|

市场调查报告书

商品编码

1911446

编码和标记解决方案:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)Coding And Marking Solutions - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

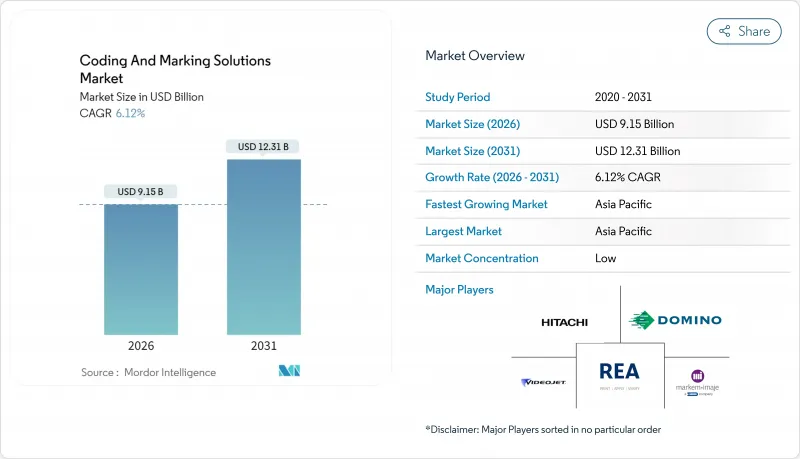

预计到 2026 年,编码和标记解决方案市场价值将达到 91.5 亿美元,从 2025 年的 86.2 亿美元增长到 2031 年的 123.1 亿美元,2026 年至 2031 年的年复合成长率(CAGR)为 6.12%。

对唯一产品识别码、端到端可追溯性和製造过程中更高监管合规性的强劲需求,正推动着这项扩张。日益严格的环境法规加速了从溶剂型油墨转向光纤雷射系统的转变,而支援远端分析和预测性维护的软体平台则重新定义了客户价值提案。药品序列化监管期限、二维条码的广泛应用以及GS1数位连结标准的实施,将推动2030年的关键投资。同时,半导体短缺正在推动印表机控制设备和耗材的重新设计,这加剧了成本压力,同时也为供应商多元化采购开闢了新的市场机会。亚太地区的製造业规模和政策协调使其始终处于产能扩张和升级的前沿,巩固了主导地位。

全球编码和标誌解决方案市场趋势与洞察

生产和包装产业的扩张

新兴市场产能的不断提升,持续推动对整合识别系统的订单。柔性包装的快速普及和产品生命週期的缩短,迫使製造商转向能够适应不同基材和SKU变更且无需停机的印表机。可口可乐的瓶装饮料补充装项目采用GS1数位连结QR码,在部分拉丁美洲市场,补充装饮料的销售额占比超过50%。为了实现这些目标,该公司越来越依赖高通量连续喷墨设备和坚固耐用的雷射编码器,以确保在曲面和可回收表面上的清晰可辨。随着永续性准则的日益普及,注重可重复使用的包装推动了日期、批号和押金退款资讯的印刷量增加。

端到端可追溯性的需求

药品序列化已成为食品、饮料和化妆品製造商降低召回风险和验证产品真伪的典范。 Woolworths在实施GS1 DataMatrix编码后,食品浪费减少了40%。详细的库存可视性已被证明能够提高营运效率。一个将包装标识符与分散式帐本连接起来的区块链试点专案已开始提供即时储存记录,使品牌所有者能够透过可追溯性资讯服务获利。为此,供应商正在将云端连接器和开放API整合到其编码设备中,从而从独立的设备供应商转型为资料利用支援公司。

高昂的初始投资和营运成本

光纤雷射印表机的价格从1万美元到10万美元以上不等,而连续喷墨印表机则需要不断补充墨水,从而推高了总拥有成本。小规模的合约包装商不愿投资利润率低的领域,通常会等到监管机构实施新的标籤规定后再升级。管理服务协议和租赁模式正日益普及,因为它们可以将投资从资本支出转移到可预测的营运成本,但微企业采用这些模式的比例仍然有限。

