|

市场调查报告书

商品编码

1910929

资讯揭露管理(DM)-市场占有率分析、产业趋势与统计、成长预测(2026-2031)Disclosure Management (DM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

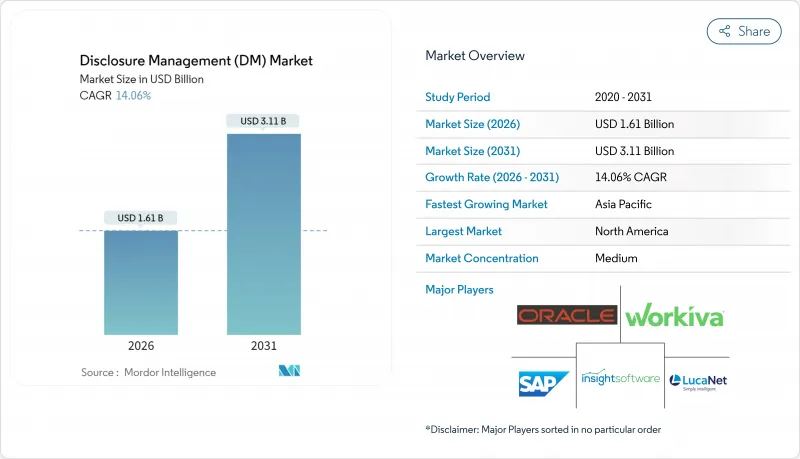

2025 年资讯揭露管理 (DM) 市场价值为 14.1 亿美元,预计到 2031 年将达到 31.1 亿美元,高于 2026 年的 16.1 亿美元。

预测期(2026-2031 年)的复合年增长率预计为 14.06%。

从在线连续XBRL 义务到 ESG 报告规则,企业正在加速采用自动化合规平台,以应对日益增多的多司法管辖区法规。随着财务团队寻求端到端管理、更快的周期和更强大的审核追踪,结合结构化资料标记和叙述生成的整合解决方案正在取代单一工具。云端技术的成熟、基于人工智慧的异常检测以及尊重资料主权要求的混合架构进一步推动了市场需求,而投资者对永续性指标日益严格的审查也巩固了 ESG 模组作为必备功能集的地位。

全球资讯揭露管理(DM)市场趋势与洞察

多表格、多司法管辖区的文件提交使合规工作变得复杂。

监管机构正在扩大机器可读揭露的范围。美国证券交易委员会 (SEC) 要求自 2024 年 7 月起以在线连续XBRL 格式提交网路安全相关资料,这推动了标籤细分,并迫使发行人对其提交工作流程进行现代化改造。同时,欧洲 ESEF 框架要求提交基于 XHTML 的年度报告,亚太地区的监管机构也在製定各自的分类标准实施计画。跨国公司现在需要同时应对不同的方案,这推动了对能够实现资料模型协调、分类标准更新管理以及从单一来源发布资讯的平台的需求。 MiCAR 的加密货币白皮书规则将于 2025 年 12 月生效,该规则将结构化报告扩展到新的资产类别,并表明监管机构对数位化提交的长期承诺。

监管机构强制要求在线连续XBRL 和即时报告

在线连续XBRL 弥合了人类可读的 HTML 和机器可读的 XBRL 之间的鸿沟,使演算法能够在资料提交的瞬间进行分析。欧洲证券及市场管理局 (ESMA) 于 2024 年 8 月发布了 ESRS Set 1 分类标准,实现了机器可读的 ESG 声明,投资者可以大规模地进行基准测试。美国证券交易委员会 (SEC) 的 EDGAR Next 专案将于 2025 年 9 月前完成申报者向个人多因素身分验证帐户的过渡,这凸显了监管机构对资料完整性和网路安全的承诺。金融机构将从标准化标籤和近乎即时的访问中获益匪浅,从而降低审核成本并加快分析速度。

全球/区域分类标准和更新方面的差异

儘管国际财务报告准则(IFRS)提供了一个通用的基础,但区域性差异导致了相容性问题。欧盟的ESRS标籤与美国证券交易委员会(SEC)的美国通用会计准则(US GAAP)扩展有所不同,日本正在建立基于ISSB的分类体系,但标籤结构上的差异仍然存在。 SEC指出,2022年至2024年间,自订标籤的使用量增加,显示发行人难以将其独特的揭露资讯对应到标准要素。供应商必须维护并行的模式库,这增加了工程开销并延缓了发布週期。跨国公司面临每季重新标记标籤的成本,阻碍了平台迁移的加速。

