|

市场调查报告书

商品编码

1911394

药物喷雾干燥:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Pharmaceutical Spray Drying - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

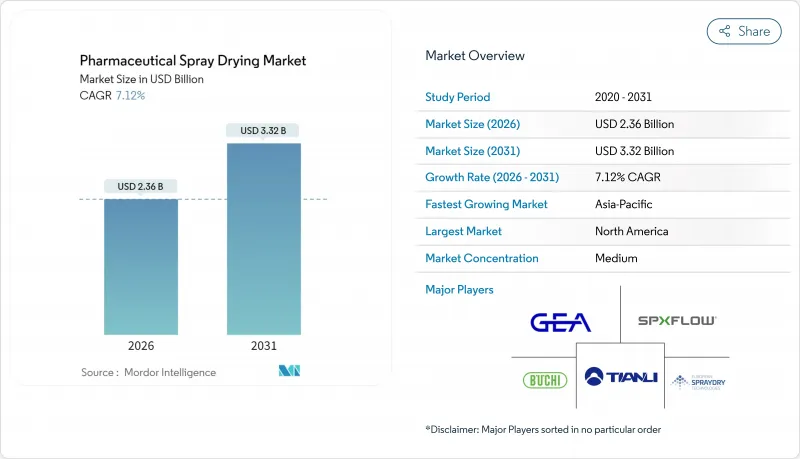

2025 年,医药喷雾干燥市场价值为 22 亿美元,预计从 2026 年的 23.6 亿美元成长到 2031 年的 33.2 亿美元,在预测期(2026-2031 年)内,复合年增长率为 7.12%。

这一发展势头使药物喷雾干燥市场成为现代药物研发策略的核心驱动力,这些策略优先考虑提高药物溶解度、加快生物利用度和实现可扩展的连续流生产。推动成长的因素包括:有利的监管政策、对先进固体分散体日益增长的需求,以及合约研发生产机构 (CDMO) 向整合颗粒工程服务的显着转变。设备供应商正在整合即时分析和先进的自动化技术,而生物製药开发商则利用这些平台来缩短小分子原料药、疫苗、生物製药和吸入疗法的研发週期。永续性需求、溶剂减量要求以及不断提高的能源效率目标,进一步加速了闭合迴路和熔融分散系统的应用,巩固了药物喷雾干燥市场作为下一代治疗药物首选生产途径的地位。

全球製药喷雾干燥市场趋势及洞察

提高药物溶解度的需求日益增长

约40%的在开发平臺水溶性较差,因此喷雾干燥无定形固体分散体对于释放其治疗潜力至关重要。临床试验表明,该方法可将灰黄霉素的溶出时间从21.5分钟缩短至8.5分钟,生物利用度可望提高三倍。共聚维酮和羟丙基甲基纤维素基质可维持胃肠道液中的过饱和状态,而乙酸处理可使弱碱的溶解度提高10倍,同时保持相当的体内表现。这些技术的进步持续推动药物喷雾干燥市场的强劲需求。

药品製剂服务外包增加

製药业对专业CDMO的依赖程度日益加深。 Catalent与赛诺菲活性成分解决方案公司的合作确保了其能够获得Niro PSD2/PSD4干燥设备,从而在无需大量资本投入的情况下实现快速规模化生产。 Hovione的ViSync业务将细胞和基因技术与颗粒工程相结合,标誌着CDMO正式进军治疗方法多元化。随着连续加工技术的普及,外包降低了验证风险,并加快了监管申报速度,从而推动了药物喷雾干燥市场的成长。

高昂的初始资本投资和营运成本

安装製药级喷雾干燥设备的成本在200万美元至1000万美元之间,其中包括高效能空气过滤器(HEPA过滤器)、随线分析和10万级洁净室。年消费量可达每吨2500至4000千瓦时,从而推高营运预算。此外,维护和GMP认证还会增加20%至25%的经常性间接成本。诸如BUCHI的S-300等提高产量的技术创新可以部分抵消这些成本。然而,中小型赞助商通常选择与合约研发生产机构(CDMO)合作,在维持製药喷雾干燥市场产能的同时,减少直接设备投资。

细分市场分析

预计到2025年,辅料生产将占总收入的42.85%,这充分体现了喷雾干燥技术在生产具有流动性、可压缩性和直接压片性的粉末方面的优势,从而提高了片剂生产的效率。兼具崩坏和黏合性的多功能辅料可减少配方步骤,并提高生产柔软性。生物利用度增强应用预计将以9.05%的复合年增长率成长,这反映了业界对利用具有治疗价值但溶解度低的分子的关注。