细分市场分析

预计到2025年,设备收入将占总收入的大部分,这主要得益于工厂持续的多条生产线安装。硬体编码和标记解决方案市场预计将达到49.9亿美元,而服务和软体市场将以6.78%的复合年增长率增长,到2031年将超过21.8亿美元,这主要得益于分析订阅和远端监控仪表板的普及。 VideojetConnect中嵌入的预测性维护模组可通知操作员液位、温度偏差和喷嘴状态,从而减少高达20%的停机时间。备件和耗材采用年度收入模式,色带和墨水的销售额与整体列印量的成长密切相关,从而保障了供应商的盈利。

向基于云端的编码管理套件的转变反映了SKU日益增长的复杂性以及对分散工厂的列印规则进行集中管理的需求。开放的API架构能够与ERP和MES平台无缝集成,简化审核期间的合规性报告。随着工业5.0讨论的不断深入,供应商正将编码设备定位为「融合人工监督和人工智慧辅助决策的协作资产」。

2025年,连续喷墨列印仍占出货量的43.78%,证实了其在高速瓶装和罐装生产线上的多功能性。随着品牌商采用耐磨损、防潮的无溶剂永久性标记,雷射打码机的市占率不断扩大。 Markem-Imaje公司的SmartLase F500每分钟可对多达2000个铝罐进行打码,这项性能标准降低了饮料製造商采用雷射技术的门槛。光纤雷射打码机无需耗材,并减少了VOC排放,从而巩固了其在环境法规严格的地区的地位。

热感喷墨和按需喷墨系统对于在瓦楞纸箱等多孔材料上进行列印仍然至关重要,而热感印表机则适用于需要以中等速度列印清晰、可变影像的软包装。为了满足预期的需求激增,Epson等组件製造商正在将其印表机头产能提高四倍。该公司在日本新建的工厂是一项价值51亿美元的策略性投资。

区域分析

预计到2025年,亚太地区将占全球营收的33.55%,并继续以6.45%的复合年增长率推动成长。中国的大型快速消费品工厂正在大量安装高速连续喷墨设备,而印度的药品出口商正在维修其生产线以满足印度药品供应链安全局(DSCSA)的进口要求。像DKSH这样的本地分销商正在结合其区域市场知识和Koenig & Bauer的喷码硬件,以加强其在东南亚的售后市场地位。政府为促进智慧工厂而采取的支持措施正在进一步加速硬体和软体的普及应用,并推动喷码单元整合到电子和汽车产业丛集的自动化检测单元中。

北美地区拥有稳定的法规环境,这得益于《药品安全追踪法案》(DSCSA) 和美国食品药物管理局(FDA) 的食品安全法规。随着零售通路全面过渡到二维条码(预计在 2027 年完成),能够以每分钟 1000 个单元以上的速度进行 300 dpi 图形显示的印表机的早期应用正在加速。墨西哥凭藉在美国墨加协定 (USMCA) 下的地理优势,吸引了许多电子产品和白色家电的组装基地。美国零售商对包装薄膜按需喷码机的应用也在稳定成长。

儘管欧洲的雷射喷码机装置量已相当成熟,但其更新换代需求依然强劲,尤其对符合循环经济目标、旨在减少溶剂排放的雷射喷码机的需求更为旺盛。德国原始设备製造商 (OEM) 正在指定使用支援 OPC UA 的喷码机,以便更轻鬆地整合到现有的 PLC 架构中。英国脱欧后,合规要求保持不变,基于 EN 标准的法规仍然有效,这为仓库自动化列印贴标系统的持续投资提供了支援。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 生产和包装产业的扩张

- 端到端可追溯性的需求

- 批次编码的监理要求

- 面向工业4.0的预测性维护

- 朝向无溶剂光纤雷射涂层的转变

- 市场限制

- 高昂的资本和营运成本

- 预印包装替代品的成长

- 印表机控制设备半导体短缺

- 价值/供应链分析

- 监管环境

- 技术展望

- 投资分析

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 透过解决方案

- 装置

- 流体和带状物

- 备用零件

- 服务和软体

- 透过设备技术

- 连续喷墨(CIJ)

- 热感喷墨(TIJ)

- 雷射打码机

- 按需滴注和阀门喷射系统

- 热感

- 透过使用

- 组件识别

- 品牌意识与行销

- 可追溯性和防伪措施

- 合规性和监理编码

- 按最终用户行业划分

- 食品/饮料

- 製药

- 化妆品和个人护理

- 建筑与工业

- 其他行业

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ASEAN

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 奈及利亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Videojet Technologies Inc.

