|

市场调查报告书

商品编码

1910816

直线运动系统:市占率分析、产业趋势与统计、成长预测(2026-2031)Linear Motion System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

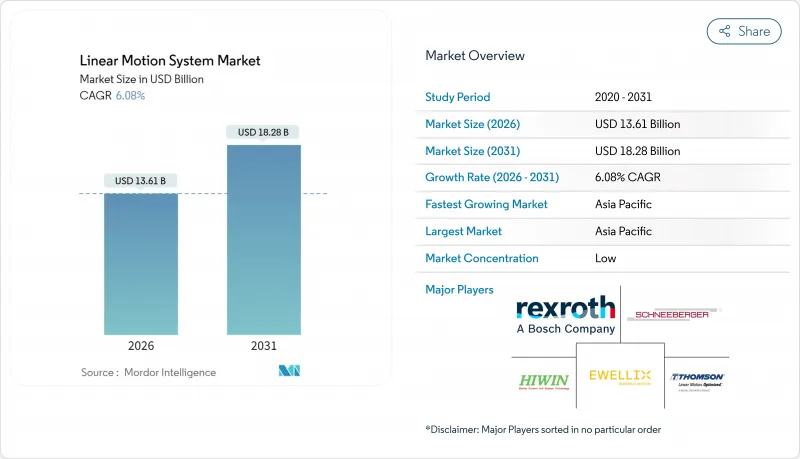

预计到 2026 年,直线运动系统市场规模将达到 136.1 亿美元,高于 2025 年的 128.3 亿美元。预计到 2031 年,该市场规模将达到 182.8 亿美元,2026 年至 2031 年的复合年增长率为 6.08%。

这项扩张反映了汽车、半导体和仓储自动化产业对高精度定位日益增长的需求,以及将运动组件整合到工业IoT网路中的数位化工厂投资的增加。多轴平台凭藉其在多个自由度上实现同步运动的能力,正在推动市场价值的成长,这种能力在复杂的机器人单元和高密度储存网格中尤其重要。同时,单轴单元製造商也收到了来自註重成本的用户的强劲订单,这些用户只需要单向线性运动,例如输送机改造和稀土元素。

全球直线运动系统市场趋势与洞察

加速工业4.0自动化

工厂正在将感测器和边缘运算模组整合到线性致动器中,以即时采集振动、负载和温度数据。如果演算法侦测到效能偏差,系统会降低轴的运行速度,从而安排维护并防止非计划性停机。这项功能使一家德国汽车製造商预计到 2024 年生产率将提高 15% 至 20%。此外,智慧线性控制设备现在可以直接连接到企业资源计划 (ERP) 软体,使生产计画负责人无需手动重新编程即可调整节拍时间。这项技术近期影响最大的可能是基于输送机的组装,因为这些装配线需要同步 X、Y 和 Z 轴运动以适应更多种类的车型。 ISO 9001审核也在推动这项技术的应用,因为运动动作控制器会为每个循环建立数位轨迹文件,从而简化合规性报告。

电子商务的成长推动了仓库自动化

预计到2024年,全球小包裹量将超过2,000亿件,仓库业者正向「立方体储存」转型,在这种模式下,週转箱以网格状排列,并由高速穿梭车在线性轨道上移动。这种高密度模式推动了对加速度可达5公尺/秒的致动器的需求,使履约中心能够实现当日出货。北美杂货店也开始引进穿梭式冷冻库,将工作人员与低至-25°C的低温环境隔离开来,从而提高工人安全并保障食品品质。为了符合美国职业安全与健康管理局(OSHA)关于人机协作的规定,供应商正在每个轴上整合双通道安全编码器和冗余煞车电路。随着小包裹形状变得越来越不规则,电商分类机依靠线性模组在毫秒内调整夹爪宽度,以维持每小时15,000件小包裹的吞吐量。

客製化系统的初始成本和投资回报週期

客製化线性运动改造的成本可能比现成配置高成本40% 至 60%,这需要工程师重新设计工装、升级电气控制柜并重建运动控製程式。对于利润微薄的中小型製造商而言,这笔额外的支出往往会将投资回收期延长至 18 至 24 个月。集成时间也会造成摩擦。生产线在试运行期间必须停产数週,这造成了机会成本的损失,而这些损失很少被计入初始资本需求中。产品配置高度多样化的二级供应商受到的影响最大,因为每种新的零件几何形状都需要客製化工装板和重新认证测试。因此,财务经理在核准采购前会要求提供量化的总拥有成本 (TCO) 模型,从而延长了决策週期。

