|

市场调查报告书

商品编码

1910913

IT外包(ITO)-市场占有率分析、产业趋势与统计、成长预测(2026-2031年)IT Outsourcing (ITO) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

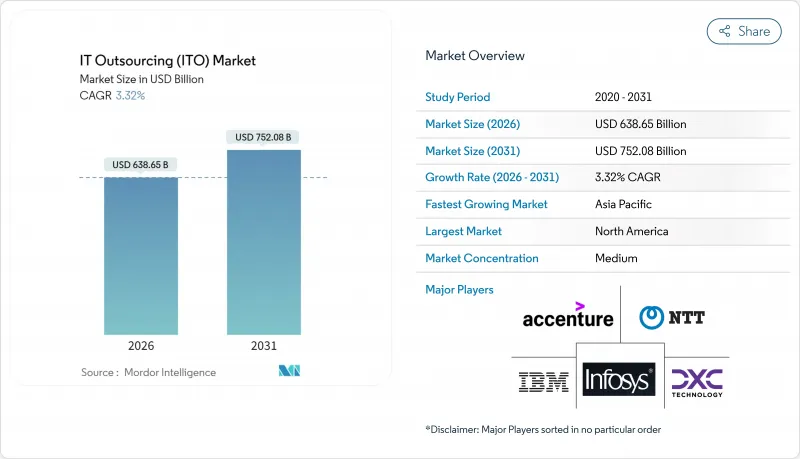

2025 年 IT 外包 (ITO) 市值为 6,181.3 亿美元,预计到 2031 年将达到 7,520.8 亿美元,而 2026 年为 6,386.5 亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 3.32%。

这项预测通道反映了产业的成熟度,生成式人工智慧驱动的自动化正在改变劳动密集的交付模式,推动新型人工智慧服务的发展,同时减少对传统员工依赖型合约。日益加剧的地缘政治紧张局势促使企业为应对主权云指令和资料居住法规而实现采购多元化,许多买家倾向于采用离岸、近岸和在岸中心相结合的模式来降低风险。全球网路安全人才缺口高达480万人,这催生了託管侦测和回应服务的超额需求。产业整合正在加速。近期的一些案例,例如Cognizant以13亿美元收购Belcan以及Capgemini SA收购WNS的谈判,显示成熟企业正在吸收细分领域的专家,以增强其人工智慧能力并拓展服务组合。随着企业在管理混合云和多重云端环境方面面临挑战,云端管理服务的重要性日益凸显,而基于绩效的定价模式因其与可衡量的业务成果挂钩而越来越受欢迎。

全球IT外包(ITO)市场趋势与洞察

云端原生应用程式现代化改造的需求

企业正在将单体系统重构为微服务、容器和无伺服器函数,这给平台工程、Kubernetes编配和事件驱动设计带来了大规模的挑战。尤其是在金融服务和医疗保健等监管严格、合规性日益复杂的行业,服务提供者越来越多地提供基本契约,以保证性能、成本目标和可扩展性,而不是按工作量收费。技术转型也需要管理文化变革,通常需要外部合作伙伴来指导敏捷流程,因为内部团队很难轻易采用这些流程。

利用生成式人工智慧实现服务台自动化

生成式人工智慧透过智慧路由和自癒脚本,将一级工单量减少了高达 40%,平均解决时间缩短了 25%。虚拟助理现在能够理解跨多个系统的上下文,提供个人化回应,并在使用者註意到故障之前预测事件。然而,对于需要上下文判断的复杂安全问题,服务提供者必须将自动化与人工监控结合。

智慧财产权窃盗和勒索软体保险成本飙升

网路安全事件的增加迫使企业增加加密、存取监控和隔离开发环境等措施,这推高了计划成本,同时保险费上涨,承保范围缩小(安永)。采购者现在要求供应商持有更高的保险限额并定期进行穿透测试,这些限制使规模较小的供应商处于不利地位,并加速了行业整合。

细分市场分析

到2025年,基础设施外包将占IT外包(ITO)市场的45.05%,这主要得益于企业对需要持续监控和合规性的弹性资料中心营运的日益依赖。然而,随着企业面临涵盖AWS、Azure、Google Cloud和私有环境的混合环境的复杂性,云端管理服务将以3.44%的复合年增长率推动市场成长。目前,服务提供者正在将统一的管理平台捆绑在一起,这些平台能够根据成本、延迟和合规性要求对工作负载进行排序,从而模糊了传统基础设施管理和新兴的多重云端编配之间的界限。

