|

市场调查报告书

商品编码

1910714

腐植酸:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Humic Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

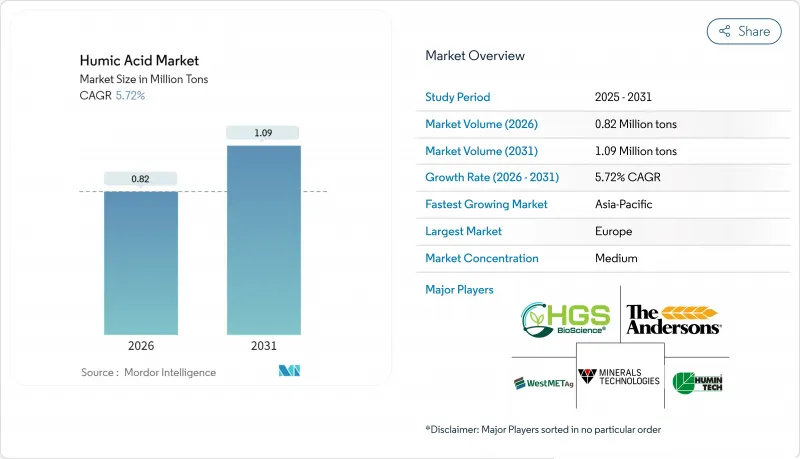

预计腐植酸市场规模将从 2025 年的 78 万吨成长到 2026 年的 82 万吨,到 2031 年将达到 109 万吨,2026 年至 2031 年的复合年增长率为 5.72%。

这一成长轨迹反映出,在政府化肥监管日益严格以及碳市场中土壤有机碳增值价值不断提升的背景下,生物来源土壤健康解决方案的接受度日益提高。再生农业的扩张,加上可控环境农业的需求,正在重塑整个农业价值链的筹资策略。那些能够展现稳定品质并整合精准施肥技术的製造商,正在高价值作物领域获得先发优势。同时,气候融资机制鼓励农民投资于能增加土壤碳含量的投入品,使腐植酸产品从可有可无的土壤改良剂转变为能产生收益的气候资产。

全球腐植酸市场趋势与洞察

土壤健康法规和碳信用激励措施

政府机构目前正将土壤有机碳量化为可交易指标,使腐植酸材料从成本中心转变为收入来源。美国农业部 (USDA) 于 2024 年推出了第 336 号实践准则,为透过施用堆肥和生物炭增加土壤有机质的生产者提供补偿。欧洲碳计画也类似地为土壤碳蕴藏量的可衡量成长提供积分,使腐植酸产品成为一种工具,既能为农民带来额外收入,又能满足监管要求。金融机构正将这些积分纳入绿色金融产品,扩大投入品采购的资金筹措管道。随着检验通讯协定日益严格,审核的可追溯性已成为腐植酸市场的差异化优势,使拥有标准化测试和数位化报告平台的公司更具优势。随着区域碳计画的成熟,预计北美和欧盟将在中期内加速采用,随后扩展到亚太地区。

再生农业的日益普及

再生农业系统强调微生物活性、永久性地表覆盖和多样化的作物轮作——所有这些都受益于腐殖质增强的阳离子交换能力及其对根际微生物群落的培育作用。在印度,制度上的推动力显而易见。该国的国家自然农业使命支持1万个生物投入资源中心,并计划在75万公顷土地上推广生物投入,以确保向当地生产者稳定供应腐植质。在北美,食品公司正在设定再生农业的面积目标,并将腐殖质投入纳入供应链合同,为符合要求的农民提供价格溢价。随着再生有机认证计画证明腐植酸对土壤有机质指标的贡献,长期需求正在形成。科技公司正在将土壤健康仪錶板整合到农场管理软体中,并将实验室有机碳数据转化为实用的应用指南,以鼓励重复购买。