- Domino Printing Sciences plc

- Markem-Imaje Corporation

- Hitachi, Ltd.

- REA Elektronik GmbH

- Linx Printing Technologies Ltd.

- Matthews International Corporation

- Keyence Corporation

- Paul Leibinger GmbH & Co. KG

- Koenig & Bauer Coding GmbH

- Control Print Limited

- ITW FoxJet

- United Barcode Systems SL

- KGK Jet Group

- ID Technology, LLC(ProMach)

- SATO Holdings Corporation

- Danaher Corporation

- Squid Ink Manufacturing, Inc.

- Guangzhou EC-JET Technology Co., Ltd.

- Diagraph Corporation(ITW)

第七章 市场机会与未来展望

The coding and marking solutions market size in 2026 is estimated at USD 9.15 billion, growing from 2025 value of USD 8.62 billion with 2031 projections showing USD 12.31 billion, growing at 6.12% CAGR over 2026-2031.

Robust demand for unique product identifiers, end-to-end traceability and tighter regulatory compliance across manufacturing industries underpins this expansion. Migrating from solvent-based inks to fiber-laser systems is accelerating as environmental regulations tighten, while software-centric platforms that enable remote analytics and predictive maintenance are redefining customer value propositions. Pharmaceutical serialization deadlines, the proliferation of 2D barcodes and the rollout of GS1 Digital Link standards are creating non-discretionary investments through 2030. Meanwhile, semiconductor shortages have prompted redesigns of printer controls and consumables, added cost pressures yet opening white-space opportunities for suppliers with diversified sourcing. Asia-Pacific's manufacturing scale, coupled with policy harmonization, keeps the region at the forefront of capacity expansions and equipment upgrades, consolidating its lead in the coding and marking solutions market.

Global Coding And Marking Solutions Market Trends and Insights

Expansion of production and packaging industry

Capacity additions across emerging markets generate sustained orders for integrated identification systems. Rapid uptake of flexible packaging, coupled with shorter product life cycles, pushes manufacturers toward printers that adapt to multiple substrates and SKU changes without line stoppages. Coca-Cola's refillable bottle program uses GS1 Digital Link-enabled QR codes, and refillable formats now account for more than 50% of sales in select Latin American markets. These objectives drive greater reliance on high-throughput continuous inkjet units and rugged laser coders that preserve legibility on curved or returnable surfaces. As sustainability guidelines take hold, reuse-focused packaging creates incremental print volumes for date, batch and deposit-refund information.

Demand for end-to-end traceability

Pharmaceutical serialization has become a model for food, beverage and cosmetics producers that seek to mitigate recalls and demonstrate authenticity. Woolworths achieved a 40% reduction in food waste after deploying GS1 DataMatrix codes, illustrating the operational gains from granular inventory visibility. Blockchain pilots that connect on-pack identifiers with distributed ledgers are beginning to offer real-time custody records, allowing brand owners to monetize traceability data services. Solution vendors respond by embedding cloud connectors and open APIs into coding hardware, positioning themselves as data enablers rather than stand-alone machine suppliers.

High capital and running costs

Fiber-laser units range from USD 10,000 to over USD 100,000, while continuous inkjet models require a steady supply of make-up fluids that inflate the total cost of ownership. Smaller contract packers hesitate to commit capital in tight-margin categories and often defer upgrades until regulators enforce new labeling rules. Managed service contracts and leasing schemes are gaining popularity because they shift investments from capital expenditure to predictable operating expenses, yet uptake remains modest among micro-enterprises.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory mandates for batch coding

- Industry 4.0-enabled predictive maintenance

- Semiconductor shortages in printer controls

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Equipment generated the bulk of 2025 revenue as factories continued multi-line installations; the coding and marking solutions market size for hardware reached USD 4.99 billion. Services and software, however, posted a 6.78% CAGR and are on track to exceed USD 2.18 billion by 2031 on the back of analytics subscriptions and remote-monitoring dashboards. Predictive-maintenance modules embedded in VideojetConnect alert operators to solvent levels, temperature deviations and nozzle health, cutting downtime by up to 20%. Spares and consumables preserve an annuity-style revenue model, with ribbon and ink sales closely mirroring overall print-volume growth and thereby buttressing vendor profitability.