细分市场分析

到2025年,多轴组装将占据线性运动系统市场65.31%的份额,主要得益于复杂拾取放置、焊接和视觉引导插入任务中对协调运动的需求。与多个单轴单元相比,整合式驱动器和现场汇流排布线可将安装时间缩短30%。由于运动指令并行执行而非顺序执行,使用者可获得更高的生产效率。此优势在电池模组组装上尤为显着,每个电芯的循环时间已缩短至10秒以内。此外,与臂展相当的关节机器人相比,多轴龙门架面积较小,这使得汽车製造商能够实现更密集的工位布局。

然而,单轴产品凭藉其满足特定需求并降低初始成本的优势,维持着7.05%的复合年增长率。例如,输送机整合商正越来越多地用电动滑轨取代机械挡块,以根据不同尺寸的纸箱调整行程长度。专业电子代工製造商则倾向于使用单轴导轨来製造表面黏着技术送料器,因为这些送料器仅需在单一平面内达到微米级的重复精度。这些致动器的模组化设计使工厂能够逐步扩展产能,从而节省资金用于其他升级。整体而言,线性运动系统市场在满足大批量多轴附加元件的同时,也兼顾了灵活的单轴附加组件,为终端用户提供了丰富的性价比选择。

到2025年,致动器和马达将占总收入的38.05%,因为所有装置仍然需要机械推力和扭力。然而,整合人工智慧韧体以实现自学习曲线优化的运动控制器将展现出最高的复合年增长率,达到8.05%。早期采用者报告称,由于自动调整的加加速度限制降低了峰值电力消耗,节能效果可达8-10%。新型控制器板整合了时间敏感网络,能够以亚微秒的精度将运动指令同步到机械臂。

儘管直线导轨仍然必不可少,但创新重点在于低维护涂层,即使在冲洗区域,也能保持润滑长达 20,000 公里。专为真空、低温和磁场环境设计的轴承服务于质子治疗和量子计算平台等细分市场。电缆链供应商现在提供的套件包含预先安装的乙太网路、电源和冷却管线,显着缩短了现场布线时间。随着工业 4.0 的成熟,价值正向软体转移,买家越来越多地评估控制器生态系统和诊断仪表板,而不仅仅是马达的最大推力。

区域分析

到2025年,亚太地区将占全球收入的39.75%,这主要得益于中国「中国製造2025」计划,该计划为自动化焊接和电子组装提供补贴。日本供应商保持着技术优势,尤其是在光刻和医疗诊断领域的亚微米级导轨方面,这使得区域客户能够在本地获得尖端的运动控制技术。韩国的智慧工厂计画正在推动对内建安全功能的控制器的需求,而印度的生产连结奖励计画计画则正在推动药品包装领域首次采用相关技术。

北美正经历稳定成长,回流政策推动了汽车、半导体和航太产品的国内製造。美国原始设备製造商(OEM)正在指定乙太网路整合安全功能以符合美国国家标准协会(ANSI)标准,从而推动了对高端控制设备的需求。加拿大林业和矿业加工企业正在部署50kN以上的重型轨道,以实现锯木厂和选矿厂的自动化。墨西哥的加工厂(maquiladoras)正在将成本效益高的劳动力与线性运动相结合,以在保持高产量的同时提高产品品质。

欧洲仍然是一个多元化且技术先进的消费市场。工具机丛集推广用于五轴加工的伺服驱动线性马达,而一家义大利包装设备製造商则青睐每分钟循环次数高达200次的紧凑型皮带传动装置。欧洲绿色交易鼓励转向节能型运动方式,包括可回收煞车能量的再生驱动装置。斯堪地那维亚电子工厂则体现了区域特色,例如,他们指定使用不銹钢导轨来防止低温焊接区域出现冷凝现象。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 加速采用工业4.0自动化技术

- 电子商务的扩张正在推动仓库转型为自动化。

- 半导体和电子设备对精度的需求日益增长

- 对诊断设备用紧凑型、免维护学习管理系统(LMS)的需求激增

- 需要高精度操作的永续柔性包装形式

- 医疗设备无尘室生产线回流激励措施

- 市场限制

- 客製化系统的初始成本高,且投资回报週期长。

- 熟练的LMS工程师短缺

- 稀土元素磁铁价格波动

- IEC-62443 智慧学习管理系统的网路安全合规成本

- 产业价值链分析

- 影响市场的宏观经济因素

- 技术展望

- 监管环境

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

第五章 市场规模与成长预测

- 按类型

- 单轴线性运动系统

- 多轴线性运动系统

- 按组件

- 致动器和电机

- 线性导轨

- 直线轴承

- 控制器

- 其他部件

- 按最终用户行业划分

- 车

- 电子和半导体

- 製造业

- 航太

- 卫生保健

- 食品/饮料

- 其他终端用户产业

- 透过使用

- 物料输送

- 工具机

- 机器人技术

- 包装

- 其他用途

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 奈及利亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Bosch Rexroth AG

- THK Co. Ltd

- Hiwin Corporation

- Schneeberger Group

- NSK Ltd

- Nippon Bearing Co. Ltd

- Thomson Industries Inc.(Regal Rexnord Corporation)

- The Timken Company

- Rockwell Automation Inc.