细分市场分析

到2025年,软体凭藉其整合的标籤、工作流程和分析功能,仍将占据资讯揭露管理(DM)市场70.68%的份额。然而,随着企业寻求咨询、实施和管理服务的专业知识以因应监管变化,服务领域正以15.74%的复合年增长率快速成长。专业服务合作伙伴将分类更新整合到平台配置中,并协调财务、法律和IT团队之间的变更管理。管理服务模式对人手不足的中型申报企业极具吸引力,因为它提供与申报週期挂钩的可预测订阅费用。因此,预计到2031年,业务收益将与软体收入差距缩小,从而重塑供应商的经济模式,使其围绕着基本契约。

服务领域的快速成长标誌着结构性转变,即转型为「合规即服务」模式。服务供应商利用共用的卓越中心在客户间分摊监管监控成本,而客户则将XBRL分类映射和ESG重要性范围界定等专业技能外包。人工智慧驱动的服务台现在可以产生解释性文件并自动解决检验错误,从而提高生产力和利润率。这种营运模式加强了供应商与客户之间的联繫。外包揭露工作流程增加了转换成本,从而确保了持续的收入来源,并提高了整个揭露管理(DM)市场的韧性。

预计到2025年,云端采用将占总营收的63.64%,年增率达16.78%,印证了企业对弹性运算、自动更新和协作审查的偏好。 SaaS供应商提供隔夜分类更新,无需本地打补丁即可保持提交合规性。自动扩充功能可应对提交高峰週的负载,而整合的电子签章和审核日誌则简化了身分验证流程。虽然本地工作负载仍集中在银行和国防等高度监管的行业,但将敏感资料保留在本地节点上,同时将处理结果发送到公共云端门户的混合部署模式正日益普及。

云端主权问题促使多区域架构的出现,这些架构采用专用加密金钥和客户管理的硬体安全模组 (HSM)。领先的云端服务供应商推出欧盟专用主权云端区域,使机构能够满足 Schrems II 迁移法规的要求。 Workiva 的多租户 SaaS 设计支援跨团队协作,同时该公司也为处理敏感资讯揭露的政府机构推出了单一租户政府专用云端选项。这些综合增强功能巩固了云端作为未来部署的预设选择的地位,并强化了其作为资讯揭露管理 (DM) 市场成长引擎的作用。

区域分析

北美地区在2025年维持了33.68%的收入占比,这得益于美国证券交易委员会(SEC)积极推动XBRL在线连续和网路安全相关文件的提交。美国发行人正在利用自动化平台,透过多因素身份验证管理EDGAR Next登录,并将文件标籤与不断更新的GAAP同步。加拿大监管机构正在与美国分类标准保持一致,而墨西哥证券委员会正在为大型企业实施和测试XBRL模板。凭藉着高度成熟的云端技术和丰富的XBRL人才,该地区已成为人工智慧驱动的叙事生成和异常检测引擎创新的试验场。

在《企业永续发展报告指令》(CSRD) 和《欧洲永续发展报告架构》(ESEF) 文件打包要求的推动下,欧洲的永续发展报告业务稳步扩张。目前已有超过 5 万家公司受 CSRD 约束,这导致双重重要性评估和范围 3 数据汇总的处理能力需求呈指数级增长。欧洲证券及市场管理局 (ESMA) 发布的 ESRS Set 1 分类法为永续发展报告建立了通用的数位语言,从而实现了跨境可比性。资料主权要求正在推动混合架构的发展,而主权云端计画则使发行人能够在欧盟境内保留个人资料,同时利用 SaaS 资讯揭露引擎提高透明度。

亚太地区预计将以16.92%的复合年增长率实现最快成长,这主要得益于监管机构对其申报制度的现代化。日本针对大型股的强制性ESG规则以及新加坡的人工智慧驱动型监管报告沙盒正在推动云端平台的早期应用。中国已在其科创板申报中启动ESG指标的测试,而印度不断增长的上市公司数量也推动了对低成本标籤工具的需求。澳洲和韩国正在不断完善其气候风险揭露模板,为跨境平台拓展了机会。一旦资料居住要求得到解决,该地区对行动优先用户体验和订阅定价模式的需求将加速云端平台的普及。

其他福利

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 多表格、多司法管辖区备案,合规复杂性日益增加

- 监管机构强制要求在线连续XBRL 和即时报告

- 投资者对ESG/永续性透明度的需求

- 自动化对于缩短发现週期时间和减少人为错误至关重要。

- 透过云端原生报表即服务平台,降低整体拥有成本 (TCO)

- 人工智慧驱动的叙事生成和异常检测工具

- 市场限制

- 全球/区域分类标准的变化和更新

- 云端采用中的网路安全和资料主权问题

- 缺乏专门从事资讯揭露工作的财务人员

- 从传统 Excel/ERP 插件转换过来成本很高

- 监管环境

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 价值链分析

- 投资分析

第五章 市场规模与成长预测

- 按组件

- 软体

- 独立揭露软体

- 整合CPM/ERP模组

- 服务

- 专业(实施咨询)

- 管理服务/业务流程外包

- 软体

- 按部署模式

- 本地部署

- 云

- 杂交种

- 按最终用户公司规模划分

- 大公司

- 小型企业

- 透过使用

- 法规和税务申报

- 财务合併与结算

- 内部和外部财务报告

- 环境、社会及公司治理(ESG)及永续发展报告

- 按最终用户行业划分

- BFSI

- 资讯科技和电信

- 医疗保健和生命科学

- 零售与电子商务

- 製造业

- 能源公共产业

- 政府和公共部门

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲和纽西兰

- 亚太其他地区

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- SAP SE

- Oracle Corporation

- Workiva Inc.

- insightsoftware(包括 Certent)

- LucaNet AG

- DataTracks Services Ltd.

- Wolters Kluwer NV(CCH Tagetik)

- CoreFiling Ltd.

- Trintech Inc.

- IRIS Business Services Ltd.(IRIS Carbon)

- Donnelley Financial Solutions(DFIN)

- OCR Services Inc.

- BlackLine Inc.

- Fluence Technologies

- Sturnis365

- Certinia Inc.

- Deloitte(Disclosure Insight)

- PwC Workbench

- EY Canvas

- KPMG Clara

第七章 市场机会与未来展望

The Disclosure Management market was valued at USD 1.41 billion in 2025 and estimated to grow from USD 1.61 billion in 2026 to reach USD 3.11 billion by 2031, at a CAGR of 14.06% during the forecast period (2026-2031).

Enterprises are accelerating the adoption of automated compliance platforms to cope with mounting multi-jurisdictional regulations, from inline XBRL mandates to ESG reporting rules. Integrated solutions that combine structured data tagging with narrative generation are overtaking point tools as finance teams seek end-to-end control, lower cycle times, and stronger audit trails. Cloud maturity, AI-based anomaly detection, and hybrid architectures that respect data-sovereignty requirements further propel demand, while investor scrutiny of sustainability metrics cements ESG modules as a must-have feature set.

Global Disclosure Management (DM) Market Trends and Insights

Rising Compliance Complexity Across Multi-Format, Multi-Jurisdiction Filings

Regulators are widening the scope of machine-readable disclosures. The SEC's inclusion of cybersecurity exhibits in inline XBRL from July 2024 heightened tagging granularity and pushed issuers to modernize filing workflows. Simultaneously, Europe's ESEF framework demands XHTML-based annual reports, while Asia-Pacific regulators establish their own taxonomy timelines. Multinationals now juggle divergent schemes, prompting demand for platforms that harmonize data models, manage taxonomy updates and enable single-source publishing. Crypto-asset white-paper rules under MiCAR, effective December 2025, extend structured reporting to new asset classes and illustrate regulators' long-term commitment to digital filings.

Mandates for Inline XBRL and Real-Time Reporting by Regulators

Inline XBRL collapses the historical gap between human-readable HTML and machine-readable XBRL, letting algorithms parse data the instant it is filed. ESMA's ESRS Set 1 Taxonomy, published August 2024, enables machine-readable ESG statements that investors can benchmark at scale. The SEC's EDGAR Next program, which transitions filers to individual multifactor-authenticated accounts by September 2025, underscores regulators' drive for data integrity and cybersecurity. Financial institutions gain most, trimming audit fees and accelerating analytics thanks to standardized tags and near-real-time access.

Conflicting Global / Regional Taxonomy Standards and Updates

While IFRS offers a common baseline, regional overlays spawn incompatibilities. EU ESRS tags differ from SEC U.S. GAAP extensions, and Japan is building an ISSB-based taxonomy that still diverges in label structure. The SEC highlighted rising custom tag rates between 2022-2024 as issuers struggled to map unique disclosures onto standard elements. Vendors must maintain parallel schema libraries, inflating engineering overhead and slowing release cycles. Multinationals face re-tagging costs each quarter, dampening rapid platform migrations.

Other drivers and restraints analyzed in the detailed report include:

- Demand for ESG / Sustainability Transparency from Investors

- Automation Needs to Reduce Disclosure Cycle-Time and Manual Errors

- Cyber-Security and Data-Sovereignty Concerns in Cloud Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software retained 70.68% of the Disclosure Management market in 2025 by bundling tagging, workflow and analytics in unified suites. Yet the Services segment is racing ahead at a 15.74% CAGR as enterprises seek advisory, implementation and managed-service expertise to keep pace with rule changes. Professional-service partners translate taxonomy updates into platform configurations and orchestrate change-management across finance, legal and IT teams. The managed-service model appeals to mid-sized filers that lack headcount and want predictable subscription fees tied to filing cycles. As a result, Services revenue is forecast to close a portion of the gap with Software by 2031, reshaping vendor economics around outcome-based engagements.

The surge in Services illustrates a structural shift toward "compliance-as-a-service." Providers leverage shared centers of excellence to spread regulatory surveillance costs across clients, while customers offload niche skill-sets such as XBRL taxonomy mapping or ESG materiality scoping. AI-enabled service desks now draft narrative sections and auto-resolve validation errors, raising productivity and margins. This operating model reinforces vendor-customer stickiness: once disclosure workflows are outsourced, switching costs rise, which in turn anchors recurring revenue streams that improve overall Disclosure Management market resilience.

Cloud deployments accounted for 63.64% revenue in 2025 and are forecast to grow 16.78% annually, underscoring enterprises' preference for elastic compute, automated updates and collaborative review. SaaS vendors ship taxonomy refreshes overnight, ensuring filings remain compliant without local patching. Automated scaling accommodates peak filing-week loads, while integrated e-signatures and audit logs simplify attestation. Remaining on-premise workloads cluster in heavily regulated verticals such as banking and defense, yet hybrid deployments that keep sensitive data on local nodes while piping rendered outputs to public-cloud portals are gathering momentum.

Cloud sovereignty concerns encourage multi-region architectures with dedicated encryption keys and customer-controlled HSMs. Major providers launched EU-specific sovereign-cloud zones in 2024, allowing institutions to satisfy Schrems II transfer rules. Workiva's multi-tenant SaaS design enables cross-team co-authoring, but the firm also introduced single-tenant government-cloud options for agencies handling classified disclosures. Collectively, these enhancements reinforce cloud as the default path for future implementations and cement its role as the Disclosure Management market's growth engine.

The Disclosure Management Market Report is Segmented by Component (Software, Services), Deployment Model (On-Premises, Cloud, Hybrid), End-User Enterprise Size (Large Enterprises, Smes), Application (Regulatory and Tax Filing, Financial Consolidation and Close, and More), End-User Industry (BFSI, IT and Telecom, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintained 33.68% of 2025 revenue, underpinned by the SEC's proactive stance on inline XBRL and cybersecurity exhibits. U.S. issuers rely on automated platforms to manage multifactor EDGAR Next logins and to synch exhibit tagging with evolving GAAP updates. Canadian regulators are aligning with U.S. taxonomy schedules, while Mexico's securities commission pilots XBRL templates for large caps. High cloud maturity and a deep bench of XBRL talent make the region an innovation laboratory for AI-driven narrative generation and anomaly detection engines.

Europe demonstrated steady expansion on the back of CSRD obligations and ESEF file-package requirements. More than 50,000 companies fall under CSRD scope, driving surge-capacity needs for double materiality and Scope 3 data aggregation. ESMA's release of the ESRS Set 1 taxonomy built a common digital language for sustainability statements, enabling cross-country comparability. Data-sovereignty mandates boost hybrid architectures; sovereign-cloud initiatives let issuers keep personal data within EU borders while using SaaS disclosure engines for rendering.

Asia-Pacific delivered the fastest 16.92% CAGR outlook as regulators modernize filing regimes. Japan's mandatory ESG rules for large caps and Singapore's AI-powered regulatory reporting sandbox spur early uptake of cloud platforms. China is trialing ESG indicators within its STAR Market filings, while India's growing public-company base pushes demand for low-cost tagging tools. Australia and South Korea refine climate-risk templates, widening cross-border platform opportunities. Regional appetite for mobile-first user experiences and subscription pricing accelerates cloud adoption once data-residency hurdles are addressed.

- SAP SE

- Oracle Corporation

- Workiva Inc.

- insightsoftware (incl. Certent)

- LucaNet AG

- DataTracks Services Ltd.

- Wolters Kluwer N.V. (CCH Tagetik)

- CoreFiling Ltd.

- Trintech Inc.