The shift toward cloud-hosted code-management suites reflects mounting SKU complexity and the need for centralized governance of print rules across dispersed plants. Open API architecture enables seamless exchanges with ERP and MES platforms, simplifying compliance reporting during audits. As Industry 5.0 discussions advance, vendors frame coding devices as collaborative assets that integrate human oversight with AI-assisted decision making.

Continuous inkjet retained 43.78% of 2025 shipments, underscoring its versatility on high-speed bottling and canning lines. The coding and marking solutions market share for laser coders expanded as brands embraced solvent-free, permanent marks that withstand abrasion and moisture. Markem-Imaje's SmartLase F500 engraves up to 2,000 aluminum cans per minute, a performance benchmark that eased laser entry barriers for beverage producers. Fiber-laser coders eliminate consumable costs and reduce VOC emissions, strengthening their position in jurisdictions with rigorous environmental acts.

Thermal inkjet and drop-on-demand systems remain vital in porous applications such as corrugated boxes, while thermal-transfer overprinters cater to flexible packaging that demands crisp variable graphics at moderate speeds. Component makers such as Epson are quadrupling printhead capacity to satisfy anticipated demand spikes; its new plant in Japan embodies USD 5.1 billion in strategic investment.

The Coding and Marking Solutions Market Report is Segmented by Solution (Equipment, Fluids and Ribbons, Spares, Services and Software), Equipment Technology (Continuous Inkjet, Thermal Inkjet and More), Application (Component Identification, Brand Recognition and Marketing, and More), End-User Industry (Food & Beverage, Pharmaceutical, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 33.55% of global revenue in 2025 and continues to lead growth with a 6.45% CAGR. China's large-scale FMCG plants consume fleets of high-speed continuous inkjets, while India's pharmaceutical exporters retrofit lines to satisfy DSCSA import requirements. Local distributors such as DKSH pair regional market knowledge with Koenig & Bauer Coding's hardware, improving aftermarket coverage in Southeast Asia. Government incentives that fund smart-factory upgrades further stimulate hardware and software uptake, embedding coding units into automated inspection cells across electronics and automotive clusters.

North America shows high regulatory stability anchored by DSCSA and FDA food-safety statutes. The looming 2027 deadline for full 2D barcode transition across retail channels spurs early adoption of printers capable of 300 dpi graphics at line speeds above 1,000 units per minute. Mexico leverages USMCA proximity to attract electronics and white-goods assembly, resulting in incremental installations of drop-on-demand coders on packaging films destined for U.S. retailers.

Europe maintains a mature installed base yet demonstrates steady replacement demand, particularly for laser coders aligned with circular-economy objectives to cut solvent emissions. Germany's OEMs specify OPC UA-ready coders, easing their integration into existing PLC architecture. Brexit has not altered United Kingdom compliance expectations, keeping EN-aligned regulations intact and supporting ongoing investments in print-and-apply systems for warehouse automation.

- Videojet Technologies Inc.

- Domino Printing Sciences plc

- Markem-Imaje Corporation

- Hitachi, Ltd.

- REA Elektronik GmbH

- Linx Printing Technologies Ltd.

- Matthews International Corporation

- Keyence Corporation

- Paul Leibinger GmbH & Co. KG

- Koenig & Bauer Coding GmbH

- Control Print Limited

- ITW FoxJet

- United Barcode Systems S.L.

- KGK Jet Group

- ID Technology, LLC (ProMach)

- SATO Holdings Corporation

- Danaher Corporation

- Squid Ink Manufacturing, Inc.

- Guangzhou EC-JET Technology Co., Ltd.