低程式码和人工智慧辅助开发正在重塑应用开发和维护的需求,迫使供应商透过领域知识和整合专长来脱颖而出。边缘运算和人工智慧模式生命週期服务属于「其他」类别,代表着一个新兴但利润丰厚的市场机会。随着云端运算的普及,现有企业正转向自动化站点可靠性工程服务,透过人工智慧驱动的自癒机制来确保服务等级目标的达成,从而保护基础设施收入免受价格压缩的影响。

即使到了2025年,大型企业仍将占据67.25%的支出份额,这主要是因为维护复杂的传统环境需要深厚的架构专业知识。然而,中小企业(SME)的成长速度更快,复合年增长率(CAGR)达到3.96%。中小企业更倾向于绩效付费的合约模式,因为它将IT支出与具体的业务成果而非员工人数挂钩。云端原生供应商透过自助服务入口网站和自动化配置降低了进入门槛,将以往只有财富500强企业才能享有的按需人工智慧、分析和网路安全安全功能带给了中小企业。这种技术的普及化正在扩大IT外包市场的潜在规模,同时也迫使现有供应商创建模组化、标准化的服务,以便在不损害利润率的情况下实现经济规模化。

IT外包(ITO)市场按服务类型(基础设施外包、应用开发与维护及其他)、组织规模(中小企业和大型企业)、外包地点(境内、近岸及其他)、最终用户行业(银行、金融服务和保险、医疗保健和生命科学及其他)以及地区进行细分。市场预测以美元计价。

区域分析

北美24.12%的市占率巩固了其作为人工智慧和云端现代化倡议领先采用地区的地位,这些专案需要经验丰富的服务供应商。美国公司正在重新谈判传统合同,转向基于结果的条款,明确规定每次交易的成本和收入提升指标,从而降低劳动力套利风险。加拿大公司优先考虑零信任安全框架和主权云端实例,以遵守严格的隐私法律。墨西哥的近岸外包中心正在扩展敏捷团队和DevOps能力,以减少计划延误并增强与美国客户的文化契合度。

亚太地区3.66%的复合年增长率主要得益于印度的持续领先地位和东协日益增长的贡献。越南、印尼和马来西亚正透过政府奖励和学术合作加强其工程人才储备,试图将自身打造成为应用开发测试的二级中心。日本和韩国正将下一代网路营运和边缘云端编配外包,以弥补国内人才短缺。澳洲对託管网路安全和云端金融营运服务的需求不断增长。

在欧洲,我们看到严格的资料保护条例和对数位主权的高度重视。本地服务供应商正与超大规模资料中心业者商合作,开发区域专属的主权云端区域。德国、法国和荷兰在推动特定产业的云端迁移的同时,也维持国内资料处理能力。即使在脱欧之后,英国仍然是金融服务外包的中心,并强调弹性测试和营运风险管理。东欧的软体工程丛集提供高阶研发外包服务,并透过与西欧客户达成多元化协议,规避地缘政治的不确定性。

其他福利

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 云端原生应用程式现代化改造的需求

- 利用生成式人工智慧实现服务台自动化

- 将人工智慧和自动化整合到 DevOps 外包中

- 网路安全和可观测性领域的人才短缺

- 主权云端的兴起与资料居住义务

- 供应商转向基于绩效的定价模式

- 市场限制

- 智慧财产权侵权和勒索软体保险成本飙升

- 地缘政治紧张局势加剧扰乱了离岸交付中心

- 超大规模资料中心业者出口费用波动

- 利用基于人工智慧的程式码产生技术减少外包范围

- 供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 激烈的竞争

- 评估市场中的宏观经济因素

第五章 市场规模与成长预测

- 按服务类型

- 基础建设外包

- 应用开发和维护

- 云端管理服务

- 其他的

- 按组织规模

- 小型企业

- 大公司

- 依采购地点

- 陆上

- 近岸

- 离岸

- 按最终用户行业划分

- BFSI

- 医疗保健和生命科学

- 媒体传播

- 零售与电子商务

- 製造业

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 其他欧洲

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 澳洲

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- IBM Corporation

- Tata Consultancy Services

- Infosys Ltd

- Cognizant Technology Solutions

- Wipro Ltd

- HCLTech

- Capgemini SE

- DXC Technology

- NTT Data Corporation

- Atos SE

- CGI Inc.

- Tech Mahindra

- EPAM Systems

- LTI Mindtree

- Globant

- Endava plc

- Softtek

- Andela Inc.

