|

市场调查报告书

商品编码

1910722

液态屋顶材料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Liquid Roofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

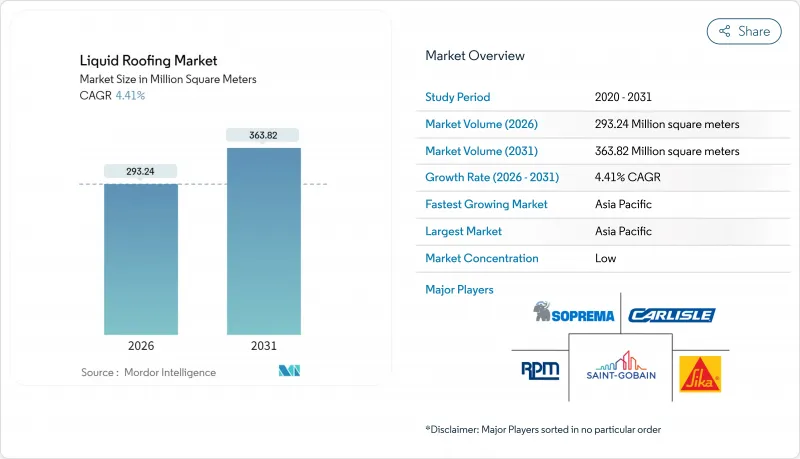

预计液体屋顶市场将从 2025 年的 2.8085 亿平方公尺成长到 2026 年的 2.9324 亿平方公尺,预计到 2031 年将达到 3.6382 亿平方公尺,2026 年至 2031 年的复合年增长率为 4.41%。

基础设施的快速现代化、频繁的风暴以及更严格的能源标准正在缩短屋顶更换週期,并推动人们对现场固化无缝涂料的偏好。承包商倾向于使用无需切割或焊接即可包裹穿孔的液态涂料系统,从而降低洩漏风险和现场废弃物。对挥发性有机化合物 (VOC) 更严格的监管限制进一步促进了水性化学品的普及,而政府对冷屋顶的激励措施则推动了其在炎热和温带地区的应用。同时,私募股权收购浪潮正在重塑分销网络,使得供应的稳定性与价格在竞标决策中同等重要。

全球液体屋顶材料市场趋势与洞察

气候变迁导致极端天气频繁,屋顶维修需求迅速成长

日益频繁的强风、冰雹和降水迫使建筑物业主在保固期到期前维修旧屋顶。液态涂料系统具有诸多优势,例如可在潮湿环境下固化,无需使用焊枪或溶剂焊接即可修復微裂缝。四级飓风过后,承包商订单数月之久,保险公司也优先考虑无缝涂层以减少未来的索赔。市政灾后重建资金正在加速公共屋顶维修项目,尤其是在飓风易发地区的学校和医疗机构。将液态涂料喷涂或滚涂到现有基材上,可以降低掩埋成本,并促进受损建筑物的早期再利用。

快速固化聚脲和混合体系,可减少工地停机时间

纯聚脲膜仅需30秒即可完全固化,实现当日即可通行,并可快速进行机械安装。丙烯酸-聚氨酯混合化学技术兼具低成本且加速干燥的优点,使安装人员能够在非尖峰时段延长每日生产时间。设施管理人员非常欣赏这种无需中断业务运营即可维修零售店屋顶的选择。早期采用者包括配送仓库(运作意味着直接产能损失)和需要持续环境控制的资料中心。改进的固化特性使设计人员更有信心在计划紧迫的关键专案中部署液态材料。

异氰酸酯和沥青价格波动加剧,挤压承包商利润空间

聚氨酯液体体係依赖异氰酸酯单体,例如MDI和HDI。由于欧洲一家工厂停产检修,这些单体的价格在2024年飙升了15-20%。随着订单转向现货定价,中小型屋顶承包商难以获得融资。这种价格波动加速了不含石油化学衍生的水性丙烯酸和硅酮体系的转变。订单量大的承包商透过与原料供应商建立一体化供应链来规避成本波动风险。大型原始设备製造商(OEM)可以轻易地将附加费转嫁给客户,从而扩大竞争差距,并进一步推动产业整合。

细分市场分析

到2025年,丙烯酸涂料的需求量将占51.47%,这主要得益于其符合VOC法规和冷屋顶标准。聚合物技术的不断改进,例如拉伸强度和防水性能的提升,预计将推动丙烯酸涂料市场在2031年前以4.74%的复合年增长率成长。丙烯酸液体屋顶材料的市场规模得益于其与多种基材的兼容性,使得安装人员无需拆除即可对老化的单层屋面膜进行重新涂装。聚氨酯基系统在化学和冷冻设施中仍然至关重要,因为这些场所需要卓越的耐磨性,但价格敏感度限制了其成长。硅基产品在年紫外线照射天数超过300天的沙漠气候地区正逐渐站稳脚步。

丙烯酸产品的普及也得益于其易于清理和低资本投入,这使得配备滚筒和无气喷涂设备的小规模承包商也能进入该领域。监管部门向水性技术的转变正在加速溶剂型沥青产品的市占率萎缩。环氧树脂和PMMA(聚甲基丙烯酸甲酯)等特殊解决方案被应用于重工业和历史建筑等领域,在这些领域,与石材和历史基材的黏合性比成本更为重要。总体而言,能够满足即将出台的微塑胶排放法规的化学产品预计将在未来获得更大的市场份额。

液体屋顶材料报告按类型(聚氨酯涂料、丙烯酸涂料、沥青基涂料、硅酮涂料等)、应用(穹顶屋顶、坡屋顶、平屋顶)、终端用户行业(住宅、商业、工业/公共、基础设施)和地区(亚太地区、北美、欧洲等)进行细分。市场预测以销售量(平方公尺)为单位。

区域分析

预计到2025年,亚太地区将占全球市场份额的41.18%,并在2031年之前以4.82%的复合年增长率成长。这主要得益于铁路、机场和资料中心等项目的建设,这些项目对现场固化防水卷材的需求较高。在中国,地方政府的维修补贴正在推动老旧住宅大楼的防水维修;印度则将屋顶冷却系统纳入智慧城市竞标。东南亚国协正透过公私合营,在学校和诊所推广液态防水卷材,以降低维修成本。在印尼和越南,拥有当地混合工厂的供应商能够减少跨境物流摩擦,并满足在地采购要求。

由于2005年至2010年间建造的大型零售商店和仓库的屋顶更换週期,北美市场仍然十分重要。 《基础设施投资与就业法案》为交通枢纽和水处理厂提供了资金,并促使附属建筑采用液态防水材料。科罗拉多州等州由于能源法规的修订而采用了加州的反射率标准,刺激了对丙烯酸白色屋顶的需求。德克萨斯州和奥克拉荷马州发生的严重冰雹灾害加速了使用抗衝击聚氨酯弹性体的屋顶更换。

在欧洲,逐步淘汰高挥发性有机化合物(VOC)含量的材料,强调环境合规性,并因此透过房产扣除额鼓励安装隔热冷屋顶。德国提案的绿色奖励策略优先考虑公共建筑的维修,这为在不损害历史石板屋顶外观的情况下涂覆硅酮面漆创造了机会。在英国,「未来住宅标准」鼓励建筑商使用反射性防水材料,以减少夏季过热。南欧的饭店度假村则指定使用液体防水材料,以避免在淡季进行防水施工期间转移住宿。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 气候变迁导致极端天气频繁,屋顶维修需求迅速成长

- 利用快速固化聚脲和混合系统减少工地停机时间

- 美国和欧盟对隔热和反射屋顶提供税收优惠

- 亚太主要城市的基建奖励策略

- 利用无人机进行喷涂施工,提高劳动生产力

- 市场限制

- 异氰酸酯和沥青价格的波动正在挤压承包商的利润空间。

- 区域性禁止使用高挥发性有机化合物(VOC)产品

- 新兴经济体熟练建筑工人短缺

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按类型

- 聚氨酯涂层

- 丙烯酸涂层

- 沥青基涂料

- 硅涂层

- 环氧树脂涂层

- 其他类型

- 透过使用

- 圆顶屋顶

- 山墙屋顶

- 平屋顶

- 按最终用户行业划分

- 住宅

- 商业的

- 行业/机构

- 基础设施

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 其他欧洲

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 卡达

- 埃及

- 阿拉伯聯合大公国

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- 3M

- Akzo Nobel NV

- Alumasc Building Products

- Carlisle Companies Incorporated

- Fosroc, Inc.

- Garland Company, Inc.

- Johns Manville(A Berkshire Hathaway Company)

- Kemper System Ltd

- Langley UK Ltd

- Mapei SpA

- PPG Industries, Inc.

- RPM INTERNATIONAL INC.

- Saint-Gobain

- SIG plc

- Sika AG

- SOPREMA Group

- Standard Industries Inc.

第七章 市场机会与未来展望

The Liquid Roofing Market is expected to grow from 280.85 million square meters in 2025 to 293.24 million square meters in 2026 and is forecast to reach 363.82 million square meters by 2031 at 4.41% CAGR over 2026-2031.

Rapid infrastructure modernization, more frequent storm events, and stricter energy codes shorten reroofing cycles and shift specification preferences toward seamless coatings that cure in-place. Contractors gravitate to liquid systems that wrap penetrations without cutting or welding, thereby lowering leak liability and jobsite debris. Regulatory moves that tighten volatile organic compound (VOC) thresholds further advantage waterborne chemistries, while government incentives for cool roofs reinforce adoption across hot and temperate zones. A concurrent wave of private-equity-backed rollups reshapes distribution reach, putting supply certainty on par with price in bid decisions.

Global Liquid Roofing Market Trends and Insights

Surging Reroofing Demand Amid Climate-Induced Extreme Weather

Escalating wind, hail, and precipitation intensities push building owners to upgrade aging roofs before warranty expiry. Liquid systems excel because they cure under damp conditions and bridge minor cracks without torching or solvent welding. Contractors report multi-month backlogs after Category 4 storms, and insurers prioritize seamless coatings that mitigate future claims through continuous membranes. Municipal recovery funds accelerate public reroofing programs, especially for schools and healthcare facilities located in hurricane corridors. The ability to spray or roll liquid products over existing substrates limits landfill fees and promotes faster re-occupancy of storm-damaged structures.

Fast-Curing Polyurea and Hybrid Systems Reducing Site Downtime

Pure polyurea membranes now reach full cure in as little as 30 seconds, enabling same-day foot traffic and rapid staging for mechanical trades. Hybrid acrylic-polyurethane chemistries combine lower cost with accelerated drying, allowing applicators to widen daily production windows during shoulder seasons. Facility managers value the option to restore roofs over occupied retail space without suspending operations. Early adopters include logistics warehouses where downtime translates directly into lost throughput, and data centers that require continuous environmental control. As cure profiles improve, specifiers gain confidence in deploying liquids on critical-path projects with tight schedules.

Volatile Isocyanate and Bitumen Prices Squeezing Contractor Margins

Polyurethane liquid systems rely on isocyanate monomers such as MDI and HDI whose prices spiked 15-20% in 2024 during maintenance shutdowns at European plants. Small and mid-sized roofing firms faced cash-flow stress as purchase orders shifted to spot pricing. The volatility accelerates substitution toward waterborne acrylics and silicones that sidestep petrochemical derivatives. Contractors with volume commitments hedge cost swings via integrated suppliers that backward-integrate into raw materials. Larger OEMs pass through surcharges more easily, widening the competitive gap and encouraging further consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Tax Incentives for Cool and Reflective Roofs in the United States and European Union

- Infrastructure Stimulus Packages Across APAC Megacities

- Regional Bans on High-VOC Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylic coatings accounted for 51.47% of 2025 demand, illustrating their successful alignment with VOC and cool-roof criteria. The segment is projected to post a 4.74% CAGR to 2031 as continuous polymer improvements boost tensile strength and ponding resistance. The liquid roofing market size for acrylics is supported by broad substrate compatibility, allowing contractors to recoat aged single-ply membranes rather than remove them. Polyurethane systems remain essential in chemical processing and cold-storage facilities that require superior abrasion resistance, though price sensitivity curbs expansion. Silicone offerings gain a foothold in desert climates where UV exposure exceeds 300 days annually.

Acrylic adoption also benefits from ease of cleanup and lower equipment investment, enabling small contractors to enter the arena with rollers and airless sprayers. Regulatory migration toward waterborne technology accelerates cannibalization of solvent-based bituminous products. Epoxy and PMMA niche solutions serve heavy-duty industrial or heritage-building sectors where adhesion to masonry or historic substrates outweighs cost. Overall, chemistries able to comply with the upcoming microplastic emission rules will capture future share.

The Liquid Roofing Report is Segmented by Type (Polyurethane Coatings, Acrylic Coatings, Bituminous Coatings, Silicone Coatings, and More), Application (Domed Roofs, Pitched Roof, and Flat Roofed), End-User Industry (Residential, Commercial, Industrial/Institutional, and Infrastructure), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Volume (Square Meters).

Geography Analysis

Asia-Pacific accounted for 41.18% of global coverage in 2025 and is set for a 4.82% CAGR to 2031, supported by rail, airport, and data-center pipelines that prefer onsite-cured membranes. China's Tier-3 city retrofit subsidies target waterproofing upgrades in aging housing blocks, while India integrates roof cooling into Smart City tenders. ASEAN economies push liquid specifications in public-private partnership schools and clinics to cut maintenance budgets. Suppliers with regional blending plants mitigate cross-border logistics frictions and satisfy local content rules in Indonesia and Vietnam.

North America remains a substantial market through replacement cycles in retail big-box and warehouse roofs built between 2005 and 2010. The Infrastructure Investment and Jobs Act channels funding into transit hubs and water treatment facilities that incorporate liquid roofing in ancillary buildings. Energy-code revisions in states such as Colorado adopt California's reflectance thresholds, stimulating acrylic white-roof demand. Severe hail outbreaks in Texas and Oklahoma accelerate reroofing with impact-resistant polyurethane elastomers.

Europe emphasizes environmental compliance by phasing out high-VOC materials and rewarding cool roofs via property tax credits. Germany's proposed green stimulus prioritizes public building retrofits, opening opportunities for silicone topcoats over historic slate roofs without altering appearance. The United Kingdom progresses toward the Future Homes Standard, nudging builders to select reflective membranes that cut summer overheating. Southern European hospitality resorts specify liquid waterproofing to avoid guest relocation during coating work performed in shoulder seasons..

- 3M

- Akzo Nobel N.V.

- Alumasc Building Products

- Carlisle Companies Incorporated

- Fosroc, Inc.

- Garland Company, Inc.

- Johns Manville (A Berkshire Hathaway Company)

- Kemper System Ltd

- Langley UK Ltd

- Mapei S.p.A.

- PPG Industries, Inc.

- RPM INTERNATIONAL INC.

- Saint-Gobain

- SIG plc

- Sika AG

- SOPREMA Group

- Standard Industries Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging reroofing demand amid climate-induced extreme weather

- 4.2.2 Fast-curing polyurea and hybrid systems reducing site downtime

- 4.2.3 Tax incentives for cool/reflective roofs in the US and EU

- 4.2.4 Infrastructure stimulus packages across APAC megacities

- 4.2.5 Drone-enabled spray-on application improving labor productivity

- 4.3 Market Restraints

- 4.3.1 Volatile isocyanate and bitumen prices squeezing contractor margins

- 4.3.2 Regional bans on high-VOC products

- 4.3.3 Skilled-applicator shortage in emerging economies

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Polyurethane Coatings

- 5.1.2 Acrylic Coatings

- 5.1.3 Bituminous Coatings

- 5.1.4 Silicone Coatings

- 5.1.5 Epoxy Coatings

- 5.1.6 Other Types

- 5.2 By Application

- 5.2.1 Domed Roofs

- 5.2.2 Pitched Roof

- 5.2.3 Flat Roofed

- 5.3 By End-user Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial/Institutional

- 5.3.4 Infrastructure

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordic Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Nigeria

- 5.4.5.4 Qatar

- 5.4.5.5 Egypt

- 5.4.5.6 United Arab Emirates

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Alumasc Building Products

- 6.4.4 Carlisle Companies Incorporated

- 6.4.5 Fosroc, Inc.

- 6.4.6 Garland Company, Inc.

- 6.4.7 Johns Manville (A Berkshire Hathaway Company)

- 6.4.8 Kemper System Ltd

- 6.4.9 Langley UK Ltd

- 6.4.10 Mapei S.p.A.

- 6.4.11 PPG Industries, Inc.

- 6.4.12 RPM INTERNATIONAL INC.

- 6.4.13 Saint-Gobain

- 6.4.14 SIG plc

- 6.4.15 Sika AG

- 6.4.16 SOPREMA Group

- 6.4.17 Standard Industries Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

液体屋顶市场-全球产业规模、份额、趋势、机会和预测,按产品类型、应用、最终用户、地区和竞争细分,2020-2030 年

液体屋顶市场-全球产业规模、份额、趋势、机会和预测,按产品类型、应用、最终用户、地区和竞争细分,2020-2030 年 全球液体屋顶市场报告(2025年)

全球液体屋顶市场报告(2025年) 全球液体屋顶市场规模研究与预测(按类型、应用和区域划分)2025-2035 年

全球液体屋顶市场规模研究与预测(按类型、应用和区域划分)2025-2035 年