产品诈欺和品质差异

比色测试和萃取通讯协定的差异会导致腐植酸含量测定结果出现高达40%的偏差,进而削弱消费者信心。当生产商无法比较不同品牌的宣称时,价格就成为唯一的差异化因素,降低了正规生产商的利润率。儘管AOAC(官方分析方法协会)的拉马尔法和HPTA(腐植酸产品贸易协会)的指南提供了可靠的标准,但由于检测成本高昂以及欧盟以外地区监管力度不足,这些标准的应用受到阻碍。在监管机构缺乏资源监督标籤的地区,伪装成腐植酸浓缩物的合成尿素混合物充斥通路,加剧了短期市场低迷。高端品牌已透过QR码追溯和第三方检测证书来应对,但这些安全措施的普及程度仍然参差不齐,限制了腐植酸市场近期的销售成长。

细分市场分析

液态浓缩液预计将以6.68%的复合年增长率(CAGR)实现最快增长,直至2031年,这主要得益于其与滴灌施肥和叶面喷布平台的整合。由于其在垂直农场和精密农业中的应用日益广泛,液态腐植酸市场预计将持续成长。颗粒状和粉末状腐植酸仍然是广谱作物种植的主要产品,但价格主导的市场定位限制了其利润成长。液态腐植酸的竞争优势在于其在高浓度(腐植酸含量高于12%)下的稳定性以及与富钙水质的兼容性。製造商正在投资螯合技术,以抑制沉淀物并实现1000公升吨桶装运输,从而显着降低每公顷的物流成本。

到2025年,粉状腐植酸仍将占据33.75%的市场份额,但随着液态产品在大规模园艺种植中越来越受欢迎,其市场份额将逐渐下降。对于缺乏滴灌系统、人工施肥仍是主流的新兴经济体合作社而言,粉状产品仍具有成本效益。美国混合肥料生产商正在尿素基NPK复合肥中添加微粉化腐植酸,以提高分销效率并维持此细分市场。然而,生命週期分析表明,液态肥料的单位重量功效优于粉状肥料,且碳足迹更低,这是范围3排放报告的关键指标。种植者正在透过引入太阳能干燥生产线来应对这一挑战,从而将碳中和的粉状肥料推向市场,以弥合永续性。

腐植酸市场报告按形态(粉末、颗粒、液体)、应用(有机肥料、动物饲料、其他应用)和地区(亚太地区、北美地区、欧洲地区、南美地区、中东和非洲地区)进行细分。市场预测以吨为单位。

区域分析

亚太地区腐植酸市场正以7.18%的复合年增长率快速成长,这主要得益于公共部门推行生物投入品製度化的计画。印度耗资1974.4亿卢比的「总理农业改革计画」(PM-PRANAM)根据减少的合成肥料补贴向各邦政府提供补偿,使农业部门能够透过合作社分发腐植酸颗粒。中国的「十四五」规划确保了土壤健康研发的资金投入,使地方政府能够补贴液态腐植酸浓缩液和滴灌设备。卡纳塔克邦的数据平台试点计画将土壤检测结果与QR码码腐植酸产品推荐相结合,以消除推广服务中的瓶颈。该地区众多的小规模农户正在采用越南首创的微型包装模式来使用腐植酸。这些结构性干预措施建立了稳定的需求基础,促进了大规模生产和社区配製厂的建设,从而降低了对进口的依赖。

欧洲占据腐植酸市场32.10%的份额,这主要得益于CE认证的统一以及到2024年超过1600万公顷的有机面积。零售商的自有品牌计划要求使用生物刺激剂以获得「地球评分」(Planet Score)货架标籤,这正在推动水果和蔬菜产业的需求。欧盟创新基金的碳农业试点计画将腐植酸产生的有机碳货币化,腐植酸供应商与遥感探测平台共同扮演检验。低碳食品品牌拓展了收入来源,在价格分布水果领域,叶面喷布的白利糖度和色泽指数,从而实现与品质挂钩的定价。然而,由于2024年起海运中断,欧洲经销商将面临进口成本上升的局面,这促使欧洲地区投资泥炭地开采和褐煤加工设施,以稳定供应。