- Persistent Systems

- Accenture plc

第七章 市场机会与未来展望

The IT outsourcing market was valued at USD 618.13 billion in 2025 and estimated to grow from USD 638.65 billion in 2026 to reach USD 752.08 billion by 2031, at a CAGR of 3.32% during the forecast period (2026-2031).

The measured trajectory mirrors the sector's maturation as generative AI automation reshapes labor-intensive delivery models, spurring new AI-enabled services while compressing traditional headcount-driven contracts. Geopolitical tensions are prompting enterprises to diversify sourcing footprints in response to sovereign-cloud mandates and data-residency rules, leading many buyers to blend offshore, nearshore, and onshore centers for risk mitigation. The cybersecurity talent shortfall of 4.8 million positions worldwide is creating premium demand for managed detection and response offerings. Consolidation is accelerating: recent deals such as Cognizant's USD 1.3 billion Belcan purchase and Capgemini's negotiations to acquire WNS illustrate how scale players absorb niche specialists to deepen AI capabilities and broaden portfolios. Cloud-managed services are gaining prominence as enterprises struggle to govern hybrid, multicloud estates, while outcome-based pricing gains favor for its alignment with measurable business results.

Global IT Outsourcing (ITO) Market Trends and Insights

Cloud-native Application Modernization Demand

Enterprises are re-architecting monolithic systems into microservices, containers, and serverless functions, which opens sizable engagements for platform engineering, Kubernetes orchestration, and event-driven design. Providers increasingly deliver outcome-based contracts that guarantee performance, cost targets, and scalability rather than billing for effort, particularly in highly regulated verticals such as financial services and healthcare where compliance adds complexity. Cultural change management complements the technical shift, and external partners frequently guide agile processes that internal teams cannot easily instill.

GenAI-enabled Service-desk Automation

Generative AI is cutting Level 1 ticket volumes by up to 40% and trimming mean-time-to-resolution by 25% through intelligent routing and self-healing scripts. Virtual assistants now grasp context across multiple systems, drive personalized responses, and predict incidents before users notice disruption. Providers must, however, pair automation with human oversight for complex security issues that demand contextual judgment.

Escalating IP-theft and Ransomware Insurance Costs

Increasing cyber incidents raise premiums and narrow coverage, forcing enterprises to add encryption, access monitoring, and segregated development zones that inflate project costs EY. Buyers now demand providers carry higher insurance limits and submit to regular penetration tests, a hurdle that disadvantages smaller vendors and fuels consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Integration of AI and Automation in DevOps Outsourcing

- Talent-scarcity in Cybersecurity and Observability

- Rising Geopolitical Tensions Disrupting Offshore Delivery Centers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Infrastructure outsourcing commanded 45.05% of the IT outsourcing market in 2025 due to enterprises' reliance on resilient data center operations that need continuous monitoring and regulatory compliance. Cloud-managed services, however, are pacing the field with a 3.44% CAGR as organizations confront the complexity of hybrid estates spanning AWS, Azure, Google Cloud, and private environments. Providers now bundle unified management platforms that sequence workloads by cost, latency, and compliance preferences, challenging the boundaries between traditional infrastructure management and emerging multicloud orchestration.

Demand for application development and maintenance is being reshaped by low-code and AI-assisted development, pushing vendors to differentiate through domain knowledge and integration expertise. Edge computing and AI model lifecycle services sit in the "Others" bucket and represent nascent yet high-margin opportunities. As cloud adoption rises, incumbents pivot to automated site-reliability-engineering services that deliver guaranteed service-level objectives using AI-driven self-healing, thereby protecting infrastructure revenue streams against price compression.

Large enterprises retained 67.25% of spending in 2025 as their complex legacy estates require deep architectural know-how, yet SMEs are expanding faster at a 3.96% CAGR. Outcome-based contracts resonate with smaller firms because they align IT spending to tangible business outcomes instead of headcount. Cloud-native vendors lower entry barriers with self-service portals and automated provisioning, giving SMEs on-demand access to AI, analytics, and cybersecurity capabilities once exclusive to Fortune 500 budgets. This democratization of technology widens the total addressable IT outsourcing market and pressures established providers to create modular, standardized offerings that scale down economically without compromising margin.