- Parker Hannifin Corporation

- HepcoMotion Inc.

- Ewellix AB

- Rollon SpA

- SKF AB

- Schneider Electric Motion USA Inc.

- PBC Linear Inc.

- Altra Industrial Motion Corp.

- Akribis Systems Pte Ltd

- Aerotech Inc.

- Lintech Corporation

第七章 市场机会与未来展望

linear motion system market size in 2026 is estimated at USD 13.61 billion, growing from 2025 value of USD 12.83 billion with 2031 projections showing USD 18.28 billion, growing at 6.08% CAGR over 2026-2031.

The expansion reflects rising demand for high-precision positioning in the automotive, semiconductor, and warehouse automation sectors, along with stronger digital-factory investments that integrate motion components into Industrial Internet of Things networks. Multi-axis platforms dominate value because they can deliver synchronized movement across several degrees of freedom, a capability prized in complex robotic cells and high-density storage grids. Meanwhile, manufacturers that build single-axis units are seeing robust orders from cost-sensitive users that only need linear travel in one direction, such as conveyor retrofits and pick-and-place modules. On the supply side, leading vendors are integrating predictive-maintenance analytics to address customer concerns over unforeseen downtime, and they are localizing component production in the Asia-Pacific region to contain logistics costs and hedge against fluctuations in rare-earth magnet prices.

Global Linear Motion System Market Trends and Insights

Accelerating Adoption of Industry 4.0 Automation

Factories are embedding sensors and edge-computing modules into linear actuators, enabling the devices to capture vibration, load, and thermal data in real-time. When algorithms detect a drift in performance, the system slows the axis, schedules service, and prevents unexpected downtime, a capability that German auto makers credited with 15-20% productivity gains in 2024. In addition, smart linear controllers now connect directly to enterprise resource planning software, allowing production planners to adjust takt times without manual reprogramming. The greatest near-term lift comes from conveyor-based assembly lines that need synchronized X-Y-Z travel to match a higher vehicle mix. ISO 9001 audits further encourage adoption because the motion controllers create digital trace files for every cycle, simplifying compliance reporting.

Expanding E-Commerce Boosting Automated Warehousing

Global parcel volumes surged past 200 billion units in 2024, pushing warehouse operators toward cube-based storage that packs totes in a grid and moves them via high-speed shuttles riding on linear rails.The densification model drives demand for actuators capable of 5 m/s acceleration profiles so that fulfillment centers can ship within the same day. North American grocers have also deployed shuttle-based freezers that keep operators out of -25 °C zones, improving worker safety while protecting food quality. To meet Occupational Safety and Health Administration rules on human-robot collaboration, suppliers integrate dual-channel safety encoders and redundant braking circuits into each axis. With parcel mix shifting toward irregular shapes, e-commerce sorters now rely on linear modules that adjust gripper width in milliseconds, sustaining 15,000 packages per hour throughput.

High Upfront Cost and ROI Cycle of Customised Systems

Bespoke linear motion retrofits can cost 40-60% more than off-the-shelf configurations because engineers must redesign tooling, upgrade electrical panels, and rewrite motion programs. That premium extends payback periods to the 18-24 month mark for small manufacturers operating on thin margins. Integration time adds friction because production lines often need to stop for several weeks during commissioning, resulting in lost-opportunity costs that are rarely factored into the initial capital request. Tier-2 suppliers with high product mix feel the pinch most acutely, as each new part geometry may require custom tooling plates and requalification trials. Financial controllers, therefore, demand quantified total-cost-of-ownership models before approving a purchase, which slows the decision cycle.

Other drivers and restraints analyzed in the detailed report include:

- Rising Semiconductor and Electronics Precision Needs

- Demand Surge for Miniature Maintenance-Free LMS in Diagnostic Devices

- Scarcity of Skilled LMS Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Multi-axis assemblies held 65.31% of linear motion system market share in 2025 as manufacturers required coordinated movement for complex pick-and-place, welding, and vision-guided insertion tasks. Their integrated drives and field-bus wiring cut installation time by 30% relative to linking several single-axis units. Users gain higher throughput because motion commands execute in parallel rather than sequentially, a benefit most obvious in battery-module assembly lines where cycle times fell below 10 seconds per cell. Auto makers also value the compact footprint that multi-axis gantries offer compared with articulated robots of similar reach, enabling denser workstation layouts.

