真空浸渍(VPI)处理,从而降低热点温度、抑制振动并延长重绕週期。为了满足能源审核标准,製造商指定使用耐温等级为180°C且损耗係数低的浸渍树脂。随着工厂寻求降低营运成本,浸渍树脂市场对维修套件和现场服务树脂的售后需求持续成长。类似的更换週期也在东南亚和拉丁美洲的中型工业区出现,增强了中期成长动能。

原始设备製造商转向无溶剂浸渍工艺

美国环保署 (EPA) 2025 年气溶胶涂料反应性修正案以及日益严格的欧洲挥发性有机化合物 (VOC)排放限值,正在加速向 100%固态、不排放任何受管制溶剂的系统过渡。无溶剂树脂可在真空条件下高效渗透捲绕线圈,并在可控温度下快速聚合,从而消除工人接触风险,并有助于获得 ISO 14001 认证。像 Gehring 的 IMFLEX 这样的感应加热滴涂生产线展现出工艺柔软性,与传统的浸渍烘烤生产线相比,可将循环时间缩短 20%。通风负载的降低和废弃物处理方案的简化所带来的成本节约,使得无溶剂生产线实际上成为新建工厂的首选资本投资方案。这些营运优势正在增强已开发国家和新兴市场浸渍树脂市场的成长动能。

加强挥发性有机化合物和高空气污染综合症法规

全球监管机构持续降低工业涂料中挥发性有机化合物(VOC)的容许量。加拿大2024年的法规对130种产品设定了浓度限制,要求重新配製或退出市场。南加州修订后的汽车涂料1151号规则意味着对电气绝缘应用的监管也将收紧,导致合规文件和测试成本增加。小规模的树脂配方商通常缺乏内部环境人员或溶剂回收设施,这限制了它们在优先考虑绿色化学的原始设备製造商(OEM)合约竞争中的能力。两年或更短的过渡期压缩了资本规划时间,导致一些区域企业选择退出浸渍树脂市场,而不是承担升级成本。

细分市场分析

预计到2025年,无溶剂配方将占据浸渍树脂市场64.12%的份额,并在2031年之前以5.10%的复合年增长率超越所有其他替代配方。此优势源自于其100%固态的化学特性,此特性使得定子迭片能够在真空环境下进行无气泡浸渍,从而达到H级和N级热等级。这减少了局部放电事件,并延长了牵引和风力发电机定子的使用寿命。电厂营运人员指出,无溶剂配方消除了消防法规的限制,并显着降低了烟气洗涤设备的负荷,从而在维修的两年内降低了营运成本。

我们的创新研发管线持续改进用于自动化滴涂和辊涂製程的无溶剂流变技术。近期经RSC认证的聚酯网路材料实现了331°C (700°F)的劣化起始温度,介电损耗较基准降低了38%,从而拓展了其在高频逆变器领域的应用范围。 IEEE 275-1992和1553-2002评估通讯协定指导OEM製造商的认证,并确保新型树脂能够与现有绝缘系统无缝整合。虽然溶剂型树脂仍被用于一些注重延长适用期的小型复绕厂,但随着监管和保险政策的利好,其市场份额正在逐年下降。因此,早期投资固态溶剂设备的製造商获得了溢价和特许权使用费,巩固了在主导地位。

浸渍树脂报告依技术(无溶剂树脂与溶剂型树脂)、树脂类型(环氧树脂、聚酯树脂、聚酯酰亚胺树脂及其他树脂类型)、应用领域(马达及发电机、家用电器、变压器、电气及电子元件等)及地区(亚太地区、北美地区、欧洲地区等)进行细分。市场预测以美元以金额为准。

区域分析

预计到2025年,亚太地区将占全球浸渍树脂市场收入的41.20%,并在2031年之前保持5.11%的复合年增长率,成为成长最快的地区。中国在电机生产领域的领先地位将保持区域需求的强劲,而福建和广东两省针对离岸风力发电丛集的定向奖励也确保了树脂需求的增长。印度针对高效能家用电器的绩效奖励为下游企业带来了巨大的发展机会,因为国内製造商正在扩大其真空浸渍(VPI)生产线。东南亚国家凭藉其具有竞争力的劳动力成本和不断增长的电子产品出口,正在巩固其本地浸渍树脂产能,为构建区域供应链、供应全球原始设备製造商(OEM)网路奠定基础。

北美市场正经历成熟但强劲的需求,这主要得益于车辆电气化、工业资本投资的復苏以及电网现代化项目。主要树脂製造商目前正使用再生能源运作其在美国和墨西哥的工厂,从而降低产品的碳足迹,并为原始设备製造商 (OEM) 提供范围 3排放优势。美国能源局的马达和变压器标准正在推动维修,并将监管措施与可预测的树脂销售挂钩。加拿大将于 2024 年生效的 VOC 法规将进一步推动无溶剂解决方案的发展,并为技术先进的供应商提供市场机会。