北美市场需求稳定成长,但同时也日益分散。在美国,保护创新补助金(Conservation Innovation 津贴)正在支持各州进行试点项目,评估腐植酸配方在碳效率供应链中的应用。爱荷华州和伊利诺伊州的大型合作社正在将腐植酸计量模组整合到其变数施肥平台中,以创建服务包。加拿大的温室种植者对重金属含量低于100ppm的认证纯度液体产品需求旺盛,以符合加拿大食品检验局(CFIA)的标准。巴西的南美出口大豆综合体正在应用腐植酸强化技术,以支持其获得再生农业认证的出口合约。同时,中东和非洲的生产商正在采用腐植酸产品来缓解土壤盐碱化问题,提高作物的抗旱能力,尤其是在埃及一项面积达100万费丹(约666万公顷)的土地改良计划中。每个地区独特的农业挑战都创造了独特的价值提案,因此,在全球腐植酸市场中,行销必须采取适应性策略。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 土壤健康法规和排碳权计划

- 提高再生农业的采用率

- 欧盟对合成肥料使用的限制

- 垂直农业中的营养优化

- 腐植酸基生物刺激剂提高植物耐旱性

- 市场限制

- 产品诈欺和品质差异

- 缺乏机械化应用基础设施

- 竞争性微生物联合产品

- 价值链分析

- 波特五力模型

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争程度

- 价格概览

第五章 市场规模及成长预测(价值及数量)

- 按形式

- 粉末

- 颗粒状

- 液体

- 透过使用

- 有机肥料

- 动物饲料

- 其他用途

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 印尼

- 马来西亚

- 泰国

- 越南

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 土耳其

- 北欧国家

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 南非

- 奈及利亚

- 埃及

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Agbest Technology Co., Ltd.

- Arctech Inc.

- Cifo Srl

- Desarrollo Agricola y Minero, SA

- Grow More, Inc.

- HGS BioScience

- Humintech

- Jiloca Industrial SA

- Minerals Technologies Inc.

- Nutri-Tech Solutions Pty Ltd

- SAINT HUMIC ACID

- Sichuan Green Microbial Biotechnology Co., Ltd.

- The Andersons, Inc.

- WestMET LLC

- ZHENGZHOU SHENGDA KHUMIC AGRI TECH CO., LTD.

第七章 市场机会与未来展望

The Humic Acid market is expected to grow from 0.78 million tons in 2025 to 0.82 million tons in 2026 and is forecast to reach 1.09 million tons by 2031 at 5.72% CAGR over 2026-2031.

This trajectory reflects broadening acceptance of biologically derived soil-health solutions as governments tighten fertilizer regulations and carbon markets monetize soil organic carbon gains. Expansion of regenerative farming, coupled with demand from controlled-environment agriculture, reshapes procurement strategies across the agricultural value chain. Manufacturers that prove quality consistency and integrate with precision-application technology capture early-mover advantages in high-value crop segments. Meanwhile, climate-linked finance mechanisms fuel farmers' willingness to invest in inputs that boost soil carbon, elevating humic products from discretionary soil conditioners to revenue-generating climate assets.

Global Humic Acid Market Trends and Insights

Soil-health Regulations and Carbon-credit Incentives

Government agencies now quantify soil organic carbon as a tradable metric, shifting humic inputs from cost centers to revenue drivers. The USDA introduced Practice Code 336 in 2024, reimbursing growers who apply compost or biochar that lifts soil organic matter. European carbon programs similarly assign credits to measurable gains in soil carbon stocks, turning humic products into tools that meet compliance while earning farmers additional income streams. Financial institutions bundle these credits into green-finance products, broadening access to capital for input purchases. As verification protocols sharpen, audited traceability becomes a product differentiator in the Humic Acid market, favoring firms with standardized testing and digital reporting platforms. Medium-term uptake accelerates in North America and the EU before spreading to APAC as regional carbon schemes mature.