- Diagraph Corporation (ITW)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of production and packaging industry

- 4.2.2 Demand for end-to-end traceability

- 4.2.3 Regulatory mandates for batch coding

- 4.2.4 Industry 4.0-enabled predictive maintenance

- 4.2.5 Shift to solvent-free fiber-laser coding

- 4.3 Market Restraints

- 4.3.1 High capital and running costs

- 4.3.2 Growth of pre-printed packaging alternatives

- 4.3.3 Semiconductor shortages in printer controls

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Investments Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Solution

- 5.1.1 Equipment

- 5.1.2 Fluids and Ribbons

- 5.1.3 Spares

- 5.1.4 Services and Software

- 5.2 By Equipment Technology

- 5.2.1 Continuous Inkjet (CIJ)

- 5.2.2 Thermal Inkjet (TIJ)

- 5.2.3 Laser Coders

- 5.2.4 Drop-on-Demand and Valve Jet

- 5.2.5 Thermal Transfer Overprinting

- 5.3 By Application

- 5.3.1 Component Identification

- 5.3.2 Brand Recognition and Marketing

- 5.3.3 Traceability and Anti-counterfeiting

- 5.3.4 Compliance and Regulatory Coding

- 5.4 By End-user Industry

- 5.4.1 Food and Beverages

- 5.4.2 Pharmaceutical

- 5.4.3 Cosmetics and Personal Care

- 5.4.4 Construction and Industrial

- 5.4.5 Other Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Videojet Technologies Inc.

- 6.4.2 Domino Printing Sciences plc

- 6.4.3 Markem-Imaje Corporation

- 6.4.4 Hitachi, Ltd.

- 6.4.5 REA Elektronik GmbH

- 6.4.6 Linx Printing Technologies Ltd.

- 6.4.7 Matthews International Corporation

- 6.4.8 Keyence Corporation

- 6.4.9 Paul Leibinger GmbH & Co. KG

- 6.4.10 Koenig & Bauer Coding GmbH

- 6.4.11 Control Print Limited

- 6.4.12 ITW FoxJet

- 6.4.13 United Barcode Systems S.L.

- 6.4.14 KGK Jet Group

- 6.4.15 ID Technology, LLC (ProMach)

- 6.4.16 SATO Holdings Corporation

- 6.4.17 Danaher Corporation

- 6.4.18 Squid Ink Manufacturing, Inc.

- 6.4.19 Guangzhou EC-JET Technology Co., Ltd.

- 6.4.20 Diagraph Corporation (ITW)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis

2026年全球骨材配料机市场报告

2026年全球骨材配料机市场报告 编码和标记设备市场:2026-2032年全球市场预测(按技术类型、产品类型、印刷图案、印刷材料、应用和最终用户行业划分)编码与识别市场:2026-2032年全球市场预测(按作业系统、分销管道、最终用户和应用划分)携带式直接零件标记条码扫描器市场:按扫描器技术、连接方式、代码类型和最终用户产业划分-全球预测,2026-2032年全球直接零件标记解决方案市场(按技术、组件、材料、应用和最终用途行业划分)预测(2026-2032 年)

编码和标记设备市场:2026-2032年全球市场预测(按技术类型、产品类型、印刷图案、印刷材料、应用和最终用户行业划分)编码与识别市场:2026-2032年全球市场预测(按作业系统、分销管道、最终用户和应用划分)携带式直接零件标记条码扫描器市场:按扫描器技术、连接方式、代码类型和最终用户产业划分-全球预测,2026-2032年全球直接零件标记解决方案市场(按技术、组件、材料、应用和最终用途行业划分)预测(2026-2032 年) 雷射编码打标设备:全球市占率及排名、总收入及需求预测(2025-2031年)

雷射编码打标设备:全球市占率及排名、总收入及需求预测(2025-2031年) 工业赋码与识别解决方案(2025):按需可变资料需求推动转型

工业赋码与识别解决方案(2025):按需可变资料需求推动转型 2025 年至 2033 年食品和饮料编码和标记设备市场报告(按类型、技术、应用和地区)

2025 年至 2033 年食品和饮料编码和标记设备市场报告(按类型、技术、应用和地区) 全球生成人工智慧编码助理市场

全球生成人工智慧编码助理市场 全球打码和标记设备市场(2025-2029)

全球打码和标记设备市场(2025-2029)