- IRIS Business Services Ltd. (IRIS Carbon)

- Donnelley Financial Solutions (DFIN)

- OCR Services Inc.

- BlackLine Inc.

- Fluence Technologies

- Sturnis365

- Certinia Inc.

- Deloitte (Disclosure Insight)

- PwC Workbench

- EY Canvas

- KPMG Clara

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising compliance complexity across multi-format, multi-jurisdiction filings

- 4.2.2 Mandates for Inline XBRL and real-time reporting by regulators

- 4.2.3 Demand for ESG/Sustainability transparency from investors

- 4.2.4 Automation needs to reduce disclosure cycle-time and manual errors

- 4.2.5 Cloud-native "report-as-a-service" platforms lowering TCO

- 4.2.6 AI-driven narrative generation and anomaly detection tools

- 4.3 Market Restraints

- 4.3.1 Conflicting global/regional taxonomy standards and updates

- 4.3.2 Cyber-security and data-sovereignty concerns in cloud adoption

- 4.3.3 Shortage of disclosure-specialised finance talent

- 4.3.4 High switching cost from legacy Excel/ERP add-ins

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Value Chain Analysis

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Stand-alone Disclosure Software

- 5.1.1.2 Integrated CPM/ERP Modules

- 5.1.2 Services

- 5.1.2.1 Professional (Implementation, Consulting)

- 5.1.2.2 Managed / BPO

- 5.1.1 Software

- 5.2 By Deployment Model

- 5.2.1 On-premises

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By End-user Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Regulatory and Tax Filing

- 5.4.2 Financial Consolidation and Close

- 5.4.3 Internal and External Financial Reporting

- 5.4.4 ESG and Sustainability Reporting

- 5.5 By End-user Industry

- 5.5.1 BFSI

- 5.5.2 IT and Telecom

- 5.5.3 Healthcare and Life Sciences

- 5.5.4 Retail and E-commerce

- 5.5.5 Manufacturing

- 5.5.6 Energy and Utilities

- 5.5.7 Government and Public Sector

- 5.5.8 Other End-user Industry

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia Pacific

- 5.6.4 Middle East

- 5.6.4.1 United Arab Emirates

- 5.6.4.2 Saudi Arabia

- 5.6.4.3 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Nigeria

- 5.6.5.3 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Workiva Inc.

- 6.4.4 insightsoftware (incl. Certent)

- 6.4.5 LucaNet AG

- 6.4.6 DataTracks Services Ltd.

- 6.4.7 Wolters Kluwer N.V. (CCH Tagetik)

- 6.4.8 CoreFiling Ltd.

- 6.4.9 Trintech Inc.

- 6.4.10 IRIS Business Services Ltd. (IRIS Carbon)

- 6.4.11 Donnelley Financial Solutions (DFIN)

- 6.4.12 OCR Services Inc.

- 6.4.13 BlackLine Inc.

- 6.4.14 Fluence Technologies

- 6.4.15 Sturnis365

- 6.4.16 Certinia Inc.

- 6.4.17 Deloitte (Disclosure Insight)

- 6.4.18 PwC Workbench

- 6.4.19 EY Canvas

- 6.4.20 KPMG Clara

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

资讯揭露管理市场-全球产业规模、份额、趋势、机会和预测(按组件、按部署模式、按行业垂直、按地区和竞争细分,2020-2030 年预测)

资讯揭露管理市场-全球产业规模、份额、趋势、机会和预测(按组件、按部署模式、按行业垂直、按地区和竞争细分,2020-2030 年预测) 全球资讯揭露管理市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年)

全球资讯揭露管理市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年) 资讯揭露管理市场(按服务提供、组织规模、部署模式、应用程式和最终用户产业)—2025 年至 2030 年全球预测

资讯揭露管理市场(按服务提供、组织规模、部署模式、应用程式和最终用户产业)—2025 年至 2030 年全球预测 美国资讯揭露管理市场规模、份额、趋势分析报告:按组件、业务功能、部署、公司规模、最终用途、细分市场预测,2025 年至 2033 年资讯揭露管理市场规模、份额、趋势分析报告:按组件、业务功能、部署、公司规模、最终用途、地区、细分市场预测,2025 年至 2033 年

美国资讯揭露管理市场规模、份额、趋势分析报告:按组件、业务功能、部署、公司规模、最终用途、细分市场预测,2025 年至 2033 年资讯揭露管理市场规模、份额、趋势分析报告:按组件、业务功能、部署、公司规模、最终用途、地区、细分市场预测,2025 年至 2033 年