Rising Adoption in Regenerative Agriculture

Regenerative systems emphasize microbial activity, permanent ground cover, and diversified rotations-all practices that thrive when humic substances elevate cation-exchange capacity and foster root-zone microbiomes. India illustrates institutional momentum: its National Mission on Natural Farming backs 10,000 Bio-Input Resource Centers targeting 750,000 ha for bio-input adoption, ensuring stable offtake for local humic producers. In North America, food companies commit to regenerative acreage targets, embedding humic inputs in supply-chain contracts that offer price premiums to compliant growers. Long-term demand becomes structural as certification programs such as Regenerative Organic validate humic acid's contribution to soil-organic-matter metrics. Technology firms integrate soil-health dashboards into farm-management software, translating laboratory organic-carbon data into actionable dosing guides that drive repeat purchases.

Product Adulteration and Quality Variance

Colorimetric tests and divergent extraction protocols yield humic readings that can vary by 40%, undermining buyer confidence. When growers cannot compare label claims across brands, price becomes the sole differentiator, eroding margins for authentic producers. The AOAC (Association of Official Analytical Communities) Lamar method and HPTA (Humic Products Trade Association) guidelines offer robust baselines, yet adoption lags due to testing fees and a lack of enforcement outside the EU. Short-term market drag intensifies in regions where regulators lack resources to police labeling, allowing synthetic urea blends masquerading as humic concentrates to flood distribution channels. Premium brands respond with QR-code traceability and third-party lab certificates, but scale-up of these safeguards remains uneven, limiting near-term volume gains for the Humic Acid market.

Other drivers and restraints analyzed in the detailed report include:

- EU Limits on Synthetic Fertilizer Usage

- Vertical-farm Nutrient Optimization

- Limited Mechanized Application Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid concentrates logged the fastest trajectory at 6.68% CAGR through 2031, propelled by integration with fertigation and foliar-spray platforms. The Humic Acid market for liquids is projected to rise amid rising adoption by vertical farms and precision-ag operations. Granular and powdered forms remain staples for extensive cereal cropping, but their price-led positioning limits upside on margins. Competitive differentiation in the liquid tier hinges on stability at high concentrations (>= 12% humic fraction) and compatibility with calcium-rich waters. Manufacturers invest in chelation technology to suppress sedimentation, allowing 1,000-L tote shipments that slash per-hectare logistics costs.

Powdered formulations, while retaining 33.75% Humic Acid market share in 2025, face incremental erosion as liquids gain favor with large-scale horticulture. Powder remains cost-effective for cooperatives in emerging economies that lack drip-system infrastructure, where manual broadcasting prevails. Blending houses in the United States add micronized humic powder to urea-based NPK, achieving distribution efficiencies that keep this segment resilient. However, lifecycle analyses illustrate lower carbon footprints for liquids, as their efficacy per kilogram surpasses powders, a metric increasingly scrutinized under scope-3 emissions reporting. Producers counter by deploying solar-powered drying lines to market carbon-neutral powder, bridging the sustainability narrative gap.

The Humic Acid Market Report is Segmented by Form (Powdered, Granular, and Liquid), Application (Organic Fertilizer, Animal Feed, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific's Humic Acid market accelerates at 7.18% CAGR, fueled by public-sector programs institutionalizing bio-input adoption. India's Rs 19,744 crore PM-PRANAM scheme reimburses states based on reductions in synthetic-fertilizer subsidies, prompting agriculture departments to distribute humic granules via cooperatives. China's 14th Five-Year Plan earmarks soil-health R&D (research and development) funding, and provincial governments subsidize drip-fertigation kits bundled with liquid humic concentrates. Data-platform pilots in Karnataka integrate soil-test results with QR-coded humic product recommendations, lowering extension-service bottlenecks. The region's vast smallholder base adopts humic inputs through micro-pack sachets, a packaging model pioneered in Vietnam. These structural interventions establish reliable offtake, driving scale production and localized formulation plants that reduce import dependency.