IT Outsourcing (ITO) Market is Segmented by Service Type (Infrastructure Outsourcing, Application Development and Maintenance, and More), Organization Size (SMEs and Large Enterprises), Sourcing Location (On-Shore, Near-Shore, and More), End-User Industry (BFSI, Healthcare and Life-Sciences, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 24.12% share confirms its status as the prime adopter of AI and cloud modernization initiatives that demand seasoned providers. United States enterprises are renegotiating legacy contracts toward outcome-based terms that stipulate cost-per-transaction or revenue uplift metrics, reducing labor-arbitrage exposure. Canadian firms prioritize zero-trust security frameworks and sovereign cloud instances to comply with stringent privacy acts. Mexican nearshore centers expand agile pods and DevOps capabilities, reducing project latency and enhancing cultural alignment for US clients.

Asia-Pacific's 3.66% CAGR stems from India's continued dominance and rising contributions from ASEAN economies. Vietnam, Indonesia, and Malaysia are nurturing engineering talent pipelines through government incentives and academic partnerships, positioning themselves as secondary hubs for application development and testing. Japan and South Korea outsource next-generation network operations and edge-cloud orchestration to compensate for local workforce gaps, and Australia increases demand for managed cybersecurity and cloud FinOps services.

Europe combines stringent data-protection mandates with an appetite for digital sovereignty. Local providers form alliances with hyperscalers to launch region-specific sovereign cloud zones. Germany, France, and the Netherlands drive sectoral cloud migration while insisting on in-country data processing. The United Kingdom, despite Brexit, remains a hub for financial-services outsourcing, emphasizing resilience testing and operational-risk controls. Eastern Europe's software-engineering clusters offer high-end R&D outsourcing but navigate geopolitical uncertainty through diversification agreements with Western European clients.

- IBM Corporation

- Tata Consultancy Services

- Infosys Ltd

- Cognizant Technology Solutions

- Wipro Ltd

- HCLTech

- Capgemini SE

- DXC Technology

- NTT Data Corporation

- Atos SE

- CGI Inc.

- Tech Mahindra

- EPAM Systems

- LTI Mindtree

- Globant

- Endava plc

- Softtek

- Andela Inc.

- Persistent Systems

- Accenture plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-native application modernisation demand

- 4.2.2 GenAI-enabled service-desk automation

- 4.2.3 Integration of AI and automation in DevOps outsourcing

- 4.2.4 Talent-scarcity in cybersecurity and observability

- 4.2.5 Rise of sovereign-cloud and data-residency mandates

- 4.2.6 Vendor shift to outcome-based pricing models

- 4.3 Market Restraints

- 4.3.1 Escalating IP-theft and ransomware insurance costs

- 4.3.2 Rising geopolitical tensions disrupting offshore delivery centers

- 4.3.3 Volatility in hyperscaler egress pricing

- 4.3.4 AI-enabled code-generation reducing outsourcing scope

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Assesment of Macroeconomic Factors on the market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Infrastructure Outsourcing

- 5.1.2 Application Development and Maintenance

- 5.1.3 Cloud-Managed Services

- 5.1.4 Others

- 5.2 By Organization Size

- 5.2.1 Small and Medium Enterprises

- 5.2.2 Large Enterprises

- 5.3 By Sourcing Location

- 5.3.1 On-shore

- 5.3.2 Near-shore

- 5.3.3 Off-shore

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life-Sciences

- 5.4.3 Media and Telecommunications

- 5.4.4 Retail and E-commerce

- 5.4.5 Manufacturing

- 5.4.6 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Tata Consultancy Services

- 6.4.3 Infosys Ltd

- 6.4.4 Cognizant Technology Solutions

- 6.4.5 Wipro Ltd

- 6.4.6 HCLTech

- 6.4.7 Capgemini SE

- 6.4.8 DXC Technology

- 6.4.9 NTT Data Corporation

- 6.4.10 Atos SE

- 6.4.11 CGI Inc.

- 6.4.12 Tech Mahindra

- 6.4.13 EPAM Systems

- 6.4.14 LTI Mindtree

- 6.4.15 Globant

- 6.4.16 Endava plc

- 6.4.17 Softtek

- 6.4.18 Andela Inc.

- 6.4.19 Persistent Systems

- 6.4.20 Accenture plc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2026年全球IT外包市场报告

2026年全球IT外包市场报告 软体外包市场规模、份额和成长分析:按服务类型、交付模式、客户规模、应用、产业和地区划分-2026年至2033年产业预测

软体外包市场规模、份额和成长分析:按服务类型、交付模式、客户规模、应用、产业和地区划分-2026年至2033年产业预测 2025 年至 2033 年 IT 外包市场规模、份额、趋势及预测(按服务模式、组织规模、最终用户和地区)

2025 年至 2033 年 IT 外包市场规模、份额、趋势及预测(按服务模式、组织规模、最终用户和地区)