|

市场调查报告书

商品编码

1910822

过程仪器:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Process Instrumentation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

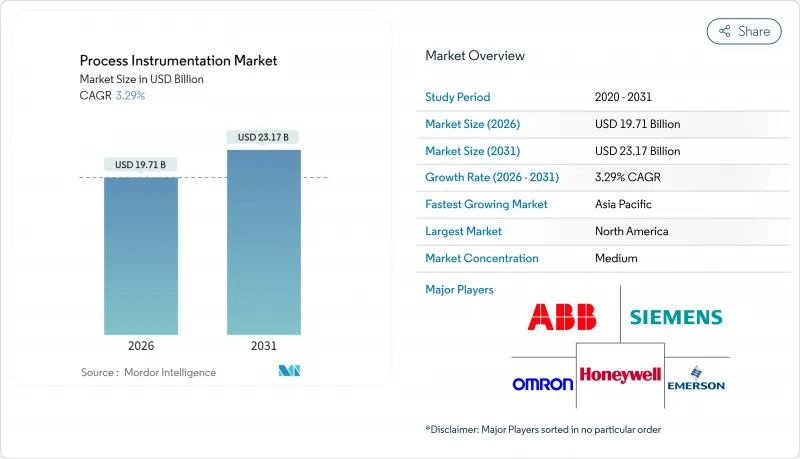

2025年过程仪器市场价值为190.8亿美元,预计到2031年将达到231.7亿美元,高于2026年的197.1亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 3.29%。

儘管数位化、脱碳要求和维修週期加剧了设备更新换代的需求,但这种温和的成长轨迹反映出基本客群日益成熟。供应商持续提供整合的硬体、软体和服务解决方案,以降低生命週期成本并支援排放监控合规性。老旧工厂的维修计划、单对乙太网路的普及以及劳动力短缺共同支撑了现有资产升级的稳定需求。同时,绿色氢能和水资源再利用计划正在创造新的需求,为製程仪器市场提供了强劲的前景。由于客户优先考虑测量精度、网路安全认证和服务应对力,价格竞争有限,这使得供应商能够透过数位化差异化来维持利润率。

全球过程仪器市场趋势与洞察

与脱碳相关的製程优化需求

欧盟碳边境调节机制(CBAM)等碳减量法规已将持续排放监测和能源效率测量列为核心营运指标。如今,工厂指定使用的仪器需结合高精度感测和安全的资料管道,以产生符合IEC 62443-2-1:2024网路安全计画标准的审核报告。化工、炼油和水泥产业的需求最为强劲,这些产业需要即时分析来降低燃料消费量并达到范围1和范围2的排放目标。为此,供应商正在提供整合自诊断、边缘检验和加密云端连接的智慧分析仪,从而将合规性转化为可衡量的收益,例如降低能源成本和减少碳排放税。这些法规正在扩展规范要求,使其不再局限于基本精度,而是涵盖资料完整性和可追溯性,从而推高了整个製程仪器市场的价格。

老旧工厂爆炸探测器的维修週期

上世纪八、九十年代建造的工厂面临校准成本不断上涨和计划外停机的双重困境。资产延寿计划透过对现有设备维修和感测器数位化,将传统变送器替换为能够提供多变量资料和预测性诊断的智慧型型号。恩德斯豪斯(Endress+Hauser)的紧凑型不銹钢仪器就是一个绝佳的例子,其现代化的外形设计能够承受CIP清洗,并最大限度地减少死角积垢,从而实现无需停机即可进行维护。工厂经理已证实,维护成本最多可降低20%,安全事故也显着减少,从而实现了快速的投资回报和更快的订购週期。由于超过60%的已安装设备仍在运作类比4-20mA迴路,改装专案仍是製程仪器市场未来几年持续成长的动力。

智慧发射器晶片供应瓶颈

工业微处理器仍受配额限制,预计到2025年,支援HART和乙太网路的变送器前置作业时间将延长至32週。供应商正在使用替代元件重新设计基板,但12至18个月的认证週期延缓了大量生产的恢復。亚太地区化工厂计划报告称,由于加急运输和临时设计变更,成本超支高达150万美元。对于需要专用类比数位转换器的多元分析仪而言,短缺情况尤其严重,导致出货延迟,并造成製程仪器市场短期放缓。

细分市场分析

到2025年,变送器将占製程仪器市场的37.62%,巩固其作为液位、压力和温度控制迴路核心的地位。诊断功能的不断改进、网路安全韧体的增强以及热插拔模组化设计,为现有设备基础设施提供了保障。供应商目前正在采用先进的漂移补偿演算法,并将校准週期从一年延长至三年,以确保运作运作。诸如Magnetrol的Jupiter JM4等现场可更换式头部设计,使得工厂能够在不破坏过程密封的情况下更换电子元件,从而降低维护和排气风险。预计在整个预测期内,变送器将保持稳定的收入来源,而日益严格的排放测量法规将推动需求成长。

分析仪器的复合年增长率高达3.62%,其测量工具包中新增了即时光谱、溶解氧感测和多分析物气体分析等功能。它们的崛起反映了应用场景从简单的状态监控转向主动流程最佳化。模组化平台允许在单一底盘内安装光学、电化学和质谱分析组件,从而缩小面积并最大限度地减少备件库存。分析仪器的日益普及为软体授权和云端网关的拓展创造了机会,提高了每个分析点的终身收益。这一趋势将支撑整个过程测量市场的持续成长。

到2025年,可程式逻辑控制器(PLC)将占据製程仪器市场34.02%的份额,这得益于其确定性的扫描时间、故障安全冗余以及灵活的维护技术。升级的重点在于安全引导载入、冗余Gigabit背板以及嵌入式OPC UA伺服器,这些都简化了上游资料共用。氢气电解撬装设备和水循环模组中控制器的日益普及,也增强了PLC出货量的稳定性。

随着越来越多的工厂寻求「单一管理平台」来统一生产计划、电子批次记录和即时品质分析,製造执行系统 (MES) 正以 3.76% 的复合年增长率 (CAGR) 高速成长。艾默生 DeltaV Edge 2.0 支援北向传输上下文相关的历史数据,从而简化了IT安全审核,同时避免控制器暴露于双向流量。 MES 与先进製程控制的融合降低了决策延迟,并将感测器智慧转化为节能并提高生产效率,从而保障了整个製仪器市场的投资回报。

区域分析

到2025年,北美将占据製程仪器市场29.12%的份额。该地区的环保署(EPA)法规要求对排放和水质进行持续监测,这推动了传统模拟迴路的加速更新换代。美国公共产业正在投资智慧变送器,以符合全氟和多氟烷基物质的严格监管标准。同时,加拿大油砂业者正在部署能够承受磨蚀性浆料的多变量流量计。跨境供应链和本地服务网路增强了售后市场的韧性,确保了供应商拥有充足的备件供应和稳定的业务收益。

亚太地区是成长最快的地区,预计到2031年将以3.81%的年复合成长率(CAGR)成长。这主要得益于快速的工业化、绿色氢电解的应用以及製造业向中国、印度和东南亚的回流。中国的化工中心正在利用高频雷达位准计来管理挥发性有机化合物,而印度的製药丛集正在实施基于光谱技术的製程分析技术(PAT)框架,以满足美国FDA的出口要求。日本和韩国政府对半导体工厂的支援措施正在推动对超仪器和亚ppm级气体分析仪的需求。对新资本设备投资的不断增长,使得亚太地区成为全球供应商在製程仪器市场拓展本地生产和支援中心的优先区域。

在脱碳立法和工业4.0普及的推动下,欧洲保持稳定成长。一家德国特种化学品联合企业正在升级其乙太网路APL现场网络,该网络整合了安全性和网路安全认证,符合ATEX和IEC 62443的要求。英国正在供水事业进行现代化改造,采用氨洩漏监测系统以满足更严格的排放法规;法国则投资建设一座氢电解示范工厂,该工厂需要冗余的A级变送器。在整个欧洲大陆,各国復苏基金正利用效率提升计画来保障基准需求,即使面临经济逆风。在中东和非洲地区,石化一体化计划、海水淡化厂和矿业扩张正在刺激仪器订单,并为全球和区域企业拓展其在製程仪器市场的影响力提供了邻近的成长领域。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场环境