Europe commands 32.10% Humic Acid market share owing to harmonized CE marking and entrenched organic-farming acreage exceeding 16 million ha in 2024. Retailer private-label programs stipulate biostimulant usage to earn "Planet Score" shelf labels, amplifying demand in the fruit and vegetable sectors. Carbon-farming pilots under the EU (European Union) Innovation Fund monetize humic-induced organic-carbon gains, positioning humic suppliers as verifiers alongside remote-sensing platforms. Low-carbon food branding expands revenue pools, and premium-priced fruit categories use humic foliar sprays to enhance Brix and color indices, forging quality-linked pricing. European distributors, however, face rising import costs after 2024 maritime freight disruptions, prompting investment in regional peat-bog extraction and lignite-processing facilities to secure supply resilience.

North American demand grows steadily but faces fragmentation. The United States deploys Conservation Innovation Grants to fund state-level pilots that evaluate humic blends in carbon-smart supply chains. Large cooperatives in Iowa and Illinois integrate humic dosing modules into in-house variable-rate platforms, creating bundled service packages. Canadian greenhouse operators drive concentrated demand for liquids with purity guarantees below 100 ppm heavy metals to comply with CFIA (Canadian Food Inspection Agency) standards. South America's export soybean complexes in Brazil incorporate humic enrichments to support regenerative-certified export contracts. Meanwhile, Middle East & African growers adopt humic products to mitigate saline-soil challenges, especially in Egypt's million-feddan reclamation project, reinforcing drought-resilience positioning. Each region's specific agronomic pressures carve distinct value propositions, requiring adaptive marketing in the global Humic Acid market.

- Agbest Technology Co., Ltd.

- Arctech Inc.

- Cifo Srl

- Desarrollo Agricola y Minero, S.A.

- Grow More, Inc.

- HGS BioScience

- Humintech

- Jiloca Industrial SA

- Minerals Technologies Inc.

- Nutri-Tech Solutions Pty Ltd

- SAINT HUMIC ACID

- Sichuan Green Microbial Biotechnology Co., Ltd.

- The Andersons, Inc.

- WestMET LLC

- ZHENGZHOU SHENGDA KHUMIC AGRI TECH CO., LTD.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Soil-health Regulations and Carbon-credit Incentives

- 4.2.2 Rising Adoption in Regenerative Agriculture

- 4.2.3 EU Limits on Synthetic Fertilizer Usage

- 4.2.4 Vertical-farm Nutrient Optimization

- 4.2.5 Humic-acid-based Biostimulants for Drought Resilience

- 4.3 Market Restraints

- 4.3.1 Product Adulteration and Quality Variance

- 4.3.2 Limited mechanized application infrastructure

- 4.3.3 Competing Microbial Consortia Products

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Price Overview

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Form

- 5.1.1 Powdered

- 5.1.2 Granular

- 5.1.3 Liquid

- 5.2 By Application

- 5.2.1 Organic Fertilizer

- 5.2.2 Animal Feed

- 5.2.3 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Indonesia

- 5.3.1.6 Malaysia

- 5.3.1.7 Thailand

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Turkey

- 5.3.3.8 Nordic Countries

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 South Africa

- 5.3.5.5 Nigeria

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Agbest Technology Co., Ltd.

- 6.4.2 Arctech Inc.

- 6.4.3 Cifo Srl

- 6.4.4 Desarrollo Agricola y Minero, S.A.

- 6.4.5 Grow More, Inc.

- 6.4.6 HGS BioScience

- 6.4.7 Humintech

- 6.4.8 Jiloca Industrial SA

- 6.4.9 Minerals Technologies Inc.

- 6.4.10 Nutri-Tech Solutions Pty Ltd

- 6.4.11 SAINT HUMIC ACID

- 6.4.12 Sichuan Green Microbial Biotechnology Co., Ltd.

- 6.4.13 The Andersons, Inc.

- 6.4.14 WestMET LLC

- 6.4.15 ZHENGZHOU SHENGDA KHUMIC AGRI TECH CO., LTD.

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment