|

市场调查报告书

商品编码

1910899

豪华乙烯基瓷砖地板材料:市场份额分析、行业趋势和统计数据、成长预测(2026-2031)Luxury Vinyl Tile Floor Covering - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

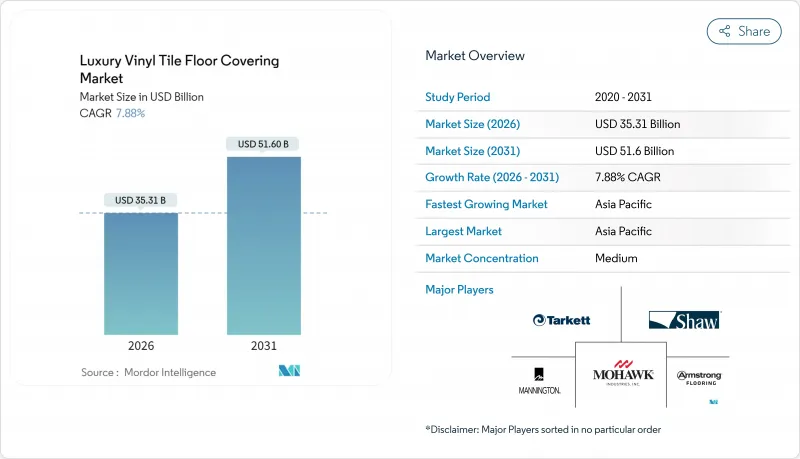

预计豪华乙烯基地板材料市场将从 2025 年的 327.3 亿美元增长到 2026 年的 353.1 亿美元,并预计在 2031 年达到 516 亿美元,2026 年至 2031 年的复合年增长率为 7.88%。

凭藉亲民的价格、逼真的外观、防水性和耐用性,该产品已成为翻新和新建计划中与实木和瓷砖直接竞争的领先产品。国内生产速度的提升、便捷的卡扣式安装以及全通路零售模式正在扩大其市场覆盖范围,而数位印刷技术的进步则进一步增强了产品的逼真度,甚至促使设计住宅在高端项目中指定使用乙烯基复合地板。医疗机构、饭店和混合计划都将该产品视为一种卫生、易于维护且兼顾安全性和品牌形像要求的地面材料。同时,与其他弹性地板材料解决方案相比,豪华乙烯基复合地板材料市场独有的优势——週末即可轻鬆安装、耐刮擦以及房间之间无缝衔接——也深受业主青睐。

全球豪华乙烯基瓷砖地板材料市场趋势与洞察

经济实惠的硬木替代品

豪华乙烯基瓷砖地板完美復刻了白橡木、胡桃木和再生谷仓木材的外观,是实木地板的经济实惠之选。这些地板避免了季节性翘曲和需要反覆打磨等问题。先进的同步暂存器印刷技术将木纹图案与触感纹理完美融合,打造出手工打造般的质感。设计师在审查设计方案时,常常会误以为它们是真正的实木地板。多用户住宅连锁店也开始贩售72吋(约183公分)超长和10吋(约25公分)超宽规格的地板,为开放成本绩效布局增添视觉层次感。随着利率上升给消费者融资带来压力,豪华乙烯基瓷砖地板材料市场销售量激增,因为这种经济实惠的地板材料已成为打造奢华美感的理想选择。

防水刚性芯材维修

石塑复合材料 (SPC) 和木塑复合材料 (WPC) 芯材具有防潮性能,因此可用于地下室、浴室和泳池房厨房等传统上铺设瓷砖的区域。 Cortec 的 18x18 吋 SPC 磁砖采用一体成型倒角接缝,安装时间缩短约三分之一。它无需湿式切割即可达到瓷砖的质感。易受洪水侵袭地区的保险公司建议在维修中承保硬芯地板材料,推动了市场需求。现场数据显示,与强化超耐磨地板因潮湿引起的返工率降低了 35%,增强了安装人员的信心。多代同堂住宅的兴起(地下室改造较为常见)进一步加速了硬芯产品在豪华乙烯基地板材料市场的应用。

PVC原物料价格波动

由于建筑开工量放缓,聚氯乙烯树脂价格在2023年8月飙升2美分/磅,挤压了未避险加工商的利润空间。小规模製造商缺乏储槽容量来储存价格较低的货物,因此更容易受到现货价格波动的影响。远期采购合约现在要求更高的违约金,加剧了营运资金紧张。公共部门竞标通常价格上涨条款有限,导致授标週期延长。在原料价格稳定之前,这些成本不确定性可能会限制豪华乙烯基地板材料市场的短期订单量。

细分市场分析

到2025年,硬质芯材产品将占豪华乙烯基地板材料市场总收入的63.92%,这印证了其显着的市场份额和不断增长的需求。预计13.71%的复合年增长率表明,市场对SPC和WPC材料的先进性能特性越来越依赖。 SPC卓越的抗静载重能力和WPC卓越的衝击绝缘等级(IIC)是推动其在各种终端用户应用中广泛应用的关键因素。这些材料在需要耐用性和降噪性能的环境中尤其重要,例如医疗机构、零售商店和住宅。它们能够承受重物(例如医院担架和食品托盘),同时降低噪音向楼下的传播,使其成为商业和住宅应用的理想选择。

儘管库存结构不断变化,但柔软性LVT地板在预算有限的公寓维修中仍然扮演着重要角色,因为不平整的基层和租金冻结限制了资本投资。供应商正在透过固化UV涂层和玻璃纤维网格来增强这些入门级产品,从而进一步防止透底。混合型地板设计将柔性面层与刚性基材结合,为承包商提供了高利润的中檔选择。设计部门正在利用数位印刷技术开发微型系列,例如水磨石碎片和石灰水洗橡木。季节性地更新产品系列,而无需改变模具,就能保持豪华乙烯基瓷砖地板材料市场的兴趣。

在豪华乙烯基地板材料市场中,胶合式安装占总收入的47.64%,巩固了其显着的市场份额。同时,锁扣式安装的成长速度超过了黏合式安装,复合年增长率达到10.62%。由于无异味安装带来的许多便利,DIY(自行安装)细分市场正蓬勃发展,安装后即可立即使用地板材料。这项特性契合了消费者对便利性和效率的需求,尤其是在住宅应用领域。此外,由于溶剂型黏合剂产生的有害气体降低了保险风险,小规模企业承包商也受益于更安全、更合规的工作环境。为了迎合不断变化的消费者偏好和现代设计美学,多个品牌推出了更宽的10英寸板。这些板材采用精密加工的型材设计,确保稳固的锁扣机制,进而提升耐用性和结构性能。

由于自黏地砖能够满足严格的捲材承重要求和防火安全标准中的边缘密封要求,因此在超级市场、机场和医疗机构走廊等高人流量的商业环境中,自黏地砖仍然占据着重要的地位。压敏黏着剂技术的创新进一步优化了黏合剂的安装,加快了固化速度,从而降低了人事费用,并缩小了与浮动系统的效率差距。自黏地砖在展位和季节性零售亭等特殊应用领域也越来越受欢迎,为豪华乙烯基地砖市场提供了更高的柔软性和适应性。此外,一些SPC地板製造商正在推出混合解决方案,在边缘接缝下方加入部分黏合条。这种方法结合了全浮动和半永久性系统的优点,既保证了安装时的稳定性和性能,也为最终用户提供了未来拆卸更换的功能。

区域分析

预计到2025年,亚太地区将占总营收的42.29%,并在2031年之前保持两位数成长,复合年增长率(CAGR)为12.49%。都市区进程每年新增数亿平方英尺的多用户住宅占地面积,而买家青睐硬质地板,因为它简洁现代,美观大方。製造地正从中国沿海地区转移到内陆省份以及邻国越南和柬埔寨,这不仅降低了美国接近性的到岸成本,也能满足当地市场需求。印度政府的住宅计画正在将硬芯板材作为标准配置,加速了豪华乙烯基地板材料市场的基准消费成长。

北美是第二大市场。位于乔治亚、田纳西州和安大略省的国内生产线提供按需配色服务,使当地住宅翻新者能够在一个月内找到与当地装饰颜色相匹配的瓷砖。美国联邦基础设施建设资金中包含的产品优先政策,迫使机构投资者选择美国製造的瓷砖,从而提高了工厂使用率。 SPC瓷砖的耐寒性受到加拿大度假屋业主的青睐,因为他们需要应对季节性的冻融循环,这确保了其额外的市场需求。

欧洲已成为永续性声明的试验场。 LEED、BREEAM 和法国 VOC 法规高度重视环境产品声明和消费后回收成分。提供第三方检验回收服务的品牌在公共竞标中获得高分。经济逆风令德国新建案的前景蒙上阴影。然而,节能维修的奖励使地板支出保持强劲。儘管目前南美和波湾合作理事会(GCC) 的市场规模较小,但 2026 年 FIFA 世界杯和 2030 年世博会的饭店建筑计划促使设计人员寻求快速安装和低维护的解决方案,预计该地区的豪华乙烯基地板材料市场将出现高于平均水平的增长。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 经济实惠的硬木替代品

- 刚性芯材防水改造工程快速成长

- 全通路与电子商务扩张

- 商业设施维修热潮(医疗设施、饭店/餐厅、办公大楼)

- 扩大国内LVT产能(关税反制措施和二氧化碳避险)

- 使用生物基/不含PVC的LVT

- 市场限制

- PVC原物料价格波动

- 亚洲供应贸易关税的不确定性

- SPC现场缺陷和保固索赔

- 脆弱的回收环境—ESG反弹

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依产品类型

- 灵活的

- 刚性核心

- 石塑复合材料(SPC)

- 木塑复合材料(WPC)

- 按安装类型

- 自黏乙烯基瓷砖

- 黏合式LVT

- 互锁式乙烯基瓷砖

- 其他的

- 最终用户

- 住宅

- 商业的

- 透过分销管道

- B2C/零售消费者

- B2B/承包商/建筑商

- 按地区

- 北美洲

- 加拿大

- 美国

- 墨西哥

- 南美洲

- 巴西

- 秘鲁

- 智利

- 阿根廷

- 南美洲其他地区

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 比荷卢经济联盟国家

- 北欧国家

- 其他欧洲地区

- 亚太地区

- 印度

- 中国

- 日本

- 澳洲

- 韩国

- 东南亚

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Armstrong Flooring

- Tarkett Group

- Mohawk Industries

- Shaw Industries

- Mannington Mills

- Gerflor

- Interface Inc.

- Forbo Flooring Systems

- Karndean Designflooring

- Amtico International

- Polyflor

- Beaulieu International Group

- CFL Flooring

- AHF Products

- Floor & Decor Holdings

- HMTX Industries

- Republic Floor

- MSI Surfaces

- Raskin Industries

- FloorFolio Industries

第七章 市场机会与未来展望

The luxury vinyl tile floor covering market is expected to grow from USD 32.73 billion in 2025 to USD 35.31 billion in 2026 and is forecast to reach USD 51.6 billion by 2031 at 7.88% CAGR over 2026-2031.

A combination of affordability, authentic aesthetics, and waterproof durability enables the category to compete directly with hardwood and ceramic across remodel and new-build projects. Accelerating domestic production, faster click-lock installation methods, and omnichannel retail models are widening access, while digital printing elevates realism to the point that even design professionals specify vinyl planks in premium developments. Healthcare networks, hotels, and hybrid offices now regard the product as a hygiene-forward, low-maintenance surface that fulfils both safety and branding requirements. Homeowners, conversely, prize the weekend install capability, scratch resistance, and seamless room-to-room coordination that the luxury vinyl tile floor covering market uniquely offers compared with other resilient solutions.

Global Luxury Vinyl Tile Floor Covering Market Trends and Insights

Cost-effective hardwood alternative

Luxury vinyl tile planks replicate the appearance of white oak, walnut, and reclaimed barn wood, offering a cost-efficient alternative to solid wood. These planks eliminate challenges such as seasonal cupping and the need for sanding cycles. Advanced emboss-in-register printing synchronizes grain patterns with tactile ridges, creating a hand-scraped feel that designers frequently mistake for hardwood during specification walk-throughs. Multifamily developers redirect savings toward upgraded lighting and smart-home packages, improving asset valuation without exceeding budget ceilings. Home-improvement chains now stock extra-long 72-inch planks and extra-wide 10-inch formats, extending sight lines in open-concept layouts. The luxury vinyl tile floor covering market gains incremental volume whenever interest rates squeeze consumer financing capacity, as value-engineered floors become the practical route to upscale aesthetics.

Rigid-core waterproof renovations

Stone Plastic Composite (SPC) and Wood Plastic Composite (WPC) cores resist subfloor moisture, allowing installation in basements, bathrooms, and pool-house kitchens that historically defaulted to ceramic tile. Coretec's 18 X 18 inch SPC tiles with integrated grout bevels shorten labour time by close to one-third and deliver ceramic realism without wet saws. Insurance carriers in flood-prone states recommend rigid-core floors in renovation payouts, reinforcing demand. Field data show a 35% reduction in callbacks tied to moisture-related failures versus laminate, raising installer confidence. Rising multigenerational housing, where basement conversions are common, further accelerates the penetration of rigid-core products in the luxury vinyl tile floor covering market.

PVC feedstock price volatility

Polyvinyl chloride resin prices spiked by two cents per pound in August 2023 despite sluggish construction starts, slicing margins at converters without hedges. Small manufacturers lack tank-farm capacity to stockpile low-priced cargoes, leaving them exposed to spot swings. Forward-buy contracts now require higher take-or-pay penalties, straining working capital. Public-sector bids often restrict price-escalation clauses, slowing award cycles. Resulting cost uncertainty tempers short-term order quantities in the luxury vinyl tile floor covering market until input prices stabilize.

Other drivers and restraints analyzed in the detailed report include:

- Omnichannel & e-commerce expansion

- Domestic LVT capacity build-outs (tariff & CO2 hedge)

- Trade-tariff uncertainty on Asian supply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, rigid core products accounted for 63.92% of the total revenue in the luxury vinyl tile floor covering market, underscoring their significant market share and growing demand. The projected CAGR of 13.71% highlights the increasing reliance on the advanced performance characteristics of SPC and WPC materials. SPC's exceptional static-load tolerance and WPC's superior Impact Insulation Class (IIC) ratings are critical factors driving their widespread adoption across various end-user applications. These materials are particularly valued in environments requiring durability and noise reduction, such as healthcare facilities, retail spaces, and multi-family residential buildings. Their ability to withstand heavy loads, such as hospital gurneys and grocery pallets, while simultaneously reducing noise transmission to lower floors, positions them as a preferred choice for both commercial and residential applications.

As inventory mix evolves, flexible LVT retains a role in budget apartment turns where sub-floors are uneven and rent moratoria squeeze CapEx. Suppliers enhance these entry products with hardened UV coatings and fiberglass meshes to mitigate telegraphing. Hybrid plank designs marry a pliable top film to a rigid backbone, offering installers a margin-friendly mid-tier option. Design departments exploit digital printing to issue micro-collections, such as terrazzo chip or lime-washed oak, that refresh assortments seasonally without tooling changes, sustaining engagement for the luxury vinyl tile floor covering market.

Glue-down accounted for 47.64% of the total revenue in the luxury vinyl tile floor covering market, underscoring its significant market share. Interlocking profiles overtook glue-down in share growth, recording a 10.62% CAGR. The do-it-yourself (DIY) segment highlights the operational advantages of odor-free installations, which allow immediate usability of newly installed flooring. This feature aligns with consumer demand for convenience and time efficiency, particularly in residential applications. Small-business contractors also benefit from reduced insurance risks associated with solvent-based adhesive fumes, which contribute to safer and more compliant work environments. To address shifting consumer preferences and modern design aesthetics, several brands have introduced extra-wide 10-inch planks. These planks are designed with precision-milled profiles to ensure strong locking mechanisms, enhancing durability and structural performance.

Glue-down tiles maintain a significant presence in high-traffic commercial environments, such as supermarkets, airports, and medical corridors, due to their ability to meet stringent rolling-load requirements and fire-code edge-sealing standards. Innovations in pressure-sensitive adhesive technology have further optimized glue-down installations by accelerating set times, thereby reducing labour costs and narrowing the efficiency gap with floating systems. Self-adhesive tiles have also gained popularity in specialized applications, including trade-show booths and seasonal retail kiosks, offering enhanced flexibility and adaptability within the luxury vinyl tile market. Additionally, some manufacturers of SPC flooring have implemented hybrid solutions by incorporating partial adhesive strips beneath end joints. This approach combines the benefits of fully floating and semi-permanent systems, providing end-users with the option for future lift-and-replace functionality while maintaining installation stability and performance.

The Luxury Vinyl Tile Floor Covering Market is Segmented by Product Type (Rigid Core, Flexible), End User (Residential, Commercial), Installation Type (Self-Adhesive Vinyl Tiles, Glue-Down LVT, Interlocking Vinyl Tiles, Others), Distribution Channel (B2C / Retail Consumers, B2B / Contractors / Builders) and Geography (North America, South America and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 42.29% of 2025 revenue and is forecast to maintain double-digit expansion at 12.49% CAGR through 2031. Urban migration adds hundreds of millions of square feet of multifamily floor area each year, and buyers prefer hard surfaces for perceived cleanliness and modern aesthetic. Manufacturing shifts from coastal China to inland provinces and neighbouring Vietnam and Cambodia, reducing landed cost in the United States while keeping proximity to local demand intact. Government housing schemes in India now include rigid-core planks in their standard specification, accelerating baseline consumption in the luxury vinyl tile floor covering market.

North America ranks second in value. Domestic lines in Georgia, Tennessee, and Ontario supply colour-on-demand programs, enabling regional house flippers to match local trim colours within a month. Buy-American restrictions embedded in federal infrastructure funding steer institutional buyers toward U.S.-made tiles, lifting plant utilization rates. The cold-weather durability of SPC appeals to Canadian cottage owners who face seasonal freeze-thaw cycles, ensuring additional volume.

Europe is the proving ground for sustainability claims. LEED, BREEAM, and French VOC regulations reward Environmental Product Declarations and post-consumer content. Brands offering third party-verified take-back receive preferential scoring on public tenders. Economic headwinds in Germany dim new-build forecasts, but renovation incentives for energy-efficient makeovers keep flooring spend resilient. South America and the Gulf Cooperation Council are smaller today, yet hotel pipelines for the 2026 FIFA World Cup and Expo 2030 push specification teams toward quick-install, low-maintenance solutions, positioning the luxury vinyl tile floor covering market for above-average regional growth.

- Armstrong Flooring

- Tarkett Group

- Mohawk Industries

- Shaw Industries

- Mannington Mills

- Gerflor

- Interface Inc.

- Forbo Flooring Systems

- Karndean Designflooring

- Amtico International

- Polyflor

- Beaulieu International Group

- CFL Flooring

- AHF Products

- Floor & Decor Holdings

- HMTX Industries

- Republic Floor

- MSI Surfaces

- Raskin Industries

- FloorFolio Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost-effective hardwood alternative

- 4.2.2 Surge in rigid-core waterproof renovations

- 4.2.3 Omnichannel & e-commerce expansion

- 4.2.4 Commercial retrofit boom (healthcare, hospitality, offices)

- 4.2.5 Domestic LVT capacity build-outs (tariff & CO2 hedge)

- 4.2.6 Bio-based / PVC-free LVT adoption

- 4.3 Market Restraints

- 4.3.1 PVC feed-stock price volatility

- 4.3.2 Trade-tariff uncertainty on Asian supply

- 4.3.3 SPC field-failure & warranty claims

- 4.3.4 Weak recycling ecosystem - ESG backlash

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Flexible

- 5.1.2 Rigid Core

- 5.1.2.1 Stone Plastic Composite (SPC)

- 5.1.2.2 Wood Plastic Composite (WPC)

- 5.2 By Installation Type

- 5.2.1 Self-Adhesive Vinyl Tiles

- 5.2.2 Glue-Down LVT

- 5.2.3 Interlocking Vinyl Tiles

- 5.2.4 Others

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.4 By Distribution Channel

- 5.4.1 B2C / Retail Consumers

- 5.4.2 B2B / Contractors / Builders

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 Canada

- 5.5.1.2 United States

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX

- 5.5.3.7 NORDICS

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South East Asia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Armstrong Flooring

- 6.4.2 Tarkett Group

- 6.4.3 Mohawk Industries

- 6.4.4 Shaw Industries

- 6.4.5 Mannington Mills

- 6.4.6 Gerflor

- 6.4.7 Interface Inc.

- 6.4.8 Forbo Flooring Systems

- 6.4.9 Karndean Designflooring

- 6.4.10 Amtico International

- 6.4.11 Polyflor

- 6.4.12 Beaulieu International Group

- 6.4.13 CFL Flooring

- 6.4.14 AHF Products

- 6.4.15 Floor & Decor Holdings

- 6.4.16 HMTX Industries

- 6.4.17 Republic Floor

- 6.4.18 MSI Surfaces

- 6.4.19 Raskin Industries

- 6.4.20 FloorFolio Industries

7 Market Opportunities & Future Outlook

- 7.1 Launch click-lock PVC-free hybrid LVT targeting LEED & EU Green Deal projects

- 7.2 AI-driven room-visualizer platforms to raise online conversion for mid-tier retailers