- 市场概览

- 市场驱动因素

- 与脱碳相关的强制性流程优化

- 老旧工厂爆炸探测器的维修週期

- 乙太网路 - APL 单对乙太网路部署

- 捆绑式运维合约(作为仪器服务提供)

- 新冠疫情后的劳动力短缺推动了无人自动化发展。

- 绿色氢能大型企划推动了对测量设备的需求。

- 市场限制

- 智慧发射器晶片供应瓶颈

- 多重通讯协定遗留锁定成本

- 校准实验室容量不足

- 工业物联网连接的网路安全保险费

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 对宏观经济趋势的市场评估

第五章 市场规模与成长预测

- 透过装置

- 发送器

- 液位传送器

- 温度变送器

- 压力变送器

- 控制阀

- 分析设备

- 现场控制器(RTU/PLC)

- 过程分析仪器

- 气体分析仪

- 液体分析仪

- 其他设备

- 发送器

- 透过技术

- 分散式控制系统(DCS)

- 可程式逻辑控制器(PLC)

- 监控与数据采集(SCADA)

- 製造执行系统(MES)

- 其他控制技术

- 按最终用户行业划分

- 水和污水处理

- 石油和天然气开采

- 化学製造业

- 能源与公共产业

- 製药

- 金属和采矿

- 食品/饮料

- 纸浆和造纸

- 其他流程工业

- 透过测量参数

- 流动

- 压力

- 等级

- 温度

- 湿度

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲

- 亚太地区

- 中国

- 日本

- 印度

- 新加坡

- 韩国

- 澳洲

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Endress+Hauser AG

- Yokogawa Electric Corporation

- Emerson Electric Co.

- ABB Ltd.

- Honeywell International Inc.

- Siemens AG

- Schneider Electric SE

- Rockwell Automation Inc.

- Azbil Corporation

- KROHNE Messtechnik GmbH

- Pepperl+Fuchs SE

- Brooks Instrument LLC

- Mettler-Toledo International Inc.

- Badger Meter Inc.

- Spirax-Sarco Engineering plc

- AMETEK Inc.(Process Instruments)

- Omron Corporation

- Valmet Flow Control Oy

- HIMA Paul Hildebrandt GmbH

- Omega Engineering Inc.

- Samson AG

第七章 市场机会与未来展望

The process instrumentation market was valued at USD 19.08 billion in 2025 and estimated to grow from USD 19.71 billion in 2026 to reach USD 23.17 billion by 2031, at a CAGR of 3.29% during the forecast period (2026-2031).

The moderate growth trajectory reflects a maturing customer base, even as digitalization, decarbonization mandates, and retrofit cycles strengthen replacement demand. Suppliers continue to bundle hardware, software, and services, offering integrated solutions that reduce lifecycle costs and support compliance with emissions monitoring. Retrofit programs in aging plants, single-pair Ethernet rollouts, and labor shortages collectively sustain a steady flow of brownfield upgrades. At the same time, green hydrogen and water reuse projects create incremental greenfield opportunities, anchoring a resilient demand outlook for the process instrumentation market. Price competition remains limited because customers prioritize measurement accuracy, cybersecurity certification, and service responsiveness, allowing vendors to defend margins with digitally enabled differentiators.

Global Process Instrumentation Market Trends and Insights

Decarbonization-Linked Process-Optimization Mandates

Carbon-reduction legislation, such as the European Union's Carbon Border Adjustment Mechanism, elevates continuous emissions monitoring and energy-efficiency measurement to core operational metrics. Plants now specify instruments that combine high-accuracy sensing with secure data pipelines, enabling the generation of audit-ready reports under the IEC 62443-2-1:2024 cybersecurity program standard. Demand is strongest in the chemicals, refining, and cement industries, where real-time analytics help trim fuel consumption and align with Scope 1 and Scope 2 inventory targets. Suppliers respond with smart analyzers that integrate self-diagnostics, edge-based verification, and encrypted cloud connectors, turning compliance into measurable returns through reduced energy bills and lower carbon tax exposure. These mandates lift specification requirements beyond basic accuracy to encompass data integrity and traceability, reinforcing premium pricing across the process instrumentation market.

Explosive Sensor Retrofit Cycles in Ageing Plants

Facilities built during the 1980s and 1990s face rising calibration expenses and unplanned downtime. Asset-life extension projects now bundle sensor retrofits with digital upgrades, replacing legacy transmitters with smart models that deliver multivariable data and predictive diagnostics. Endress+Hauser's compact stainless-steel instrumentation demonstrates how modern form factors can withstand cleaning-in-place while minimizing dead-leg buildup, allowing for maintenance without process shutdowns. Plant managers document maintenance cost savings of up to 20% and safety-incident reductions, justifying quick payback periods that accelerate order cycles. Because more than 60% of installed base devices still run analog 4-20 mA loops, retrofit programs remain a multi-year growth engine for the process instrumentation market.

Chip-Supply Bottlenecks for Smart Transmitters

Industrial-grade microprocessors remain subject to allocation, extending lead-times for HART and Ethernet-enabled transmitters to as long as 32 weeks in 2025. While vendors re-engineer boards around second-source components, qualification cycles spanning 12-18 months defer volume recovery. Projects in Asia Pacific chemical complexes have documented cost overruns of up to USD 1.5 million due to expedited freight and last-minute redesigns. The shortage disproportionately affects multivariable analyzers that require specialized A/D converters, slowing shipments and tempering short-term momentum in the process instrumentation market

Other drivers and restraints analyzed in the detailed report include:

- Ethernet-APL Single-Pair Ethernet Roll-outs

- Bundled O&M Contracts (Instrument-as-a-Service)

- Multi-Protocol Legacy Lock-in Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transmitters held a 37.62% share of the process instrumentation market size in 2025, cementing their role as the backbone of level, pressure, and temperature control loops. Continuous improvements in diagnostics, cybersecurity firmware, and hot-swap modularity protect this installed base. Vendors now embed advanced drift-compensation algorithms that extend calibration cycles from yearly to once every three years, preserving uptime in 24/7 operations. Field-removable head designs, such as Magnetrol's Jupiter JM4, enable plants to replace electronics without breaching process seals, thereby reducing maintenance labor and venting risk.Over the forecast horizon, transmitters remain a stable revenue pillar, with incremental demand driven by tighter emissions-measurement rules.

Analytical instruments, growing at a 3.62% CAGR, add real-time spectroscopy, dissolved-oxygen sensing, and multi-parameter gas analysis to the instrumentation toolkit. Their rise reflects a shift from simple condition monitoring to active process optimization. Modular platforms enable a single chassis to accept optical, electrochemical, or mass spectrometric cartridges, thereby reducing the footprint and minimizing spare parts inventory. The expanding analytics footprint brings additional software licensing and cloud gateway opportunities, elevating lifetime revenue per point. This dynamic supports sustained growth across the process instrumentation market.

PLCs commanded 34.02% of the process instrumentation market in 2025, valued for deterministic scan times, fail-safe redundancy, and universal service know-how. Upgrades focus on secure bootloading, redundant gigabit backplanes, and embedded OPC UA servers that simplify upstream data sharing. Wider controller footprints emerge in hydrogen electrolyzer skids and water-recycling modules, reinforcing the stability of PLC volume.

Manufacturing execution systems are growing at the fastest rate of 3.76% CAGR as facilities seek a single pane of glass for production scheduling, electronic batch records, and real-time quality analytics. Emerson's DeltaV Edge 2.0 enables contextualized historian data to flow northbound without exposing controllers to bidirectional traffic, easing IT security audits. The convergence of MES with advanced process control narrows decision latency, translating sensor intelligence into energy savings and throughput gains that safeguard return on investment across the process instrumentation market.

The Process Instrumentation Market is Segmented by Instrument (Transmitters, Control Valves, Analytical Instruments, and More), Technology (DCS, PLC, SCADA, MES, Other Control Technologies), End-User Industry (Water and Wastewater Treatment, Oil and Gas Extraction, and More), Measurement Parameter (Flow, Pressure, Level, Temperature, Humidity), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held a 29.12% market share in the process instrumentation market in 2025. The region benefits from Environmental Protection Agency mandates that require continuous emissions and water quality monitoring, driving the accelerated replacement of legacy analog loops. U.S. utilities invest in smart transmitters to comply with stricter limits on per- and polyfluoroalkyl substances, while Canadian oil sands operators deploy multivariable flowmeters that withstand abrasive slurries. Cross-border supply chains and local service networks strengthen aftermarket resilience, ensuring high spare-part attachment rates and stable service revenue for vendors.

The Asia Pacific is the fastest-growing region, with a 3.81% CAGR through 2031, driven by rapid industrialization, green hydrogen electrolyzer deployments, and manufacturing reshoring in China, India, and Southeast Asia. Chinese chemical hubs utilize high-frequency radar level instruments for the control of volatile organic compounds, while Indian pharmaceutical clusters employ spectroscopy-enabled PAT frameworks to meet U.S. FDA export requirements. Government incentives for semiconductor fabs in Japan and South Korea spur demand for ultra-pure water instrumentation and sub-ppm gas analyzers. The breadth of new capacity investments positions Asia Pacific as a priority for global vendors expanding localized production and support centers in the process instrumentation market.

Europe maintains steady momentum, supported by decarbonization legislation and the adoption of Industry 4.0. German specialty-chemicals complexes upgrade to Ethernet-APL field networks, leveraging integrated safety and cybersecurity certification to satisfy both ATEX and IEC 62443 demands. The United Kingdom modernizes water utilities with ammonia-slip monitoring to hit tightening discharge consents, while France invests in hydrogen electrolyzer demonstration plants that require redundancy-class transmitters. Across the continent, national recovery funds channel capital toward efficiency upgrades, protecting baseline demand despite economic headwinds. Middle East and Africa provide growth adjacency as oil-to-chemicals integration projects, desalination plants, and mining expansions stimulate instrumentation orders, extending reach for global and regional players within the process instrumentation market.

- Endress+Hauser AG

- Yokogawa Electric Corporation

- Emerson Electric Co.

- ABB Ltd.

- Honeywell International Inc.

- Siemens AG

- Schneider Electric SE

- Rockwell Automation Inc.

- Azbil Corporation

- KROHNE Messtechnik GmbH

- Pepperl + Fuchs SE

- Brooks Instrument LLC

- Mettler-Toledo International Inc.

- Badger Meter Inc.

- Spirax-Sarco Engineering plc

- AMETEK Inc. (Process Instruments)

- Omron Corporation

- Valmet Flow Control Oy

- HIMA Paul Hildebrandt GmbH

- Omega Engineering Inc.

- Samson AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDCSAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Decarbonisation-linked process-optimisation mandates

- 4.2.2 Explosive sensor retrofit cycles in ageing plants

- 4.2.3 Ethernet-APL single-pair Ethernet roll-outs

- 4.2.4 Bundled OandM contracts (instrument-as-a-service)

- 4.2.5 Post-COVID labour shortfalls driving lights-out automation

- 4.2.6 Green-hydrogen mega-projects instrument demand

- 4.3 Market Restraints

- 4.3.1 Chip-supply bottlenecks for smart transmitters

- 4.3.2 Multi-protocol legacy lock-in costs

- 4.3.3 Shortage of calibration-lab capacity

- 4.3.4 Cyber-security insurance surcharges on IIoT links

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macro-economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Instrument

- 5.1.1 Transmitters

- 5.1.1.1 Level Transmitters

- 5.1.1.2 Temperature Transmitters

- 5.1.1.3 Pressure Transmitters

- 5.1.2 Control Valves

- 5.1.3 Analytical Instruments

- 5.1.4 Field Controllers (RTU/PLC)

- 5.1.5 Process Analyzer

- 5.1.5.1 Gas Analyzer

- 5.1.5.2 Liquid Analyzer

- 5.1.6 Other Instruments

- 5.1.1 Transmitters

- 5.2 By Technology

- 5.2.1 Distributed Control System (DCS)

- 5.2.2 Programmable Logic Controller (PLC)

- 5.2.3 Supervisory Control and Data Acquisition (SCADA)

- 5.2.4 Manufacturing Execution System (MES)

- 5.2.5 Other Control Technologies

- 5.3 By End-User Industry

- 5.3.1 Water and Wastewater Treatment

- 5.3.2 Oil and Gas Extraction

- 5.3.3 Chemical Manufacturing

- 5.3.4 Energy and Utilities

- 5.3.5 Pharmaceutical

- 5.3.6 Metals and Mining

- 5.3.7 Food and Beverage

- 5.3.8 Paper and Pulp

- 5.3.9 Other Process Industries

- 5.4 By Measurement Parameter

- 5.4.1 Flow

- 5.4.2 Pressure

- 5.4.3 Level

- 5.4.4 Temperature

- 5.4.5 Humidity

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Singapore

- 5.5.4.5 South korea

- 5.5.4.6 Australia

- 5.5.4.7 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Endress+Hauser AG

- 6.4.2 Yokogawa Electric Corporation

- 6.4.3 Emerson Electric Co.

- 6.4.4 ABB Ltd.

- 6.4.5 Honeywell International Inc.

- 6.4.6 Siemens AG

- 6.4.7 Schneider Electric SE

- 6.4.8 Rockwell Automation Inc.

- 6.4.9 Azbil Corporation

- 6.4.10 KROHNE Messtechnik GmbH

- 6.4.11 Pepperl + Fuchs SE

- 6.4.12 Brooks Instrument LLC

- 6.4.13 Mettler-Toledo International Inc.

- 6.4.14 Badger Meter Inc.

- 6.4.15 Spirax-Sarco Engineering plc

- 6.4.16 AMETEK Inc. (Process Instruments)

- 6.4.17 Omron Corporation

- 6.4.18 Valmet Flow Control Oy

- 6.4.19 HIMA Paul Hildebrandt GmbH

- 6.4.20 Omega Engineering Inc.

- 6.4.21 Samson AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

流程分析仪市场:全球市场按产品类型、安装方式、销售管道和最终用户分類的预测-2026-2032年过程液体分析仪市场:2026-2032年全球市场预测(依产品类型、技术、分析物质、应用、最终用途及销售管道)

流程分析仪市场:全球市场按产品类型、安装方式、销售管道和最终用户分類的预测-2026-2032年过程液体分析仪市场:2026-2032年全球市场预测(依产品类型、技术、分析物质、应用、最终用途及销售管道) 储罐计量感测器市场规模、份额和成长分析:按储罐感测器类型、技术、终端用户产业、测量类型和地区划分 - 2026-2033 年产业预测

储罐计量感测器市场规模、份额和成长分析:按储罐感测器类型、技术、终端用户产业、测量类型和地区划分 - 2026-2033 年产业预测 过程分析仪市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2026-2034)

过程分析仪市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2026-2034) 2026年全球模具液位计市场报告2026年全球製程分析仪市场报告2026年全球工业製程变数测量仪器市场报告

2026年全球模具液位计市场报告2026年全球製程分析仪市场报告2026年全球工业製程变数测量仪器市场报告 过程分析仪市场-全球产业规模、份额、趋势、机会与预测:液体分析仪、气体分析仪,按产业、地区和竞争格局划分,2021-2031年

过程分析仪市场-全球产业规模、份额、趋势、机会与预测:液体分析仪、气体分析仪,按产业、地区和竞争格局划分,2021-2031年 过程仪器市场机会、成长要素、产业趋势分析及预测(2026年至2035年)半导体液体感测器市场:按技术、安装类型、输出类型、应用、最终用户和销售管道,全球预测,2026-2032年

过程仪器市场机会、成长要素、产业趋势分析及预测(2026年至2035年)半导体液体感测器市场:按技术、安装类型、输出类型、应用、最终用户和销售管道,全球预测,2026-2032年