Single-axis products nevertheless post a 7.05% CAGR because they satisfy focused needs at a lower upfront price. Conveyor integrators, for example, often replace mechanical stops with electric slides to vary stroke length as carton sizes change. Electronics contract manufacturers favor one-axis rails for surface-mount feeders that only demand micron-level repeatability along one plane. The modular nature of these actuators lets plants expand capacity gradually, preserving capital for other upgrades. In sum, the linear motion system market balances high-capacity multi-axis deployments with agile single-axis add-ons, giving end users a spectrum of cost-performance trade-offs.

Actuators and motors accounted for 38.05% of revenue in 2025 because every installation still needs mechanical thrust and torque. Yet the strongest 8.05% CAGR comes from motion controllers that now embed artificial-intelligence firmware for self-learning profile optimization. Early adopters report 8-10% energy savings when autotuned jerk limits reduce peak power draw. Newer controller boards integrate Time-Sensitive Networking, aligning motion commands with robot arms to sub-microsecond precision.

Linear guides remain indispensable, though innovation focuses on low-maintenance coatings that retain lubricant for 20,000 km travel even in wash-down zones. Bearings tailored for vacuum, cryogenic, or magnetic-field environments serve niche markets such as proton therapy and quantum-computing stages. Cable-chain suppliers now ship pre-harnessed kits that include Ethernet, power, and cooling lines, slashing field wiring hours. As Industry 4.0 matures, buyers increasingly judge controller ecosystems and diagnostic dashboards rather than the motor's peak thrust alone, shifting value toward software.

The Linear Motion System Market Report is Segmented by Type (Single-Axis Linear Motion System, and Multi-Axis Linear Motion System), Component (Actuators and Motors, Linear Guides, and More), End-User Industry (Automotive, Electronics and Semiconductor, Manufacturing, Aerospace, Healthcare, and More), Application (Material Handling, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific controlled 39.75% of global revenue in 2025, driven by China's Made in China 2025 program, which subsidizes automated welding and electronics assembly lines. Japanese suppliers retain technological leadership in sub-micron guides, particularly for lithography and medical diagnostics, enabling regional customers to access cutting-edge motion locally. South Korea's smart-factory initiative pushes demand for controllers with built-in cybersecurity, while India's Production-Linked Incentive scheme catalyzes first-time adoptions in pharmaceutical packaging.

North America enjoys steady growth because reshoring incentives encourage domestic production of vehicles, semiconductors, and aerospace products. U.S. original-equipment manufacturers specify integrated safety over Ethernet to comply with ANSI standards, creating pull-through for high-end controllers. Canadian lumber and mining processors purchase heavy-duty rails rated above 50 kN to automate sawmills and concentrators. Mexican maquiladoras combine cost-effective labor with linear motion to enhance quality while maintaining high throughput.

Europe remains a diverse yet technologically advanced consumer market. German machine-tool clusters in Baden-Wuerttemberg champion servo-driven linear motors for five-axis machining, whereas Italian packaging OEMs prefer compact belt drives tuned for 200 cycles per minute. The European Green Deal nudges users toward energy-efficient motion, including regenerative drives that harvest braking energy . Scandinavian electronics plants specify stainless guides to combat condensation in low-temperature soldering halls, rounding out regional nuance.

- Bosch Rexroth AG

- THK Co. Ltd

- Hiwin Corporation

- Schneeberger Group

- NSK Ltd

- Nippon Bearing Co. Ltd

- Thomson Industries Inc. (Regal Rexnord Corporation)

- The Timken Company

- Rockwell Automation Inc.

- Parker Hannifin Corporation

- HepcoMotion Inc.

- Ewellix AB

- Rollon S.p.A.

- SKF AB

- Schneider Electric Motion USA Inc.

- PBC Linear Inc.

- Altra Industrial Motion Corp.

- Akribis Systems Pte Ltd

- Aerotech Inc.

- Lintech Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating adoption of Industry 4.0 automation

- 4.2.2 Expanding e-commerce boosting automated warehousing

- 4.2.3 Rising semiconductor and electronics precision needs

- 4.2.4 Demand surge for miniature maintenance-free LMS in diagnostic devices

- 4.2.5 Sustainable flexible-package formats requiring high-precision motion

- 4.2.6 Reshoring incentives for medical-device clean-room lines

- 4.3 Market Restraints

- 4.3.1 High upfront cost and ROI cycle of customised systems

- 4.3.2 Scarcity of skilled LMS technicians

- 4.3.3 Rare-earth magnet price volatility

- 4.3.4 IEC-62443 cybersecurity compliance cost for smart LMS

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Technological Outlook

- 4.7 Regulatory Landscape

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Intensity of Competitive Rivalry

- 4.8.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Single-Axis Linear Motion System

- 5.1.2 Multi-Axis Linear Motion System

- 5.2 By Component

- 5.2.1 Actuators and Motors

- 5.2.2 Linear Guides

- 5.2.3 Linear Bearings

- 5.2.4 Controllers

- 5.2.5 Other Components

- 5.3 By End-User Industry

- 5.3.1 Automotive

- 5.3.2 Electronics and Semiconductor

- 5.3.3 Manufacturing

- 5.3.4 Aerospace

- 5.3.5 Healthcare

- 5.3.6 Food and Beverage

- 5.3.7 Other End-User Industries

- 5.4 By Application

- 5.4.1 Material Handling

- 5.4.2 Machine Tools

- 5.4.3 Robotics

- 5.4.4 Packaging

- 5.4.5 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products AND Services, and Recent Developments)

- 6.4.1 Bosch Rexroth AG

- 6.4.2 THK Co. Ltd

- 6.4.3 Hiwin Corporation

- 6.4.4 Schneeberger Group

- 6.4.5 NSK Ltd

- 6.4.6 Nippon Bearing Co. Ltd

- 6.4.7 Thomson Industries Inc. (Regal Rexnord Corporation)

- 6.4.8 The Timken Company

- 6.4.9 Rockwell Automation Inc.

- 6.4.10 Parker Hannifin Corporation

- 6.4.11 HepcoMotion Inc.

- 6.4.12 Ewellix AB

- 6.4.13 Rollon S.p.A.

- 6.4.14 SKF AB

- 6.4.15 Schneider Electric Motion USA Inc.

- 6.4.16 PBC Linear Inc.

- 6.4.17 Altra Industrial Motion Corp.

- 6.4.18 Akribis Systems Pte Ltd

- 6.4.19 Aerotech Inc.

- 6.4.20 Lintech Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment

直线运动系统市场:按类型、组件、驱动系统、安装方式、产业和分销管道划分-2026年至2032年全球市场预测医疗设备直线马达模组市场:按类型、阶段、销售管道和应用划分,全球预测(2026-2032年)

直线运动系统市场:按类型、组件、驱动系统、安装方式、产业和分销管道划分-2026年至2032年全球市场预测医疗设备直线马达模组市场:按类型、阶段、销售管道和应用划分,全球预测(2026-2032年) 直线运动系统市场报告:按类型、组件、最终用途行业和地区划分(2026-2034 年)XYZ龙门平台市场:按驱动类型、轴配置、行程范围、负载能力、类型、应用、最终用户划分,全球预测(2026-2032年)平面龙门架市场按驱动类型、轴配置、应用和最终用户产业划分,全球预测(2026-2032年)

直线运动系统市场报告:按类型、组件、最终用途行业和地区划分(2026-2034 年)XYZ龙门平台市场:按驱动类型、轴配置、行程范围、负载能力、类型、应用、最终用户划分,全球预测(2026-2032年)平面龙门架市场按驱动类型、轴配置、应用和最终用户产业划分,全球预测(2026-2032年) 全球直线运动产品市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)

全球直线运动产品市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034) 直线运动系统市场 - 全球产业规模、份额、趋势、机会及预测(按类型、最终用户产业、地区和竞争格局划分,2021-2031年)机器人直线运动轴市场(按致动器、轴类型、驱动类型和最终用户产业划分),全球预测,2026-2032年线性压电平台市场:依平台配置、驱动方式、行程范围、负载能力、终端用户产业及通路划分-2026-2032年全球预测

直线运动系统市场 - 全球产业规模、份额、趋势、机会及预测(按类型、最终用户产业、地区和竞争格局划分,2021-2031年)机器人直线运动轴市场(按致动器、轴类型、驱动类型和最终用户产业划分),全球预测,2026-2032年线性压电平台市场:依平台配置、驱动方式、行程范围、负载能力、终端用户产业及通路划分-2026-2032年全球预测 线性滑台市场规模、份额及成长分析(按产品、应用、产业和地区划分)-产业预测(2026-2033 年)

线性滑台市场规模、份额及成长分析(按产品、应用、产业和地区划分)-产业预测(2026-2033 年)