儘管面临能源价格波动,欧洲仍持续推行有利于低排放树脂的前瞻性政策,例如将于2026年生效的REACH法规附件十七甲醛限制。北海和波罗的海离岸风力发电装置量的快速增长巩固了对高性能硅酮的需求,部分抵消了家用电器生产放缓的影响。对进口环氧树脂征收的反倾销税支持了国内树脂生产,但也给下游加工带来了成本压力。整体而言,浸渍树脂市场保持着均衡的地理分布,亚太地区的规模、北美地区以标准主导的升级改造以及欧洲在环境技术领域的领先地位,共同构成了互补的成长支柱。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 对高效电动机的需求正在成长

- 原始设备製造商转向无溶剂浸渍工艺

- 电网级风力发电机装机量的成长

- 加快电动车驱动马达的生产

- 家用电子电器的微型化

- 市场限制

- 加强对挥发性有机化合物(VOCs)和有害空气污染物(HAPS)的监管

- 双酚A和苯乙烯原料的价格波动

- 资本密集型真空和压力设备

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 透过技术

- 无溶剂树脂

- 溶剂型树脂

- 依树脂类型

- 环氧树脂

- 聚酯纤维

- 聚酯酰亚胺

- 其他树脂类型(聚氨酯、硅酮等)

- 透过使用

- 马达和发电机

- 家用电器

- 变压器

- 电气和电子元件

- 汽车零件

- 其他用途

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 南非

- 奈及利亚

- 埃及

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- 3M

- AEV Group

- Axalta Coating Systems, LLC

- BASF

- Borger GmbH

- Chetak Manufacturing Company

- ALTANA(ELANTAS)

- Henkel AG and Co. KGaA

- Huntsman International LLC

- Momentive

- NIPPON RIKA INDUSTRIES CORPORATION

- Resonac Holdings Corporation

- Von Roll

- Wacker Chemie AG

第七章 市场机会与未来展望

The Impregnating Resins Market was valued at USD 1.75 billion in 2025 and estimated to grow from USD 1.84 billion in 2026 to reach USD 2.35 billion by 2031, at a CAGR of 5.02% during the forecast period (2026-2031).

Robust demand for high-efficiency electrical insulation in motors, generators, transformers, and power-electronics modules underpins this expansion. Original-equipment manufacturers increasingly specify vacuum pressure impregnation (VPI) systems that elevate dielectric strength and cut partial-discharge losses, supporting durable performance in renewables and e-mobility platforms. Scale-up of offshore wind turbines, higher-voltage electric vehicles, and smart-grid upgrades reinforce multi-year procurement pipelines for premium liquid insulation. Persistent capital requirements for advanced VPI equipment favor established players with vertically integrated resin and machinery offerings, gradually concentrating the impregnating resins market.

Global Impregnating Resins Market Trends and Insights

Surging Demand for High-Efficiency Electric Motors

Global regulations now mandate tighter loss limits for industrial motors; in the United States, updated Department of Energy rules require minimum nominal efficiencies across horsepower classes. These thresholds spur retrofits with VPI-treated windings that cut hot-spot temperatures, reduce vibration, and extend rewind intervals. Manufacturers consequently specify impregnating resins that tolerate 180 °C thermal classes and exhibit a low dissipation factor to meet energy audits. As plants chase operational expense reductions, the impregnating resins market sees stable aftermarket demand for rewind kits and field-service resins. Mid-size industrial hubs in Southeast Asia and Latin America replicate this replacement cycle, reinforcing the medium-term growth impulse.

OEM Shift Toward Solvent-Free Impregnation Processes

The U.S. Environmental Protection Agency's 2025 amendments on aerosol-coating reactivity, plus Europe's evolving VOC caps, accelerate the transition to 100% solids systems that release no regulated solvents. Solventless resins penetrate winding stacks efficiently under vacuum, polymerize faster under controlled heat, and remove worker-exposure liabilities, enabling ISO 14001 certification. Induction-heated trickle lines such as Gehring's IMFLEX illustrate process agility, cutting cycle times by 20% versus conventional dip-and-bake lines. Cost savings accrue from lower ventilation loads and simpler waste-treatment schemes, making solventless lines the de-facto capex choice for greenfield plants. These operational gains reinforce the impregnating resins market trajectory in developed and emerging economies alike.

VOC and HAPS Regulatory Tightening

Authorities worldwide keep lowering permissible VOC thresholds for industrial coatings; Canada's 2024 rules cap concentrations across 130 product classes, requiring reformulation or market withdrawal. Southern California's revised Rule 1151 on automotive coatings signals similar tightening for electrical-insulation applications, adding compliance documentation and lab-testing expenses. Smaller resin formulators often lack in-house environmental staff and solvent-recovery infrastructure, constraining their ability to compete for OEM contracts prioritizing green chemistry. Transition timelines of two years or less compress capital-planning windows, prompting some regional players to exit the impregnating resins market rather than absorb upgrade costs.

Other drivers and restraints analyzed in the detailed report include:

- Grid-Scale Wind-Turbine Installation Growth

- Miniaturization of Consumer Electronics

- Price Volatility of Bisphenol-A and Styrene Feedstocks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solventless formulations account for 64.12% of the impregnating resins market share in 2025, outpacing all alternatives with a 5.10% CAGR to 2031. This dominance derives from the ability of 100% solids chemistries to impregnate stator stacks under high vacuum without entrapped air pockets, yielding class H and class N thermal ratings. The resulting reduction in partial-discharge inception bolsters service lives of traction and wind-generator stators. Plant operators emphasize solvent elimination because it removes fire-code constraints and slashes exhaust-scrubber loads, shrinking operating costs within two years of retrofit.