掩味、缓释和包封仍然是重要的细分领域。罗盖特公司于2024年收购IFF Pharma Solutions,凸显了製剂创新在策略上的重要性,它将聚合物科学与喷雾干燥技术相结合,以应对不断变化的给药挑战。这些应用领域的趋势表明,药物喷雾干燥市场将持续扩张。

到2025年,小分子原料药将占总收入的47.10%。各公司正在采用这项技术将结晶质活性成分转化为无定形形式,确保快速溶解和体内持续暴露。疫苗,包括mRNA/LNP製剂,将成为成长最快的类别,复合年增长率将达到9.62%。疫情期间的投资验证了常温保存的喷雾干燥吸入疫苗的有效性,使其能够摆脱冷藏链的限制,实现全球分销。

生物製药正受益于能够保留其三级结构的温和干燥技术,其中单株抗体的粉末回收率超过90%,且稳定性指标与冷冻干燥製剂相当。肽类和基因治疗的应用案例日益增多,进一步增强了药物喷雾干燥市场在各个治疗领域的适用性。

区域分析

北美将在2025年继续保持领先地位,市场份额将达到39.85%,这主要得益于其大规模的合约研发生产能力、美国食品药物管理局(FDA)支持创新的态度以及大型製药企业的大规模资本投资。 Catalent公司在肯塔基州工厂投资4,000万美元进行扩建,以及Seran Biosciences公司在佛罗里达州本德市工厂计划2亿美元,都是持续资本投资的例证。

预计到2031年,亚太地区将以8.18%的最高成长速度成长,主要得益于中国、韩国和印度产能的积极扩张。 SK Pharmatech在韩国投资2.6亿美元的工厂体现了与半导体产业同等的投资理念。政府对先进製造技术的支持以及简化的法规结构正在加速本地化应用,为製药喷雾干燥市场的发展提供了强劲动力。

欧洲拥有强大的製造地,在欧盟「地平线计画」的津贴下,相关係统正在不断改进。勃林格殷格翰在希腊投资1.2亿欧元扩建工厂,将整合新型分子的喷雾干燥粉末生产。同时,在世界卫生组织技术转移倡议和各国卫生政策改革的推动下,中东、非洲和南美地区正从依赖进口的地区转型为区域製剂中心。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 提高药物溶解度的需求日益增长

- 药品製剂服务外包增加

- 扩大吸入式和口服薄膜疗法

- 连续加工技术的应用日益广泛

- 对先进药物输送平台的有利监管支持

- 市场限制

- 高昂的初始资本投资和营运成本

- 严格的验证和合规要求

- 喷雾干燥级添加剂供应有限

- 能源强度和永续性问题

- 监管环境

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 透过使用

- 增材製造

- 封装

- 提高生物有效性

- 其他用途

- 依配方类型

- 小分子原料药

- 生物製药和胜肽类

- 疫苗(包括mRNA/LNP)

- 吸入剂

- 其他的

- 喷雾干燥型

- 旋转雾化器

- 喷嘴雾化器

- 流体化床/封闭回路型

- 其他的

- 按尺寸

- 实验室/中试规模

- 商业规模

- 地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 亚太其他地区

- 中东和非洲

- GCC

- 南非

- 其他中东和非洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 市占率分析

- 公司简介

- GEA Group AG

- SPX FLOW Inc.

- Buchi Labortechnik AG

- ProCepT NV

- European SprayDry Technologies

- Shandong Tianli Energy

- Labplant UK

- New AVM Systech

- Advanced Drying Systems

- Lemar Drying Engineering

- Freund-Vector Corp.

- Glatt GmbH

- Fluid Air(Spraying Systems)

- Syntegon Technology

- Spray-Tek Inc.

- Coperion GmbH

- Carrier Vibrating Equipment

- Powder Systems Ltd.

- Innojet GmbH

- Cyclops Spray Drying

第七章 市场机会与未来展望

The pharmaceutical spray drying market was valued at USD 2.20 billion in 2025 and estimated to grow from USD 2.36 billion in 2026 to reach USD 3.32 billion by 2031, at a CAGR of 7.12% during the forecast period (2026-2031).

This momentum positions the pharmaceutical spray drying market size as a core enabler for contemporary drug development strategies that prioritize enhanced solubility, rapid bioavailability, and scalable continuous-flow production. Growth is fueled by supportive regulation, rising demand for advanced solid dispersions, and a clear pivot by contract development and manufacturing organizations (CDMOs) toward integrated particle-engineering services. Equipment suppliers are embedding real-time analytics and advanced automation, while biopharma innovators leverage the platform to shorten development cycles for small-molecule APIs, vaccines, biologics, and inhalable therapies. Sustainability imperatives, solvent-reduction mandates, and heightened energy-efficiency objectives further accelerate adoption of closed-loop and fusion-dispersion systems, reinforcing the pharmaceutical spray drying market as a preferred route for next-generation therapeutics.

Global Pharmaceutical Spray Drying Market Trends and Insights

Growing Demand for Enhanced Drug Solubility

Approximately 40 % of pipeline molecules present low aqueous solubility, making spray-dried amorphous solid dispersions indispensable for recovery of therapeutic potential. Clinically, the method reduced griseofulvin dissolution times from 21.5 minutes to 8.5 minutes, tripling bioavailability improvement prospects. Copovidone and hypromellose matrices sustain supersaturation in gastrointestinal fluids, and acetic-acid aided processing elevates solubility of weak bases tenfold while maintaining equivalent in-vivo performance. Together, these advances sustain robust forward demand for the pharmaceutical spray drying market.

Rising Outsourcing of Pharmaceutical Formulation Services

Pharma's reliance on specialty CDMOs is intensifying. Catalent's collaboration with Sanofi Active Ingredient Solutions secured access to Niro PSD2/PSD4 dryers, enabling rapid scale without significant capital outlay. Hovione's ViSync venture pairs cell-and-gene technologies with particle engineering, illustrating CDMOs' push into modality diversification. As continuous processing skills proliferate, outsourcing mitigates validation risk and accelerates dossier filings, anchoring growth in the pharmaceutical spray drying market.

High Initial Capital Investment and Operating Costs

Pharmaceutical-grade spray dryer installations range from USD 2-10 million inclusive of HEPA filtration, in-line analytics, and Class 100,000 cleanrooms. Annual energy consumption of 2,500-4,000 kWh per ton inflates operating budgets, while maintenance and GMP certification add 20-25 % repeating overhead. Innovations such as BUCHI's S-300, with enhanced yield capture, partially offset these burdens. Nonetheless, smaller sponsors often pivot to CDMOs, reducing direct equipment uptake yet sustaining volumes within the pharmaceutical spray drying market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Inhalable and Oral Thin-Film Therapies

- Increasing Adoption of Continuous Processing Technologies

- Stringent Validation and Compliance Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Excipient production held 42.85 % of 2025 revenue, highlighting spray drying's ability to engineer flowable, compressible, and directly compressible powders that streamline tablet manufacturing. Spray-dried multifunctional excipients with integrated disintegration and binding properties reduce formulation steps, enhancing manufacturing agility. Bioavailability-enhancement applications are forecast to advance at a 9.05 % CAGR, reflecting industry emphasis on unlocking therapeutically valuable but poorly soluble molecules.

Taste-masking, controlled-release, and encapsulation remain vital niches. Roquette's acquisition of IFF Pharma Solutions in 2024 underscores the strategic importance of excipient innovation, combining polymer science with spray-drying know-how to address evolving delivery challenges. Collectively, the application landscape signals sustained expansion of the pharmaceutical spray drying market.

Small-molecule APIs provided 47.10 % of 2025 revenue. Companies deploy the technology to transform crystalline actives into amorphous forms, securing rapid dissolution and consistent in-vivo exposure. Vaccines, including mRNA/LNP formats, represent the fastest-growing category with a projected 9.62 % CAGR. Pandemic-era investments validated room-temperature, spray-dried respirable vaccines that facilitate global distribution without cold chain constraints.

Biologics benefit from gentle drying that preserves tertiary structure, with monoclonal antibodies achieving > 90 % powder recovery and stability metrics comparable to lyophilized alternatives. Peptide and gene-therapy use cases are gaining traction, reinforcing the adaptability of the pharmaceutical spray drying market across therapeutic classes.

The Pharmaceutical Spray Drying Market Report is Segmented by Application (Excipient Production, and More), Formulation Type (Small-Molecule APIs, and More), Spray Dryer Type (Rotary Atomizer, and More), Scale (Laboratory/Pilot and Commercial-Scale), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintained leadership at 39.85 % share in 2025, cemented by substantial CDMO capacity, a pro-innovation FDA stance, and large-scale internal builds from big pharma. Catalent's USD 40 million Kentucky upgrade and Seran BioScience's USD 200 million Bend project illustrate sustained capital deployment.

Asia-Pacific will post the fastest 8.18 % CAGR through 2031, driven by aggressive capacity expansion across China, South Korea, and India. SK pharmteco's USD 260 million South Korean facility exemplifies the region's semiconductor-like investment mentality. Government incentives for advanced manufacturing and simplified regulatory frameworks accelerate local uptake, injecting tailwinds into the pharmaceutical spray drying market.

Europe remains a stalwart manufacturing cluster, adding continuous systems under Horizon Europe grants. Boehringer Ingelheim's EUR 120 million Greek expansion integrates spray-dried powder production for novel molecules. Meanwhile, Middle East & Africa and South America are evolving from import-dependent regions into regional formulation hubs, encouraged by WHO tech-transfer initiatives and domestic healthcare policy reforms.

- GEA Group

- SPX FLOW Inc.

- Buchi Labortechnik AG

- ProCepT NV

- European SprayDry Technologies

- Shandong Tianli Energy

- Labplant UK

- New AVM Systech

- Advanced Drying Systems

- Lemar Drying Engineering

- Freund-Vector Corp.

- Glatt

- Fluid Air (Spraying Systems)

- Syntegon Technology

- Spray-Tek Inc.

- Coperion

- Carrier Vibrating Equipment

- Powder Systems Ltd.

- Innojet GmbH

- Cyclops Spray Drying

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Enhanced Drug Solubility

- 4.2.2 Rising Outsourcing of Pharmaceutical Formulation Services

- 4.2.3 Expansion of Inhalable and Oral Thin-Film Therapies

- 4.2.4 Increasing Adoption of Continuous Processing Technologies

- 4.2.5 Favorable Regulatory Support for Advanced Drug Delivery Platforms

- 4.3 Market Restraints

- 4.3.1 High Initial Capital Investment and Operating Costs

- 4.3.2 Stringent Validation and Compliance Requirements

- 4.3.3 Limited Availability of Spray-Drying-Grade Excipients

- 4.3.4 Energy Intensity and Sustainability Concerns

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Application

- 5.1.1 Excipient Production

- 5.1.2 Encapsulation

- 5.1.3 Enhancing Bioavailability

- 5.1.4 Other Applications

- 5.2 By Formulation Type

- 5.2.1 Small-Molecule APIs

- 5.2.2 Biologics & Peptides

- 5.2.3 Vaccines (Incl. mRNA/LNP)

- 5.2.4 Inhalable Formulations

- 5.2.5 Others

- 5.3 By Spray Dryer Type

- 5.3.1 Rotary Atomizer

- 5.3.2 Nozzle Atomizer

- 5.3.3 Fluidized / Closed-Loop

- 5.3.4 Others

- 5.4 By Scale

- 5.4.1 Laboratory / Pilot

- 5.4.2 Commercial-Scale

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 GEA Group AG

- 6.3.2 SPX FLOW Inc.

- 6.3.3 Buchi Labortechnik AG

- 6.3.4 ProCepT NV

- 6.3.5 European SprayDry Technologies

- 6.3.6 Shandong Tianli Energy

- 6.3.7 Labplant UK

- 6.3.8 New AVM Systech

- 6.3.9 Advanced Drying Systems

- 6.3.10 Lemar Drying Engineering

- 6.3.11 Freund-Vector Corp.

- 6.3.12 Glatt GmbH

- 6.3.13 Fluid Air (Spraying Systems)

- 6.3.14 Syntegon Technology

- 6.3.15 Spray-Tek Inc.

- 6.3.16 Coperion GmbH

- 6.3.17 Carrier Vibrating Equipment

- 6.3.18 Powder Systems Ltd.

- 6.3.19 Innojet GmbH

- 6.3.20 Cyclops Spray Drying

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

2026年全球喷雾干燥设备市场报告

2026年全球喷雾干燥设备市场报告 全球药品喷雾干燥市场:依产品类型、干燥方法、应用、最终用户、国家及地区划分-产业分析、市场规模、份额及未来预测(2025-2032年)

全球药品喷雾干燥市场:依产品类型、干燥方法、应用、最终用户、国家及地区划分-产业分析、市场规模、份额及未来预测(2025-2032年) 喷雾干燥设备市场(按干燥设备类型、最终用户产业、干燥能力、自动化程度和安装类型)—2025-2032 年全球预测油漆烘干机市场按技术、应用、涂料类型和最终用途行业划分-2025-2032年全球预测

喷雾干燥设备市场(按干燥设备类型、最终用户产业、干燥能力、自动化程度和安装类型)—2025-2032 年全球预测油漆烘干机市场按技术、应用、涂料类型和最终用途行业划分-2025-2032年全球预测 喷雾干燥设备市场-全球产业规模、份额、趋势、机会和预测,按类型、按干燥阶段、按流程类型、按应用、按地区和竞争情况细分,2020-2030 年喷雾干燥设备的全球市场:到 2033 年的机会和策略

喷雾干燥设备市场-全球产业规模、份额、趋势、机会和预测,按类型、按干燥阶段、按流程类型、按应用、按地区和竞争情况细分,2020-2030 年喷雾干燥设备的全球市场:到 2033 年的机会和策略