Innovation pipelines continue to refine solventless rheology for automated trickling and roll-dip methods. Recent RSC-documented polyester networks achieve 331 °C onset degradation and 38% lower dielectric loss versus baseline, expanding suitability for high-frequency inverters. IEEE 275-1992 and 1553-2002 evaluation protocols guide OEM qualifications, ensuring that new resin grades integrate seamlessly with existing insulation systems. Solvent-based grades persist in niche rewind shops that value extended pot life, yet their share erodes annually as regulatory and insurance incentives favor solids technology. Consequently, producers that invested early in solventless assets enjoy pricing premiums and loyalty contracts, solidifying leadership positions across the global impregnating resins market.

The Impregnating Resins Report is Segmented by Technology (Solventless Resins and Solvent-Based Resins), Resin Type (Epoxy, Polyester, Polyester-Imide, and Other Resin Types), Application (Motors and Generators, Home Appliances, Transformers, Electrical and Electronic Components, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 41.20% of 2025 sales in the impregnating resins market and posts the quickest 5.11% CAGR to 2031. China's dominance in electric-motor production keeps regional demand vibrant, while targeted incentives for offshore wind clusters in Fujian and Guangdong provinces guarantee resin pull-through. India's performance incentives for high-efficiency appliances signal a sizable downstream opportunity as domestic manufacturers scale VPI lines. Southeast Asian nations leverage competitive labor costs and growing electronics exports to source localized impregnating capacity, anchoring regional supply chains that feed global OEM networks.

North America exhibits mature but resilient demand underpinned by automotive electrification, rebounding industrial capex, and grid modernization programs. Major resin suppliers now run U.S. and Mexican plants on renewable electricity, shrinking product carbon footprints and giving OEMs a Scope 3 emissions advantage. U.S. Department of Energy motor and transformer standards drive retrofits, translating regulatory action into predictable resin sales. Canada's VOC rules, effective 2024, further push solventless adoption, giving technologically advanced suppliers a market opening.

Europe navigates energy-price volatility yet sustains forward-looking policy drivers such as REACH Annex XVII formaldehyde limits effective 2026, which favor low-emission resins. Offshore-wind installation rates in the North Sea and Baltic Sea lock in high-performance silicone demand, partially offsetting weaker appliance production. Anti-dumping tariffs on foreign epoxy imports shore up domestic resin manufacturing, though they add cost pressure downstream. Overall, the impregnating resins market retains a balanced geographic footprint with Asia-Pacific's scale, North America's standards-driven upgrades, and Europe's environmental-technology leadership acting as complementary growth pillars.

- 3M

- AEV Group

- Axalta Coating Systems, LLC

- BASF

- Borger GmbH

- Chetak Manufacturing Company

- ALTANA (ELANTAS)

- Henkel AG and Co. KGaA

- Huntsman International LLC

- Momentive

- NIPPON RIKA INDUSTRIES CORPORATION

- Resonac Holdings Corporation

- Von Roll

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for High-Efficiency Electric Motors

- 4.2.2 OEM Shift toward Solvent-Free Impregnation Processes

- 4.2.3 Grid-Scale Wind-Turbine Installation Growth

- 4.2.4 EV Traction-Motor Production Acceleration

- 4.2.5 Miniaturisation of Consumer Electronics

- 4.3 Market Restraints

- 4.3.1 VOC and HAPS Regulatory Tightening

- 4.3.2 Price Volatility of Bisphenol-A and Styrene Feedstocks

- 4.3.3 Capital-Intensive Vacuum-Pressure Equipment

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Solventless Resins

- 5.1.2 Solvent-based Resins

- 5.2 By Resin Type

- 5.2.1 Epoxy

- 5.2.2 Polyester

- 5.2.3 Polyester-imide

- 5.2.4 Other Resin Types (Polyurethane, silicone, etc.)

- 5.3 By Application

- 5.3.1 Motors and Generators

- 5.3.2 Home Appliances

- 5.3.3 Transformers

- 5.3.4 Electrical and Electronic Components

- 5.3.5 Automotive Components

- 5.3.6 Other Applications

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordic Countries

- 5.4.3.7 Russia

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 South Africa

- 5.4.5.5 Nigeria

- 5.4.5.6 Egypt

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 AEV Group

- 6.4.3 Axalta Coating Systems, LLC

- 6.4.4 BASF

- 6.4.5 Borger GmbH

- 6.4.6 Chetak Manufacturing Company

- 6.4.7 ALTANA (ELANTAS)

- 6.4.8 Henkel AG and Co. KGaA

- 6.4.9 Huntsman International LLC

- 6.4.10 Momentive

- 6.4.11 NIPPON RIKA INDUSTRIES CORPORATION

- 6.4.12 Resonac Holdings Corporation

- 6.4.13 Von Roll

- 6.4.14 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment